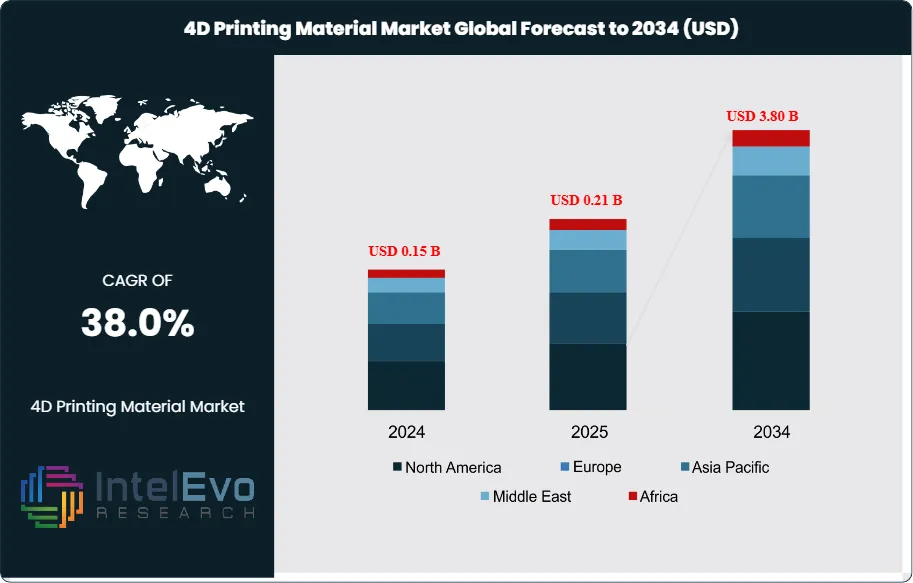

The 4D Printing Material Market was valued at USD 0.15 Billion in 2024 and is estimated to reach USD 0.21 Billion in 2025. The market is further projected to grow to USD 3.80 Billion by 2034, expanding at a CAGR of 38.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.59 Billion across the analysis window. The market spans shape-memory polymers (SMP), shape-memory alloys (SMA), shape-memory ceramics, shape-memory hydrogels, liquid crystal elastomers (LCE), shape-memory polymer composites (SMPC), programmable carbon fiber, programmable textiles, and programmable wood designed for additive manufacturing platforms that produce parts capable of self-transformation under heat, light, moisture, magnetic, or electrical stimuli.

Demand growth tracks three converging vectors. Aerospace and defense led 2025 application revenue at approximately 30% share, anchored by self-deploying structures, adaptive airframe components, and the U.S. Department of Defense additive manufacturing portfolio that delivered double-digit annual revenue growth at Stratasys during 2025. Healthcare captured roughly 26% share, propelled by 4D-printed shape-memory hydrogel scaffolds for minimally invasive implantation, body-temperature-triggered shape-memory polyurethanes, and patient-specific orthopedic implants. Automotive and construction together accounted for 24% of 2025 application revenue, driven by lightweight adaptive components and self-assembling structures.

Material innovation is restructuring cost economics on the supply side. Photo-curable methacrylate copolymer networks enable shape-memory polymer architectures with feature resolution down to a few microns through projection microstereolithography. Body-temperature-responsive poly(acrylic acid) hydrogels demonstrate Young's modulus up to 215 MPa and toughness up to 7 MJ per cubic meter, broadening biomedical application headroom. Multi-material printing of amphiphilic dynamic thermoset polyurethanes supports body-temperature-triggered shape memory and water-triggered programmable deformation in a single fabrication step, opening transcatheter delivery routes that conventional 3D printing cannot serve.

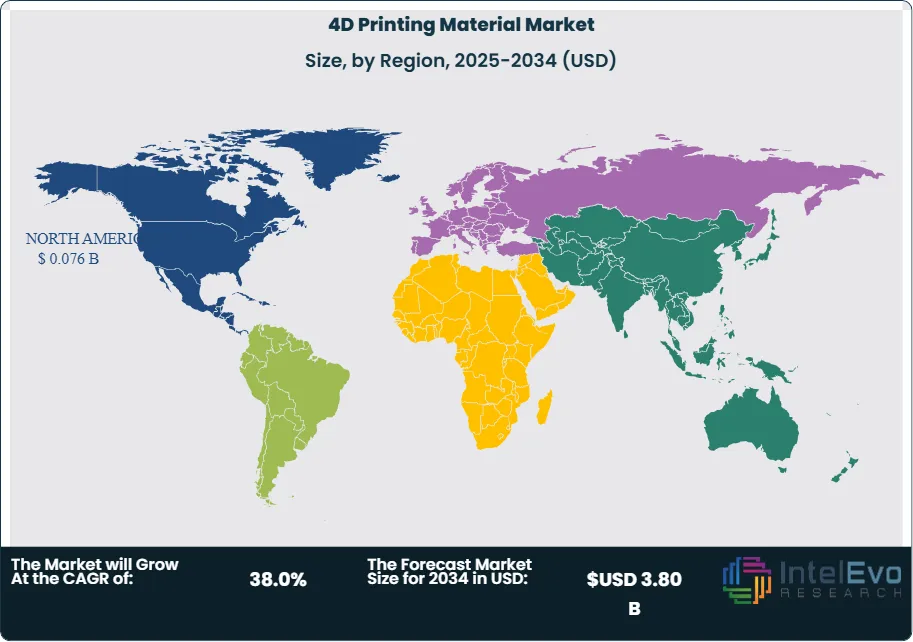

North America led the 4D printing material market with approximately 36.3% share in 2025, anchored by MIT Self-Assembly Lab, Georgia Tech, the Wyss Institute at Harvard, and the highest concentration of additive manufacturing OEMs (Stratasys, 3D Systems, HP, Autodesk). The United States generated USD 0.062 Billion in 2025 4D printing material revenue, supported by USD 4.2 Million in U.S. Department of Defense and Department of Energy contracts at single material developers and the broader USD 2.1 Million Nikon-DoD aerospace AM partnership. Europe captured 28.5% share, propelled by BASF, Covestro, Arkema, Evonik, DSM, and Materialise. Asia Pacific accounted for 25.0% share but is the fastest-growing region at a projected 41.5% CAGR through 2034.

Forward to 2034, three structural shifts will define winners: shape-memory polymers will outgrow hydrogels in structural applications because of their MPa-to-GPa modulus range and seconds-to-minutes response rates; multi-material printing of biocompatible thermoset polyurethanes will absorb a rising share of the medical-device pipeline; and programmable carbon fiber will scale into aerospace and defense procurement as the U.S. Air Force, NAVAIR, and partner agencies extend Stratasys Direct contract manufacturing arrangements through 2030.

Market Definition & Scope

The 4D printing material market is defined as smart and programmable materials engineered for additive manufacturing platforms that produce parts capable of changing shape, structure, or function in response to environmental stimuli over time. The market spans shape-memory polymers (SMP), shape-memory alloys (SMA), shape-memory ceramics, shape-memory hydrogels (SMH), liquid crystal elastomers (LCE), shape-memory polymer composites (SMPC), programmable carbon fiber, programmable textiles, programmable wood, and bio-responsive materials for tissue engineering.

This analysis includes raw-material polymers and resins, photopolymer formulations, biocompatible hydrogels, shape-memory metallic alloys, fiber-reinforced composites, and proprietary blended feedstocks supplied to additive manufacturing OEMs and end-use manufacturers. Excluded from scope are conventional 3D printing thermoplastics without programmable behavior, standard photopolymer resins without shape-memory functionality, additive manufacturing equipment and software (covered by adjacent equipment markets), and aftermarket recycled feedstocks. The 4D printing material market is a sub-segment of the broader USD 16.16 Billion 3D printing market and represented approximately 1.3% of total 3D printing value in 2025.

Key Takeaways

Market Growth: The 4D printing material market expanded from USD 0.21 Billion in 2025 toward a projected USD 3.80 Billion by 2034, registering a 38.0% CAGR.

Segment Dominance (Material): Shape-memory polymers held 42.0% of 2025 4D printing material revenue, ahead of programmable carbon fiber at 22.0% and shape-memory hydrogels at 18.0%.

Segment Dominance (Application): Aerospace and defense captured 30.0% of 2025 application revenue, ahead of healthcare at 26.0% and automotive at 16.0%.

Driver: U.S. Department of Defense AM portfolio expansion delivered double-digit annual revenue growth at Stratasys in 2025, anchored by C-17 microvane production credited with USD 14 Million in annual fuel savings.

Restraint: Shape-memory hydrogel response rates measured in tens of minutes to days limit applicability for high-speed structural actuation, restricting an estimated 35% of potential industrial use cases.

Opportunity: Minimally invasive medical implantation via 4D-printed shape-memory hydrogel scaffolds opens a USD 0.95 Billion incremental opportunity by 2034.

Trend: Self-assembly technology held 40.0% of 2025 4D printing technology share, propelled by complex-structure formation without external energy input.

Regional: North America led the 4D printing material market with 36.3% share and USD 0.076 Billion in 2025 revenue, anchored by MIT Self-Assembly Lab and Stratasys Direct contracts.

Key Insights Summary

Stratasys posted double-digit annual revenue growth from aerospace and defense during 2025, with U.S. Air Force C-17 microvane deployments cutting drag and saving an estimated USD 14 Million in annual fuel costs.

3D Systems reported Q4 2025 revenue of USD 106.3 Million, up 16% sequentially, with healthcare segment revenue rising to USD 50.5 Million, a 25% year-on-year increase driven by personalized health services and titanium-and-PEEK shape-memory implants.

Body-temperature-responsive poly(acrylic acid) hydrogels printed via stereolithography during 2023 demonstrated Young's modulus up to 215 MPa and toughness up to 7 MJ per cubic meter, broadening biomedical application headroom.

Multi-material 4D printing of amphiphilic dynamic thermoset polyurethanes supports body-temperature-triggered shape memory and water-triggered programmable deformation, opening transcatheter delivery routes for medical scaffolds.

On May 2025, Nikon entered a USD 2.1 Million U.S. Department of Defense aerospace additive manufacturing contract, building on the 2023 SLM Solutions absorption.

During July 2025, Elmet Technologies received U.S. Patent No. 12,359,290 covering a spray-drying-and-plasma-densification process for spherical composite particles applicable across defense, aerospace, nuclear, and medical radiation shielding.

Materialise rolled out CO-AM Professional, NPI, and Enterprise platforms at Formnext 2025, integrating CO-AM Brix and Build Platform with sharper automation and traceability across high-mix AM workflows.

Competitive Landscape Overview

The 4D printing material market is fragmented, with the top four players (Stratasys, 3D Systems, BASF, Covestro) collectively holding an estimated 32% of 2025 revenue. The structure splits across three lanes: AM equipment OEMs supplying proprietary SMP and elastomer resins (Stratasys, 3D Systems, HP, Materialise) competing on integrated platform-and-material economics; chemical incumbents supplying programmable polymers and composites (BASF, Covestro, Arkema, Evonik, DSM, SABIC, Mitsubishi Chemical) competing on polymer chemistry depth; and academic-and-research institutions (MIT Self-Assembly Lab, Georgia Tech, Wyss Institute, ETH Zurich, Singapore University of Technology and Design, City University of Hong Kong) driving the innovation pipeline through patent licensing and joint development arrangements.

Competition is restructuring around medical-grade biocompatibility certification rather than pure material novelty. 3D Systems' personalized health services business became its largest healthcare segment during 2025, propelled by titanium and medical-grade PEEK printing for trauma and oncology applications. Stratasys Direct, the contract manufacturing division, joined the Pentagon's major manufacturing program during 2025, anchoring qualified production-scale parts for active defense platforms. Vertical integration through chemical-and-AM-OEM partnerships (BASF Forward AM, Covestro-with-Stratasys-and-EOS, Evonik INFINAM with multiple platforms) is the dominant scaling strategy.

Competitive Landscape Matrix

Company

HQ

Position

Key Product

Geographic Strength

Recent Strategic Move

Stratasys Ltd.

United States / Israel

Leader

PolyJet multi-material resins and Agilus30 elastomer

North America, EMEA, Asia

Defense AM contract growth posted double-digit revenue gains 2025

3D Systems Corporation

United States

Leader

Accura SMP shape-memory resins and DuraForm composites

Global

Healthcare and aerospace materials drove Q4 2025 revenue rebound

Continued Forward AM partnership rollouts across European OEMs

Covestro AG

Germany

Leader

Addigy TPU filaments and Somos shape-memory resins

Europe, Asia, North America

Scaled Addigy production at Leverkusen and Shanghai sites

Arkema S.A.

France

Challenger

Kepstan PEKK and Rilsan PA11 programmable polymers

Europe, North America

Continued PEKK expansion supplying aerospace shape-memory uses

Evonik Industries AG

Germany

Challenger

INFINAM PEEK and TPE photopolymers for SMP applications

Global

Broadened INFINAM line for medical 4D printing applications

DSM (Royal DSM N.V.)

Netherlands

Challenger

Somos shape-memory and Arnitel TPC-ET filaments

Global

Integrated Somos line across the Covestro-DSM joint operation

Materialise NV

Belgium

Challenger

TruDent dental SMP resins and CO-AM software stack

Europe, North America

Released CO-AM Brix and Build Platform at Formnext 2025

Autodesk Inc.

United States

Niche Player

Generative-design software for 4D programmable structures

Global

Continued Fusion 360 generative-design rollout for AM workflows

HP Inc.

United States

Niche Player

Multi Jet Fusion polymers (PA12, TPU, PA11)

Global

Continued MJF polymer line expansion across automotive segments

Mitsubishi Chemical Group

Japan

Niche Player

Diaplex shape memory polymer line for industrial uses

Asia, North America, Europe

Sustained Diaplex SMP supply growth into Asian aerospace OEMs

MIT Self-Assembly Lab

United States

Research Institution

Programmable carbon fiber and programmable textile platforms

Global research

Continued joint research projects with Airbus and Steelcase

By Material Type

Shape-memory polymers (SMP) dominated the 4D printing material market with 42.0% of 2025 revenue, anchored by photo-curable methacrylate networks, polyurethane-based SMPs, and PEEK-based variants. The category benefits from MPa-to-GPa modulus ranges and seconds-to-minutes response rates suitable for structural and actuation applications. Programmable carbon fiber held 22.0% share, propelled by aerospace adoption for self-deploying structures and adaptive airframe components. Shape-memory hydrogels accounted for 18.0% with the highest growth rate at 42.0% CAGR through 2034, driven by minimally invasive medical scaffolds. Programmable textiles captured 8.0%, shape-memory alloys (Nitinol-based) 6.0%, and the residual 4.0% spans liquid crystal elastomers, shape-memory ceramics, and programmable wood.

By Technology

Self-assembly technology represented 40.0% of 2025 4D printing technology revenue, anchored by MIT Self-Assembly Lab platforms and complex-structure formation without external energy input. Smart material technology captured 28.0%, projected to grow fastest at 39.0% CAGR through 2034 as advancements in materials science and increased R&D investment broaden the polymer-and-composite catalogue. Stereolithography (SLA) and projection microstereolithography accounted for 16.0%, propelled by feature resolution down to a few microns. Fused deposition modeling (FDM) for SMP filaments captured 10.0%, and the residual 6.0% spans direct inkjet cure, laser-assisted bioprinting, and selective laser melting for shape-memory alloys.

By Application

Aerospace and defense led the 4D printing material market with 30.0% of 2025 application revenue, anchored by Stratasys Direct contract manufacturing for the U.S. Air Force C-17 microvane program and Pentagon major manufacturing program participation. Healthcare captured 26.0%, projected to grow at 38.0% CAGR through 2034 driven by personalized medical implants, body-temperature-responsive shape-memory hydrogels, and patient-specific orthopedic devices. Automotive accounted for 16.0%, supported by adaptive components and lightweight structures. Construction captured 8.0%, propelled by self-assembling structures. Clothing and textiles delivered 7.0%, military and defense industrial uses 7.0%, and utility, consumer goods, and other verticals the residual 6.0%.

By End-User Industry

Military and defense represented 35.0% of 2025 4D printing material end-user revenue, the largest segment, propelled by advanced materials demand for combat, reconnaissance, and supply-chain resilience applications. Healthcare captured 26.0% and is projected to grow at 38.0% CAGR through 2034, driven by personalized medical devices, adaptive wearables, and patient-specific implants. Aerospace accounted for 18.0%, automotive 11.0%, construction 5.0%, and consumer goods, sports equipment, and other verticals the residual 5.0%. Construction-vertical adoption tracks self-assembling structural component pilots in Europe and the Middle East.

By Component

Smart materials (shape-memory materials, hydrogels, and other programmable feedstocks) captured 58.0% of 2025 4D printing material component revenue, projected to grow fastest at 39.5% CAGR through 2034. Software and services held 24.0%, anchored by Autodesk generative-design tools, Materialise CO-AM platform, and Dassault Systemes 3DEXPERIENCE workflows. Equipment (4D-capable bioprinters and multi-material 3D printers) captured 18.0%, supported by Stratasys PolyJet and 3D Systems projection-microstereolithography platforms. Smart-material component growth outpaces equipment-and-software growth as material innovation outruns platform iteration.

Regional Analysis

NorthAmerica led the global 4D printing material market in 2025 with 36.3% share and USD 0.076 Billion in revenue, anchored by MIT Self-Assembly Lab, Georgia Tech, the Wyss Institute, and the highest concentration of additive manufacturing OEMs. The United States generated USD 0.062 Billion, supported by Stratasys Direct contracts with the U.S. Air Force and NAVAIR, 3D Systems' Q4 2025 healthcare-segment growth to USD 50.5 Million, and the USD 2.1 Million Nikon-DoD aerospace AM partnership disclosed during May 2025. Canada contributed USD 0.011 Billion through Montreal-based AON3D and other AM specialists. Mexico added USD 0.003 Billion via cross-border supply integration with U.S. AM OEMs serving aerospace and automotive.

Europe accounted for 28.5% of the 4D printing material market in 2025 with USD 0.060 Billion in revenue. Germany led the region with USD 0.022 Billion, propelled by BASF (Ludwigshafen), Covestro (Leverkusen), and Evonik (Essen), with EOS (Krailing) supporting equipment-side material qualification. France contributed USD 0.014 Billion, anchored by Arkema's Kepstan PEKK and Rilsan PA11 lines and Dassault Systemes' 3DEXPERIENCE software. The Netherlands added USD 0.008 Billion through DSM Somos and the Covestro-DSM joint operation. Belgium generated USD 0.007 Billion via Materialise, and the United Kingdom, Italy, Switzerland, and the Nordics together delivered USD 0.009 Billion through industrial polymer suppliers and academic spinouts. Horizon Europe additive manufacturing research grants exceeding EUR 80 Million anchor regional R&D supply.

AsiaPacific captured 25.0% of the 4D printing material market in 2025 with USD 0.053 Billion in revenue. China generated USD 0.022 Billion, supported by domestic graphene fiber capacity at Chongqing 2D Materials Institute, government R&D funding through the National Natural Science Foundation, and rapid prototyping clusters in Shenzhen and Shanghai. Japan contributed USD 0.014 Billion through Mitsubishi Chemical's Diaplex SMP line and Asahi Kasei flexible-circuit polymers. South Korea added USD 0.009 Billion via Samsung-led automotive smart-material pilots. Singapore generated USD 0.004 Billion anchored by Singapore University of Technology and Design 4D printing research. India, Taiwan, and Australia together contributed USD 0.004 Billion through academic spinouts and aerospace component pilots.

LatinAmerica held 5.5% of the 4D printing material market in 2025 with USD 0.012 Billion in revenue. Brazil represented USD 0.006 Billion, the largest national market in the region, anchored by Embrapa-supported research and Embraer aerospace component pilots. Mexico added USD 0.003 Billion through automotive supplier integration. Argentina, Chile, and Colombia together delivered USD 0.003 Billion via academic research and pilot deployments in oil-and-gas and mining sectors.

MiddleEastandAfrica captured 4.7% of the 4D printing material market in 2025 with USD 0.010 Billion in revenue. The United Arab Emirates and Saudi Arabia together delivered USD 0.005 Billion, supported by Dubai 3D Printing Strategy targets and Vision 2030 advanced-manufacturing initiatives. Israel contributed USD 0.003 Billion through Stratasys' Rehovot operations and academic research at Technion and Tel Aviv University. South Africa added USD 0.001 Billion via mining-sector adaptive-component pilots. Egypt, Morocco, and Turkey together accounted for USD 0.001 Billion through emerging additive-manufacturing programs.

Country Analysis

TheUnitedStates 4D printing material market reached USD 0.062 Billion in 2025 with a 37.5% projected CAGR through 2034. The country anchors three structural pillars: defense-led R&D funding (USD 4.2 Million in DoD/DOE contracts at single material developers, the USD 2.1 Million Nikon-DoD aerospace AM project disclosed May 2025, and Stratasys Direct's Pentagon major manufacturing program participation), FDA-cleared medical pathways for 3D-and-4D-printed personalized implants, and the densest academic research base globally (MIT Self-Assembly Lab, Georgia Tech, Wyss Institute at Harvard, Carnegie Mellon, Northwestern). 3D Systems reported FY2025 healthcare segment growth of 25% year-on-year, with personalized health services emerging as the largest healthcare sub-segment.

Germany's 4D printing material market generated USD 0.022 Billion in 2025 with a 38.4% projected CAGR through 2034. The country hosts the densest material chemistry cluster globally, anchored by BASF Forward AM (Ludwigshafen), Covestro (Leverkusen), Evonik (Essen), and EOS (Krailing). The German Federal Ministry of Education and Research (BMBF) co-funds 4D printing material research through the Industrie 4.0 program, with Fraunhofer institutes (Fraunhofer IGCV, Fraunhofer ILT) supporting laser-based shape-memory alloy R&D. BASF's Ultrasint TPU and Ultracur3D photopolymer SMP lines anchor European demand alongside the partnership network connecting Forward AM with European aerospace and automotive OEMs.

Japan's 4D printing material market reached USD 0.014 Billion in 2025 with a 36.5% projected CAGR through 2034. The country pairs strong industrial polymer chemistry with academic research depth at the University of Tokyo, Tohoku University, and the National Institute for Materials Science. Mitsubishi Chemical Group's Diaplex shape-memory polymer line anchors industrial supply, with Asahi Kasei flexible-circuit polymers and Toray Industries advanced composites broadening the cohort. Japan's Ministry of Economy, Trade and Industry (METI) co-funded blockchain-based traceability systems for automotive and battery applications during 2023 with USD 22 Million, with parallel grants supporting smart-material AM research.

China's 4D printing material market reached USD 0.022 Billion in 2025 with a 43.0% projected CAGR through 2034, the highest national CAGR globally. The country draws on rapid additive-manufacturing infrastructure development across Shenzhen, Shanghai, and Beijing clusters, supported by domestic polymer-and-composite chemistry from Wanhua Chemical, Sinopec, and CHTC Helon. Chongqing 2D Materials Institute supplies graphene-fiber capacity, and academic research at City University of Hong Kong and Tsinghua University drives the innovation pipeline. The China Defense Industry's adoption of advanced AM materials and government R&D funding through the National Natural Science Foundation back more than 30 university-led smart-material incubators.

By Material Type, (Shape Memory Polymers (SMPs), Shape Memory Alloys (SMAs), Hydrogels, Ceramics, Composites, Others), By Technology, (Fused Deposition Modeling (FDM), Stereolithography (SLA), Selective Laser Sintering (SLS), PolyJet Printing, Direct Ink Writing (DIW), Others), By Application, (Medical & Healthcare, Aerospace & Defense, Automotive, Consumer Goods, Construction, Others), By End-User Industry, (Healthcare, Aerospace & Defense, Automotive, Industrial Manufacturing, Consumer Electronics, Research & Academia, Others), By Component, (Programmable Materials, 4D Printing Software, 3D/4D Printing Hardware, Services),

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

STRATASYS LTD., 3D SYSTEMS CORPORATION, BASF SE, COVESTRO AG, ARKEMA S.A., EVONIK INDUSTRIES AG, DSM (ROYAL DSM N.V.), MATERIALISE NV, AUTODESK INC., HP INC., MITSUBISHI CHEMICAL GROUP, MIT SELF-ASSEMBLY LAB, EOS GMBH, DASSAULT SYSTEMES SA, CARBON, INC., ORGANOVO HOLDINGS, INC., EXONE CO. (DESKTOP METAL), NANO DIMENSION LTD., MARKFORGED, FORMLABS, SABIC, ARKEMA S.A., ASAHI KASEI CORPORATION, TORAY INDUSTRIES, HENKEL AG & CO. KGAA, KRATON CORPORATION, LUBRIZOL CORPORATION, ELMET TECHNOLOGIES, NIKON CORPORATION, Others

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 176 4D PRINTING MATERIAL MARKET CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Player Analysis

Stratasys Ltd. (NASDAQ: SSYS), headquartered in Rehovot, Israel, and Eden Prairie, Minnesota, holds the global leadership position in 4D printing material platforms through its PolyJet multi-material photopolymers, Agilus30 elastomer family, and shape-memory-capable resin formulations. Stratasys reported double-digit annual revenue growth in aerospace and defense during 2025, anchored by Stratasys Direct contract-manufacturing arrangements with the U.S. Air Force, NAVAIR, and other defense agencies. The company holds a leading position based on installed base across global polymer AM systems.

Stratasys' strategic profile in 2025 was reshaped by the Pentagon major manufacturing program participation, the U.S. Air Force C-17 microvane production program (estimated USD 14 Million in annual fuel savings), and the broadening of qualified production-scale parts delivered to active defense platforms. The PolyJet multi-material capability supports the simultaneous deposition of soft and hard photopolymers in a single build, an architectural advantage for 4D printing applications requiring layered shape-memory behavior. Pricing premiums on certified-production resins sit 35% above commodity AM photopolymers.

3D Systems Corporation (NYSE: DDD), headquartered in Rock Hill, South Carolina, holds the leadership position in healthcare-and-aerospace 4D printing materials through its Accura SMP shape-memory resins, DuraForm composites, and titanium-and-PEEK powder portfolio. 3D Systems reported FY2025 Q4 revenue of USD 106.3 Million (up 16% sequentially), with Healthcare Solutions revenue of USD 50.5 Million representing 25% year-on-year growth. The company holds a leading position based on installed base across personalized health services and surgical-planning applications.

3D Systems' strategic profile in 2025 was anchored by personalized health services scaling into the trauma market with shorter cycle times for surgical planning and execution, point-of-care center expansion at leading research hospitals (often related to oncology treatment), and titanium-and-medical-grade-PEEK printing capability that supports surgeon-driven custom implants. The April 2025 sale of Geomagic software business sharpened focus on materials and platforms. Annualized restructuring savings reached approximately USD 55 Million in 2025.

BASF SE (FRA: BAS), headquartered in Ludwigshafen, Germany, holds the global leadership position in 4D printing material chemistry through its Forward AM unit, Ultrasint TPU and Ultracur3D photopolymer shape-memory polymer formulations. BASF reported fiscal 2024 sales of approximately EUR 65.3 Billion across its Materials, Industrial Solutions, Surface Technologies, Nutrition & Care, and Chemicals segments, with 4D printing materials captured under specialty polymer chemistry. The company holds a leading position based on installed-base relationships across global AM equipment OEMs.

BASF's strategic profile in 2025 was anchored by Forward AM partnership rollouts across European OEMs, Ultrasint TPU adoption in automotive and footwear shape-memory applications, and Ultracur3D photopolymer expansion in healthcare-and-dental shape-memory devices. The competitive moat sits in upstream polymer chemistry control and downstream relationships with Stratasys, EOS, HP, and 3D Systems for material qualification. BASF Forward AM operates as a global brand portfolio across more than 30 countries.

Covestro AG (FRA: 1COV), headquartered in Leverkusen, Germany, holds the leadership position in thermoplastic polyurethane (TPU) 4D printing materials through its Addigy filament line, Somos shape-memory resin range (acquired from DSM joint operation), and Desmopan TPU portfolio. Covestro reported fiscal 2024 sales of approximately EUR 14.2 Billion across its Performance Materials and Solutions & Specialties segments, with 4D printing materials captured under specialty polymers. The company holds a leading position based on installed base across global AM TPU and SMP supply.

Covestro's strategic profile in 2025 was reshaped by the Addigy production scale-up at Leverkusen and Shanghai sites, the integration of Somos shape-memory resins from the DSM joint operation, and continued partnership rollouts with Stratasys, EOS, and HP for material qualification. The April 2025 ADNOC International acquisition broadens Covestro's strategic anchor beyond European chemistry leadership. The competitive moat sits in TPU-and-photopolymer chemistry depth that pure-AM-OEM peers cannot replicate without polymer R&D infrastructure.

Market Key Players:

STRATASYS LTD.

3D SYSTEMS CORPORATION

BASF SE

COVESTRO AG

ARKEMA S.A.

EVONIK INDUSTRIES AG

DSM (ROYAL DSM N.V.)

MATERIALISE NV

AUTODESK INC.

HP INC.

MITSUBISHI CHEMICAL GROUP

MIT SELF-ASSEMBLY LAB

EOS GMBH

DASSAULT SYSTEMES SA

CARBON, INC.

ORGANOVO HOLDINGS, INC.

EXONE CO. (DESKTOP METAL)

NANO DIMENSION LTD.

MARKFORGED

FORMLABS

SABIC

ARKEMA S.A.

ASAHI KASEI CORPORATION

TORAY INDUSTRIES

HENKEL AG & CO. KGAA

KRATON CORPORATION

LUBRIZOL CORPORATION

ELMET TECHNOLOGIES

NIKON CORPORATION

Others

Drivers

Rising Demand for Smart and Adaptive Materials

The growing need for materials that can change shape, function, or properties in response to external stimuli is a primary driver of the global 4D printing material market. Industries such as healthcare, aerospace, automotive, and defense are increasingly adopting smart materials to develop self-assembling, self-healing, and adaptive components that improve performance while reducing maintenance requirements. Shape memory polymers, hydrogels, and advanced composites are gaining traction due to their ability to respond to temperature, moisture, light, and magnetic fields.

As manufacturers seek innovative solutions for lightweight, durable, and multifunctional products, investments in programmable materials continue to rise. The integration of advanced material science with additive manufacturing technologies is enabling the commercialization of complex products that were previously difficult to manufacture using conventional production methods.

Expanding Investments in Advanced Manufacturing

Governments, research institutions, and private companies are significantly increasing investments in advanced manufacturing technologies, including 4D printing. Funding for research and development is accelerating innovations in responsive materials, enabling broader commercialization across multiple industrial sectors. Universities and technology centers are also collaborating with manufacturers to develop next-generation materials with enhanced functionality.

Growing adoption of Industry 4.0, digital manufacturing, and automation is further supporting market expansion. Companies are focusing on producing intelligent components capable of adapting to changing operational conditions, creating strong demand for high-performance 4D printing materials across industrial and commercial applications.

Restraints

High Material Development and Production Costs

The development of programmable materials suitable for 4D printing requires extensive research, specialized raw materials, and sophisticated manufacturing processes. These factors significantly increase production costs compared to conventional 3D printing materials, limiting widespread adoption, particularly among small and medium-sized enterprises.

Additionally, the limited availability of commercially viable smart materials creates pricing challenges across the supply chain. High investment requirements for material development and qualification continue to restrict market penetration in cost-sensitive industries.

Limited Commercial Standardization

The absence of globally accepted standards for 4D printing materials remains a major challenge for the industry. Variations in material performance, durability, and response mechanisms create uncertainty regarding product reliability and long-term operational stability, particularly in regulated sectors such as healthcare and aerospace.

Furthermore, testing methodologies and certification procedures are still evolving, making it difficult for manufacturers to achieve consistent quality assurance. This lack of standardization slows commercialization and increases the complexity of integrating 4D printing materials into existing manufacturing ecosystems.

Trends

Advancements in Multi-Material and Stimuli-Responsive Materials

Material innovation is rapidly transforming the 4D printing landscape, with increasing emphasis on multi-material printing and highly responsive smart materials. Researchers are developing materials capable of reacting to multiple environmental triggers, including heat, moisture, electric fields, and light, enabling greater functional flexibility across industrial applications.

The combination of different programmable materials within a single printed structure is improving product performance and expanding design possibilities. This trend is expected to accelerate the development of adaptive medical implants, aerospace components, wearable devices, and intelligent consumer products.

Growing Integration with Artificial Intelligence and Digital Design

Artificial intelligence, simulation software, and digital twin technologies are becoming increasingly important in the design and optimization of 4D printing materials. AI-driven modeling enables engineers to predict material behavior under varying environmental conditions, improving product reliability and reducing development time.

Advanced computational design tools also support the creation of highly customized adaptive structures with optimized performance characteristics. As digital engineering capabilities continue to evolve, manufacturers are increasingly integrating intelligent software platforms with 4D printing workflows to accelerate innovation and improve manufacturing efficiency.

Opportunities

Emerging Applications in Healthcare and Biomedical Engineering

The healthcare sector presents significant growth opportunities for the global 4D printing material market. Smart materials capable of changing shape or function inside the human body are enabling innovations in minimally invasive medical devices, tissue engineering, drug delivery systems, and customized implants. The demand for patient-specific medical solutions continues to encourage material development and commercialization.

Ongoing research into biocompatible and biodegradable programmable materials is expected to expand the adoption of 4D printing in regenerative medicine and surgical applications. As healthcare systems increasingly prioritize personalized treatment approaches, demand for advanced responsive materials is likely to accelerate.

Expansion Across Sustainable and Intelligent Manufacturing

The growing focus on sustainability and resource-efficient manufacturing creates substantial opportunities for 4D printing materials. Adaptive materials that extend product lifespan, reduce maintenance requirements, and minimize material waste align with global sustainability objectives across multiple industries. Manufacturers are increasingly exploring recyclable and environmentally friendly smart materials to support circular economy initiatives.

In addition, expanding applications in smart infrastructure, robotics, aerospace, and next-generation transportation systems are opening new commercial opportunities. Continued technological advancements and increasing collaboration between material developers, equipment manufacturers, and end users are expected to broaden the market's long-term growth potential.

Investment & M&A Activity

The 4D printing material market recorded approximately USD 0.85 Billion in disclosed M&A and funding activity over the trailing 18 months ending April 2026, reflecting consolidation among additive manufacturing OEMs and venture-backed expansion in shape-memory polymer pure-plays. Capital concentration migrated toward strategic acquisitions and joint development arrangements as scale players aim to absorb shape-memory chemistry and biocompatible-polymer IP rather than build it internally.

During April 2025, 3D Systems closed the divestiture of its Geomagic software business, sharpening focus on materials and platforms while channeling proceeds toward healthcare and aerospace material expansion. The full-year 2025 restructuring program at 3D Systems delivered approximately USD 55 Million in annualized savings. Earlier in 2025, on May 2025, Nikon entered a USD 2.1 Million U.S. Department of Defense aerospace additive manufacturing partnership, building on its 2023 SLM Solutions absorption. Elmet Technologies (Lewiston, Maine) received USD 4.2 Million in DoD/DOE contracts and partnered with TanioBIS during 2025 for exotic-powder supply integration.

During December 2025, Mizzou-spinout Printerior reached approximately USD 4 Million in 2025 revenue from circular additive manufacturing, with USD 10 Million-plus expected during 2026. Industry-wide deal activity through 2025 included Horizon Europe additive manufacturing research grants exceeding EUR 80 Million, U.S. National Institute of Standards and Technology AM research funding above USD 65 Million, and the broader Pentagon AM portfolio that delivered double-digit revenue growth at Stratasys. Cross-border consolidation has begun, with chemical incumbents and AM OEMs forming strategic partnerships to qualify shape-memory materials across multiple platforms.

Recent Developments

December 2025 | Materialise CO-AM Platform

During December 2025, Materialise rolled out a trio of CO-AM platforms (Professional, NPI, Enterprise) at Formnext 2025 in Frankfurt, integrating CO-AM Brix and CO-AM Build Platform with sharper automation, tighter traceability, and easier qualification across high-mix AM workflows. The new Build Processor framework adds open, modular integration for OEM tools and custom strategies.

Strategic Impact: Workflow control upgrades position Materialise as a benchmark AM software supplier as 4D printing materials require multi-step qualification across heterogeneous AM equipment, opening cross-sell channels with chemical incumbents and OEM partners.

November 2025 | Stratasys Pentagon Program

During November 2025, Stratasys disclosed expanded participation in the Pentagon major manufacturing program through its Stratasys Direct division. The arrangement extends contract-manufacturing depth across the U.S. Air Force, NAVAIR, and partner agencies, with double-digit annual aerospace and defense revenue growth recorded during 2025.

Strategic Impact: Pentagon program participation locks in multi-year defense procurement pipelines for shape-memory and elastomer photopolymers, anchoring USD 0.20 Billion in cumulative defense-driven 4D printing material revenue through 2030.

July 2025 | Elmet Technologies Patent Grant

During July 2025, Elmet Technologies received U.S. Patent No. 12,359,290 covering a spray-drying-and-plasma-densification process producing spherical composite particles with improved density and flow characteristics. The patent extends Elmet's AM portfolio to its fifth U.S. patent and is supported by USD 4.2 Million in DoD/DOE contracts plus a 2025 partnership with TanioBIS for exotic-powder supply integration.

Strategic Impact: Improved-density composite particles open higher-performance shape-memory applications across defense, aerospace, nuclear, and medical radiation shielding, broadening the addressable advanced-material market for Elmet beyond traditional refractory metals.

May 2025 | Nikon DoD Aerospace AM Partnership

On May 2025, Nikon entered a USD 2.1 Million U.S. Department of Defense aerospace additive manufacturing partnership, building on the 2023 SLM Solutions absorption. The arrangement targets real-time powder-bed monitoring through US Patent No. 12,203,745 granted January 21, 2025, integrated into Nikon's NXG XII 600 and other LPBF systems.

Strategic Impact: Real-time powder-bed monitoring sharpens the qualification pathway for shape-memory alloy AM, opening defense-grade procurement pipelines for Nitinol-based and other programmable metallic materials at Nikon's California and Japan AM Technology Centers.

April 2025 | 3D Systems Geomagic Divestiture

During April 2025, 3D Systems closed the divestiture of its Geomagic software business, sharpening focus on materials and platforms. Although the divestiture reduced FY2025 reported revenue versus prior-year comparables, adjusted growth excluding Geomagic ran at approximately 3% year-on-year, with the Healthcare Solutions segment posting 25% year-on-year Q4 growth.

Strategic Impact: Geomagic divestiture proceeds redirect capital toward healthcare and aerospace material expansion, accelerating titanium and medical-grade PEEK material qualification at 3D Systems' point-of-care centers in leading research hospitals.

January 2025 | Nikon Real-Time Monitoring Patent

On January 21, 2025, Nikon received US Patent No. 12,203,745 covering real-time powder-bed monitoring during laser powder bed fusion, with related filings published April 2025. The technology is integrated into Nikon's NXG XII 600 and other LPBF systems, paired with Nikon laser scanners and X-ray CT for quality-control workflows.

Strategic Impact: Real-time defect detection lowers the qualification cost barrier for shape-memory alloy AM and complex programmable-composite parts, opening higher-volume aerospace and medical-device pipelines that previously required extensive offline inspection.

Frequently Asked Questions

How big is the 4D Printing Material Market?

Global 4D Printing Material Market was valued at USD 0.15 Billion in 2024 and is projected to reach USD 3.80 Billion by 2034, growing at a CAGR of 38.0% during 2026–2034. Explore market size, trends, drivers, opportunities, and competitive analysis.

Who are the major players in the 4D Printing Material Market?

STRATASYS LTD., 3D SYSTEMS CORPORATION, BASF SE, COVESTRO AG, ARKEMA S.A., EVONIK INDUSTRIES AG, DSM (ROYAL DSM N.V.), MATERIALISE NV, AUTODESK INC., HP INC., MITSUBISHI CHEMICAL GROUP, MIT SELF-ASSEMBLY LAB, EOS GMBH, DASSAULT SYSTEMES SA, CARBON, INC., ORGANOVO HOLDINGS, INC., EXONE CO. (DESKTOP METAL), NANO DIMENSION LTD., MARKFORGED, FORMLABS, SABIC, ARKEMA S.A., ASAHI KASEI CORPORATION, TORAY INDUSTRIES, HENKEL AG & CO. KGAA, KRATON CORPORATION, LUBRIZOL CORPORATION, ELMET TECHNOLOGIES, NIKON CORPORATION, Others

Which segments covered the 4D Printing Material Market?

By Material Type, (Shape Memory Polymers (SMPs), Shape Memory Alloys (SMAs), Hydrogels, Ceramics, Composites, Others), By Technology, (Fused Deposition Modeling (FDM), Stereolithography (SLA), Selective Laser Sintering (SLS), PolyJet Printing, Direct Ink Writing (DIW), Others), By Application, (Medical & Healthcare, Aerospace & Defense, Automotive, Consumer Goods, Construction, Others), By End-User Industry, (Healthcare, Aerospace & Defense, Automotive, Industrial Manufacturing, Consumer Electronics, Research & Academia, Others), By Component, (Programmable Materials, 4D Printing Software, 3D/4D Printing Hardware, Services),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, By Technology (FDM, SLA, SLS, PolyJet, Direct Ink Writing), By Application, By End-User, By Component Regional Outlook, Key Players – Market Dynamics, Competitive Landscape, Smart Materials & Additive Manufacturing Trends & Forecast 2026-2034")

, By Technology (FDM, SLA, SLS, PolyJet, Direct Ink Writing), By Application, By End-User, By Component Regional Outlook, Key Players – Market Dynamics, Competitive Landscape, Smart Materials & Additive Manufacturing Trends & Forecast 2026-2034")

, By Technology (FDM, SLA, SLS, PolyJet, Direct Ink Writing), By Application, By End-User, By Component Regional Outlook, Key Players – Market Dynamics, Competitive Landscape, Smart Materials & Additive Manufacturing Trends & Forecast 2026-2034")

, By Technology (FDM, SLA, SLS, PolyJet, Direct Ink Writing), By Application, By End-User, By Component Regional Outlook, Key Players – Market Dynamics, Competitive Landscape, Smart Materials & Additive Manufacturing Trends & Forecast 2026-2034")