- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Account-to-Account (A2A) Payment Market Size | CAGR 14.2%

Global Account-to-Account Payment Market Size, Share, Analysis By Payment Type (Instant/Real-Time Payments, Batch & Bulk Transfers, Scheduled Payments), By Channel & Application (E-commerce Checkout, Bill Payments, P2P Transfers, B2B Corporate Payments, B2C Disbursements), By Technology (Open Banking APIs, Real-Time Clearing Rails, Proxy Directory Services), By End-User (BFSI, Retail, Utilities, Healthcare) Region & Key Players-Dynamics, Strategies & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

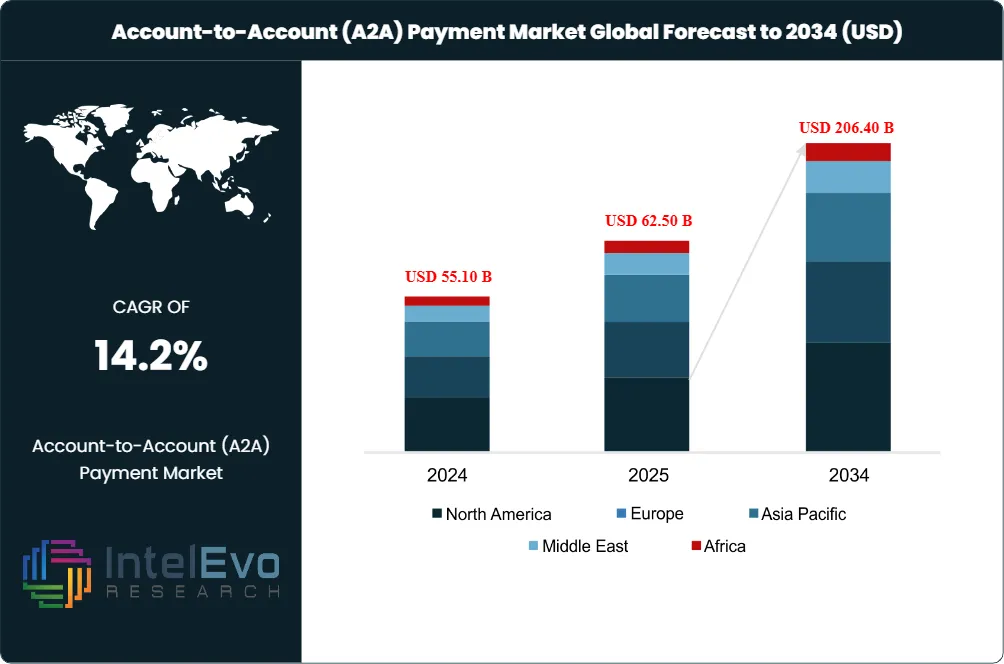

| USD 62.50 Billion | USD 206.40 Billion | 14.2% | Asia Pacific, 42.0% |

The Account-to-Account (A2A) Payment Market was valued at approximately USD 55.10 Billion in 2024 and approximately USD 62.50 Billion in 2025. The market is projected to reach approximately USD 206.40 Billion by 2034, expanding at a CAGR of 14.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of approximately USD 143.90 billion over the analysis period, positioning A2A payments as the fastest-growing structural shift in global payment economics since the card-network build-out of the 1990s.

Get More Information about this report -

Request Free Sample ReportThe primary demand driver is a cost-structure advantage that has become impossible for merchants and corporates to ignore: the U.S. Federal Reserve's FedNow instant payment service charges approximately USD 0.04 per transaction, compared with average credit card interchange fees of 2.0%-3.5% of the transaction value. This differential translates to annual savings of USD 1-2 million for a mid-size retailer processing USD 100 million in annual payments, a calculation now embedded in procurement decisions across retail, healthcare, insurance, and subscription commerce. Simultaneously, government-built real-time payment rails — India's Unified Payments Interface (UPI), Brazil's Pix, the EU's SEPA Instant Credit Transfer, and the U.K.'s Faster Payments Service — have eliminated the infrastructure gap that previously kept A2A confined to peer-to-peer transfers and large-value corporate settlements.

India's UPI processed 228.3 billion transactions in 2025, a 33% year-on-year increase, moving approximately USD 3.4 trillion in value and accounting for 84.8% of the country's retail digital payment volume. Brazil's Pix approached 7.9 billion monthly transactions in December 2025, with total 2025 transaction value reaching approximately USD 6.7 trillion. Together, these two systems account for the vast majority of global A2A transaction volume and demonstrate the demand-side conditions — zero-cost consumer transfers, ubiquitous QR-code acceptance, and biometric authentication — under which A2A displaces both cash and card payments at scale.

In Europe, the European Payments Initiative (EPI) brought its Wero digital wallet to e-commerce in Germany by November 2025, with Belgium, France, Luxembourg, and the Netherlands scheduled for progressive roll-out through 2026. Wero had surpassed 52 million registered consumers by March 2026, and its planned integration of iDEAL — which processes more than 70% of Dutch e-commerce payments — positions it to become the dominant European A2A brand. In the United States, FedNow and The Clearing House's RTP network together enable 78% of U.S. bank accounts for real-time credit settlement, though consumer adoption for merchant payments remains nascent at approximately 1.5% of all consumer transactions, per a PYMNTS and Trustly survey covering the 12 months ending June 2025.

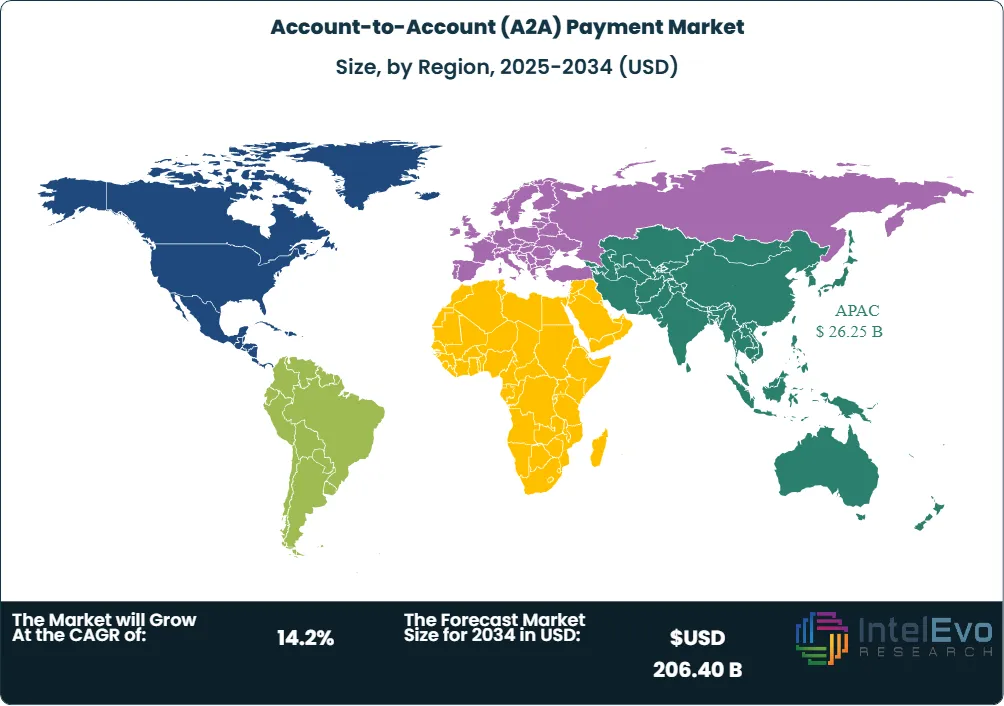

Asia Pacific led all regions with approximately 42.0% of global A2A payment market revenue in 2025, driven by UPI and the ASEAN QR-code interoperability framework. Europe held approximately 26.0%, anchored by SEPA Instant and the Wero expansion, while North America captured approximately 22.0%, where FedNow's institutional ramp-up and open banking regulatory momentum are beginning to unlock merchant-facing use cases. The competitive field spans global payment platforms — PayPal Holdings, Stripe, Adyen — alongside open-banking specialists including Plaid, Trustly, TrueLayer, and Token.io, each competing to own the A2A payment initiation layer between bank infrastructure and merchant checkout.

Through 2034, industry analysis projects that A2A will transition from a niche alternative to a core payment method across online, in-store, and B2B channels. The FIS Global Payments Report projects A2A will account for 11% of U.S. e-commerce transaction value by 2026, and the BIS Project Nexus initiative is designing cross-border interoperability bridges that could unify more than 100 national instant-payment schemes, making A2A the default rail for cross-border consumer and commercial payments in the decade ahead.

Market Definition & Scope

The account-to-account (A2A) payment market is defined as the global commercial supply of technology platforms, payment processing services, and infrastructure solutions that enable direct bank-to-bank fund transfers between payer and payee without routing through card network intermediaries such as Visa, Mastercard, or American Express. The market encompasses real-time payment rails (FedNow, RTP, SEPA Instant, UPI, Pix, Faster Payments), ACH-based batch transfers, open-banking-enabled payment initiation services under PSD2/PSD3 and analogous regulatory frameworks, and the software platforms (APIs, SDKs, fraud engines, account verification) that connect these rails to merchant checkout, corporate treasury, and consumer wallet applications.

This analysis covers P2P (person-to-person), P2M/C2B (person-to-merchant / consumer-to-business), B2B (business-to-business), and cross-border A2A payment flows across cloud and on-premises deployment models. Excluded from scope are card-on-file transactions that settle through Visa or Mastercard rails even when initiated from a digital wallet, pure cash remittance services without digital origination, and central bank digital currency (CBDC) pilot programmes that have not reached commercial deployment. The A2A payment market sits within the broader global digital payments market, which processed approximately USD 24.07 trillion in total transaction value in 2025.

, By Channel & Application (E-commerce Checkout, Bill Payments, P2P Transfers, B2B Corporate Payments, B2C Disbursements), By Technology (Open Banking APIs, Real-Time Clearing Rails, Proxy Directory Services), By End-User (BFSI, Retail, Utilities, Healthcare) Region & Key Players-Dynamics, Strategies & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global account-to-account payment market was valued at approximately USD 62.50 billion in 2025 and is projected to reach approximately USD 206.40 billion by 2034, at a CAGR of 14.2%, representing an absolute opportunity of approximately USD 143.90 billion.

- Segment Dominance (By Channel): The online and e-commerce channel held the largest share at approximately 42.0% in 2025, driven by open-banking-enabled checkout buttons, SEPA Instant merchant acceptance, and India's UPI integration into e-commerce platforms where QR-code payments dominate.

- Segment Dominance (By End-User): The BFSI segment accounted for approximately 34.0% of total market revenue in 2025, as banks deploy A2A rails for corporate treasury management, payroll disbursement, and inter-bank settlement alongside consumer-facing services like pay-by-bank.

- Driver: Transaction cost compression represents the primary structural driver; FedNow's per-transaction fee of approximately USD 0.04 versus credit card interchange of 2.0%-3.5% creates a measurable savings incentive that scales linearly with merchant payment volume, making A2A adoption a procurement optimization rather than a technology experiment.

- Restraint: Consumer awareness and trust remain the primary constraint in North American and certain Western European markets, where card reward programmes and chargeback protections create behavioural inertia; only 1.5% of U.S. consumer transactions used pay-by-bank in the 12 months ending June 2025.

- Opportunity: Cross-border A2A interoperability, driven by the BIS Project Nexus framework targeting unification of 100+ national instant-payment schemes, represents the single largest addressable expansion opportunity, with global A2A cross-border transaction value projected to exceed USD 1.0 trillion by 2030.

- Trend: Agentic AI integration into A2A payment workflows for fraud prevention and transaction orchestration is accelerating, with the fraud detection market for AI-powered payment solutions projected to reach USD 37.76 billion by 2029, at a 48.7% CAGR.

- Regional: Asia Pacific led with approximately 42.0% of global market share in 2025, equating to approximately USD 26.25 billion, anchored by India's UPI (228.3 billion transactions, USD 3.4 trillion in value) and Indonesia's QRIS (18.6 billion transactions, up 47% year-on-year).

Key Insights Summary

- India's UPI processed 228.3 billion transactions in 2025, a 33% year-on-year increase from 172.2 billion in 2024, with approximately 500 million unique users by early 2026 and a daily average of 698 million transactions in December 2025 alone; UPI accounted for 84.8% of India's retail digital payment volume in the first half of 2025, making it the world's largest A2A payment system by transaction count.

- Brazil's Pix approached 7.9 billion monthly transactions in December 2025, with total 2025 transaction value reaching approximately USD 6.7 trillion — a 34% year-on-year increase — and 174 million individual consumers using the platform by March 2026, representing approximately 82% of Brazil's adult population.

- The European Payments Initiative's (EPI) Wero digital wallet surpassed 52 million registered consumers by March 2026, with the platform processing instant A2A payments through SEPA Instant Credit Transfer protocols across Germany, France, and Belgium; in March 2026, Global Payments' Worldpay division joined EPI as a Principal Member to enable Wero acceptance across its merchant network.

- In the United States, the FedNow instant payment service and The Clearing House's RTP network together cover 78% of U.S. bank accounts for real-time credit settlement; FedNow charges approximately USD 0.04 per transaction versus average credit card interchange of 2.0%-3.5%, creating a cost differential that A2A providers project will drive 11% of U.S. e-commerce value to A2A rails by 2026.

- Global A2A payment transactions are projected to increase from 60 billion in 2024 to 186 billion by 2029, a 209% increase, with transaction value rising from USD 1.7 trillion to USD 5.7 trillion over the same period; A2A's e-commerce share alone is forecast to grow from USD 525 billion in 2022 to approximately USD 850 billion by 2026.

- In October 2025, Razorpay, NPCI, and OpenAI initiated a pilot programme for agentic AI-powered payments on UPI, enabling conversational commerce where AI agents can initiate, verify, and complete payment transactions on behalf of consumers — a use case that could redefine A2A payment initiation from user-directed to AI-directed within the forecast period.

Competitive Landscape Overview

The global account-to-account payment market is moderately fragmented, with the top ten providers accounting for a majority of 2025 platform revenue but no single company commanding more than single-digit global market share. Competition operates across three distinct layers: infrastructure operators (central banks and clearing houses that own the real-time rails), payment initiation service providers (PISPs such as Trustly, TrueLayer, and Token.io that connect merchant checkout to bank infrastructure), and payment platforms (Stripe, Adyen, PayPal, Plaid) that embed A2A alongside card and wallet acceptance within unified commerce APIs.

The competitive dynamic shifted materially in 2025 as incumbent card networks mounted defensive responses: Visa's USD 1 billion acquisition of open-banking platform Tink and Mastercard's purchase of Aiia demonstrate that card-network companies view A2A not as a complementary channel but as a structural threat to interchange revenue. Global Payments completed its acquisition of Worldpay in January 2026 to form a combined commerce solutions provider and promptly joined EPI as a Principal Member to enable Wero A2A acceptance — signalling that acquirer-processor consolidation is driven partly by the need to offer merchants a multi-rail alternative that includes A2A alongside card acceptance. In Asia Pacific, competition is shaped primarily by sovereign rail dominance: NPCI's UPI in India and the Central Bank of Brazil's Pix leave limited space for private-sector intermediaries, pushing fintech innovation toward value-added layers such as fraud analytics, credit-on-UPI, and cross-border connectivity.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product/Platform | Geo Strength | Recent Strategic Move |

| PayPal Holdings | USA | Leader | PayPal, Venmo, Braintree, Xoom | Global | Processed USD 1.68T in total payment volume in 2024; integrated pay-by-bank checkout in 18 markets |

| Stripe, Inc. | USA/Ireland | Leader | Stripe Financial Connections, Stripe ACH, Link | N. America, Europe | Filed for a Georgia-based limited-purpose bank charter (Apr 2025) to secure direct payment network access |

| Adyen N.V. | Netherlands | Leader | Adyen Pay by Bank, iDEAL integration, SEPA | Europe, Global | Enabled Wero A2A acceptance for European merchants through its unified platform in early 2026 |

| Plaid Inc. | USA | Leader | Plaid Transfer, Plaid Signal, Plaid Link | N. America | Extended Plaid Transfer to support FedNow and RTP rails alongside ACH, providing unified multi-rail coverage |

| Trustly Group AB | Sweden | Challenger | Trustly Open Banking Payments, Pay N Play | Europe, N. America | Expanded U.S. pay-by-bank coverage to 12,000+ financial institutions via Open Banking APIs |

| TrueLayer | UK | Challenger | TrueLayer Payments, Payouts, Signup+ | Europe, UK | Secured GBP 50M Series E (2024) to scale Open Banking payment initiation across European markets |

| Token.io | UK | Challenger | Token A2A, Open Banking hub | Europe | Connected 5,000+ banks across 25 European markets for PSD2-compliant payment initiation |

| Nuvei Corporation | Canada | Niche Player | Nuvei A2A, Wero acceptance, iDEAL | Global | Became one of the first processors to go live with Wero e-commerce transactions (Nov 2025) |

| Dwolla, Inc. | USA | Niche Player | Dwolla ACH API, RTP, FedNow | N. America | Unified ACH, RTP, and FedNow rails under a single API for insurance and financial services verticals |

| Volt | UK | Niche Player | Volt real-time A2A, merchant gateway | Europe, LATAM | Entered Worldpay partnership to expand A2A acceptance to millions of merchants globally |

By Channel

The online and e-commerce channel captured approximately 42.0% of global A2A payment market revenue in 2025, the largest single channel, because the merchant checkout environment provides the most natural integration point for open-banking payment initiation. In the Netherlands, iDEAL — now migrating into Wero — processes more than 70% of domestic e-commerce transaction value, making A2A the default online payment method. In Brazil, Pix accounted for 24% of e-commerce value in 2024 and is projected to reach 58% within five years, according to the FIS Global Payments Report. The cost differential between A2A and card checkout is most visible in e-commerce because merchants bear interchange directly; A2A fees of 0.1%-0.5% per transaction compared with card fees of 1.5%-3.0% create a measurable margin improvement that e-commerce CFOs now model into quarterly financial planning. Stripe and Adyen integrated A2A acceptance into their checkout APIs in 2024-2025, reducing the technical barrier for merchants who previously needed separate integrations per rail.

The peer-to-peer (P2P) channel held approximately 28.0% of revenue in 2025 and remains the segment where A2A adoption is most mature. India's UPI began as a P2P system and still processes a significant share of P2P transfers, though person-to-merchant (P2M) now accounts for 63% of UPI volume as of May 2025. In Europe, Wero's initial launch focused on P2P transfers in Germany, France, and Belgium before extending to e-commerce; the platform reported 8 million P2P transactions before November 2024, establishing consumer familiarity. In the United States, Zelle processed USD 1 trillion in payments in 2024 across 2.9 billion transactions, cementing its position as the dominant domestic P2P rail.

Business-to-business (B2B) represented approximately 18.0% of channel revenue in 2025, driven by corporate treasury departments using SEPA Instant, RTP, and ACH for supplier payments, payroll, and inter-company transfers. ISO 20022 data-rich messaging adoption, mandated for cross-border SWIFT payments from November 2025, enhances reconciliation and automated matching for B2B A2A flows, addressing a historical barrier to adoption in complex supply-chain payment environments. In-store and point-of-sale (POS) A2A captured the remaining approximately 12.0%, a segment set for accelerated growth as QR-code-based merchant acceptance scales beyond Asia Pacific; Indonesia's QRIS processed 18.6 billion transactions in 2025, a 47% year-on-year increase, demonstrating the viability of A2A at physical retail.

By Deployment Mode

Cloud-based A2A payment solutions accounted for approximately 62.0% of market revenue in 2025, because the API-first architecture of modern A2A platforms — Stripe Financial Connections, Plaid Transfer, Dwolla, TrueLayer — is inherently cloud-native, enabling merchants and corporates to onboard, process, and reconcile bank payments without dedicated on-premises infrastructure. Cloud deployment eliminates the need for direct integration with individual clearing houses, as the provider abstracts rail selection (ACH, RTP, FedNow, SEPA Instant) into a single endpoint. Dwolla unified ACH, RTP, and FedNow rails under a single API, reducing integration time from months to days for insurance and financial services companies deploying A2A payout workflows.

On-premises deployment retained approximately 38.0% of market revenue in 2025, driven by large financial institutions, central counterparties, and government agencies with regulatory mandates for data residency, on-site audit access, and direct control over payment processing infrastructure. Banks participating directly in FedNow or RTP as settlement members typically maintain on-premises connections to clearing infrastructure, although they may overlay cloud-based service layers for merchant-facing APIs. The on-premises share is expected to contract gradually through the forecast period as regulatory frameworks — including the EU's Digital Operational Resilience Act (DORA) and revised PSD3 — establish cloud-specific compliance pathways that reduce the regulatory friction historically associated with cloud adoption in financial services.

By End-User Industry

The BFSI segment held approximately 34.0% of A2A payment market revenue in 2025, as banks and non-bank financial institutions are both the operators and the largest direct consumers of A2A infrastructure. Banks deploy A2A rails for internal settlement, corporate cash management products, payroll disbursement, and consumer-facing pay-by-bank services; fintech companies use A2A for wallet funding, investment account deposits, and loan disbursement. JPMorgan Chase and Mastercard jointly announced Pay-by-Bank, an ACH-based open-banking payment service for bill-pay and merchant checkout, expanding A2A from institutional settlement into consumer commerce. Retail and e-commerce represented approximately 30.0% of revenue, driven by merchant checkout integration and subscription billing use cases where the recurring nature of A2A debits reduces card-on-file churn. Healthcare captured approximately 10.0%, the fastest-growing vertical at an estimated CAGR above 18%, as telehealth billing, patient-responsibility payments, and insurance claim disbursements shift to instant A2A rails for faster fund availability. Government and public sector absorbed approximately 8.0%, with tax collection, social benefit disbursement, and utility payments increasingly routed through sovereign A2A rails.

Regional Analysis

Asia Pacific held the largest regional share of the global account-to-account payment market at approximately 42.0% in 2025, equating to approximately USD 26.25 billion. India dominates the region through UPI, which processed 228.3 billion transactions worth USD 3.4 trillion in 2025, with PhonePe (48.3% volume share) and Google Pay (37.0%) controlling more than 85% of UPI transaction flow. The Reserve Bank of India mandated zero merchant discount rates for UPI from 2019, removing acceptance cost barriers and enabling QR-code penetration across an estimated 600 million merchant endpoints. Indonesia's QRIS reached 18.6 billion transactions in 2025, a 47% year-on-year increase. Thailand's PromptPay, Singapore's PayNow, and Malaysia's DuitNow are interlinked through bilateral agreements, creating an ASEAN cross-border A2A corridor that the BIS is evaluating as a template for wider interoperability.

Europe captured approximately 26.0% of global market revenue in 2025, at approximately USD 16.25 billion. The EU's PSD2 regulatory framework created the legal foundation for open-banking payment initiation services, and the forthcoming PSD3 and Payment Services Regulation (PSR) will extend access rights and standardise API performance requirements. Wero's expansion across Germany, France, Belgium, Luxembourg, and the Netherlands through 2025-2026 is consolidating national A2A schemes — Giropay, Paylib, Payconiq, iDEAL — into a pan-European brand backed by 16 major banks and payment service providers. The UK's Variable Recurring Payments (VRPs) now account for 16% of Open Banking payment volumes, and a consortium of 31 companies established the UK Payments Initiative (UKPI) to expand VRPs into utility, government, and financial services payments.

North America accounted for approximately 22.0% of global market revenue in 2025, at approximately USD 13.75 billion. The United States is the primary driver, with FedNow and The Clearing House's RTP network providing 24/7 instant settlement rails now accessible to 78% of U.S. bank accounts. However, consumer-facing A2A adoption remains early: only 1.5% of all U.S. consumer transactions used pay-by-bank in the year ending June 2025. Card reward programmes and chargeback protections create behavioural inertia that A2A providers are addressing through purchase-protection guarantees and loyalty programme integrations. In Canada, Interac e-Transfer remains the dominant domestic A2A rail, and the country's exploration of Real-Time Rail (RTR) is in advanced development under Payments Canada.

Latin America held approximately 7.0% of global market revenue in 2025, representing approximately USD 4.38 billion. Brazil's Pix drives the region, having processed approximately USD 6.7 trillion in transaction value in 2025 and reached 174 million individual users by March 2026. The Central Bank of Brazil's Pix Automatico feature, enabling recurring payments, directly challenges credit card subscription billing and BNPL providers. In Argentina, Modo — a bank-consortium digital wallet — processed growing A2A volumes, while Peru's Yape and PLIN collectively pushed A2A to an estimated 28% of domestic e-commerce value by 2026.

Middle East & Africa represented approximately 3.0% of global market revenue in 2025, at approximately USD 1.87 billion. Nigeria's NIBSS Instant Payments emerged as the first mature African A2A service, extending financial access to unbanked populations. Saudi Arabia's Sarie and the UAE's Instant Payment Platform (IPP) are building A2A infrastructure aligned with Vision 2030 financial-sector reform targets. South Africa's PayShap, launched in March 2023, is scaling person-to-person and person-to-merchant instant payments, and Kenya's M-Pesa is exploring A2A interoperability with traditional banking rails.

Country Analysis

The United States A2A payment market was valued at approximately USD 11.00 billion in 2025, with a country-level CAGR estimated at 16.7% through 2034, reflecting the acceleration phase of FedNow adoption and open-banking regulatory momentum. FedNow processed USD 20 billion during its early months following the July 2023 launch and continues to onboard financial institutions; The Clearing House's RTP network complements FedNow with higher transaction limits and established institutional connectivity. The CFPB's Section 1033 open-banking rulemaking, which requires financial institutions to provide consumer-authorised data access to third-party payment initiators, is expected to accelerate A2A checkout adoption by removing the bank-linking friction that currently hampers consumer conversion. Stripe's April 2025 filing for a limited-purpose banking charter in Georgia signals that payment platforms are seeking direct rail access to reduce intermediary dependence and lower per-transaction costs for merchants.

India's A2A payment market reached approximately USD 12.50 billion in 2025, representing the world's largest A2A ecosystem by transaction volume. The country-level CAGR is estimated at 18.5% through 2034, driven by credit-on-UPI deployment, UPI Lite offline payment expansion, and NPCI International's cross-border UPI acceptance programme, which reached 12 countries by early 2026. UPI surpassed Visa in daily digital payment transactions in 2025, processing approximately 640 million daily transactions compared with Visa's 639 million globally. The October 2025 pilot by Razorpay, NPCI, and OpenAI for agentic AI payments on UPI — enabling conversational AI to initiate payment transactions — represents a potential inflection point in how A2A payments are initiated, moving from user-directed tapping to AI-directed voice or chat commands.

Germany's A2A payment market was valued at approximately USD 4.80 billion in 2025, with a country CAGR estimated at 12.5% through 2034. As the first market for Wero e-commerce acceptance (November 2025), Germany is the proving ground for EPI's pan-European A2A strategy. Wero replaces Giropay, which was discontinued in 2024, and targets the 89% of German consumers who hold bank accounts at institutions participating in the initiative. The combination of SEPA Instant mandate compliance (all EU banks must offer SEPA Instant from 2025) and Wero's e-commerce rollout creates a regulatory and commercial framework that is expected to lift A2A's share of German e-commerce from approximately 15% in 2024 to above 25% by 2028.

Brazil's A2A payment market reached approximately USD 8.00 billion in 2025, with a country CAGR estimated at 15.8% through 2034, reflecting Pix's continued penetration into e-commerce and B2B segments. Pix processed approximately USD 6.7 trillion in transaction value in 2025, with person-to-business (P2B) transactions surpassing person-to-person (P2P) for the first time in September 2025, reaching approximately 44% of total volume versus 43% for P2P. The Central Bank of Brazil's Pix Automatico feature for recurring payments and the ongoing exploration of cross-border Pix under the BIS Project Nexus framework position Brazil as both a benchmark for A2A adoption and a future node in the global instant-payment interoperability network.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Channel

- Online Payments

- Mobile Payments

- Bank Transfer Payments

- E-Commerce Payments

- Others

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid Deployment

- Others

By End-User Industry

- Banking, Financial Services, and Insurance (BFSI)

- Retail and E-Commerce

- Healthcare

- Information Technology and Telecommunications

- Government and Public Sector

- Travel and Hospitality

- Manufacturing

- Media and Entertainment

- Transportation and Logistics

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 62.50 B |

| Forecast Revenue (2034) | USD 206.40 B |

| CAGR (2025-2034) | 14.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Channel, (Online Payments, Mobile Payments, Bank Transfer Payments, E-Commerce Payments, Others), By Deployment Mode, (Cloud-Based, On-Premises, Hybrid Deployment, Others), By End-User Industry, (Banking, Financial Services, and Insurance (BFSI), Retail and E-Commerce, Healthcare, Information Technology and Telecommunications, Government and Public Sector, Travel and Hospitality, Manufacturing, Media and Entertainment, Transportation and Logistics, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PAYPAL HOLDINGS, INC., STRIPE, INC., ADYEN N.V., PLAID INC., TRUSTLY GROUP AB, TRUELAYER, TOKEN.IO, NUVEI CORPORATION, DWOLLA, INC., VOLT, JPMORGAN CHASE & CO., MASTERCARD INCORPORATED, VISA INC., BLOCK, INC. (SQUARE), WISE PLC, ORUM, GLOBAL PAYMENTS INC., THE CLEARING HOUSE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Channel & Application (E-commerce Checkout, Bill Payments, P2P Transfers, B2B Corporate Payments, B2C Disbursements), By Technology (Open Banking APIs, Real-Time Clearing Rails, Proxy Directory Services), By End-User (BFSI, Retail, Utilities, Healthcare) Region & Key Players-Dynamics, Strategies & Forecast 2026-2034")

, By Channel & Application (E-commerce Checkout, Bill Payments, P2P Transfers, B2B Corporate Payments, B2C Disbursements), By Technology (Open Banking APIs, Real-Time Clearing Rails, Proxy Directory Services), By End-User (BFSI, Retail, Utilities, Healthcare) Region & Key Players-Dynamics, Strategies & Forecast 2026-2034")

, By Channel & Application (E-commerce Checkout, Bill Payments, P2P Transfers, B2B Corporate Payments, B2C Disbursements), By Technology (Open Banking APIs, Real-Time Clearing Rails, Proxy Directory Services), By End-User (BFSI, Retail, Utilities, Healthcare) Region & Key Players-Dynamics, Strategies & Forecast 2026-2034")

Frequently Asked Questions

How big is the Account-to-Account (A2A) Payment Market?

The Global Account-to-Account (A2A) Payment Market was valued at approximately USD 55.10 Billion in 2024 and approximately USD 62.50 Billion in 2025, and is projected to reach approximately USD 206.40 Billion by 2034, growing at a CAGR of 14.2% from 2026 to 2034. Market growth is driven by real-time payments, open banking, and digital payment infrastructure.

Who are the major players in the Account-to-Account (A2A) Payment Market?

PAYPAL HOLDINGS, INC., STRIPE, INC., ADYEN N.V., PLAID INC., TRUSTLY GROUP AB, TRUELAYER, TOKEN.IO, NUVEI CORPORATION, DWOLLA, INC., VOLT, JPMORGAN CHASE & CO., MASTERCARD INCORPORATED, VISA INC., BLOCK, INC. (SQUARE), WISE PLC, ORUM, GLOBAL PAYMENTS INC., THE CLEARING HOUSE, Others

Which segments covered the Account-to-Account (A2A) Payment Market?

By Channel, (Online Payments, Mobile Payments, Bank Transfer Payments, E-Commerce Payments, Others), By Deployment Mode, (Cloud-Based, On-Premises, Hybrid Deployment, Others), By End-User Industry, (Banking, Financial Services, and Insurance (BFSI), Retail and E-Commerce, Healthcare, Information Technology and Telecommunications, Government and Public Sector, Travel and Hospitality, Manufacturing, Media and Entertainment, Transportation and Logistics, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Account-to-Account (A2A) Payment Market

Published Date : 01 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date