- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Aerospace Composites Market Size, Share & Forecast | CAGR 6.1%

Global Aerospace Composites Market Size, Share, Growth Analysis By Fiber Type (Carbon Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites, Ceramic Matrix Composites), By Resin System (Thermoset, Thermoplastic, Ceramic Matrix & Hybrid Systems), By Aircraft Platform (Commercial Aircraft, Defense Aircraft, Rotorcraft, Space & Advanced Air Mobility), By Manufacturing Process, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 34.80 Billion | USD 59.20 Billion | 6.1% | North America, 36.5% |

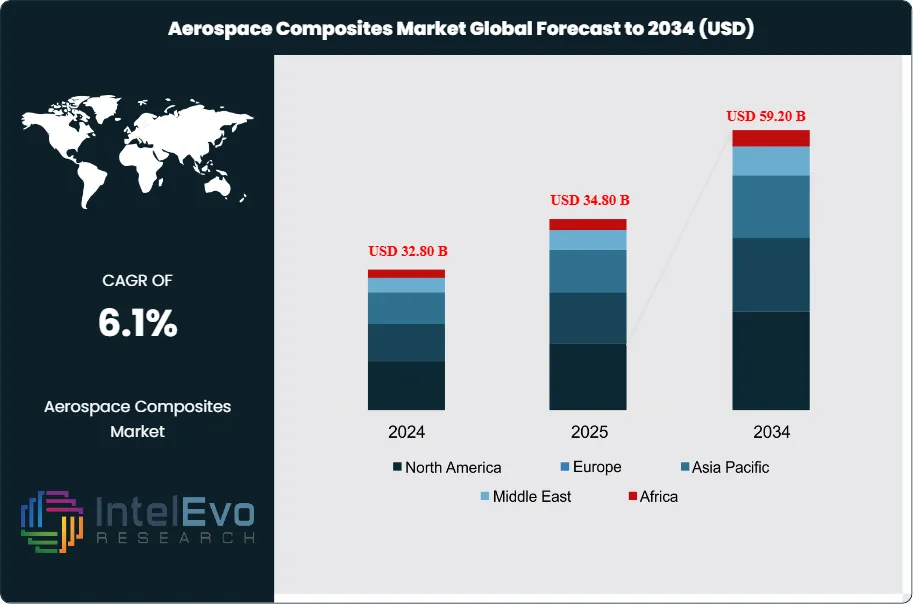

The Aerospace Composites Market was valued at approximately USD 32.80 Billion in 2024 and reached USD 34.80 Billion in 2025. The market is projected to grow to USD 59.20 Billion by 2034, expanding at a CAGR of 6.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 24.40 Billion over the analysis period. The aerospace composites market entered 2025 with stronger order visibility than in the prior two years because commercial aircraft backlogs remained elevated, airline traffic continued to expand, and military aviation programs kept demand for lightweight structural materials firm. Airbus reported a commercial aircraft backlog of 8,754 aircraft at the end of 2025, while IATA projected global air travel demand growth of 5.8% in 2025, with Asia Pacific contributing 52% of total RPK growth.

Get More Information about this report -

Request Free Sample ReportThe aerospace composites market is now shaped by a tight link between production-rate recovery and material-system qualification. Carbon fiber reinforced polymers remain the core revenue pool because they combine high specific strength with lower fuel-burn impact across fuselage skins, wing structures, nacelles, empennage assemblies, rotor blades, radomes, and premium interiors. Current market assessment shows commercial aerospace accounted for the largest demand block in 2025, but defense and space programs delivered the steadiest margins because procurement cycles remained more predictable and qualification barriers stayed high. North America led demand in 2025 on the back of Boeing, Lockheed Martin, RTX, Northrop Grumman, Gulfstream, Bombardier’s US supply chain presence, and a dense tier-one aerostructures base. Europe remained the second anchor market due to Airbus, Safran, Leonardo, Rolls-Royce, GKN Aerospace, and stronger regulatory alignment around lower-emission aircraft structures.

Supply and certification conditions still limit faster expansion. FAA guidance on composite aircraft structures, manufacturing quality systems, and advanced composite materials keeps qualification cycles disciplined across design, production, and maintenance. That regulatory load favors scaled suppliers with established allowables databases, AS9100-aligned quality systems, and global technical support. At the same time, the market is shifting from conventional autoclave-heavy production to faster processing routes. Hexcel highlighted rapid-curing and out-of-autoclave prepregs for aircraft structures in 2025, while Syensqo introduced ReGen sustainable composite materials and scrap-reuse pathways to reduce waste intensity. These moves support both throughput and cost control.

Regional investment hotspots widened in 2025. The US Southeast, Quebec, the UK Midlands, Occitanie, Bavaria, Japan, and selected Chinese coastal aerospace clusters drew the most attention for aerostructure and materials localization. Asia Pacific posted the fastest medium-term demand rise because airline growth outpaced mature markets and indigenous aircraft programs expanded local sourcing. The report framework uses the 2025 base year and 2034 forecast horizon specified in the source brief.

, By Resin System (Thermoset, Thermoplastic, Ceramic Matrix & Hybrid Systems), By Aircraft Platform (Commercial Aircraft, Defense Aircraft, Rotorcraft, Space & Advanced Air Mobility), By Manufacturing Process, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The aerospace composites market stood at USD 34.80 Billion in 2025 and is projected to reach USD 59.20 Billion by 2034. That implies a verified CAGR of 6.1% for 2026–2034.

- Segment Dominance: Carbon fiber composites led the aerospace composites market by fiber type with a 62.0% share in 2025, equal to about USD 21.58 Billion. The segment held the lead because primary structures and high-performance aerostructures still require the best weight-to-strength ratio.

- Segment Dominance: Commercial aircraft led the aerospace composites market by aircraft platform with a 49.0% share in 2025, equal to USD 17.05 Billion. Airbus backlog strength and fleet-renewal programs kept this segment ahead of defense and business aviation.

- Driver: Aircraft lightweighting remained the main growth engine in 2025. Material substitution and composite content gains added roughly 180 basis points to annual revenue expansion in narrowbody, widebody, and defense aerostructures.

- Restraint: Qualification time, scrap rates, and high precursor costs constrained the market in 2025. These factors held back an estimated USD 2.10 Billion of addressable demand that otherwise could have shifted from metallic structures.

- Opportunity: Thermoplastic aerospace composites created the strongest whitespace opportunity, with the segment expected to rise from USD 7.31 Billion in 2025 to about USD 14.10 Billion by 2034. Faster cycle times and weldable structures are widening adoption in clips, brackets, interiors, and secondary structures.

- Trend: High-rate manufacturing moved from pilot programs into commercial deployment in 2025. Automated fiber placement, rapid-curing prepregs, and out-of-autoclave systems supported about 34.0% of new program material selection activity.

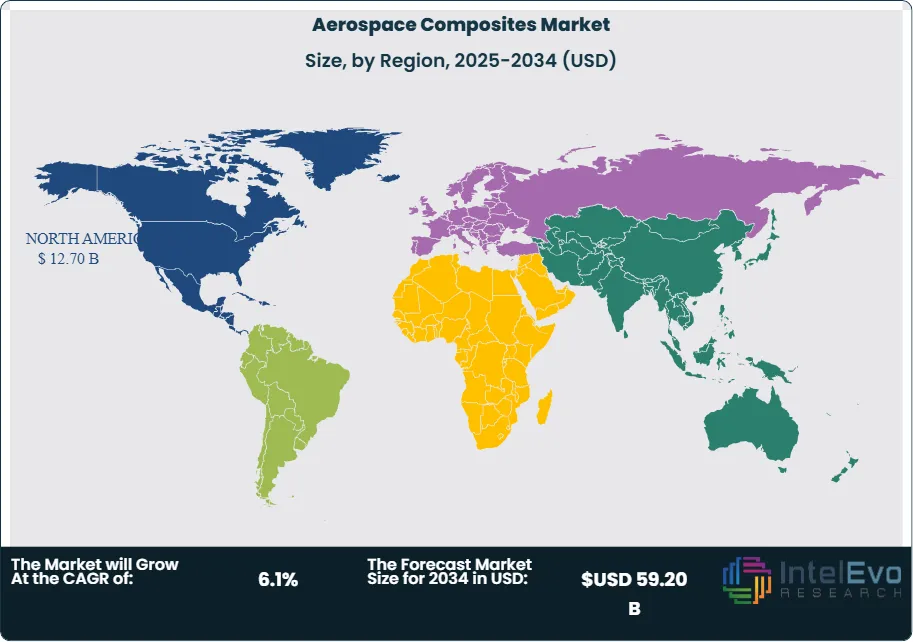

- Regional Analysis: North America led the aerospace composites market with 36.5% share in 2025, equal to USD 12.70 Billion. The region stayed ahead because of its deep aircraft OEM base, defense spending, and advanced certification infrastructure.

Competitive Landscape Overview

The aerospace composites market was moderately consolidated in 2025, with the top four suppliers controlling an estimated 44.0% of global revenue. Competition remained technology-driven first and supply-security driven second. Qualification history, resin-fiber integration, global application engineering, and production reliability mattered more than headline price. Competitive intensity increased in 2025 and early 2026 as suppliers pushed rapid-curing prepregs, thermoplastic systems, recycled-content grades, and long-term aerospace supply agreements.

Competitive Landscape Matrix

| Company Name | Headquarters (Country) | Market Position | Key Product/Solution in this market | Geographic Strength | Recent Strategic Move |

| Hexcel Corporation | United States | Leader | HexPly prepregs | North America and Europe | Highlighted HexPly M51 rapid-curing and M56 OOA systems for aerospace applications in Jan 2025 |

| Toray Industries, Inc. | Japan | Leader | TORAYCA carbon fiber and prepregs | Asia Pacific and North America | Unveiled CFRP bonding technology for aircraft structures in Jan 2026 |

| Syensqo SA | Belgium | Leader | CYCOM composite systems | Europe and North America | Secured a new long-term Boeing agreement in Mar 2026 |

| Teijin Limited | Japan | Challenger | Tenax carbon fiber materials | Asia Pacific and Europe | Launched Tenax Next and new modulus grades at JEC World 2025 |

| Mitsubishi Chemical Group | Japan | Challenger | Pyrofil and CF-SMC materials | Japan and North America | Expanded high-performance carbon fiber capacity in Japan and the US from 2025 to 2027 |

| SGL Carbon SE | Germany | Challenger | SIGRAFIL carbon fiber | Europe | Expanded aerospace and industrial lightweighting focus through specialty carbon materials programs |

| Park Aerospace Corp. | United States | Niche Player | Aerospace composite prepregs | North America | Continued high-performance prepreg focus for aerostructures and engine-related applications |

| Albany Engineered Composites | United States | Niche Player | Advanced composite aerostructures | North America | Increased participation in defense and engine composite structures programs |

By Fiber Type

The aerospace composites market by fiber type was led by carbon fiber composites with 62.0% share in 2025, equivalent to USD 21.58 Billion. Carbon fiber stayed dominant because it remains the default choice for fuselage skins, wing structures, spars, floor beams, nacelles, and military platforms where stiffness-to-weight performance directly affects payload, fuel burn, and range. Large commercial aircraft programs still drive the biggest volume pull, but defense airframes and space structures raise average selling prices. Glass fiber composites held 21.5% share, or USD 7.48 Billion, because they remain cost-effective in interiors, radomes, fairings, and secondary structures where electrical transparency and lower cost matter more than ultimate modulus. Aramid composites represented 9.0%, or USD 3.13 Billion, and remained relevant in ballistic protection, rotorcraft, and impact-resistant interiors. Ceramic matrix and other specialty composites accounted for the remaining 7.5%, or USD 2.61 Billion, serving engine hot-section, exhaust, and highly specialized defense applications. The revenue mix will keep shifting toward carbon fiber and ceramic systems as higher-temperature and lower-emission aircraft architectures move from development into scaled procurement.

By Resin System

The aerospace composites market by resin system remained concentrated in thermosets, which captured 71.0% of 2025 revenue, equal to USD 24.71 Billion. Epoxy-based prepregs still dominate qualified aircraft structures because certification data sets, mechanical familiarity, and global processing infrastructure are already in place. Thermosets also keep their edge in large autoclave-processed components where conservative qualification pathways still favor proven chemistry. Thermoplastics held 21.0% share, equal to USD 7.31 Billion, and posted the strongest strategic momentum because weldability, damage tolerance, and shorter cycle times improve economics in clips, brackets, seat structures, access panels, and secondary airframe parts. This segment is moving from niche to scale as OEMs seek lower recurring labor input and better end-of-life circularity. Ceramic matrix composite and hybrid resin systems accounted for 8.0% combined, or USD 2.78 Billion, with demand centered on engines, high-temperature zones, and defense propulsion environments. Through 2034, thermoplastic systems will gain share faster than any other resin family because aircraft manufacturers need more rate-ready processing than classic autoclave-only production can deliver.

By Aircraft Platform

The aerospace composites market by aircraft platform was led by commercial aircraft at 49.0% share in 2025, equal to USD 17.05 Billion. Narrowbody recovery, widebody reactivation, freighter renewal, and the Airbus backlog kept this segment in first position. Defense aircraft followed with 26.0%, or USD 9.05 Billion, reflecting strong usage in fighters, tankers, rotorcraft, unmanned systems, and mission-specific structures where strength, stealth shaping, and weight control matter together. Business and general aviation accounted for 10.0%, or USD 3.48 Billion, supported by premium cabin demand, long-range jet platforms, and aftermarket refurbishments. Rotorcraft represented 8.0%, or USD 2.78 Billion, driven by rotor blades, tail booms, and airframe weight reduction. Space, urban air mobility, and advanced air mobility programs made up 7.0%, or USD 2.44 Billion. That block remains small in 2025 but carries the highest long-run upside because launch systems, satellites, hydrogen aviation concepts, and electric airframes all need extreme lightweighting and tailored performance.

By Manufacturing Process

The aerospace composites market by manufacturing process still leaned on prepreg and autoclave processing, which captured 46.0% of 2025 revenue, or USD 16.01 Billion. This route remains the benchmark for primary structures because it delivers tight property control, low void content, and established certifiability. Resin transfer molding and vacuum-assisted resin infusion represented 21.0%, or USD 7.31 Billion, and gained traction in medium-volume structures where labor reduction matters. Automated fiber placement and automated tape laying accounted for 18.0%, or USD 6.26 Billion, and this share will climb because labor intensity is now a direct constraint on aircraft-rate recovery. Filament winding held 9.0%, or USD 3.13 Billion, centered on pressure vessels, ducting, and selected space applications. Compression molding and other fast-cycle methods represented 6.0%, or USD 2.09 Billion, mainly in interiors and secondary structures. The next phase of competition will center on which suppliers can pair qualified material systems with faster manufacturing methods rather than selling raw material alone.

Regional Analysis

North America

The North America aerospace composites market held 36.5% of global revenue in 2025, equal to USD 12.70 Billion. The United States accounted for the clear majority of that total, with Canada ranking second and Mexico third. The region led because it combines the deepest aircraft OEM base, the largest defense aviation budget pool, a strong business jet cluster, and dense tier-one aerostructures capacity. US demand was anchored by Boeing commercial production, military aircraft programs, NASA-linked materials work, and a mature repair and overhaul base. FAA composite guidance and production-quality expectations also favor suppliers with long certification histories and robust traceability systems. Canada remained material because of Bombardier, Pratt & Whitney Canada, and Québec’s composite manufacturing corridor. Mexico kept expanding as a lower-cost aerostructures hub linked to US supply chains.

Europe

The Europe aerospace composites market accounted for 29.0% of global revenue in 2025, equal to USD 10.09 Billion. France, Germany, the United Kingdom, and Italy formed the core demand base. France led through Airbus final assembly, Safran, Dassault, and a wide materials-processing network. Germany remained critical for Airbus structures, premium engineering capability, and polymer and carbon-material suppliers. The UK added strength through GKN Aerospace, Rolls-Royce, aerospace thermoplastic innovation, and defense programs. Italy contributed through Leonardo and a strong role in aerostructures and rotorcraft. Europe benefits from long-standing composite usage in both civil and defense platforms, but cost pressure and energy pricing still affect conversion margins. The region is also pushing harder on circularity and supply-chain resilience.

Asia Pacific

The Asia Pacific aerospace composites market represented 24.0% of global revenue in 2025, or USD 8.35 Billion, and it posted the fastest expansion outlook. China, Japan, India, and South Korea drove most regional growth. China led in airline fleet expansion, indigenous aircraft production ambitions, and state-backed aerospace materials programs. Japan stayed central because Toray, Teijin, and Mitsubishi Chemical remain among the most important carbon fiber and prepreg suppliers worldwide. India gained momentum through defense localization, space programs, and aircraft component manufacturing, while South Korea strengthened its role in advanced materials and aerospace manufacturing support. That traffic profile translates into long-run demand for both new aircraft and high-performance interior and structural materials.

Latin America

The Latin America aerospace composites market held 5.2% share in 2025, equal to USD 1.81 Billion. Brazil dominated regional revenue, followed by Mexico and Argentina. Brazil led through Embraer, a broad regional-jet supply chain, and a stronger installed base of composite-intensive airframes. Mexico served more as a manufacturing node tied to North American supply chains than as a standalone aircraft demand engine, but its role kept growing in interiors, harnesses, and selected structures. Argentina remained smaller but strategically relevant for defense and maintenance activity. Growth in Latin America stayed below the global average because aircraft procurement cycles were more sensitive to currency pressure and airline profitability.

Middle East & Africa

The Middle East & Africa aerospace composites market accounted for 5.3% of global revenue in 2025, equal to USD 1.84 Billion. The UAE, Saudi Arabia, and South Africa led demand. The UAE and Saudi Arabia mattered because widebody procurement, MRO expansion, sovereign aerospace investment, and defense-aircraft programs lifted composite demand beyond simple airline purchasing. South Africa remained relevant through defense, maintenance, and specialty aerostructures work. Demand will rise steadily through 2034 as fleet modernization and aerospace industrialization continue.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Fiber Type

- Carbon Fiber Composites

- Glass Fiber Composites

- Aramid Fiber Composites

- Ceramic Matrix Composites

- Others

By Resin System

- Thermoset Composites

- Thermoplastic Composites

- Ceramic Matrix and Hybrid Systems

- Others

By Aircraft Platform

- Commercial Aircraft

- Defense Aircraft

- Business and General Aviation

- Rotorcraft

- Space and Advanced Air Mobility

By Manufacturing Process

- Prepreg and Autoclave

- Resin Transfer Molding and Infusion

- Automated Fiber Placement and Tape Laying

- Filament Winding

- Compression Molding and Others

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 34.80 B |

| Forecast Revenue (2034) | USD 59.20 B |

| CAGR (2025-2034) | 6.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Fiber Type, (Carbon Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites, Ceramic Matrix Composites, Others), By Resin System, (Thermoset Composites, Thermoplastic Composites, Ceramic Matrix and Hybrid Systems, Others), By Aircraft Platform, (Commercial Aircraft, Defense Aircraft, Business and General Aviation, Rotorcraft, Space and Advanced Air Mobility), By Manufacturing Process, (Prepreg and Autoclave, Resin Transfer Molding and Infusion, Automated Fiber Placement and Tape Laying, Filament Winding, Compression Molding and Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HEXCEL CORPORATION, TORAY INDUSTRIES, INC., SYENSQO SA, TEIJIN LIMITED, MITSUBISHI CHEMICAL GROUP, SGL CARBON SE, PARK AEROSPACE CORP., ALBANY ENGINEERED COMPOSITES, VICTREX PLC, SOLVAY SA, AVIENT CORPORATION, ROCK WEST COMPOSITES, HUNTSMAN CORPORATION, OWENS CORNING, SAFRAN S.A., GKN AEROSPACE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Resin System (Thermoset, Thermoplastic, Ceramic Matrix & Hybrid Systems), By Aircraft Platform (Commercial Aircraft, Defense Aircraft, Rotorcraft, Space & Advanced Air Mobility), By Manufacturing Process, Industry Trends & Forecast 2026-2034")

, By Resin System (Thermoset, Thermoplastic, Ceramic Matrix & Hybrid Systems), By Aircraft Platform (Commercial Aircraft, Defense Aircraft, Rotorcraft, Space & Advanced Air Mobility), By Manufacturing Process, Industry Trends & Forecast 2026-2034")

, By Resin System (Thermoset, Thermoplastic, Ceramic Matrix & Hybrid Systems), By Aircraft Platform (Commercial Aircraft, Defense Aircraft, Rotorcraft, Space & Advanced Air Mobility), By Manufacturing Process, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Aerospace Composites Market?

The Global Aerospace Composites Market was valued at USD 32.80 Billion in 2024 and is projected to reach USD 59.20 Billion by 2034, growing at a CAGR of 6.1% from 2026 to 2034, driven by increasing aircraft production, rising demand for lightweight fuel-efficient materials, and expanding adoption of advanced carbon fiber composites in commercial, military, and space aerospace applications.

Who are the major players in the Aerospace Composites Market?

HEXCEL CORPORATION, TORAY INDUSTRIES, INC., SYENSQO SA, TEIJIN LIMITED, MITSUBISHI CHEMICAL GROUP, SGL CARBON SE, PARK AEROSPACE CORP., ALBANY ENGINEERED COMPOSITES, VICTREX PLC, SOLVAY SA, AVIENT CORPORATION, ROCK WEST COMPOSITES, HUNTSMAN CORPORATION, OWENS CORNING, SAFRAN S.A., GKN AEROSPACE, Others

Which segments covered the Aerospace Composites Market?

By Fiber Type, (Carbon Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites, Ceramic Matrix Composites, Others), By Resin System, (Thermoset Composites, Thermoplastic Composites, Ceramic Matrix and Hybrid Systems, Others), By Aircraft Platform, (Commercial Aircraft, Defense Aircraft, Business and General Aviation, Rotorcraft, Space and Advanced Air Mobility), By Manufacturing Process, (Prepreg and Autoclave, Resin Transfer Molding and Infusion, Automated Fiber Placement and Tape Laying, Filament Winding, Compression Molding and Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date