- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Aerospace Electronics Market Size, Growth & Forecast | CAGR 7.8%

Global Aerospace Electronics Market Size, Share & Industry Analysis By Component (Avionics Systems, Communication Systems, Radar & Navigation Systems, In-Flight Entertainment Systems, Others), By End-Use (Commercial Aviation, Military & Defense), By Platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles), By Technology & Application, Industry Region & Key Players – Market Segmentation Overview, Growth Drivers, Challenges, Competitive Strategies, Emerging Trends & Forecast 2025–2034

Report Overview

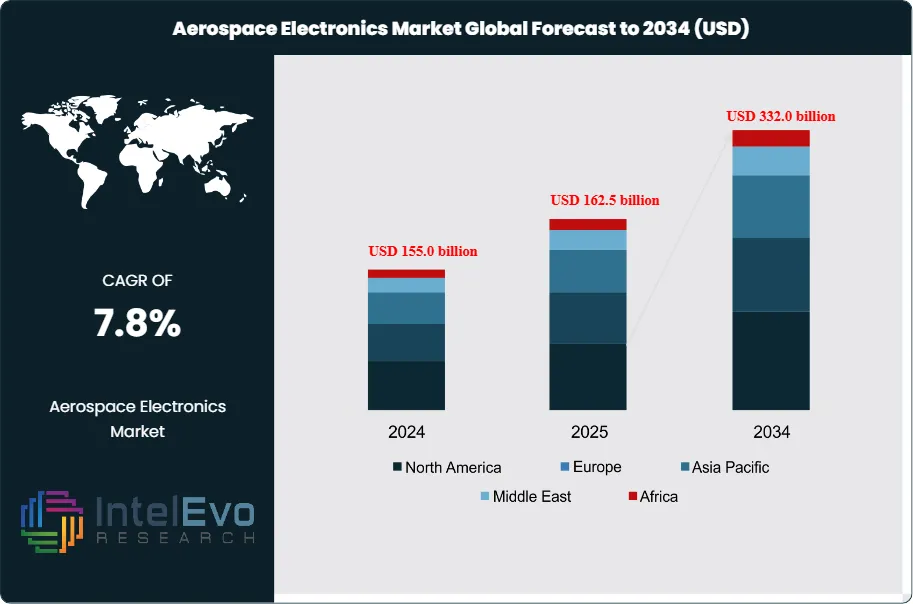

The Aerospace Electronics Market is valued at approximately USD 162.5 billion in 2025 and is projected to reach around USD 332.0 billion by 2034, expanding at a compound annual growth rate (CAGR) of about 7.8% during the forecast period from 2026 to 2034. This growth is driven by rising aircraft production, increasing defense modernization programs, and rapid adoption of advanced avionics, flight control systems, and next-generation navigation technologies. Additionally, the integration of AI-enabled electronics, lightweight components, and enhanced cybersecurity solutions is reshaping aerospace platforms, positioning the market for sustained long-term expansion across commercial, military, and space applications.

Get More Information about this report -

Request Free Sample ReportDemand draws on sustained growth in commercial air travel, fleet renewal in mature markets, and rising defense outlays, while supply reflects continuous innovation in avionics architectures, sensors, and secure communications. Core systems support communication, navigation, flight control, surveillance, and health monitoring across crewed aircraft, satellites, spacecraft, and unmanned platforms, making electronics a critical lever for safety, fuel efficiency, and mission performance.

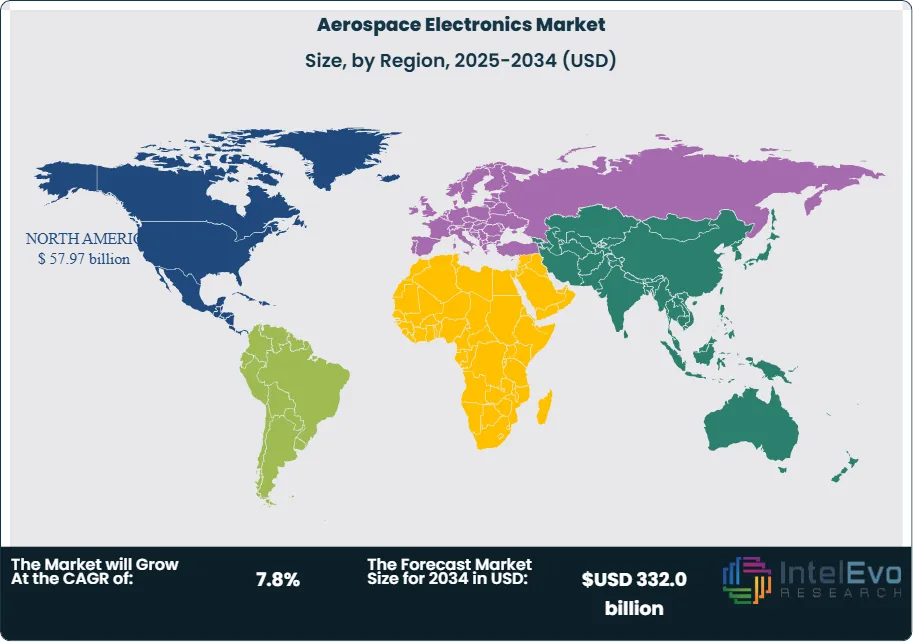

North America remains the largest regional contributor, accounting for about 37% of global revenue, underpinned by strong OEM and Tier-1 ecosystems and defense procurement. Europe maintains a solid share on the back of wide-body programs and space initiatives, while Asia Pacific is the fastest-expanding demand pool as China, India, and Southeast Asian economies scale up fleet size, MRO capacity, and indigenous aerospace programs. Emerging markets in the Middle East and Latin America increase investment in next-generation air traffic management and regional connectivity, creating additional demand for advanced avionics.

Technology change reshapes competitive dynamics. Increased use of artificial intelligence, automation, and real-time data processing enables predictive maintenance, adaptive flight management, and enhanced situational awareness. Integration of IoT connectivity, high-performance computing, and open architectures drives content growth per aircraft and shortens upgrade cycles. At the same time, cybersecurity requirements intensify as more platforms connect to ground networks and cloud-based analytics, raising compliance and certification costs.

Regulation acts as both catalyst and constraint. Tighter safety and emissions standards accelerate replacement of legacy systems with digital, software-defined solutions, while certification regimes extend development timelines and elevate technical risk. Governments support domestic aerospace electronics manufacturing through targeted incentives, infrastructure investment, and higher local-content mandates, particularly in large importing nations. For example, billion-dollar programs for aerospace parks, indigenous procurement targets of around 60% in defense electronics, and rising R&D allocations in key economies reinforce long-term demand visibility.

Competitive intensity stays high as global primes, specialized avionics firms, and digital technology providers contest share in platforms, subsystems, and software. Strategic partnerships around AI-enabled navigation, autonomous operations, and secure communications expand, with ecosystem collaboration central to meeting cost, performance, and regulatory expectations across the aerospace value chain.

, By End-Use (Commercial Aviation, Military & Defense), By Platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles), By Technology & Application, Industry Region & Key Players – Market Segmentation Overview, Growth Drivers, Challenges, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The aerospace electronics market stands at estimated: USD 162.5 billion in 2025, up from 155.0 billion USD, 2024, and is projected to approach estimated: 332.0 billion USD, 2034, reflecting a 7.8% CAGR over 2026-2034.

- Segment Dominance: Avionics systems lead the component segment with a 38.5% share, 2023, supported by demand that generates estimated: 60.0 billion USD, 2024 in integrated communication, navigation, and flight-control electronics.

- Segment Dominance: Commercial aviation dominates end-use with a 59.1% share, 2023, and likely exceeds estimated: 65.0% share, 2024 as airlines invest in cockpit upgrades, connectivity, and passenger-safety systems.

- Driver: Fleet renewal and avionics modernization drive demand, with airlines and defense programs together accounting for estimated: 70.0% of total aerospace electronics spend, 2024 and underpinning the 7.0% CAGR over 2024-2034.

- Restraint: High development, integration, and certification costs restrain faster rollout, with compliance and testing often consuming estimated: 15.0% of program budgets, 2024 and delaying platform entry into service.

- Opportunity: Unmanned platforms, satellite constellations, and new regional fleets create incremental electronics demand estimated: 35.0 billion USD, 2034, particularly in advanced flight-control, sensing, and secure communication systems.

- Trend: Suppliers increasingly embed AI, automation, and real-time analytics, and software-defined avionics could lift electronics content per aircraft by estimated: 20.0% growth, 2030 relative to 2024 systems.

- Regional Analysis: North America leads with a 37.4% share, 2023 and 54.19 billion USD, 2023 in aerospace electronics revenue, and is likely to retain more than estimated: 35.0% global share, 2034 as domestic OEMs and defense agencies sustain high investment over 2024-2034.

By Component

Avionics systems continue to represent the largest share of aerospace electronics in 2025, building on their earlier 38.5 percent share in 2023. The segment maintains a central role in flight control, navigation, and cockpit automation. Demand increases as airlines and defense operators focus on flight accuracy, fuel efficiency, and compliance with updated global safety policies. Real-time system diagnostics, enhanced flight management tools, and improved autopilot functions reinforce the segment’s importance across both new aircraft programs and fleet upgrades.

Adoption accelerates as aviation authorities strengthen requirements for communication integrity, collision-avoidance capabilities, and situational awareness. Operators invest in modern cockpit systems to support high-traffic air corridors and to reduce pilot workload during complex operations. The integration of digital communication suites and advanced sensors also sharpens the competitive edge for manufacturers able to meet these requirements.

Avionics systems continue to evolve with the rise of connected aircraft. AI-supported monitoring, IoT-enabled data exchange, and predictive maintenance tools are now embedded in many new installations. This shift increases reliability and reduces downtime, which appeals to commercial airlines and defense operators managing high-utilization fleets. These changes reinforce the leadership position of avionics in the broader component landscape.

By End-Use

The commercial aviation segment holds the largest share in 2025, following its earlier 59.1 percent share in 2023. Global passenger traffic returns to pre-pandemic growth rates, and airlines expand networks across Asia Pacific, the Middle East, and parts of Africa. This expansion fuels demand for advanced electronics that improve operational efficiency, flight scheduling, and cabin systems. In-flight entertainment upgrades and enhanced connectivity further support investment decisions for commercial operators.

Fleet modernization remains a core priority. Airlines replace older aircraft with models designed for lower emissions and improved fuel efficiency. These aircraft integrate higher levels of electronic content, including upgraded communication suites and enhanced flight-control systems. The need to reduce maintenance cycles and improve dispatch reliability also strengthens adoption of new electronics across the commercial fleet.

Military demand remains strong as governments invest in advanced avionics for improved situational awareness and mission-readiness. Modernization programs for fighter jets, transport aircraft, and UAVs continue through 2025, contributing a steady share to the overall market. Communication security, navigation precision, and electronic warfare capabilities drive procurement decisions in this segment.

By Region

North America continues to lead the aerospace electronics market in 2025 after previously accounting for 37.4 percent of global revenue and USD 54.19 billion in 2023. The region benefits from mature aircraft production clusters, strong defense spending, and active R&D pipelines. The United States remains the anchor market, supported by strategic investment in advanced flight systems, space programs, autonomous platforms, and next-generation communication infrastructure.

Europe maintains a significant role, supported by large civil aircraft programs and continued investment in sustainable aviation technologies. Regulatory requirements for emissions reduction and enhanced flight monitoring drive adoption of new systems across the region. Asia Pacific shows the fastest expansion as airlines in China, India, and Southeast Asia increase fleet sizes to support rising middle-class travel. Government initiatives encouraging domestic aerospace development also strengthen regional manufacturing activity.

Latin America and the Middle East & Africa show steady but smaller contributions. Growth in these regions comes from regional airline expansion and targeted defense upgrades. As operators modernize fleets and strengthen airspace management capabilities, demand for flight-control systems, communication electronics, and navigation solutions continues to rise.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

Component

- Avionics Systems

- Communication Systems

- Radar and Navigation Systems

- In-flight Entertainment Systems

- Other Components

End-Use

- Commercial

- Military

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 162.5 billion |

| Forecast Revenue (2034) | USD 332.0 billion |

| CAGR (2025-2034) | 7.8% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Component (Avionics Systems, Communication Systems, Radar and Navigation Systems, In-flight Entertainment Systems, Other Components), End-Use (Commercial, Military) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Panasonic Holdings Corporation, Safran SA, BAE Systems plc, Thales Group, Teledyne Technologies Incorporated, Honeywell International Inc., The Boeing Company, Airbus SE, RTX Corporation, L3Harris Technologies, Inc., Northrop Grumman Corporation, General Electric Company, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-Use (Commercial Aviation, Military & Defense), By Platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles), By Technology & Application, Industry Region & Key Players – Market Segmentation Overview, Growth Drivers, Challenges, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By End-Use (Commercial Aviation, Military & Defense), By Platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles), By Technology & Application, Industry Region & Key Players – Market Segmentation Overview, Growth Drivers, Challenges, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By End-Use (Commercial Aviation, Military & Defense), By Platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles), By Technology & Application, Industry Region & Key Players – Market Segmentation Overview, Growth Drivers, Challenges, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Aerospace Electronics Market?

The global aerospace electronics market was valued at USD 162.5 billion in 2025 and is projected to reach USD 332.0 billion by 2034, growing at a CAGR of 7.8% from 2026 to 2034, driven by advanced avionics, defense modernization, and next-generation aircraft technologies.

Who are the major players in the Aerospace Electronics Market?

Panasonic Holdings Corporation, Safran SA, BAE Systems plc, Thales Group, Teledyne Technologies Incorporated, Honeywell International Inc., The Boeing Company, Airbus SE, RTX Corporation, L3Harris Technologies, Inc., Northrop Grumman Corporation, General Electric Company, Other Key Players

Which segments covered the Aerospace Electronics Market?

Component (Avionics Systems, Communication Systems, Radar and Navigation Systems, In-flight Entertainment Systems, Other Components), End-Use (Commercial, Military)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Aerospace Electronics Market

Published Date : 04 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date