- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global 3D Printed Construction Market Size, Share | CAGR 31.3%

Global 3D Printed Construction Market Size, Share & Growth Analysis Report By Method (Extrusion-Based 3D Printing, Powder Bonding (Binder Jetting), Robotic Arm-Based 3D Printing, Gantry-Based 3D Printing, Crane-Based 3D Printing, Hybrid 3D Printing Methods), By Material Type (Concrete, Cementitious Composites, Mortar, Geopolymer Materials, Metals, Plastics and Polymer Composites, Fiber-Reinforced Materials, Recycled and Sustainable Materials), By End-Use (Residential, Commercial, Industrial, Infrastructure, Public & Government Projects), By Construction Form (Walls and Structural Components, Entire Buildings, Modular Units, Prefabricated Components, Architectural Elements, Decorative Structures), Industry Region, Market Dynamics, Emerging Trends, Competitive Landscape, Key Players, Strategic Insights and Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 2.45 Billion | USD 28.50 Billion | 31.3% | Asia Pacific, 38.7% |

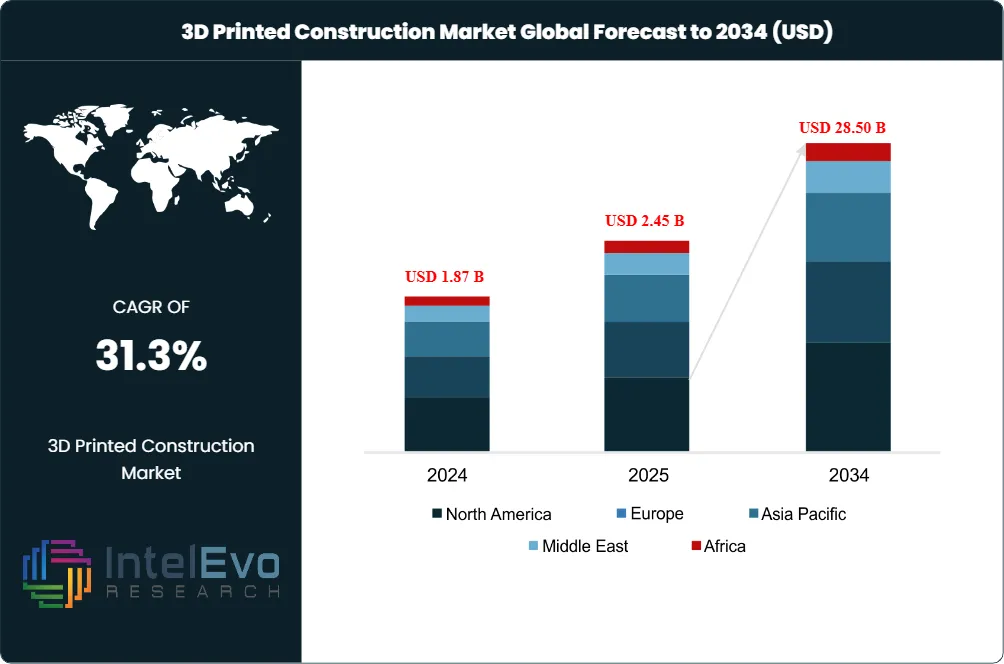

The 3D Printed Construction Market was valued at USD 1.87 Billion in 2024 and USD 2.45 Billion in 2025. The market is projected to reach USD 28.50 Billion by 2034, expanding at a CAGR of 31.3% during the forecast period from 2026 to 2034. The rapid adoption of automated construction technologies, increasing investments in affordable housing projects, and growing demand for sustainable building solutions are expected to accelerate market growth over the coming years. The market is also benefiting from advancements in large-scale 3D printing systems, robotic construction technologies, and eco-friendly printable materials, positioning 3D printed construction as a transformative solution for the future of the global construction industry.This represents an absolute dollar opportunity of USD 26.05 Billion over the analysis period. Demand acceleration reflects sustained investment in additive construction by ICON, COBOD International, Apis Cor, and Yingchuang (Winsun), alongside government-funded affordable housing pilots in the United States, Saudi Arabia, and Germany that converted prototype technology into routine project delivery.

Get More Information about this report -

Request Free Sample ReportAffordable housing pressure anchors the demand profile. The United States faces a structural shortage of approximately 6.5 million homes, while Saudi Arabia's Vision 2030 Building Technology Initiative targets 70% homeownership by 2030, both creating procurement runways for 3D printed residential delivery. Industry data indicate that 3D printed homes can lower residential construction costs by up to 45% versus traditional methods, while commercial structural cost reductions reach 80% on specific pilots. The 2024 completion of Lennar and ICON's 100-home Wolf Ranch community in Georgetown, Texas and the 2025 Dar Al Arkan three-story 345 sqm villa in Riyadh (printed in 26 days) validated full-scale viability.

Regulatory and standards activity reinforced the market through 2025. The Association for Advancing Automation published ANSI/A3 R15.06-2025 on October 29, 2025 alongside Part 3 user-requirements approved October 7, 2025, replacing the 2012 industrial robot safety standard with a 403-page document harmonized to ISO 10218-1:2025 and ISO 10218-2:2025. The US Army's Fort Bliss 3D-printed barracks demonstrated full-scale viability under the updated Unified Facilities Criteria, while NFPA and ASTM are converging on harmonized compliance pathways. The construction industry accounts for approximately 37% of global greenhouse gas emissions per the UN Environment Programme.

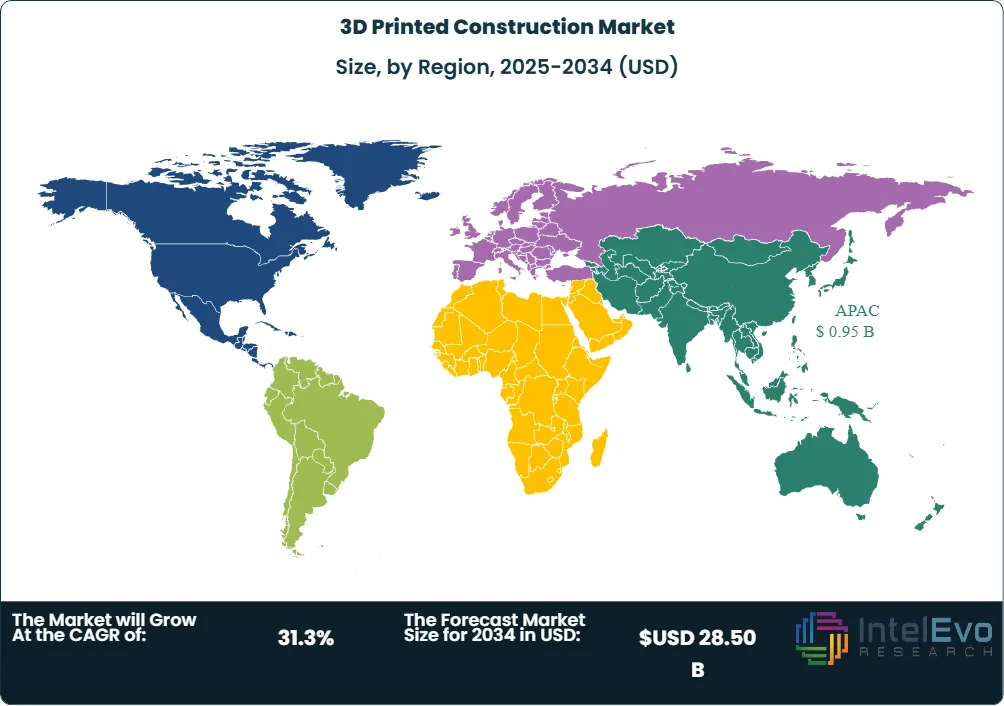

Asia Pacific held the largest revenue share at 38.7% in 2025, valued at approximately USD 0.95 Billion, driven by Yingchuang multi-story residential builds in Suzhou and Shanghai, India's growing additive construction adoption, and Japan's Lib Work residential pilots. North America followed at 28.4% with ICON's 245-plus structures completed including Lennar partnerships, US Army barracks, and the El Cosmico 3D-printed hotel in Marfa. Concrete dominated material segmentation at 55.5% revenue share in 2025 because of widespread D.fab CEMEX-COBOD local-sourcing supply chains and maturing geopolymer mixes that reduce embedded CO2 by more than 70%.

The forward outlook through 2034 hinges on three structural shifts. Sector consolidation will accelerate after the January 2025 sale process of Mighty Buildings and the liquidation of Diamond Age. Multi-story printers (ICON Phoenix, COBOD BOD3) will expand the addressable market beyond single-story residential. Low-carbon binders including geopolymer concrete and Mighty Buildings' Lumus composite will move from pilot to standard specification as embodied-carbon procurement rules tighten across EU and US public projects.

Market Definition & Scope

The 3D printed construction market is defined as additive manufacturing technologies that build structural elements, complete buildings, or infrastructure components by depositing concrete, mortar, polymer, metal, or composite materials layer by layer using gantry, robotic-arm, or crane-mounted printers. The market encompasses on-site printing equipment, off-site prefabricated module production, printable construction materials including concrete and geopolymer mixes, related software and slicing platforms, and integration services across building and infrastructure end-use categories.

This analysis includes residential, commercial, and industrial buildings; bridges, retaining walls, and utility infrastructure; military barracks and disaster-relief shelters; and additive components manufactured for assembly. Excluded from scope are conventional precast and prefabricated building methods that do not use additive deposition, formwork-replacement applications that are component-only without structural participation, lunar and Martian construction projects (NASA Olympus), and traditional industrial 3D printing not designed for permanent built environments. The 3D printed construction market represents approximately 0.02% of the USD 12 trillion global construction industry in 2025, signaling early-stage adoption with high forecast multiples.

, Robotic Arm-Based 3D Printing, Gantry-Based 3D Printing, Crane-Based 3D Printing, Hybrid 3D Printing Methods), By Material Type (Concrete, Cementitious Composites, Mortar, Geopolymer Materials, Metals, Plastics and Polymer Composites, Fiber-Reinforced Materials, Recycled and Sustainable Materials), By End-Use (Residential, Commercial, Industrial, Infrastructure, Public & Government Projects), By Construction Form (Walls and Structural Components, Entire Buildings, Modular Units, Prefabricated Components, Architectural Elements, Decorative Structures), Industry Region, Market Dynamics, Emerging Trends, Competitive Landscape, Key Players, Strategic Insights and Forecast 2026-2034")

Key Takeaways

- Market Growth: The global 3D printed construction market grows from USD 2.45 Billion in 2025 to USD 28.50 Billion by 2034, expanding at a 31.3% CAGR over the forecast period.

- Segment Dominance by Method: Extrusion held 62.4% revenue share in 2025, generating USD 1.53 Billion, anchored by gantry and robotic-arm systems from ICON, COBOD, and Apis Cor.

- Segment Dominance by Material: Concrete accounted for 55.5% of revenue in 2025, supported by D.fab CEMEX-COBOD partnerships enabling 99% local material sourcing on Saudi Arabia and India deployments.

- Driver: The United States housing shortage of approximately 6.5 million homes combined with Saudi Vision 2030's 70% homeownership target creates measurable demand that traditional construction cannot meet at required speed.

- Restraint: Vendor unit economics remain unproven, with Mighty Buildings entering a sale process in January 2025, Diamond Age liquidating, and ICON laying off 25% of staff before its USD 56 million Series C close.

- Opportunity: Multi-story residential printers including ICON Phoenix and COBOD BOD3 represent an estimated USD 4.2 Billion incremental opportunity by 2030 as municipal codes adapt to allow taller printed structures.

- Trend: Low-carbon binders including geopolymer concrete and Mighty Buildings' Lumus composite are moving from pilot to standard specification as embodied-carbon procurement rules tighten.

- Regional: Asia Pacific led with 38.7% share and USD 0.95 Billion revenue in 2025, with Saudi Arabia forecast as the fastest-growing single country at a 35.4% CAGR through 2034.

Key Insights Summary

- ICON Technology had built more than 245 homes and structures by March 2026, expanding from Lennar partnerships in Georgetown and Wimberley, Texas to military barracks at Fort Bliss in El Paso and the Texas Military Department printing facility.

- Dar Al Arkan and COBOD International completed the world's tallest on-site 3D printed building in Riyadh, a three-story 345 sqm villa printed in 26 days at less than EUR 10,000 in printable concrete cost using D.fab 99%-local-materials formulation.

- ICON closed a USD 56 million Series C funding round on January 30, 2025 led by Norwest Venture Partners and Tiger Global, lifting total funding to USD 507 million across 10 rounds, while announcing a 25% workforce reduction (114 employees) the same month.

- The UN Environment Programme reports that the construction industry accounts for approximately 37% of global greenhouse gas emissions, with USD 180 billion of cement consumed annually in US residential construction alone.

- ANSI/A3 R15.06-2025 was published October 29, 2025 as a 403-page replacement for the 2012 industrial robot safety standard, harmonized to ISO 10218-1:2025 and ISO 10218-2:2025, with Part 3 user requirements approved October 7, 2025.

- Mighty Buildings entered a four-week sale process on January 21, 2025 managed by Rock Creek Advisors with a February 14, 2025 final term sheet deadline, despite USD 150 million in cumulative funding from Wa'ed Ventures, Khosla Ventures, and Bold Capital.

Competitive Landscape Overview

The 3D printed construction market is moderately fragmented with the top four vendors (ICON Technology, COBOD International, Yingchuang Building Technique, and Apis Cor) accounting for an estimated combined 41% of global revenue in 2025. Competition shifted through 2025 from feature parity in print speed toward proven housing-customer relationships, multi-story capability, and low-carbon material qualification. ICON's March 2026 decision to sell its Titan multi-story printer to outside builders signals a strategic move from builder-operator toward equipment-and-software vendor, intensifying direct competition with COBOD's BOD2 sales model.

Pure-play vendors including ICON, COBOD, Apis Cor, WASP, CyBe Construction, and XtreeE retain leadership in printer hardware and integrated services, while material specialists Sika AG, CEMEX, and Holcim compete on printable mix qualification. New entrant Buildroid AI launched in November 2025 with USD 2 million in funding for simulation-first robotics, while the Mighty Buildings sale process opened in January 2025 may yield asset-purchase opportunities for incumbents seeking patents and Lumus composite IP. Regional specialists L&T Construction (India), JGC (Japan), Siam Cement (Thailand), and Orascom (Egypt) operate as COBOD partners.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| ICON Technology | United States | Leader | Vulcan and Phoenix multi-story 3D printers; CarbonX low-carbon mix | North America | Began selling Titan 3D-printing system to outside builders in March 2026 |

| COBOD International | Denmark | Leader | BOD2 modular 3D construction printer | Global, Europe-led | Expanded D.fab partnership with CEMEX for local material sourcing in 2025 |

| Yingchuang (Winsun) | China | Leader | Contour Crafting concrete extrusion systems | Asia Pacific | Continued multi-story residential builds across Suzhou and Shanghai |

| Apis Cor | United States | Challenger | Mobile robotic arm extrusion printer | North America, MENA | Completed Dubai Municipality administrative building in 2024 (640 sqm, two-story) |

| WASP S.r.l. | Italy | Challenger | Crane WASP modular printer for clay and concrete | Europe | Delivered TECLA earth-printed homes and TOVA bioplastic shelters through 2025 |

| CyBe Construction | Netherlands | Challenger | CyBe RC mobile mortar printer | Europe, MENA | Expanded MENA deployments through Saudi and UAE construction partners in 2025 |

| XtreeE | France | Niche Player | Connected industrial 3D printing units | Europe, Asia, US | Operating 12-plus connected printing units toward 50-unit global network target |

| MX3D | Netherlands | Niche Player | Wire arc additive manufacturing for steel structures | Europe | Continued steel bridge and architectural deployments under WAAM platform |

| PERI Group | Germany | Niche Player | BOD2 deployment partner; formwork-integrated printing | Europe | Maintained joint engineering with COBOD as strategic shareholder |

| Sika AG | Switzerland | Niche Player | SikaFiber and 3D printing mortar systems | Global | Expanded printable mortar product line for COBOD and partner printers |

By Method

The 3D printed construction market by method is led by extrusion-based deposition, which captured 62.4% revenue share in 2025 valued at approximately USD 1.53 Billion. Extrusion dominates because it accommodates near-universal site conditions, supports nozzle mounting on gantry systems (COBOD BOD2), robotic arms (Apis Cor, CyBe RC), and crane-mounted platforms (Crane WASP), and produces large continuous structural elements. ICON Vulcan and Phoenix, COBOD BOD2, and Apis Cor mobile printers deliver extruded concrete walls at print speeds approaching 0.5 cubic meters per hour for residential applications.

Powder bonding accounted for 22.8% of revenue in 2025 and is forecast to grow at a higher CAGR of 38.7% through 2034 because the method enables complex formworks, double-curved surfaces, and organic geometries that extrusion cannot match. Spray-based and other methods including wire arc additive manufacturing (MX3D Amsterdam Bridge) held the residual 14.8% share in 2025. Buying committees evaluating procurement checklists increasingly weight closed-loop quality assurance, print-head speed, and printable-volume per shift, with extrusion winning on volume and powder bonding winning on geometric complexity.

By Material Type

Concrete and mortar dominated material segmentation at 55.5% revenue share in 2025 because mature global supply chains, COBOD-CEMEX D.fab 99%-local-sourcing formulations, and Sika AG printable mortar product lines deliver predictable structural performance at attractive cost. Steel-fiber reinforcement and carbon-nanotube dispersion lift flexural strength of printed concrete without compromising flow rheology. Geopolymer mixes reducing embedded CO2 by over 70% are entering EU and California municipal procurement specifications under low-embodied-carbon requirements.

Metal printing captured 16.7% in 2025, anchored by MX3D's wire arc additive manufacturing for steel bridges including the Amsterdam stainless-steel pedestrian bridge and the US Army Jointless Hull machine for oversize structural components. Composites including foamed concretes, plant-based biocomposites, and Mighty Buildings' Lumus formulation accounted for 13.4% of revenue in 2025. Polymers represented 9.8% (modular interior partitions, facades, insulation), and other material categories the residual 4.6%. The composite segment is forecast to grow fastest because lightweight insulation gains of up to 60% address energy-efficient building requirements.

By End-Use

The building end-use segment captured 72.1% of revenue in 2025 because residential, commercial, and industrial structures represent the largest immediate addressable market, with ICON's Lennar partnership in Georgetown (100 homes), Dar Al Arkan's Saudi villa series, and Yingchuang's multi-story Suzhou residential builds anchoring volume. Within building, the residential sub-segment held 48.9% of total market revenue, followed by commercial at 25.7% and industrial at 14.8%. ROI calculations for buying committees increasingly justify 3D printed residential construction by comparing 26-day print durations against 6-to-12-month conventional build times.

Infrastructure end-use captured 27.9% revenue share in 2025 covering bridges (MX3D Amsterdam, Tsinghua University concrete bridge), retaining walls, utility infrastructure, and military structures (US Army Fort Bliss barracks, Texas Military Department training facility). The infrastructure sub-segment is forecast as the fastest-growing end-use at a 33.8% CAGR through 2034 because public-sector procurement timelines align with 3D printed construction's speed and material-saving advantages, and because bridge inspection and maintenance applications increasingly favor topology-driven printed components.

By Construction Form

On-site printing captured 58.6% of revenue in 2025 because direct deposition eliminates transport logistics, accommodates custom site geometries, and aligns with disaster-relief and remote-site deployment use cases including COBOD installations across Saudi Arabia and Egypt. Off-site prefabricated additive construction held 41.4% share, dominated by Mighty Buildings' Oakland production facility and Yingchuang's modular component manufacturing. The on-site segment is forecast at a 32.4% CAGR through 2034 because mobile printers including Apis Cor and CyBe RC are increasingly deployed in confined infill lots, where ICON's smaller-footprint robot announced in March 2025 specifically targets Austin's infill ADU market.

Regional Analysis

Asia Pacific

The global 3D printed construction market spans five regions with sharply different adoption profiles. Asia Pacific held the largest 2025 share at 38.7%, valued at approximately USD 0.95 Billion. China anchored regional revenue through Yingchuang Building Technique multi-story residential builds in Suzhou and Shanghai, with COBOD partner Siam Cement extending Thai deployments and L&T Construction expanding Indian residential pilots. Japan's Lib Work, Sekisui House, and Daiwa House subsidiaries operate research-stage additive construction projects under the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) framework. India recorded its first multi-story 3D printed residential building in 2024 in Pune through Tvasta partnership.

North America

North America captured 28.4% revenue share in 2025 valued at approximately USD 0.70 Billion. The United States anchored regional adoption through ICON's 245-plus completed structures including Lennar partnerships in Georgetown and Wimberley, US Army barracks at Fort Bliss, and the December 2025 announcement of luxury 3D printed homes at Canyon Club on Lake Travis. The HUD Housing Innovation Showcase grants and Department of Defense Unified Facilities Criteria updates anchor federal demand. Canada's Residential Housing Innovation Initiative (RHII) allocates multimillion-dollar funds to printed-home pilots, while Mexican distribution centers serving USMCA supply chains are evaluating off-site printed components.

Europe

Europe represented 21.6% revenue share in 2025 valued at approximately USD 0.53 Billion. Germany led through PERI deployments and the BSI-supervised three-story PERI 3D printed building completed in 2021. France contributed via XtreeE's network of connected industrial printing units expanding toward 50 global locations, and Italy via WASP S.r.l. TECLA earth-printed and TOVA bioplastic shelter projects. The Netherlands hosted MX3D's Amsterdam stainless-steel bridge and CyBe Construction deployments. The EU Construction Products Regulation 2024/3110 (in force March 2025) and EU Buildings Directive 2024 set lifecycle-emissions disclosure requirements that favor low-carbon printed construction.

Middle East and Africa

Middle East and Africa held 8.5% revenue share in 2025 valued at approximately USD 0.21 Billion, with Saudi Arabia forecast as the single fastest-growing country at a 35.4% CAGR through 2034. Dar Al Arkan and COBOD's three-story Riyadh villa printed in 26 days at less than EUR 10,000 in concrete cost validated commercial viability under Vision 2030's Building Technology Initiative targeting 70% homeownership. The UAE's 3D Printing Strategy targets 25% of new buildings using additive construction by 2030, with Dubai Municipality completing two-story administrative buildings via Apis Cor. Egypt's Orascom and Cairo NUCA partnerships expanded regional COBOD deployments.

Latin America

Latin America captured 2.8% revenue share in 2025 valued at approximately USD 0.07 Billion. Mexico led regional adoption through Mighty Buildings' factory in Sonora, and Brazil through Caxias do Sul residential pilots. Latin America remains a smaller revenue base because affordable housing programs lag North American and European procurement cadence, but COBOD partner deployments in Bolivia and Colombia signal expanding regional channel coverage through 2026.

Country Analysis

United States

The United States 3D printed construction market reached approximately USD 0.62 Billion in 2025, growing at a country-specific CAGR of 30.7% through 2034. Federal demand traces to the Department of Housing and Urban Development Housing Innovation Showcase grants, Department of Defense Unified Facilities Criteria updates governing 3D printed barracks, and the new ANSI/A3 R15.06-2025 robot safety standard published October 29, 2025. ICON anchors the country profile with 245-plus completed structures including Lennar's 100-home Wolf Ranch community in Georgetown, Texas, the Fort Bliss military barracks, and the El Cosmico 3D-printed hotel opening in Marfa during 2026. State-level programs include Texas SB 877 housing innovation provisions and the Austin-area infill ADU pathway under International Building Code alternative means and methods.

Saudi Arabia

Saudi Arabia generated approximately USD 0.13 Billion in 2025 3D printed construction revenue, growing at a country CAGR of 35.4% through 2034 (the highest single-country rate globally). Vision 2030's Building Technology Initiative under the Ministry of Housing targets 70% homeownership by 2030 and explicitly funds additive construction adoption. Dar Al Arkan partnered with COBOD International to complete the world's tallest on-site 3D printed building (a three-story 345 sqm villa) in Riyadh in 26 days at less than EUR 10,000 in printable concrete cost using D.fab 99%-local-materials formulation. NEOM's giga-projects include 3D printed component pilots across The Line and Trojena developments.

China

China recorded approximately USD 0.41 Billion in 2025 3D printed construction revenue with a country CAGR of 32.6% through 2034. Yingchuang Building Technique (Winsun) anchors the country profile through multi-story residential builds in Suzhou and Shanghai using contour crafting concrete extrusion technology, while Hebei Construction Group and Tsinghua University concrete bridge projects extend infrastructure applications. The 14th Five-Year Plan (2021-2025) identifies smart construction including 3D printing as a priority technology, with up to 30% subsidies for SME contractor adoption.

Germany

Germany generated approximately USD 0.18 Billion in 2025 3D printed construction revenue, with a country CAGR of 28.9% through 2034. The Federal Ministry for Housing, Urban Development and Building (BMWSB) supports additive construction under the Bauen Mit Beton initiative, while PERI Group operates as a COBOD strategic shareholder and partner deploying BOD2 printers across German residential pilots. The PERI three-story 3D printed building completed in 2021 in Beckum represented the first multi-story printed residential structure in Europe. Germany's installations of additive construction equipment grew alongside its 26,982 industrial robot installations in 2024 (32% of European total), and BSI cybersecurity certification of printer fleets entered standard procurement specifications during 2025.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Method

- Extrusion-Based 3D Printing

- Powder Bonding (Binder Jetting)

- Robotic Arm-Based 3D Printing

- Gantry-Based 3D Printing

- Crane-Based 3D Printing

- Hybrid 3D Printing Methods

By Material Type

- Concrete

- Cementitious Composites

- Mortar

- Geopolymer Materials

- Metals

- Plastics and Polymer Composites

- Fiber-Reinforced Materials

- Recycled and Sustainable Materials

- Others

By End-Use

- Residential Construction

- Single-Family Housing

- Multi-Family Housing

- Affordable Housing Projects

- Commercial Construction

- Office Buildings

- Retail Buildings

- Hospitality Facilities

- Educational Institutions

- Industrial Construction

- Warehouses

- Manufacturing Facilities

- Utility Buildings

- Infrastructure

- Bridges

- Pedestrian Walkways

- Drainage and Utility Structures

- Transportation Infrastructure Components

- Public and Government Projects

- Social Housing

- Military and Defense Facilities

- Disaster Relief and Emergency Shelters

By Construction Form

- Walls and Structural Components

- Entire Buildings

- Modular Units

- Prefabricated Components

- Architectural Elements

- Decorative Structures

- Bridges and Infrastructure Components

- Customized Construction Elements

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.45 B |

| Forecast Revenue (2034) | USD 28.50 B |

| CAGR (2025-2034) | 31.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Method, (Extrusion-Based 3D Printing, Powder Bonding (Binder Jetting), Robotic Arm-Based 3D Printing, Gantry-Based 3D Printing, Crane-Based 3D Printing, Hybrid 3D Printing Methods), By Material Type, (Concrete, Cementitious Composites, Mortar, Geopolymer Materials, Metals, Plastics and Polymer Composites, Fiber-Reinforced Materials, Recycled and Sustainable Materials, Others), By End-Use, (Residential Construction, Commercial Construction, Industrial Construction, Infrastructure, Public and Government Projects), By Construction Form, (Walls and Structural Components, Entire Buildings, Modular Units, Prefabricated Components, Architectural Elements, Decorative Structures, Bridges and Infrastructure Components, Customized Construction Elements) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ICON TECHNOLOGY, COBOD INTERNATIONAL, YINGCHUANG BUILDING TECHNIQUE (WINSUN), APIS COR, WASP S.R.L., CYBE CONSTRUCTION, XTREEE, MX3D, PERI GROUP, SIKA AG, CONTOUR CRAFTING CORPORATION, MIGHTY BUILDINGS, CONSTRUCTIONS-3D, TVASTA, HARCOURT TECHNOLOGIES, HYPERION ROBOTICS, LARGE-SCALE ADDITIVE MANUFACTURING (LSAM), BRANCH TECHNOLOGY, SQ4D, BUILDROID AI, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Robotic Arm-Based 3D Printing, Gantry-Based 3D Printing, Crane-Based 3D Printing, Hybrid 3D Printing Methods), By Material Type (Concrete, Cementitious Composites, Mortar, Geopolymer Materials, Metals, Plastics and Polymer Composites, Fiber-Reinforced Materials, Recycled and Sustainable Materials), By End-Use (Residential, Commercial, Industrial, Infrastructure, Public & Government Projects), By Construction Form (Walls and Structural Components, Entire Buildings, Modular Units, Prefabricated Components, Architectural Elements, Decorative Structures), Industry Region, Market Dynamics, Emerging Trends, Competitive Landscape, Key Players, Strategic Insights and Forecast 2026-2034")

, Robotic Arm-Based 3D Printing, Gantry-Based 3D Printing, Crane-Based 3D Printing, Hybrid 3D Printing Methods), By Material Type (Concrete, Cementitious Composites, Mortar, Geopolymer Materials, Metals, Plastics and Polymer Composites, Fiber-Reinforced Materials, Recycled and Sustainable Materials), By End-Use (Residential, Commercial, Industrial, Infrastructure, Public & Government Projects), By Construction Form (Walls and Structural Components, Entire Buildings, Modular Units, Prefabricated Components, Architectural Elements, Decorative Structures), Industry Region, Market Dynamics, Emerging Trends, Competitive Landscape, Key Players, Strategic Insights and Forecast 2026-2034")

, Robotic Arm-Based 3D Printing, Gantry-Based 3D Printing, Crane-Based 3D Printing, Hybrid 3D Printing Methods), By Material Type (Concrete, Cementitious Composites, Mortar, Geopolymer Materials, Metals, Plastics and Polymer Composites, Fiber-Reinforced Materials, Recycled and Sustainable Materials), By End-Use (Residential, Commercial, Industrial, Infrastructure, Public & Government Projects), By Construction Form (Walls and Structural Components, Entire Buildings, Modular Units, Prefabricated Components, Architectural Elements, Decorative Structures), Industry Region, Market Dynamics, Emerging Trends, Competitive Landscape, Key Players, Strategic Insights and Forecast 2026-2034")

Frequently Asked Questions

How big is the 3D Printed Construction Market?

The global 3D printed construction market was valued at USD 1.87 Billion in 2024 and USD 2.45 Billion in 2025, and is projected to reach USD 28.50 Billion by 2034, growing at a CAGR of 31.3% from 2026 to 2034. The market is driven by rising adoption of automated construction technologies, demand for affordable housing, and increasing focus on sustainable building solutions.

Who are the major players in the 3D Printed Construction Market?

ICON TECHNOLOGY, COBOD INTERNATIONAL, YINGCHUANG BUILDING TECHNIQUE (WINSUN), APIS COR, WASP S.R.L., CYBE CONSTRUCTION, XTREEE, MX3D, PERI GROUP, SIKA AG, CONTOUR CRAFTING CORPORATION, MIGHTY BUILDINGS, CONSTRUCTIONS-3D, TVASTA, HARCOURT TECHNOLOGIES, HYPERION ROBOTICS, LARGE-SCALE ADDITIVE MANUFACTURING (LSAM), BRANCH TECHNOLOGY, SQ4D, BUILDROID AI, OTHERS

Which segments covered the 3D Printed Construction Market?

By Method, (Extrusion-Based 3D Printing, Powder Bonding (Binder Jetting), Robotic Arm-Based 3D Printing, Gantry-Based 3D Printing, Crane-Based 3D Printing, Hybrid 3D Printing Methods), By Material Type, (Concrete, Cementitious Composites, Mortar, Geopolymer Materials, Metals, Plastics and Polymer Composites, Fiber-Reinforced Materials, Recycled and Sustainable Materials, Others), By End-Use, (Residential Construction, Commercial Construction, Industrial Construction, Infrastructure, Public and Government Projects), By Construction Form, (Walls and Structural Components, Entire Buildings, Modular Units, Prefabricated Components, Architectural Elements, Decorative Structures, Bridges and Infrastructure Components, Customized Construction Elements)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

3D Printed Construction Market

Published Date : 11 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date