- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global 3D Audio Market Size & Forecast 2025–2034 | 11.5% CAGR

Global 3D Audio Market Size, Share & Analysis – By Component (Hardware, Software, Services), By Technology (Binaural Audio, Object-Based Audio, Wave Field Synthesis), By Application (Gaming, AR/VR, Cinematic Production, Music Streaming, Live Events), By End-Use (Residential, Commercial), By Region, Industry Trends, Competitive Landscape, Innovation Strategies, Long-Term Revenue Outlook & Forecast 2025–2034

Report Overview

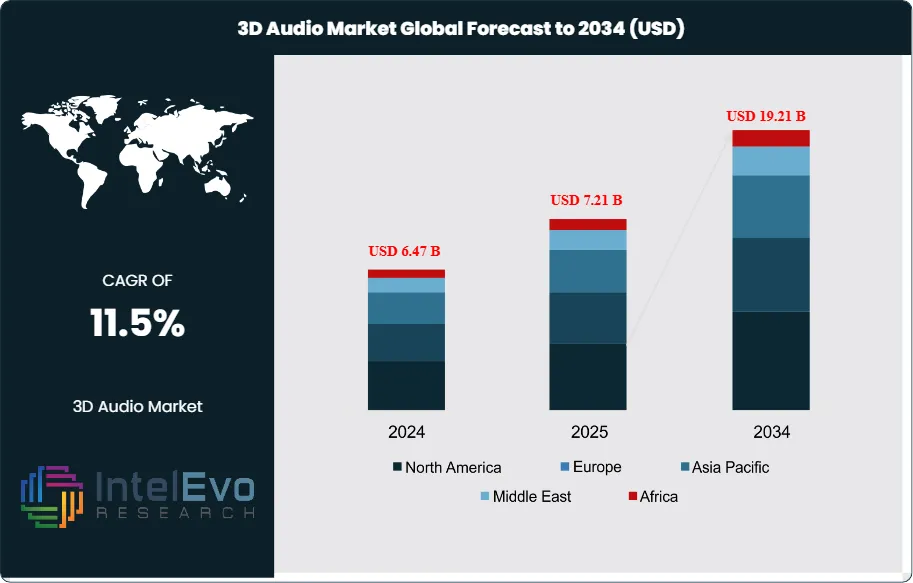

The Global 3D Audio Market was valued at approximately USD 6.47 billion in 2024 and is projected to reach nearly USD 19.21 billion by 2034, driven by growing adoption across gaming, AR/VR, cinematic production, and immersive media applications. Based on the established growth trajectory, the market size for 2025 is estimated at approximately USD 7.21 billion. From 2026 onward, the market is expected to expand at a compound annual growth rate (CAGR) of approximately 11.5% during 2026–2034, ultimately reaching around USD 19.21 billion by 2034.

Get More Information about this report -

Request Free Sample Report3D audio, also called spatial audio, recreates how people perceive sound in space by simulating depth, distance, and direction. Vendors apply advanced signal processing, psychoacoustic models, and AI-based personalization to deliver immersive sound across consumer and professional environments.

Demand expansion in entertainment is the primary growth engine. Streaming video, gaming, and music services together account for over 45% of global 3D audio revenues in 2024, as platforms compete on immersion and content differentiation. Rapid adoption of AR and VR headsets, growing at more than 15% annually, accelerates use of 3D audio in interactive games, virtual events, and cinematic experiences. On the supply side, semiconductor advances, dedicated spatial audio chips, and automated mixing tools lower production costs and enable broader device integration.

Automotive, home, and workplace applications add new growth layers. In-car spatial audio supports both premium entertainment and driver-assistance cues, with automotive expected to approach 12–15% of market revenues by 2034. Smart speakers, TVs, soundbars, and wearables embed 3D audio capabilities as standard features, supported by edge AI that adapts sound fields to room acoustics and listener profiles. Enterprises deploy 3D audio in collaboration, training, and simulation, improving speech clarity and situational awareness in hybrid work settings.

Technology standardization is emerging as a strategic battleground. The joint Samsung–Google Immersive Audio Model and Formats (IAMF) initiative, launched in 2023, seeks to provide an open 3D audio framework that supports vertical sound placement and AI-driven scene analysis as an alternative to incumbent formats. Competing ecosystems increase short-term fragmentation risk but also stimulate innovation in codecs, authoring tools, and cloud-based rendering platforms.

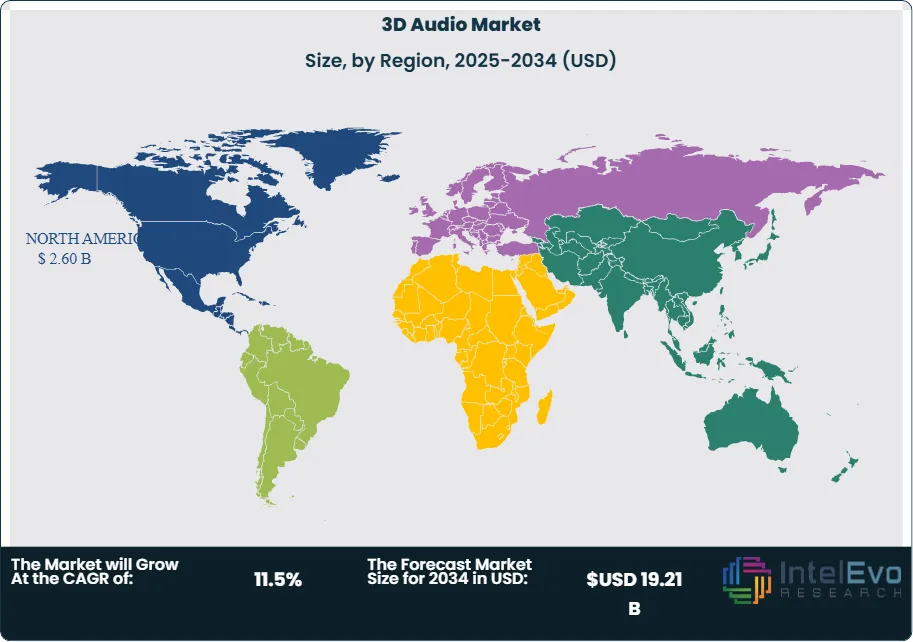

Regulatory and risk considerations gain weight as adoption scales. Content and broadcasting authorities influence codec choices, loudness norms, and accessibility features such as dialogue enhancement. Data protection rules shape AI training on listener behavior. High implementation costs, skills gaps in immersive audio production, and uneven content availability remain key restraints. Regionally, North America holds about 35% of 2024 revenues, followed by Europe at 28%, while Asia Pacific, with the fastest projected CAGR above 13%, stands out as the leading emerging investment hotspot.

, By Technology (Binaural Audio, Object-Based Audio, Wave Field Synthesis), By Application (Gaming, AR/VR, Cinematic Production, Music Streaming, Live Events), By End-Use (Residential, Commercial), By Region, Industry Trends, Competitive Landscape, Innovation Strategies, Long-Term Revenue Outlook & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global 3D audio market stands at USD 6.47 billion in 2024 and is on a path toward USD 19.21 billion by 2034, reflecting a CAGR of 11.5%, 2026-2034.

- Segment Dominance: The hardware segment leads the competitive landscape with a 46.8%, 2023 revenue share, signaling strong demand for devices that enable immersive listening. This dominance anchors an estimated: 3.0 billion USD, 2023 in hardware-driven 3D audio sales.

- Segment Dominance: The residential segment holds a 72.5%, 2023 share of total 3D audio revenues, reflecting its role as the core adoption arena. This segment likely generates estimated: 4.2 billion USD, 2023 as consumers upgrade home entertainment setups.

- Driver: Growing investment in home entertainment, supported by a 72.5%, 2023 residential share, drives sustained replacement and upgrade cycles. The 11.5%, 2024-2034 CAGR aligns with rising adoption of 3D-enabled devices and content services.

- Restraint: High upfront device costs and limited native 3D content constrain penetration beyond premium users, particularly in price-sensitive segments. These barriers could cap near-term adoption at an estimated: 60.0% of addressable households, 2024.

- Opportunity: Expansion into non-residential venues such as automotive, cinemas, and public spaces offers upside beyond the 72.5%, 2023 residential base. Emerging applications could unlock estimated: 1.5 billion USD, 2024 in incremental revenues, with outsized gains in developing economies.

- Trend: Vendors increasingly shift from pure hardware to integrated software and AI-driven spatial processing, raising the software and services contribution from an estimated: 25.0% of revenues, 2024 to higher levels over 2024-2034. This shift supports recurring revenue models and accelerates feature innovation.

- Regional Analysis: North America leads with a 36.4%, 2023 share and 2.1 billion USD, 2023 in revenues, underpinned by high spending and strong vendor presence. Asia Pacific, while smaller today at an estimated: 25.0% share, 2024, likely delivers faster growth as device affordability and content availability improve.

By Component

The hardware segment continues to hold a central position in the 3D audio landscape in 2025. It accounts for more than 46 percent of global revenue and remains the primary channel through which you experience spatial sound. Headphones, soundbars, in-ear devices, and multi-speaker systems form the core of this category. Growth reflects steady improvements in acoustic engineering, stronger output efficiency in compact devices, and rising demand for spatial sound across entertainment, gaming, and personal audio ecosystems.

Manufacturers expand hardware portfolios as 3D audio adoption increases in home theater systems, VR and AR headsets, and gaming accessories. Consumers expect consistent sound positioning and room-adaptive playback, which drives upgrades to higher precision drivers and DSP-enabled hardware. AI-supported tuning features now appear in mid-range products, and this shift supports faster replacement cycles. As smart homes expand, you see more households adopting multi-room speakers with embedded spatial audio features.

Software and services also expand their roles. Software platforms that render spatial audio in real time support higher device compatibility. Services such as spatial audio mixing, content authoring, and cloud-based tuning tools grow as content creators adopt advanced sound formats. These segments grow faster than hardware from 2025 onward, although hardware remains the revenue anchor.

By End-Use

Residential use accounts for the largest share of 3D audio deployments, reaching more than 70 percent in 2025. Households continue to upgrade entertainment systems as streaming platforms expand libraries encoded with spatial sound. You see higher adoption of 3D-enabled smart speakers, TVs, and soundbars as consumers seek more realistic sound reproduction for movies, games, and music. The expansion of VR-based entertainment also strengthens residential demand.

Commercial buyers follow a different trajectory. Cinemas, retail venues, automotive OEMs, and simulation centers integrate spatial audio to improve audience engagement and operational training. Commercial adoption grows at a steady pace as companies invest in sound systems that support immersive media, virtual collaboration, and passenger-experience upgrades. Industrial sites adopt spatial audio selectively for alert systems and situational awareness.

By Region

North America maintains the largest regional share at more than 36 percent of global revenue in 2025. Strong device penetration, high spending on entertainment, and the presence of leading technology companies support this lead. Firms such as Dolby and DTS continue to expand spatial audio standards across consumer electronics and streaming ecosystems. The region also benefits from rapid uptake of AR and VR systems in gaming and enterprise applications.

Europe holds a stable share driven by cinema modernization, automotive production, and strong demand for premium audio products. Asia Pacific records the fastest growth rate due to rising consumer spending in China, South Korea, and India. You see rapid increases in gaming adoption, smartphone upgrades, and smart home expansion. Latin America and the Middle East and Africa advance from a smaller base but show improving demand as broadband connectivity and streaming services scale across these regions.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Hardware

- Software

- Services

By End-use

- Residential

- Commercial

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.21 B |

| Forecast Revenue (2034) | USD 19.21 B |

| CAGR (2025-2034) | 11.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Hardware, Software, Services), By End-use (Residential, Commercial) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Waves Audio Ltd., Google, VisiSonics Corporation, Auro Technologies Inc, Hooke Audio, Sennheiser electronic GmbH & Co., dearVR, Dolby Labs, 3D Sound Labs, Fraunhofer, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Binaural Audio, Object-Based Audio, Wave Field Synthesis), By Application (Gaming, AR/VR, Cinematic Production, Music Streaming, Live Events), By End-Use (Residential, Commercial), By Region, Industry Trends, Competitive Landscape, Innovation Strategies, Long-Term Revenue Outlook & Forecast 2025–2034")

, By Technology (Binaural Audio, Object-Based Audio, Wave Field Synthesis), By Application (Gaming, AR/VR, Cinematic Production, Music Streaming, Live Events), By End-Use (Residential, Commercial), By Region, Industry Trends, Competitive Landscape, Innovation Strategies, Long-Term Revenue Outlook & Forecast 2025–2034")

, By Technology (Binaural Audio, Object-Based Audio, Wave Field Synthesis), By Application (Gaming, AR/VR, Cinematic Production, Music Streaming, Live Events), By End-Use (Residential, Commercial), By Region, Industry Trends, Competitive Landscape, Innovation Strategies, Long-Term Revenue Outlook & Forecast 2025–2034")

Frequently Asked Questions

How big is the 3D Audio Market?

Global 3D Audio Market valued at USD 6.47B in 2024, projected to reach USD 19.21B by 2034 at 11.5% CAGR, driven by gaming, AR/VR, and immersive media growth.

Who are the major players in the 3D Audio Market?

Waves Audio Ltd., Google, VisiSonics Corporation, Auro Technologies Inc, Hooke Audio, Sennheiser electronic GmbH & Co., dearVR, Dolby Labs, 3D Sound Labs, Fraunhofer, Other Key Players

Which segments covered the 3D Audio Market?

By Component (Hardware, Software, Services), By End-use (Residential, Commercial)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date