- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Aerospace NDT Market Size, Share, & Forecast 2034 | CAGR 7.1%

Global Aerospace NDT Market Size, Share, Analysis By Component (Equipment, Software, Services, Consumables), By Technique (Traditional/Conventional NDT, AI-enabled NDT), By Testing Method (Ultrasonic Testing, Radiographic Testing, Magnetic Particle Testing, Liquid Penetrant Testing, Visual Inspection, Eddy-Current Testing, Acoustic Emission Testing, Thermography/Infrared Testing, Computed Tomography Testing) Industry Regional Outlook, Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034

Report Overview

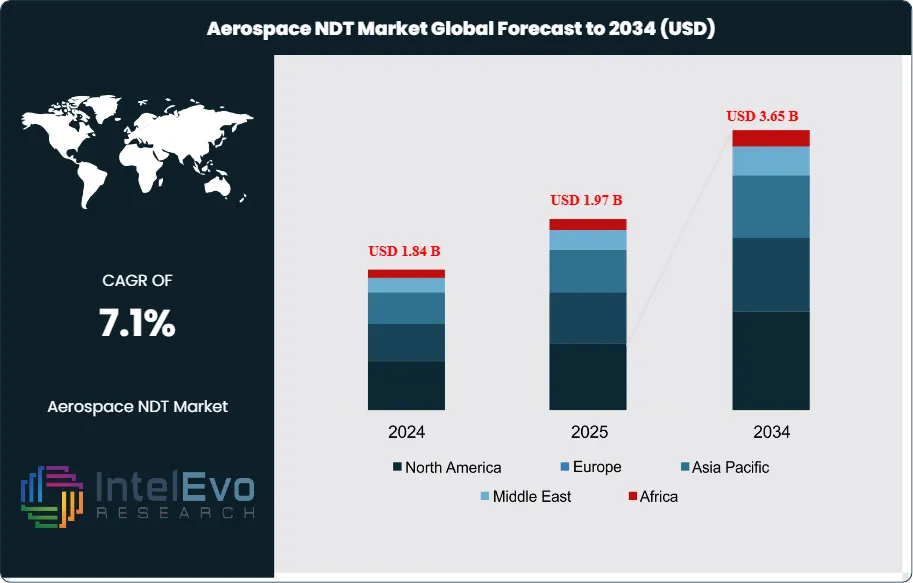

The Aerospace NDT Market was valued at USD 1.84 billion in 2024 and is projected to reach approximately USD 1.97 billion in 2025. The market is further expected to expand to nearly USD 3.65 billion by 2034, registering a compound annual growth rate (CAGR) of about 7.1% during the forecast period from 2026 to 2034. Growth in the market is driven by the increasing demand for advanced inspection technologies to ensure aircraft safety, structural integrity, and regulatory compliance across commercial aviation, defense, and space programs. Aerospace NDT techniques such as ultrasonic testing, radiographic testing, eddy current testing, and magnetic particle inspection play a crucial role in detecting material defects without damaging aircraft components.

Get More Information about this report -

Request Free Sample ReportAdditionally, the expansion of global aircraft fleets, rising maintenance, repair, and overhaul (MRO) activities, and increasing investments in next-generation aerospace manufacturing technologies are expected to further accelerate the adoption of NDT solutions across the aerospace industry.

Market expansion follows higher aircraft utilization, tighter airworthiness oversight, and increasing structural complexity across civil, defense, and space platforms. NDT supports production assurance, scheduled maintenance, and life-extension decisions across the aircraft lifecycle. Aging fleets in mature markets keep inspection intensity high, while OEM delivery backlogs increase in-process inspection volume at assembly sites and tier suppliers. Composite-heavy airframes and advanced alloys raise defect-detection requirements, which lifts demand for phased-array ultrasonics, advanced eddy current, and digital radiography.

Demand strengthens across commercial aviation, military fleets, business jets, and space systems. Airlines use NDT to protect dispatch reliability and limit aircraft-on-ground exposure under tight turnaround windows. Defense operators apply advanced inspection to sustain mission-ready aircraft and critical rotables, especially on propulsion systems and primary structures. Space launch providers and satellite manufacturers apply NDT to engines, tanks, and bonded structures where small discontinuities can drive costly rework or mission failure. On the supply side, equipment OEMs, software vendors, and certified service providers expand capacity through automation, technician training, and mobile inspection cells near major MRO hubs.

Regulation shapes purchasing and operating models. FAA and EASA maintenance requirements, aerospace quality systems such as AS9100, and accreditation regimes for inspection practices raise audit intensity and accelerate digital records and automated reporting. AI-assisted indication classification, automated scan planning, and connected instruments reduce interpretation variability and shorten inspection cycles, while analytics supports condition-based maintenance. These gains coexist with risks tied to certification lead times, skilled-labor scarcity, high capex for radiography and robotics, and cybersecurity exposure in connected workflows. North America led in 2024 with more than a 40.3% share, or USD 0.74 billion, and investment concentrates around the U.S. and Canada. Europe holds an estimated 27% share, while Asia Pacific approaches 23% with rising spend in India, China, and Singapore. The Middle East contributes about 6% of revenue, led by the UAE and Saudi Arabia as widebody maintenance expands, and the balance comes from Latin America and Africa. Pricing pressure in airline MRO encourages higher automation rates and standardized digital work instructions to protect margins while maintaining compliance.

, By Technique (Traditional/Conventional NDT, AI-enabled NDT), By Testing Method (Ultrasonic Testing, Radiographic Testing, Magnetic Particle Testing, Liquid Penetrant Testing, Visual Inspection, Eddy-Current Testing, Acoustic Emission Testing, Thermography/Infrared Testing, Computed Tomography Testing) Industry Regional Outlook, Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market expands at 7.1%, 2026-2034, supported by higher aircraft build rates and inspection intensity. The U.S. market reaches 0.67 billion USD, 2025.

- Segment Dominance: Equipment leads with 45.2%, 2024, driven by spending on precision scanners, phased-array probes, and CT systems. Capital deployment concentrates in high-throughput manufacturing and MRO lines at estimated: 0.9 billion USD, 2024.

- Segment Dominance: Conventional techniques hold 73.6%, 2024, as certification and auditability keep them preferred in safety-critical programs. AI-enabled and automated methods advance from estimated: 12.0%, 2024, as validation evidence accumulates.

- Driver: Aircraft production and composite adoption drive higher inspection demand at estimated: 6.0%, 2024, across new-build and heavy-check workloads. Operators raise utilization to estimate: 9.0 hours/day, 2024, which increases recurring NDT cycles.

- Restraint: Certification lead times and qualified labor constraints slow deployment, keeping technician shortages at estimated: 8.0%, 2024. High capex limits rapid upgrades, with advanced CT systems priced at estimated: 2.5 million USD, 2024.

- Opportunity: Digital and automated inspection expands addressable spend to estimate: 1.6 billion USD, 2034, as OEMs and MROs standardize digital traceability. AI-assisted analytics improves defect triage speed by estimated: 20.0%, 2024.

- Trend: Phased-array and AI-enhanced ultrasonic tools accelerate, with UT at 20.8%, 2024, and growing share within critical structure inspection. Automation increases scan repeatability to estimated: 95.0% pass consistency, 2024, in high-volume cells.

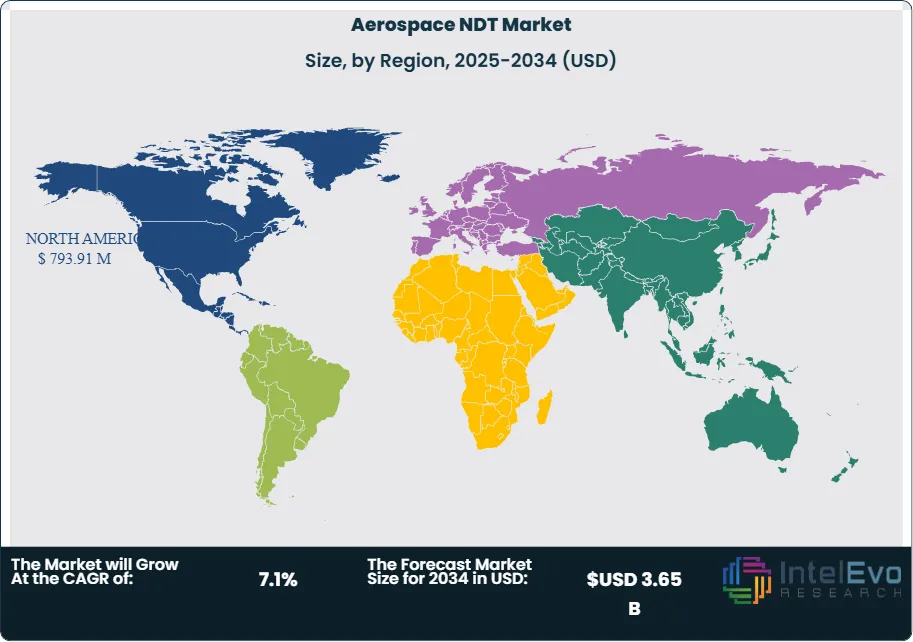

- Regional Analysis: North America leads with 40.3%, 2024, anchored by FAA oversight and a deep MRO base. The region delivers 0.74 billion USD, 2024, and the U.S. contributes 0.67 billion USD, 2025.

By Component

Equipment represents the largest share of the aerospace non-destructive testing market, accounting for about 45% of total revenue in 2025. Demand concentrates on high-precision assets such as ultrasonic inspection systems, digital radiography units, phased-array probes, and computed tomography platforms. These systems form the backbone of quality assurance across aircraft manufacturing lines and maintenance facilities, where regulators require consistent detection of micro-cracks, voids, and material fatigue.

Capital intensity remains high, with advanced radiographic and CT systems often exceeding USD 2 million per unit in 2025. Aerospace OEMs and MRO providers continue to prioritize equipment upgrades to meet tighter inspection tolerances and higher aircraft utilization rates. Equipment versatility across multiple testing techniques supports both in-process manufacturing inspections and recurring heavy maintenance checks.

Automation and embedded analytics increasingly shape equipment investment decisions. Automated scanners and sensor-rich platforms reduce inspection cycle times and support condition-based maintenance strategies. This shift lowers aircraft-on-ground duration and supports reliability targets for commercial airlines operating under narrow margin structures.

By Technique

Traditional or conventional NDT techniques retain a dominant position, holding approximately 73.6% of market share in 2025. Visual inspection, magnetic particle testing, liquid penetrant testing, and radiographic testing remain deeply embedded in aerospace certification frameworks. Regulators and operators continue to rely on these techniques for safety-critical structures due to their repeatability and established qualification standards.

Cost control also reinforces the role of conventional methods. These techniques require lower capital outlay and simpler training pathways compared with advanced digital systems. As a result, they remain standard across line maintenance and routine inspections, particularly in regions with large installed aircraft fleets.

AI-enabled and software-assisted techniques expand steadily but function mainly as supplements. Operators deploy them selectively where data density and speed offer measurable gains, while conventional techniques continue to anchor compliance-driven inspection programs.

By Testing Method

Ultrasonic testing accounts for roughly 20.8% of aerospace NDT revenue in 2025, reflecting its broad applicability across metallic and composite structures. UT plays a central role in inspecting wings, fuselage sections, landing gear, and engine components, where internal defects pose significant safety risks.

Phased-array ultrasonic systems now dominate new UT installations, enabling multi-angle inspection and faster coverage. Automated ultrasonic scanners support higher inspection throughput during scheduled maintenance events, particularly for widebody fleets with compressed turnaround schedules.

Integration of machine-assisted signal analysis improves defect characterization and consistency. These advances reduce dependency on manual interpretation and support earlier identification of fatigue-related damage, extending component service life.

By Region

North America remains the leading regional market with approximately 40.3% share in 2025, supported by strong aerospace manufacturing output and a mature MRO network. Regional revenue stands near USD 0.67 billion, with growth tracking a CAGR of about 5.3% through the forecast period. Concentration of major production and maintenance hubs sustains steady inspection demand.

Regulatory enforcement by the Federal Aviation Administration drives high inspection frequency and technology adoption. Composite-intensive aircraft programs increase reliance on ultrasonic and radiographic techniques across both commercial and defense fleets.

The United States anchors regional performance through large OEM production volumes and a robust aftermarket services sector. Ongoing investment in military fleet upgrades, space systems, and advanced air mobility platforms continues to support long-term demand for aerospace NDT services and equipment.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Equipment

- Software

- Services

- Consumables

By Technique

- Traditional/Conventional

- AI-enabled

By Testing Method

- Ultrasonic Testing

- Radiographic Testing

- Magnetic Particle Testing

- Liquid Penetrant Testing

- Visual Inspection Testing

- Eddy-Current Testing

- Acoustic Emission Testing

- Thermography/Infrared Testing

- Computed Tomography Testing

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.97 B |

| Forecast Revenue (2034) | USD 3.65 B |

| CAGR (2025-2034) | 7.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Equipment, Software, Services, Consumables), By Technique (Traditional/Conventional, AI-enabled), By Testing Method (Ultrasonic Testing, Radiographic Testing, Magnetic Particle Testing, Liquid Penetrant Testing, Visual Inspection Testing, Eddy-Current Testing, Acoustic Emission Testing, Thermography/Infrared Testing, Computed Tomography Testing) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Nikon Corporation, Mistras Group Inc., Element Materials Technology Group Ltd., Intertek Group plc, Waygate Technologies GmbH, Teledyne Technologies Incorporated, Spirit AeroSystems Holdings Inc. (NDT Centers), Applus Services SA, Zetec Inc., Bombardier Inc. (In-house NDT), Eddyfi Technologies Inc., TWI Ltd., Lufthansa Technik AG (NDT Services), Magnaflux Corporation, General Electric Company (GE Aviation NDT Solutions), Ashtead Technology Ltd., Baker Hughes Company, Fischer Technology Inc., Olympus Corporation, YXLON International GmbH, Collins Aerospace (UTAS NDT Lab), Hologic Inc. (SureScan), Sonatest Ltd., SGS SA, Airbus S.A.S (AIRTAC NDT), Vermont Ultrasonics Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technique (Traditional/Conventional NDT, AI-enabled NDT), By Testing Method (Ultrasonic Testing, Radiographic Testing, Magnetic Particle Testing, Liquid Penetrant Testing, Visual Inspection, Eddy-Current Testing, Acoustic Emission Testing, Thermography/Infrared Testing, Computed Tomography Testing) Industry Regional Outlook, Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

, By Technique (Traditional/Conventional NDT, AI-enabled NDT), By Testing Method (Ultrasonic Testing, Radiographic Testing, Magnetic Particle Testing, Liquid Penetrant Testing, Visual Inspection, Eddy-Current Testing, Acoustic Emission Testing, Thermography/Infrared Testing, Computed Tomography Testing) Industry Regional Outlook, Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

, By Technique (Traditional/Conventional NDT, AI-enabled NDT), By Testing Method (Ultrasonic Testing, Radiographic Testing, Magnetic Particle Testing, Liquid Penetrant Testing, Visual Inspection, Eddy-Current Testing, Acoustic Emission Testing, Thermography/Infrared Testing, Computed Tomography Testing) Industry Regional Outlook, Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Aerospace NDT Market?

Global Aerospace NDT Market was valued at USD 1.84 billion in 2024 and is projected to reach USD 3.65 billion by 2034, growing at a CAGR of 7.1%. Explore key trends, technologies, MRO demand, and growth opportunities.

Who are the major players in the Aerospace NDT Market?

Nikon Corporation, Mistras Group Inc., Element Materials Technology Group Ltd., Intertek Group plc, Waygate Technologies GmbH, Teledyne Technologies Incorporated, Spirit AeroSystems Holdings Inc. (NDT Centers), Applus Services SA, Zetec Inc., Bombardier Inc. (In-house NDT), Eddyfi Technologies Inc., TWI Ltd., Lufthansa Technik AG (NDT Services), Magnaflux Corporation, General Electric Company (GE Aviation NDT Solutions), Ashtead Technology Ltd., Baker Hughes Company, Fischer Technology Inc., Olympus Corporation, YXLON International GmbH, Collins Aerospace (UTAS NDT Lab), Hologic Inc. (SureScan), Sonatest Ltd., SGS SA, Airbus S.A.S (AIRTAC NDT), Vermont Ultrasonics Inc., Others

Which segments covered the Aerospace NDT Market?

By Component (Equipment, Software, Services, Consumables), By Technique (Traditional/Conventional, AI-enabled), By Testing Method (Ultrasonic Testing, Radiographic Testing, Magnetic Particle Testing, Liquid Penetrant Testing, Visual Inspection Testing, Eddy-Current Testing, Acoustic Emission Testing, Thermography/Infrared Testing, Computed Tomography Testing)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date