- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Nanocellulose Market Size, Share & Forecast | CAGR 18.4%

Global Nanocellulose Market Size, Share, Growth Analysis By Type (Cellulose Nanocrystals, Cellulose Nanofibrils, Microfibrillated Cellulose, Bacterial Nanocellulose), By Source (Wood Pulp, Cotton Linters, Agricultural Residues, Bacterial Fermentation), By Application (Packaging, Composites, Biomedical, Electronics, Paper & Board), By End-Use Industry, Market Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 0.62 Billion | USD 2.84 Billion | 18.4% | North America, 34.2% |

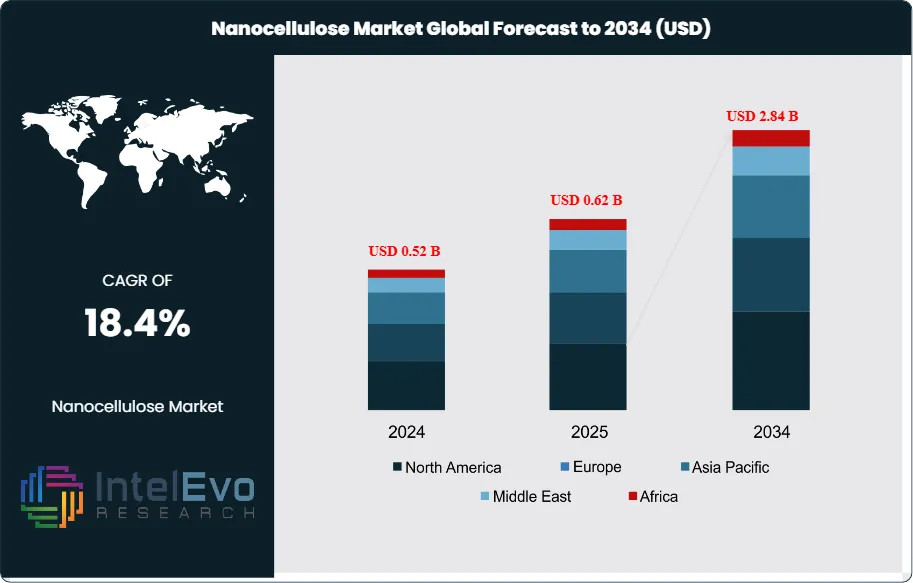

The Nanocellulose Market was valued at approximately USD 0.52 Billion in 2024 and reached USD 0.62 Billion in 2025. The market is projected to grow to USD 2.84 Billion by 2034, expanding at a CAGR of 18.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 2.22 Billion over the analysis period, driven by surging demand for bio-based and renewable nanomaterials across packaging, composites, biomedical, personal care, and coating applications where nanocellulose's exceptional mechanical properties, biodegradability, and surface functionality provide measurable performance advantages over petroleum-derived polymer alternatives.

Get More Information about this report -

Request Free Sample ReportNanocellulose encompasses three primary material forms: cellulose nanocrystals (CNC), cellulose nanofibrils (CNF), and microfibrillated cellulose (MFC), each produced through distinct processing routes and serving differentiated application requirements. CNC particles, with typical dimensions of 5-20 nm width and 100-500 nm length, exhibit crystallinity above 85%, tensile modulus of 100-140 GPa, and an axial elastic modulus comparable to Kevlar. CNF, with fiber diameters of 5-50 nm and lengths of several micrometers, forms entangled networks that provide outstanding rheological modification, barrier film formation, and composite reinforcement properties. MFC, produced at larger scale through mechanical fibrillation, delivers cost-effective reinforcement at industrial volumes for paper, board, and construction applications.

The nanocellulose market is transitioning from pilot-scale production to commercial-scale industrial output, a phase transformation marked by Stora Enso's 10,000 tonnes/year MFC facility in Imatra, Finland achieving full commercial production in December 2024. This capacity milestone reduced MFC pricing from USD 50-100 per kilogram at pilot scale to USD 8-15 per kilogram at commercial volumes, crossing the cost viability threshold for high-volume packaging and paper applications. Total global nanocellulose production capacity reached approximately 25,000 tonnes in 2025, with 12 production facilities operating at semi-commercial or commercial scale across North America, Europe, Japan, and Brazil.

Regulatory momentum is accelerating nanocellulose market growth from multiple directions. The European Union's Single-Use Plastics Directive (SUPD), effective since July 2021, and the forthcoming Packaging and Packaging Waste Regulation (PPWR) mandating minimum recycled content and bio-based material thresholds for food packaging by 2030, are creating structural demand for CNC and CNF barrier coatings as replacements for polyethylene, EVOH, and PVDC petroleum-derived barrier layers. The US Environmental Protection Agency (EPA) proposed PFAS restrictions under the Toxic Substances Control Act (TSCA) are simultaneously driving substitution of fluorinated grease-resistant coatings with nanocellulose-based alternatives in food packaging. ASTM International has published standards D7075 and D6866 covering nanocellulose characterization and bio-based content verification, establishing the quality assurance framework needed for industrial adoption.

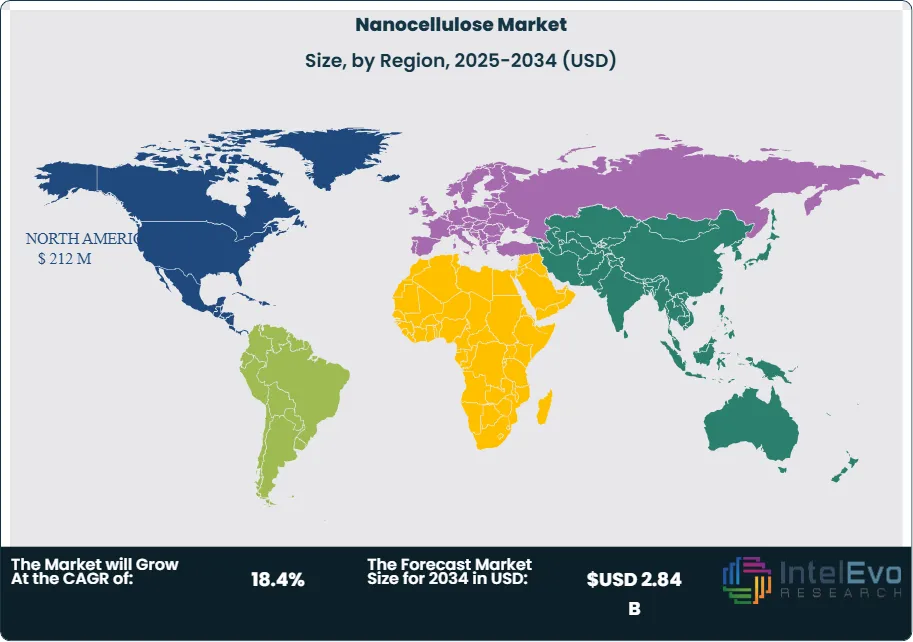

Regional dynamics in the nanocellulose market reflect forestry resource access, pulp industry infrastructure, and regulatory incentives for bio-based materials. North America leads at 34.2% market share (USD 212 Million) in 2025, supported by Canada's concentrated position in CNC production through CelluForce and a strong US research-to-commercialization pipeline anchored by the USDA Forest Products Laboratory and University of Maine Process Development Center. Europe holds 31.8% share (USD 197 Million), with Finland, Norway, and Sweden providing both forest biomass feedstock and commercial production capacity through Stora Enso, Borregaard, and FiberLean. Asia Pacific at 22.4% (USD 139 Million) is the fastest-growing region, driven by Nippon Paper and DAICEL in Japan and emerging production programs in China and India.

, By Source (Wood Pulp, Cotton Linters, Agricultural Residues, Bacterial Fermentation), By Application (Packaging, Composites, Biomedical, Electronics, Paper & Board), By End-Use Industry, Market Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The nanocellulose market was valued at USD 0.62 Billion in 2025 and is projected to reach USD 2.84 Billion by 2034, expanding at a CAGR of 18.4% across the 2026-2034 forecast period.

- Segment Dominance: Microfibrillated cellulose (MFC) leads the By Type segment with 42.0% market share in 2025, valued at USD 260 Million, driven by Stora Enso's commercial-scale production enabling cost-competitive supply for packaging, paper, and construction applications.

- Segment Dominance: Packaging and barrier coatings lead the By Application segment with 28.5% share in 2025, representing USD 177 Million in revenue, propelled by EU Single-Use Plastics Directive mandates and EPA PFAS restrictions creating regulatory-driven demand for bio-based barrier alternatives.

- Driver: Global regulatory prohibition of petroleum-derived and fluorinated packaging barriers, affecting an estimated USD 18 Billion in annual packaging material expenditure, is the primary structural driver, with nanocellulose barrier coatings positioned as the leading compliant replacement technology.

- Restraint: Production cost and scale limitations remain the primary constraint, with CNC pricing at USD 25-60 per kilogram and CNF at USD 15-40 per kilogram in 2025, compared to USD 1-3 per kilogram for competing petroleum-based polymers, restricting penetration in price-sensitive commodity applications.

- Opportunity: The biomedical and pharmaceutical nanocellulose segment represents the highest-value commercial opportunity, with an estimated addressable market of USD 520 Million by 2034 for wound dressings, drug delivery scaffolds, tissue engineering substrates, and excipient applications.

- Trend: TEMPO-mediated oxidation processing is the dominant nanocellulose manufacturing trend, adopted by 58% of new production facilities commissioned since 2023, delivering surface-carboxylated CNF with superior dispersion stability and functionalization reactivity versus mechanically produced alternatives.

- Regional Analysis: North America leads all regions with a 34.2% share in 2025, representing USD 212 Million in revenue, supported by CelluForce's CNC production leadership, USDA Forest Products Laboratory technology transfer programs, and accelerating demand from US packaging converters seeking PFAS-free barrier alternatives.

Competitive Landscape Overview

The nanocellulose market exhibits moderate fragmentation in 2025, with the top four producers — CelluForce, Stora Enso, Sappi, and Nippon Paper — collectively accounting for approximately 46% of global production capacity and 41% of market revenue. Competition is differentiated along nanocellulose type (CNC vs. CNF vs. MFC), production scale, application-specific grades, and regulatory qualification status for food contact and biomedical applications. European pulp and paper companies hold structural advantages through integrated access to wood pulp feedstock, established industrial infrastructure, and proximity to EU regulatory-driven demand. Three venture-backed startups (Melodea, Anomera, Blue Goose Biorefineries) raised a combined USD 72 Million in 2024-2025, indicating sustained investor appetite for nanocellulose application-specific commercialization opportunities.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Platform | Geo Strength | Recent Strategic Move (2024-2026) |

| CelluForce Inc. | Canada | Leader | CelluForce NCC Spray-Dried CNC | North America | Completed CAD 45M capacity expansion at Windsor, QC plant (Q1 2025), increasing CNC output to 300 tonnes/year and securing multi-year supply contracts with 3 global coating formulators. |

| Stora Enso Oyj | Finland | Leader | MFC (Microfibrillated Cellulose) | Europe / Global | Launched commercial MFC production at 10,000 tonnes/year Imatra, Finland facility (2024), the world's largest nanocellulose plant, targeting packaging and barrier coating applications. |

| Sappi Limited | South Africa | Leader | Valida Cellulose Nanofibrils | Europe / North America | Expanded Valida CNF pilot production at Ehingen, Germany to 150 tonnes/year (Mar 2025) and secured joint development agreements with 5 European personal care brand owners. |

| Nippon Paper Industries | Japan | Leader | Cellenpia CNF | Asia Pacific | Inaugurated 500 tonnes/year CNF production facility in Ishinomaki, Japan (Jun 2025), the largest dedicated CNF plant in Asia, supplying automotive composite and packaging customers. |

| Melodea Ltd. | Israel | Challenger | CNC-based Barrier Coatings | Europe / North America | Secured EUR 32M Series C funding (Sep 2025) led by Horizons Ventures to scale CNC barrier coating production for food packaging replacement of petroleum-derived barriers. |

| Suzano S.A. | Brazil | Challenger | Micro/Nano Cellulose Fibrils | Latin America / Global | Announced USD 80M investment in commercial nanocellulose production line at Limeira, Brazil facility (Q4 2025), targeting 5,000 tonnes/year MFC for packaging and construction applications. |

| Borregaard ASA | Norway | Challenger | Exilva Microfibrillated Cellulose | Europe / Global | Expanded Exilva production capacity to 1,200 tonnes/year at Sarpsborg, Norway (2025) and launched Exilva V 01-X grade for rheology modification in paints and adhesives. |

| DAICEL Corporation | Japan | Niche Player | CELISH Cellulose Nanofiber | Asia Pacific | Initiated joint development program with Toyota for nanocellulose-reinforced automotive interior components, targeting 30% weight reduction versus glass fiber-filled polymers (Jan 2026). |

| FiberLean Technologies | UK | Niche Player | FiberLean MFC | Europe | Commissioned third industrial MFC production line at Imerys UK facility (Q3 2025), increasing capacity to 8,000 tonnes/year for paper and board applications. |

| Anomera Inc. | Canada | Niche Player | DextraCel CNC | North America | Received FDA GRAS (Generally Recognized As Safe) status for DextraCel CNC in food contact applications (Feb 2026), the first CNC product to achieve US food-grade clearance. |

By Type:

Microfibrillated cellulose (MFC) leads the nanocellulose market with 42.0% share at USD 260 Million in 2025, driven by Stora Enso's and FiberLean's commercial-scale production enabling volumes sufficient for integration into existing paper mill and packaging converter operations. MFC's fiber network structure delivers rheology modification, strength enhancement, and gas barrier performance at lower cost per kilogram than CNC or CNF, making it the first nanocellulose type to achieve commodity-adjacent pricing. Cellulose nanofibrils (CNF) hold 32.5% share at USD 202 Million, valued for superior film-forming and barrier properties with oxygen transmission rates below 1 cc/m2/day at 50% relative humidity, positioning CNF as the primary technology for food packaging barrier coating applications. Cellulose nanocrystals (CNC) account for 18.5% at USD 115 Million, commanding premium pricing of USD 25-60 per kilogram for applications requiring optical transparency, liquid crystal self-assembly, and high-surface-area reinforcement in composites and biomedical devices. Bacterial nanocellulose (BNC) represents 7.0% at USD 43 Million, produced through Gluconacetobacter fermentation and valued for its ultra-high purity, water-holding capacity, and biocompatibility in wound dressings and tissue engineering scaffolds.

By Source:

Wood pulp is the dominant feedstock source at 62.0% of the nanocellulose market, valued at USD 384 Million in 2025, reflecting the established forestry and pulp industry infrastructure in Scandinavia, Canada, and Japan that provides cost-effective cellulose fiber supply. Kraft and dissolving-grade wood pulps serve as primary inputs for CNC, CNF, and MFC production. Cotton linters account for 14.5% at USD 90 Million, preferred for pharmaceutical and biomedical nanocellulose grades where purity requirements exceed wood-pulp-derived materials. Agricultural residues including sugarcane bagasse, wheat straw, and rice straw represent 12.0% at USD 74 Million, an emerging source category driven by circular-economy valorization of crop waste. Bacterial fermentation accounts for 7.0% at USD 43 Million. Algae and tunicate-derived nanocellulose holds 4.5% at USD 28 Million, primarily in research and specialty applications.

By Application:

Packaging and barrier coatings lead nanocellulose applications with 28.5% share at USD 177 Million in 2025, propelled by regulatory mandates driving substitution of petroleum-derived and fluorinated packaging barriers. CNF barrier coatings achieving oxygen transmission rates below 1 cc/m2/day provide performance parity with EVOH at competitive cost when applied at 2-5 g/m2 coat weights. Composites and automotive applications hold 18.0% at USD 112 Million, with nanocellulose reinforcement delivering 40-60% improvement in tensile strength versus unfilled biopolymers. Paints, coatings, and adhesives represent 16.5% at USD 102 Million, where MFC and CNF serve as rheology modifiers, sag-resistance agents, and film-forming additives. Biomedical and pharmaceutical applications account for 12.0% at USD 74 Million, the highest per-kilogram value segment at USD 200-800 per kilogram for medical-grade BNC wound dressings and drug delivery platforms. Personal care and cosmetics hold 8.5% at USD 53 Million, with CNC and CNF used as stabilizers, emulsifiers, and film-forming agents in premium skincare formulations. Paper and board enhancement represents 10.0% at USD 62 Million. Food and beverage applications hold 4.0% at USD 25 Million, growing rapidly following Anomera's FDA GRAS clearance. Electronics applications account for 2.5% at USD 16 Million.

By Processing Method:

Mechanical fibrillation is the most widely deployed processing method at 38.0% of nanocellulose production, used for MFC and CNF production through high-pressure homogenization, microfluidization, and grinding. TEMPO-mediated oxidation holds 28.0%, adopted by 58% of new facilities commissioned since 2023 for its ability to produce surface-carboxylated CNF with controlled dimensions and superior colloidal stability. Acid hydrolysis accounts for 20.0%, the standard method for CNC production using sulfuric acid to selectively dissolve amorphous cellulose regions. Enzymatic treatment represents 9.0%, growing as a low-energy alternative that reduces specific energy consumption from 20,000-30,000 kWh/tonne for mechanical fibrillation to 5,000-8,000 kWh/tonne. Bacterial synthesis holds 5.0% for BNC production.

By End-Use Industry:

Packaging is the dominant end-use industry at 26.0% (USD 161 Million) in 2025; automotive and aerospace at 16.0% (USD 99 Million); construction at 14.0% (USD 87 Million); healthcare and life sciences at 12.5% (USD 78 Million); consumer goods including personal care at 11.0% (USD 68 Million); pulp and paper at 10.0% (USD 62 Million); electronics at 5.0% (USD 31 Million); oil and gas at 3.5% (USD 22 Million) for drilling fluid rheology modification; other industries at 2.0%.

Regional Analysis

North America

North America leads the global nanocellulose market with a 34.2% share in 2025, valued at USD 212 Million. Canada holds a distinctive position, contributing 38% of North American revenue at USD 81 Million, anchored by CelluForce's CNC production in Windsor, Quebec and Kruger's pilot-scale CNF operations. Canada's forest biomass resource base of 347 million hectares of managed forest and its established dissolving pulp industry provide upstream feedstock advantages that support competitive nanocellulose production costs. The United States accounts for 58% of regional revenue at USD 123 Million, driven by a robust research-to-commercialization pipeline through the USDA Forest Products Laboratory in Madison, Wisconsin and the University of Maine Process Development Center, which collectively hold over 40 nanocellulose-related patents. EPA PFAS restrictions under TSCA are creating near-term substitution urgency among US food packaging converters, generating commercial demand for CNC and CNF barrier coating systems. Mexico represents 4% at USD 8 Million. North America is projected to grow at 17.8% CAGR to reach USD 948 Million by 2034.

Europe

Europe accounts for 31.8% of the nanocellulose market in 2025, valued at USD 197 Million. Finland leads European demand with 28% of regional revenue at USD 55 Million, driven by Stora Enso's commercial MFC production in Imatra and VTT Technical Research Centre's nanocellulose technology platform. Norway holds 18% at USD 35 Million, anchored by Borregaard's Exilva MFC production in Sarpsborg. Germany contributes 16% at USD 32 Million, with Sappi's Valida CNF pilot production in Ehingen supplying personal care and coating applications. France accounts for 12% at USD 24 Million. The European Union's PPWR, mandating bio-based material thresholds for food packaging by 2030, is the strongest regulatory driver in the region, with European packaging converters investing an estimated EUR 1.8 Billion in bio-based barrier technology qualification between 2024 and 2028. The EU Horizon Europe program allocated EUR 120 Million to nanocellulose research between 2021 and 2025, supporting upstream technology development that feeds commercial pipeline activity. Europe is forecast to grow at 17.6% CAGR to reach USD 870 Million by 2034.

Asia Pacific

Asia Pacific represents 22.4% of the nanocellulose market in 2025, valued at USD 139 Million, and is projected to be the fastest-growing region at a CAGR of 20.6% through 2034, reaching USD 720 Million. Japan is the dominant Asia Pacific market at 42% of regional revenue (USD 58 Million), driven by Nippon Paper's 500 tonnes/year CNF facility and DAICEL's CELISH nanofiber production for automotive composite applications. Japan's Ministry of Economy, Trade and Industry (METI) has designated nanocellulose a strategic material under the Bio-Strategy 2030, providing JPY 12 Billion in development funding through 2028. China holds 28% of Asia Pacific revenue at USD 39 Million, with the Chinese Academy of Forestry and provincial research institutes supporting nanocellulose scale-up programs aligned with the 14th Five-Year Plan for Bio-Based Materials. India accounts for 14% at USD 19 Million, with agricultural residue-based nanocellulose production from bagasse and rice straw gaining traction as a crop waste valorization strategy under National Bio-Energy Programme guidelines. South Korea represents 12% at USD 17 Million, with active R&D programs at Korea Forest Research Institute (NIFoS).

Latin America

Latin America holds 7.8% of the nanocellulose market in 2025, valued at USD 48 Million. Brazil dominates at 68% of regional revenue (USD 33 Million), supported by Suzano's USD 80 Million investment in commercial nanocellulose production announced in Q4 2025 and the country's position as the world's largest eucalyptus pulp producer, providing cost-effective cellulose feedstock. Brazil's abundant sugarcane bagasse supply, estimated at 170 million tonnes annually, creates a unique pathway for agricultural residue-based nanocellulose production that leverages existing biorefinery infrastructure. Mexico holds 16% at USD 8 Million, and Chile represents 10% at USD 5 Million with forestry-based MFC development programs. Regional growth is forecast at 16.8% CAGR to reach USD 188 Million by 2034.

Middle East and Africa

Middle East and Africa accounts for 3.8% of the nanocellulose market in 2025, valued at USD 24 Million. South Africa leads at 42% of regional revenue (USD 10 Million), anchored by Sappi's global headquarters and its R&D programs in nanocellulose applications for personal care and packaging. The UAE holds 25% at USD 6 Million, driven by construction sector demand for nanocellulose-enhanced cement and concrete additives under Dubai Smart City and NEOM-related material specifications. Saudi Arabia represents 20% at USD 5 Million. The region is in early-stage market development, with most nanocellulose consumption met through imports from European and North American producers. MEA is projected to grow at 18.2% CAGR to reach USD 105 Million by 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Cellulose Nanocrystals (CNC)

- Cellulose Nanofibrils (CNF)

- Microfibrillated Cellulose (MFC)

- Bacterial Nanocellulose (BNC)

By Source

- Wood Pulp

- Cotton Linters

- Agricultural Residues (Bagasse, Straw)

- Bacterial Fermentation

- Algae / Tunicate

By Application

- Packaging & Barrier Coatings

- Composites & Automotive

- Paints, Coatings & Adhesives

- Biomedical & Pharmaceutical

- Personal Care & Cosmetics

- Paper & Board

- Food & Beverages

- Textiles

- Electronics

By Processing Method

- Acid Hydrolysis

- Mechanical Fibrillation

- Enzymatic Treatment

- TEMPO-Mediated Oxidation

- Bacterial Synthesis

By End-Use Industry

- Packaging

- Automotive & Aerospace

- Construction

- Healthcare & Life Sciences

- Consumer Goods

- Pulp & Paper

- Electronics

- Oil & Gas

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.62 B |

| Forecast Revenue (2034) | USD 2.84 B |

| CAGR (2025-2034) | 18.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, (Cellulose Nanocrystals (CNC), Cellulose Nanofibrils (CNF), Microfibrillated Cellulose (MFC), Bacterial Nanocellulose (BNC)), By Source, (Wood Pulp, Cotton Linters, Agricultural Residues (Bagasse, Straw), Bacterial Fermentation, Algae / Tunicate), By Application, (Packaging & Barrier Coatings, Composites & Automotive, Paints, Coatings & Adhesives, Biomedical & Pharmaceutical, Personal Care & Cosmetics, Paper & Board, Food & Beverages, Textiles, Electronics), By Processing Method, (Acid Hydrolysis, Mechanical Fibrillation, Enzymatic Treatment, TEMPO-Mediated Oxidation, Bacterial Synthesis), By End-Use Industry, (Packaging, Automotive & Aerospace, Construction, Healthcare & Life Sciences, Consumer Goods, Pulp & Paper, Electronics, Oil & Gas) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CELLUFORCE INC., NIPPON PAPER INDUSTRIES, BORREGAARD ASA, ANOMERA INC., INNVENTIA (RISE), STORA ENSO OYJ, MELODEA LTD., DAICEL CORPORATION, KRUGER INC., UNIVERSITY OF MAINE PROCESS DEVELOPMENT CENTER, SAPPI LIMITED, SUZANO S.A., FIBERLEAN TECHNOLOGIES, AMERICAN PROCESS INC., VTT TECHNICAL RESEARCH CENTRE, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Source (Wood Pulp, Cotton Linters, Agricultural Residues, Bacterial Fermentation), By Application (Packaging, Composites, Biomedical, Electronics, Paper & Board), By End-Use Industry, Market Trends & Forecast 2026-2034")

, By Source (Wood Pulp, Cotton Linters, Agricultural Residues, Bacterial Fermentation), By Application (Packaging, Composites, Biomedical, Electronics, Paper & Board), By End-Use Industry, Market Trends & Forecast 2026-2034")

, By Source (Wood Pulp, Cotton Linters, Agricultural Residues, Bacterial Fermentation), By Application (Packaging, Composites, Biomedical, Electronics, Paper & Board), By End-Use Industry, Market Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Nanocellulose Market?

The Global Nanocellulose Market was valued at USD 0.52 Billion in 2024 and is projected to reach USD 2.84 Billion by 2034, growing at a CAGR of 18.4% from 2026 to 2034, driven by rising demand for sustainable bio-based materials, increasing adoption in packaging and composites, advancements in nanotechnology, and expanding applications across healthcare, electronics, automotive, and paper industries.

Who are the major players in the Nanocellulose Market?

CELLUFORCE INC., NIPPON PAPER INDUSTRIES, BORREGAARD ASA, ANOMERA INC., INNVENTIA (RISE), STORA ENSO OYJ, MELODEA LTD., DAICEL CORPORATION, KRUGER INC., UNIVERSITY OF MAINE PROCESS DEVELOPMENT CENTER, SAPPI LIMITED, SUZANO S.A., FIBERLEAN TECHNOLOGIES, AMERICAN PROCESS INC., VTT TECHNICAL RESEARCH CENTRE, OTHERS

Which segments covered the Nanocellulose Market?

By Type, (Cellulose Nanocrystals (CNC), Cellulose Nanofibrils (CNF), Microfibrillated Cellulose (MFC), Bacterial Nanocellulose (BNC)), By Source, (Wood Pulp, Cotton Linters, Agricultural Residues (Bagasse, Straw), Bacterial Fermentation, Algae / Tunicate), By Application, (Packaging & Barrier Coatings, Composites & Automotive, Paints, Coatings & Adhesives, Biomedical & Pharmaceutical, Personal Care & Cosmetics, Paper & Board, Food & Beverages, Textiles, Electronics), By Processing Method, (Acid Hydrolysis, Mechanical Fibrillation, Enzymatic Treatment, TEMPO-Mediated Oxidation, Bacterial Synthesis), By End-Use Industry, (Packaging, Automotive & Aerospace, Construction, Healthcare & Life Sciences, Consumer Goods, Pulp & Paper, Electronics, Oil & Gas)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date