- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Accounts Payable Automation Market Size, Share | CAGR 11.8%

Global Accounts Payable Automation Market Size, Share, Analysis By Component (Software & Platforms, Services), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Industry Vertical (BFSI, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, IT & Telecommunications, Government & Public Sector, Transportation & Logistics, Energy & Utilities, Media & Entertainment) Industry Trends, Competitive Landscape & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 4.85 Billion | USD 13.20 Billion | 11.8% | North America, 37.1% |

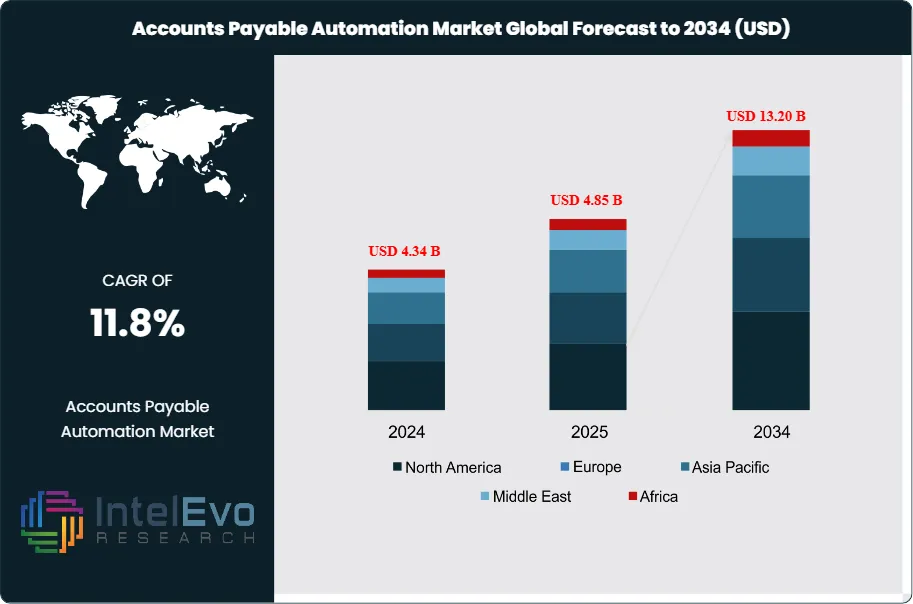

The Accounts Payable Automation Market was valued at approximately USD 4.34 Billion in 2024 and reached USD 4.85 Billion in 2025. The market is projected to grow to USD 13.20 Billion by 2034, expanding at a CAGR of 11.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 8.35 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportGrowth in the accounts payable automation market is anchored in three structural forces. First, AI-native agentic automation moved from pilot to production in 2025, with BILL Holdings launching BILL AI on October 28, 2025 covering W-9 collection, receipt reconciliation, onboarding, and a virtual back-office assistant, and Tipalti integrating agentic AI capabilities following its June 2025 acquisition of treasury automation firm Statement. Second, embedded-finance distribution expanded rapidly, with BILL signing partnerships with Oracle NetSuite on October 7, 2025 and Acumatica on October 22, 2025 to embed AP automation directly inside Cloud ERP platforms, reaching NetSuite's US customer base and Acumatica's 2025 R2 installed base. Third, private-equity consolidation accelerated category maturity, with TPG and Corpay completing a USD 2.2 Billion take-private acquisition of AvidXchange on October 15, 2025 at USD 10 per share.

The regulatory environment for accounts payable automation is framed by overlapping tax, payments, and cybersecurity regimes. In the United States, IRS Form 1099-NEC and 1099-MISC filing mandates, the Sarbanes-Oxley Act (SOX) Section 404 internal-controls requirements, and the NACHA ACH Operating Rules governing electronic payments frame compliance. The Financial Crimes Enforcement Network (FinCEN) Beneficial Ownership Information (BOI) reporting rule adds supplier due-diligence obligations. In the European Union, the VAT in the Digital Age (ViDA) package adopted in November 2024 mandates structured e-invoicing for intra-EU B2B transactions starting July 2030, and the EU AI Act's general-purpose AI provisions effective August 2, 2025 intersect with AI-driven invoice-coding. India's GST e-invoicing mandate, progressively extended through 2024-2025 to cover taxpayers above Rs 5 Crore annual turnover, anchors Asia Pacific digital AP adoption, and Brazil's eSocial plus the Nota Fiscal Eletronica system drives Latin American digitization.

Demand is consolidating around measurable adoption milestones. BILL's platform processed USD 89 Billion in payment volume (up 12% year-over-year) in Q1 FY2026 (quarter ended September 30, 2025), served 498,100 businesses, and its network processes approximately 1% of US GDP annually. BILL reported fiscal year 2025 (ended June 30, 2025) total revenue of USD 1.5 Billion with core revenue growing 16% year-over-year per its August 27, 2025 earnings release. Tipalti surpassed USD 200 Million in annually recurring revenue in September 2025 at an approximate USD 2 Billion valuation, with 10,000 customers and 30% year-over-year customer-base growth. More than 80% of US companies were affected by digital payment fraud, with 66% expecting risks to grow per a January 2025 PYMNTS report, driving AP automation demand for real-time fraud detection.

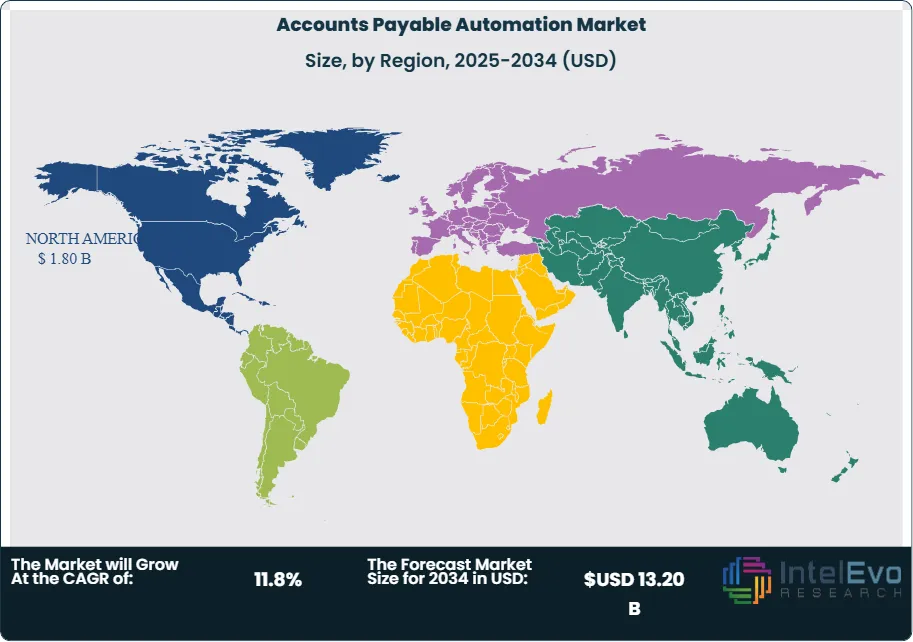

North America held the largest accounts payable automation market share at 37.1% in 2025, approximately USD 1.80 Billion per Mordor Intelligence, anchored by BILL Holdings, AvidXchange, Tipalti, Stampli, Coupa, Oracle NetSuite, and Microsoft Dynamics 365. Europe held 24.3% through SAP Ariba, Basware, Esker, Medius, and Yooz. Asia Pacific held 26.6% and is the fastest-growing region at 13.96% CAGR through 2031, with India showing the highest country-level CAGR of 14.5% per Future Market Insights. The accounts payable automation technology roadmap through 2034 tilts toward agentic AI (BILL AI, Tipalti AI agents, Coupa Navigator, Esker Synergy AI), deep ERP embeds, cross-border payment-rails integration, and unified procure-to-pay platforms.

Market Definition & Scope

The accounts payable automation market is defined as the global commercial activity in software platforms, embedded-finance integrations, and managed services that digitize and automate invoice capture, coding, approval workflows, payment execution, and vendor management across buyer, supplier, and funder counterparties. The market encompasses SaaS AP platforms (BILL, Tipalti, Stampli, AvidXchange, Coupa, Basware, Esker, Medius), enterprise-resource-planning embedded AP modules (SAP Ariba, Oracle NetSuite Intelligent Payment Automation, Microsoft Dynamics 365 Finance), and AI-agent frameworks performing invoice-coding, matching, and fraud detection.

Included in the scope are platform subscription and transaction revenues, per-invoice processing fees, supplier-network fees, cross-border FX spreads on AP-funded payments, and AI-agent premium SKUs. Explicitly excluded are pure accounts receivable automation without AP coverage, supply chain finance platforms where working-capital funding is the primary revenue (covered in a separate category), procurement-only sourcing platforms without invoice processing, and general treasury management systems. The accounts payable automation market is a subset of the broader global finance and accounting BPO category and sits adjacent to the larger global procure-to-pay software category.

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Industry Vertical (BFSI, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, IT & Telecommunications, Government & Public Sector, Transportation & Logistics, Energy & Utilities, Media & Entertainment) Industry Trends, Competitive Landscape & Forecast 2026-2034")

Key Takeaways

- Market Growth: The accounts payable automation market expands from USD 4.85 Billion in 2025 to USD 13.20 Billion by 2034, a CAGR of 11.8% over the forecast period.

- Segment Dominance by Component: Solutions led in 2025 with 67.3% revenue share per Mordor Intelligence, anchored by SaaS AP platforms from BILL, Tipalti, AvidXchange, SAP Ariba, Coupa, and Basware.

- Segment Dominance by Vertical: Banking, financial services, and insurance (BFSI) led in 2025 with 34.4% revenue share per Mordor Intelligence, driven by regulated audit-trail, SOX 404, and FFIEC cybersecurity requirements.

- Driver: BILL Holdings processed USD 89 Billion in payment volume (up 12% year-over-year) in Q1 FY2026 ended September 30, 2025 across 498,100 businesses, with the platform processing approximately 1% of US GDP annually.

- Restraint: Approximately 46% of medium-sized enterprises cite high initial setup costs as a key barrier to adopting advanced AP automation solutions, and 33% report lack of technical expertise delaying deployment per Global Growth Insights.

- Opportunity: Small and medium enterprise (SME) adoption leads growth at 18.15% CAGR per Mordor Intelligence, with BILL's Acumatica and NetSuite embed partnerships unlocking the underserved mid-market.

- Trend: Agentic AI moved from pilot to production in 2025, with BILL launching BILL AI on October 28, 2025, Tipalti integrating Statement acquisition AI agents, and Coupa extending Navigator AI capabilities across its platform.

- Regional: North America led the accounts payable automation market with 37.1% revenue share in 2025 per Mordor Intelligence, followed by Asia Pacific at 26.6% growing at 13.96% CAGR through 2031.

Key Insights Summary

- BILL Holdings reported Q1 FY2026 results on November 6, 2025 with total revenue of USD 395.7 Million (up 10% year-over-year), core revenue of USD 358 Million (up 14%), transaction fees of USD 287.2 Million (up 16%), and non-GAAP net income of USD 70.2 Million (USD 0.61 per diluted share), processing USD 89 Billion in payment volume across 498,100 businesses per the company's SEC filings and investor relations disclosures.

- BILL Holdings reported fiscal year 2025 (ended June 30, 2025) total revenue of USD 1.5 Billion with core revenue growing 16% year-over-year, non-GAAP operating income exceeding the high end of initial guidance by 23%, announced a USD 300 Million share repurchase program for fiscal 2026, and expanded non-GAAP operating margin excluding float revenue by 345 basis points year-over-year per the company's August 27, 2025 earnings release.

- TPG and Corpay completed the USD 2.2 Billion take-private acquisition of AvidXchange on October 15, 2025 at USD 10 per share, with TPG Capital holding the majority interest and Corpay investing USD 500 Million for a 33% minority stake (with option to acquire remaining shares in 2028), after the transaction was announced on May 6, 2025 and approved by AvidXchange shareholders on September 16, 2025.

- Tipalti surpassed USD 200 Million in annually recurring revenue in September 2025 with 30% year-over-year customer-base growth and 30% year-over-year annualized payment volume growth across 10,000 customers at an approximate USD 2 Billion valuation, per the company's September 24, 2025 announcement of a USD 200 Million growth financing from Hercules Capital.

- Acumatica and BILL announced a strategic partnership on October 22, 2025 to embed BILL's Accounts Payable automation directly into Acumatica Cloud ERP with availability across all Industry Editions in the Acumatica 2025 R2 product update, following Oracle NetSuite's October 7, 2025 announcement that it embedded BILL-powered payment automation into NetSuite Intelligent Payment Automation for US customers.

- On-premise installations held 54.10% of the AP automation market share in 2025, but cloud subscriptions are expanding at 14.32% CAGR through 2031 per Mordor Intelligence, while large enterprises accounted for 60.20% of 2025 revenue versus SMEs growing at an 18.15% CAGR and BFSI leading verticals with 34.40% revenue share ahead of IT and telecom at a 16.98% CAGR.

- More than 80% of US companies are affected by digital payment fraud with 66% expecting risks to grow per a January 2025 PYMNTS report, with country-level CAGRs through 2035 showing India leading at 14.5%, China at 12.8%, the UK at 12.0%, Brazil at 11.5%, the USA at 10.0%, and Germany at 9.0% per Future Market Insights.

Competitive Landscape Overview

The accounts payable automation market is moderately consolidated across three tiers. The top four companies, BILL Holdings, Tipalti, AvidXchange (now TPG/Corpay-owned), and SAP SE, collectively represented an estimated 43.8% of 2025 revenue based on public filings, private ARR disclosures, and analyst commentary. Competition is platform-depth and AI-automation led rather than price-led, because ERP integration depth, AI-agent sophistication, and supplier-network density determine displacement economics on AP automation procurement checklists.

Competitive dynamics shifted materially through 2025. BILL launched BILL AI on October 28, 2025, signed embed partnerships with Oracle NetSuite (October 7, 2025) and Acumatica (October 22, 2025), added Paychex as an Embed 2.0 partner, and announced a USD 300 Million fiscal 2026 share repurchase program. Tipalti closed USD 200 Million growth financing from Hercules Capital on September 24, 2025, acquired treasury automation firm Statement in June 2025, and extended AI-agent capabilities across reporting, tax form scanning, and purchase requests. AvidXchange transitioned to private ownership under TPG (majority) and Corpay (33%) on October 15, 2025 in a USD 2.2 Billion transaction. Activist pressure intensified at BILL, with Barington Capital Group urging the board on December 4, 2025 to implement a cost-reduction plan and explore strategic alternatives including a potential sale.

Competitive Landscape Matrix:

| Company | Headquarters | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| BILL Holdings, Inc. (NYSE: BILL) | United States | Leader | BILL AP; BILL Spend & Expense; BILL AI agents; Embed 2.0 | North America | Launched BILL AI on October 28, 2025 and embedded AP automation into Oracle NetSuite (October 7) and Acumatica (October 22) |

| Tipalti, Inc. | United States | Leader | Tipalti AP Automation; Tipalti Procurement; Tipalti Expenses; Tipalti Card | North America, Europe, APAC | Secured USD 200 Million growth financing from Hercules Capital on September 24, 2025 and acquired treasury automation firm Statement in June 2025 |

| AvidXchange Holdings, Inc. | United States | Leader | AvidXchange AP Automation; AvidPay Network | North America | Completed USD 2.2 Billion take-private acquisition by TPG and Corpay on October 15, 2025 at USD 10 per share |

| SAP SE (ETR: SAP) | Germany | Leader | SAP Ariba; SAP Business Network; SAP S/4HANA Invoice Management | Global | Integrated generative AI invoice-coding across SAP Ariba and SAP Business Network covering 5+ million connected businesses through 2025 |

| Coupa Software Incorporated | United States | Challenger | Coupa Business Spend Management; Coupa Pay; Coupa Invoice | North America, Europe, APAC | Deepened AI-first Coupa Navigator platform under Thoma Bravo's USD 8 Billion ownership established in February 2023 |

| Oracle NetSuite (NYSE: ORCL) | United States | Challenger | NetSuite Intelligent Payment Automation; Oracle Fusion Cloud AP | North America, Europe, APAC | Partnered with BILL on October 7, 2025 to embed AP automation into NetSuite Intelligent Payment Automation for US customers |

| Basware Corporation | Finland | Challenger | Basware AP Automation; Basware Procure-to-Pay; Basware Analytics | Europe, North America, APAC | Scaled AI-driven invoice capture and compliance workflows across Fortune 500 enterprise customers through 2025 |

| Esker S.A. (EPA: ALESK) | France | Challenger | Esker Accounts Payable; Esker Accounts Receivable; Esker Synergy AI | Europe, North America | Extended Esker Synergy AI capabilities across Procure-to-Pay and Order-to-Cash suites through 2025 |

| Medius AB | Sweden | Niche Player | Medius AP Automation; Medius Pay; Medius Spend Management | Europe, North America | Expanded AI-driven invoice-matching and fraud-detection modules across mid-market and enterprise deployments |

| Stampli, Inc. | United States | Niche Player | Stampli AP Automation; Billy the Bot AI; Stampli Card | North America | Scaled Billy the Bot AI invoice automation across mid-market NetSuite, Oracle, and QuickBooks customers |

Segmentation Analysis

The accounts payable automation market segments by component, deployment mode, enterprise size, and industry vertical. Each segmentation type maps to distinct buying criteria on an accounts payable automation procurement checklist, including ERP integration depth, AI-agent sophistication, SOC 2 Type II certification, and per-invoice pricing transparency.

By Component

Solutions led the accounts payable automation market at 67.3% revenue share in 2025 per Mordor Intelligence, approximately USD 3.26 Billion, covering SaaS AP platforms, invoice-capture software, approval-workflow engines, payment-execution modules, and AI-agent add-ons. Leading solution providers include BILL AP, Tipalti AP Automation, AvidXchange, SAP Ariba, Coupa Business Spend Management, Basware AP, Esker AP, Medius, and Stampli. Custom Market Insights estimates solutions at 68.4% of 2025 revenue, converging on a roughly two-thirds solution-to-one-third services split across research sources.

Services held 32.7% of 2025 revenue, approximately USD 1.59 Billion, and are the fastest-growing component sub-segment at 15.25% CAGR through 2031 per Mordor Intelligence. Services include implementation and integration consulting for ERP embeds (exemplified by BILL's NetSuite and Acumatica partnerships), ongoing managed services, supplier-onboarding services, and AI model fine-tuning and governance. The typical accounts payable automation ROI calculation shows payback inside 12 to 18 months for mid-market deployments above USD 50 Million annual AP throughput, driven by headcount reallocation, early-payment discount capture, and fraud-loss avoidance.

By Deployment Mode

On-premise installations held 54.10% of the accounts payable automation market share in 2025 per Mordor Intelligence, approximately USD 2.62 Billion, concentrated in large banks with legacy SAP and Oracle implementations, regulated government agencies, and sovereign-cloud-restricted deployments. Custom Market Insights reports a different mix, with cloud deployments already leading at 61.7% share, reflecting divergent methodologies between enterprise-weighted and SMB-weighted samples. Cloud subscriptions are expanding at 14.32% CAGR through 2031 per Mordor Intelligence, bolstered by encryption, zero-trust controls, and ISO-compliant data centers that outperform many corporate server rooms.

Cloud-delivered AP automation integrates with national real-time payment rails and tax portals through continuously updated APIs, an impossible task for static on-premise software. Subscription pricing converts capital outlays into operating expenses and allows SMEs to reach parity with larger peers. The fastest-growing deployment sub-segment is hybrid cloud with sovereign-data-residency architecture, exemplified by sovereign-cloud AP deployments in regulated European, Indian, and Middle Eastern markets under GDPR, India's DPDP Act 2023, and UAE PDPL frameworks. Monthly feature releases such as AI line-item extraction and carbon tracking reach cloud tenants in real time, widening the gap between cloud and on-premise deployment experience.

By Enterprise Size

Large enterprises held 60.20% of the accounts payable automation market in 2025 per Mordor Intelligence, approximately USD 2.92 Billion, driven by higher invoice volumes, complex approval matrices, and multi-entity reporting requirements. Anchor large enterprise platforms include SAP Ariba, Oracle Fusion Cloud AP, Coupa Business Spend Management (under Thoma Bravo ownership since February 2023), Basware, and Tipalti enterprise tier. Custom Market Insights reports large enterprises at 57.9% share, converging on a roughly 60/40 split between enterprise and SME segments.

Small and medium enterprises (SMEs) held 39.80% of 2025 revenue, approximately USD 1.93 Billion, and are the fastest-growing enterprise-size sub-segment at 18.15% CAGR through 2031 per Mordor Intelligence. SME growth is driven by per-invoice pricing models, intuitive SaaS interfaces, and embedded-finance distribution through accounting platforms. BILL serves 498,100 businesses, largely SMEs, through direct distribution and through accounting firm partnerships including over 9,000 accounting firms per the company's October 2025 Acumatica partnership disclosure. Tipalti targets mid-market and upper-mid-market customers through direct enterprise sales, while Stampli and AvidXchange serve the middle market (8,500 AvidXchange businesses).

By Industry Vertical

Banking, financial services, and insurance (BFSI) led the accounts payable automation market at 34.4% revenue share in 2025 per Mordor Intelligence, approximately USD 1.67 Billion, driven by SOX 404 internal-controls requirements, FFIEC cybersecurity guidance, and FINRA audit-trail mandates. Custom Market Insights and Future Market Insights estimate BFSI at 29.6% and 24% respectively, with differences reflecting definitional scope. IT and telecom is the fastest-growing vertical at 16.98% CAGR through 2031 per Mordor Intelligence and 14.3% CAGR per Custom Market Insights (2026-2035), driven by stock-based-compensation-adjacent expense workflows and fully remote workforces.

Retail and consumer goods held 14.6% of 2025 revenue, with large supplier bases and high invoice volumes demanding faster invoice reconciliation and payment cycles. Manufacturing held 13.2% (complex multi-tier supplier payables), healthcare and life sciences held 10.8% (regulated medical-device and pharmaceutical supplier compliance), government and public sector held 6.4%, energy and utilities held 5.2%, and other verticals including logistics and professional services held 15.4%. The accounts payable automation compliance requirements vary by vertical, with SOX Section 404 for public companies, FDA 21 CFR Part 11 for pharmaceutical electronic records, FedRAMP for federal cloud AP, and NACHA ACH Operating Rules governing electronic payments across verticals.

Regional Analysis

The accounts payable automation market is geographically led by North America, Asia Pacific, and Europe, together accounting for 88.0% of 2025 revenue. Regional dynamics differ on regulatory posture, ERP installed base, and AP platform ecosystem maturity, with North America leading on platform scale and Asia Pacific recording the fastest growth.

North America

North America held 37.1% of the accounts payable automation market in 2025 per Mordor Intelligence, approximately USD 1.80 Billion. The United States dominates through BILL Holdings in San Jose, AvidXchange in Charlotte (now TPG/Corpay-owned), Tipalti in Foster City, Stampli, Coupa Software (Thoma Bravo), Oracle NetSuite in Austin, and Microsoft Dynamics 365 Finance. Canada hosts Coupa Canada operations and regional AP deployments on NetSuite and Sage. The IRS administers 1099-NEC and 1099-MISC filing mandates, NACHA governs ACH Operating Rules effective 2024-2025, and FinCEN's Beneficial Ownership Information (BOI) reporting rule under the Corporate Transparency Act took effect January 1, 2024 driving supplier-due-diligence demand. The USA is projected to grow at 10.0% CAGR through 2035 per Future Market Insights, with more than 80% of US companies affected by digital payment fraud per January 2025 PYMNTS data.

Europe

Europe accounted for 24.3% of the accounts payable automation market in 2025, approximately USD 1.18 Billion. Germany leads through SAP SE in Walldorf anchoring SAP Ariba and SAP Business Network deployments across 5+ million connected businesses. France hosts Esker S.A. in Lyon (EPA: ALESK). Finland hosts Basware Corporation in Espoo. Sweden hosts Medius AB in Stockholm. The United Kingdom hosts Yooz, Sage Intacct, and Xero UK operations. The European Union's VAT in the Digital Age (ViDA) package adopted in November 2024 mandates structured e-invoicing for intra-EU B2B transactions starting July 2030, and Peppol network adoption accelerated through 2025 across member states. Italy's pioneering SDI mandatory B2B e-invoicing framework, France's Facture electronique schedule for 2026-2027 rollout, and Poland's KSeF mandatory e-invoicing (from February 2026) collectively underpin Continental AP digitization.

Asia Pacific

Asia Pacific held 26.6% of the accounts payable automation market in 2025, approximately USD 1.29 Billion, and recorded the fastest regional growth at 13.96% CAGR through 2031 per Mordor Intelligence and 14.5% CAGR through 2035 per Custom Market Insights. India leads at the country-CAGR level with 14.5% growth through 2035 per Future Market Insights, driven by the GST e-invoicing mandate covering taxpayers above Rs 5 Crore annual turnover and native platforms including Clear (formerly ClearTax), Zoho Books AP, and Ramco Systems. China follows at 12.8% country CAGR, with Kingdee, Yonyou, and Alibaba-adjacent platforms serving domestic enterprises. Japan hosts Money Forward, Concur Japan, and domestic AP specialists, and Australia hosts Xero, MYOB, and Lightyear. Singapore and Hong Kong serve as regional headquarters for Tipalti APAC and NetSuite APAC deployments.

Latin America

Latin America held 6.8% of the accounts payable automation market in 2025, approximately USD 330 Million, with Brazil leading at an 11.5% CAGR through 2035 per Future Market Insights. Brazil's eSocial electronic reporting framework and Nota Fiscal Eletronica (NFe) system mandate digital invoice capture, driving continuous AP platform adoption. Mexico's CFDI (Comprobante Fiscal Digital por Internet) e-invoicing mandate, administered by the Servicio de Administracion Tributaria (SAT), drives domestic AP digitization. Regional AP leadership includes TOTVS, Senior Sistemas, and Omie in Brazil; Aspel and CONTPAQi in Mexico; and multinational deployments of SAP Ariba, Oracle NetSuite, and Coupa. Argentina, Chile, and Colombia contribute smaller but growing deployments supported by real-time VAT reporting frameworks.

Middle East & Africa

Middle East & Africa accounted for 5.2% of the accounts payable automation market in 2025, approximately USD 252 Million. The United Arab Emirates leads regional adoption through Finkraft, Zoho AP, and multinational deployments of SAP Ariba and Oracle Fusion Cloud, supported by the UAE Federal Tax Authority's (FTA) phased e-invoicing rollout scheduled through 2026. Saudi Arabia follows through the Zakat, Tax and Customs Authority (ZATCA) Phase 2 (Integration) e-invoicing rollout extended through 2024-2025, with domestic suppliers including Finkraft KSA. South Africa hosts Sage VIP AP, SimplePay, and Xero South Africa. Egypt contributes through regional AP deployments supported by the Egyptian Tax Authority's e-invoicing mandate effective for all companies from April 2023 and extended through 2024-2025.

Country Analysis

Four national accounts payable automation markets, the United States, the United Kingdom, Germany, and India, collectively accounted for approximately 58.4% of 2025 revenue. These countries concentrate platform vendor headquarters, regulatory e-invoicing mandates, and the ERP installed base that drives accounts payable automation procurement.

United States

The United States represented approximately USD 1.60 Billion in 2025 accounts payable automation revenue, with a country CAGR estimated at 10.0% through 2035 per Future Market Insights. BILL Holdings in San Jose, AvidXchange in Charlotte (now TPG/Corpay-owned post October 15, 2025), Tipalti in Foster City, Stampli, Coupa Software (Thoma Bravo), Oracle NetSuite in Austin, SAP Ariba, Microsoft Dynamics 365, and Sage Intacct anchor the national platform base. The IRS administers 1099-NEC and 1099-MISC filing mandates, Sarbanes-Oxley Section 404 imposes internal-controls testing for public companies, and NACHA ACH Operating Rules govern electronic AP payments. FinCEN's Beneficial Ownership Information reporting rule under the Corporate Transparency Act took effect January 1, 2024, and PCI DSS v4.0 compliance deadlines through 2025 strengthen supplier-payment security controls. More than 80% of US companies are affected by digital payment fraud with 66% expecting risks to grow per January 2025 PYMNTS data.

United Kingdom

The United Kingdom represented approximately USD 340 Million in 2025 accounts payable automation revenue, with a country CAGR estimated at 12.0% through 2035 per Future Market Insights, among the highest developed-market growth rates. Yooz, Sage Intacct UK, Xero UK, and Quadient anchor domestic AP supplier leadership, with Coupa, SAP Ariba, and BILL serving multinational customers. HM Revenue & Customs (HMRC) administers Making Tax Digital for VAT with quarterly digital reporting, and the UK's proposed e-invoicing consultation launched in February 2025 signals upcoming mandatory B2B e-invoicing. The Prompt Payment Code administered by the Small Business Commissioner reinforces payment-discipline obligations on large buyer signatories. The Financial Reporting Council (FRC) oversees UK audit standards including ISA (UK) 315 (Revised 2019) applicable to AP internal controls.

Germany

Germany represented approximately USD 268 Million in 2025 accounts payable automation revenue, with a country CAGR estimated at 9.0% through 2035 per Future Market Insights. SAP SE in Walldorf anchors global enterprise AP leadership through SAP Ariba and SAP Business Network, alongside domestic specialists including DATEV, xSuite, and Easy Software. Germany's mandatory B2B e-invoicing framework under the Growth Opportunities Act (Wachstumschancengesetz), with phased requirements from January 1, 2025 (receipt capability) through January 1, 2028 (full rollout), drives continuous AP digitization. The Bundeszentralamt fur Steuern (BZSt) and Elster Online Portal govern VAT and tax-filing integration. German Works Council (Betriebsrat) co-determination rights under the Works Constitution Act (Betriebsverfassungsgesetz) influence AP automation roll-out plans for enterprises with 5+ employees.

India

India represented approximately USD 625 Million in 2025 accounts payable automation revenue, with a country CAGR estimated at 14.5% through 2035 per Future Market Insights, the fastest among the four profiled countries. Clear (formerly ClearTax) in Bangalore, Zoho Corporation in Chennai, Ramco Systems, Vayana Network, and Finkraft anchor the domestic platform supplier base. SAP Ariba India, Oracle NetSuite India, and Coupa serve multinational customers. The Goods and Services Tax Network (GSTN) e-invoicing mandate, launched October 2020 and progressively extended through 2024-2025 to cover all B2B transactions for taxpayers above Rs 5 Crore annual turnover, anchors digital AP adoption. The Central Board of Direct Taxes (CBDT) administers TDS (Tax Deducted at Source) on supplier payments, and India's Digital Personal Data Protection Act, 2023 (DPDP Act) adds data-protection requirements to cross-border AP processing.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Component

- Software & Platform

- Services

- Implementation & Integration

- Consulting Services

- Managed Services

- Training & Support

By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Industry Vertical

- BFSI

- Healthcare & Life Sciences

- Manufacturing

- Retail & E-Commerce

- IT & Telecommunications

- Government & Public Sector

- Transportation & Logistics

- Energy & Utilities

- Media & Entertainment

- Others (Education, Hospitality, Professional Services)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.85 B |

| Forecast Revenue (2034) | USD 13.20 B |

| CAGR (2025-2034) | 11.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Software & Platform, Services), By Deployment Mode, (Cloud-Based, On-Premise, Hybrid), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By Industry Vertical, (BFSI, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, IT & Telecommunications, Government & Public Sector, Transportation & Logistics, Energy & Utilities, Media & Entertainment, Others (Education, Hospitality, Professional Services)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BILL HOLDINGS, INC. (NYSE: BILL), TIPALTI, INC., AVIDXCHANGE HOLDINGS, INC., SAP SE (ETR: SAP), COUPA SOFTWARE INCORPORATED, ORACLE CORPORATION / NETSUITE (NYSE: ORCL), BASWARE CORPORATION, ESKER S.A. (EPA: ALESK), MEDIUS AB, STAMPLI, INC., TRADESHIFT HOLDINGS, INC., MICROSOFT CORPORATION (NASDAQ: MSFT), SAGE GROUP PLC (LON: SGE), XERO LIMITED (ASX: XRO), INTUIT INC. (NASDAQ: INTU), KYRIBA CORP. (BRIDGEPOINT GROUP), YOOZ SAS, RAMCO SYSTEMS LIMITED (BOM: 532370), PAPAYA GLOBAL LTD., FINASTRA INTERNATIONAL LIMITED, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Industry Vertical (BFSI, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, IT & Telecommunications, Government & Public Sector, Transportation & Logistics, Energy & Utilities, Media & Entertainment) Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Industry Vertical (BFSI, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, IT & Telecommunications, Government & Public Sector, Transportation & Logistics, Energy & Utilities, Media & Entertainment) Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Industry Vertical (BFSI, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, IT & Telecommunications, Government & Public Sector, Transportation & Logistics, Energy & Utilities, Media & Entertainment) Industry Trends, Competitive Landscape & Forecast 2026-2034")

Frequently Asked Questions

How big is the Accounts Payable Automation Market?

The Global Accounts Payable Automation Market was valued at USD 4.34 Billion in 2024 and is projected to reach USD 13.20 Billion by 2034, growing at a CAGR of 11.8% from 2026 to 2034. Growth is driven by increasing adoption of AI-powered invoice processing, robotic process automation (RPA), cloud-based financial management solutions, intelligent document processing, real-time payment integration, and the rising demand for finance digitalization, compliance management, and operational efficiency across enterprises worldwide.

Who are the major players in the Accounts Payable Automation Market?

BILL HOLDINGS, INC. (NYSE: BILL), TIPALTI, INC., AVIDXCHANGE HOLDINGS, INC., SAP SE (ETR: SAP), COUPA SOFTWARE INCORPORATED, ORACLE CORPORATION / NETSUITE (NYSE: ORCL), BASWARE CORPORATION, ESKER S.A. (EPA: ALESK), MEDIUS AB, STAMPLI, INC., TRADESHIFT HOLDINGS, INC., MICROSOFT CORPORATION (NASDAQ: MSFT), SAGE GROUP PLC (LON: SGE), XERO LIMITED (ASX: XRO), INTUIT INC. (NASDAQ: INTU), KYRIBA CORP. (BRIDGEPOINT GROUP), YOOZ SAS, RAMCO SYSTEMS LIMITED (BOM: 532370), PAPAYA GLOBAL LTD., FINASTRA INTERNATIONAL LIMITED, Others

Which segments covered the Accounts Payable Automation Market?

By Component, (Software & Platform, Services), By Deployment Mode, (Cloud-Based, On-Premise, Hybrid), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By Industry Vertical, (BFSI, Healthcare & Life Sciences, Manufacturing, Retail & E-Commerce, IT & Telecommunications, Government & Public Sector, Transportation & Logistics, Energy & Utilities, Media & Entertainment, Others (Education, Hospitality, Professional Services))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Accounts Payable Automation Market

Published Date : 04 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date