- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Agentic AI in Law Enforcement & Surveillance Market Size 2025–2034 | CAGR 39.1%

Global Agentic AI in Law Enforcement & Surveillance Market Size, Share & Growth Analysis By Offering (Security & Surveillance AI, Law Enforcement Software Solutions, Services), By Technology (Computer Vision, Machine Learning, Deep Learning, NLP), By Deployment Model (Cloud-Based, On-Premises), By Enterprise Size (SMEs, Large Enterprises), By Region & Key Players – Industry Overview, Regulatory Landscape, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2026–2034

Report Overview

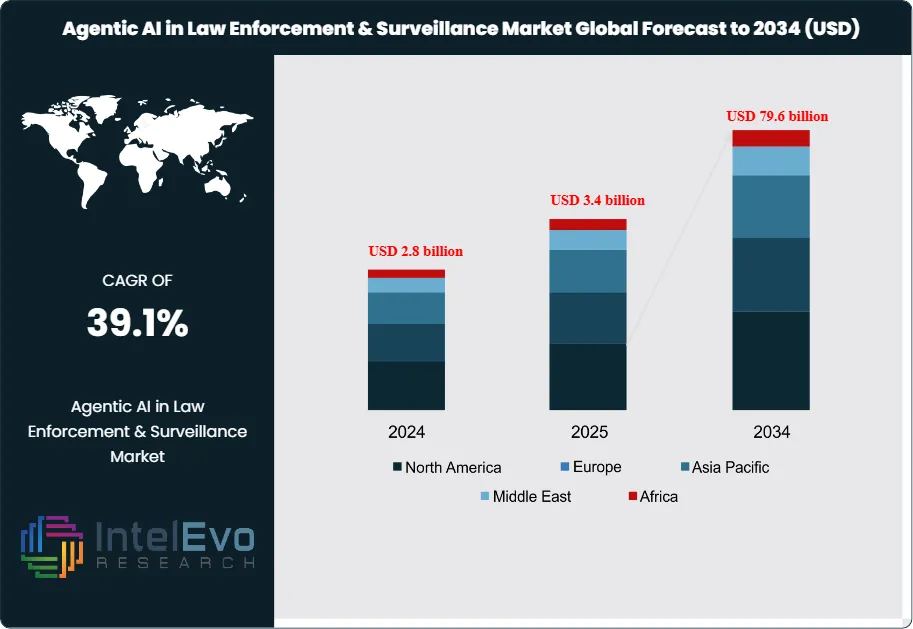

The Agentic AI in Law Enforcement & Surveillance Market is estimated to reach approximately USD 3.4 billion in 2025 and is projected to surge to around USD 79.6 billion by 2034, registering a very strong compound annual growth rate (CAGR) of about 39.1% during the forecast period from 2026 to 2034. This exceptional growth is driven by rising adoption of autonomous and semi-autonomous AI systems for real-time threat detection, predictive policing, facial recognition, and large-scale video analytics. Law enforcement agencies and public safety organizations increasingly deploy agentic AI to reduce response times, automate surveillance workflows, and enhance situational awareness across smart cities and critical infrastructure.

Get More Information about this report -

Request Free Sample ReportAdditionally, growing investments in AI-enabled border security, counterterrorism, and urban monitoring solutions are accelerating global adoption, positioning agentic AI as a transformative force in next-generation security and surveillance ecosystems. Growth reflects rapid uptake across policing, border management, and critical infrastructure as agencies seek better awareness, faster response, and leaner staffing.

Agentic AI describes systems that interpret complex environments, select actions, and execute tasks with constrained human oversight. In law enforcement and surveillance, these capabilities support facial and object recognition, anomalous behavior detection, and predictive risk scoring across video and sensor feeds. A Deloitte analysis indicates that such smart technologies can reduce crime by 30–40% and cut emergency response times by 20–35%, reinforcing the investment case.

Demand-side momentum stems from rising urbanization, sophisticated criminal activity, and heightened expectations for public safety. Governments embed AI-based monitoring into smart city programs and national security strategies, often backed by digital infrastructure budgets. On the supply side, advances in machine learning, computer vision, and edge computing improve detection accuracy, lower false positives, and enable near real-time analysis. Vendors differentiate through scalable platforms that integrate with command centers, patrol vehicles, and body-worn devices.

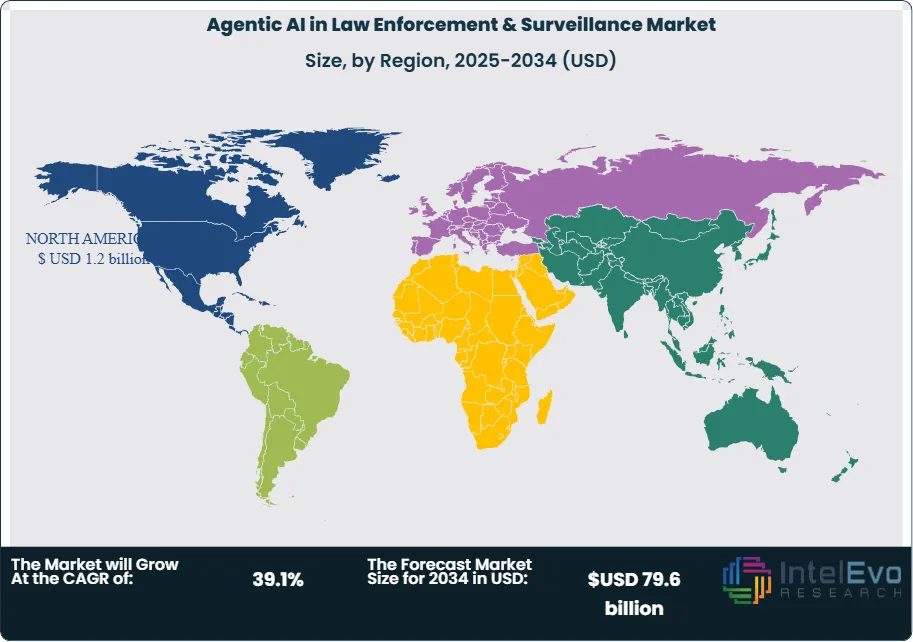

Regional adoption remains uneven. North America accounted for more than 44.5% of global revenue in 2024, or about USD 1.2 billion, supported by federal and municipal procurement and an active ecosystem of AI software and cloud providers. Europe advances under strict data protection frameworks and the EU Artificial Intelligence Act, which favor transparent and auditable systems. Asia-Pacific, the Middle East, and parts of Latin America emerge as investment hotspots as governments fund AI-enabled border surveillance and large urban video networks.

Risk and regulation now shape deployment strategies. Agencies face scrutiny over privacy, bias, and civil liberties, while interconnected assets increase cyber exposure. According to DigitalDefynd, 95% of organizations prioritize strong data safeguards to comply with evolving rules and limit breach impact. Providers respond with privacy-by-design architectures, secure data pipelines, and governance functions that log decisions and support oversight. As ethical norms, technical standards, and procurement criteria consolidate, agentic AI is set to move from pilot projects to core infrastructure within modern public safety systems.

, By Technology (Computer Vision, Machine Learning, Deep Learning, NLP), By Deployment Model (Cloud-Based, On-Premises), By Enterprise Size (SMEs, Large Enterprises), By Region & Key Players – Industry Overview, Regulatory Landscape, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market grows from USD 3.4 billion in 2025 to USD 79.6 billion by 2034, delivering a 39.1% CAGR, 2026-2034. This expansion reflects sustained deployment of agentic AI across law enforcement and surveillance operations over 2024-2034.

- Segment Dominance: Solution offerings dominate with an 82.8% revenue share, 2024, underscoring preference for full-stack platforms over standalone services. On-premises deployments hold 66.2% share, 2024, as agencies prioritize control over sensitive data and infrastructure.

- Segment Dominance: NLP capabilities secure a 30.5% share of the market, 2024, as agencies apply voice analysis, chatbots, and text intelligence in operations. Large enterprises account for 70.3% of total spending, 2024, reflecting their capacity to fund advanced AI-driven surveillance and risk systems.

- Driver: Accelerating AI adoption in security drives demand as the overall market posts a 38.7% CAGR, 2024-2034. The United States market alone grows from 0.996 billion USD, 2024 at a 36.2% CAGR, 2024-2034, highlighting strong institutional investment.

- Restraint: Strict compliance and privacy obligations slow rollout, with agencies diverting an estimated: 20.0% of implementation budgets to governance and audits, 2024. This compliance burden lengthens deployment cycles and delays some share of planned projects over 2024-2034.

- Opportunity: Vendors can unlock new revenue by targeting mid-sized agencies and cloud-ready workloads, an addressable pool estimated: 3.0 billion USD, 2034. Converting even an estimated: 25.0% of current on-premises workloads, 2024 to hybrid models, 2034 would materially expand recurring revenue.

- Trend: Agencies increasingly integrate NLP, which holds 30.5% segment share, 2024, and could rise to an estimated: 45.0% share, 2034 as conversational and analytics tools mature. Hybrid architectures that blend the 66.2% on-premises base, 2024 with secure cloud analytics gain traction through 2024-2034.

- Regional Analysis: North America leads with 44.5% of global revenue, 2024, equivalent to 1.2 billion USD, 2024, supported by U.S. spending of 0.996 billion USD, 2024. Emerging programs in Asia-Pacific are set to reach an estimated: 30.0% global share, 2034, positioning the region as the next major growth engine over 2024-2034.

By Offering

The market continues to shift toward integrated AI offerings in 2025. Solution-based deployments account for more than four fifths of total revenue, reflecting strong reliance on AI tools that support surveillance, identity verification, threat screening, and tactical decision support. Security and surveillance AI platforms, including facial recognition, video analytics, and automated threat detection, remain the core investment area for public agencies. These tools process large volumes of visual and operational data at high speed, enabling officers to act on verified information rather than manual interpretation.

Law enforcement software solutions also expand quickly. Crime analytics, digital evidence management, and predictive activity mapping allow agencies to consolidate disparate databases and identify risk patterns with greater accuracy. The market sees steady demand for digital records systems as agencies move toward standardized evidence workflows and real-time operational dashboards. Services such as implementation, integration, training, and continuous support form a growing secondary revenue stream. Agencies depend on these services to manage deployment risks and ensure compliance with internal security protocols.

Adoption increases as agencies face growing data volumes and operational pressure. You see stronger investment in software customizations that align with local legal requirements and internal governance needs. Vendors respond with modular architectures that support phased adoption and structured upgrades across policing networks.

By Technology

Natural language processing holds a sizable position in 2025, supported by the need to interpret audio, communication logs, and written records. NLP systems classify speech, extract keywords, and generate structured summaries from unstructured sources. Agencies use these tools to automate transcription, accelerate case documentation, and detect sentiment patterns that may indicate risk. Computer vision and deep learning strengthen automated detection functions, especially as camera networks expand across urban areas.

Machine learning models support forecasting and trend identification across crime datasets. These models help analysts identify hotspots, anticipate emerging behaviors, and test intervention strategies. Reinforcement learning and neural network frameworks remain in early deployment stages but gain visibility as agencies test autonomous monitoring scenarios.

The continuous flow of surveillance, sensor, and communication data pushes agencies to adopt more sophisticated AI techniques. You see growing interest in hybrid models that combine NLP and computer vision outputs for broader situational interpretation.

By Deployment Model

On-premises deployments remain dominant in 2025. Agencies continue to favor full control over sensitive data repositories, especially for facial recognition outputs, criminal records, and intelligence files. Localized infrastructure aligns with strict data governance rules and supports integration with legacy systems that require high security thresholds. Many agencies consider on-premises solutions essential when handling confidential investigations or classified intelligence.

Cloud-based deployments grow at a steady rate as modernization programs push departments toward more flexible computing resources. Cloud environments help agencies scale analytical workloads and maintain system performance during peak operational demands. Hybrid deployments are now common in larger jurisdictions, where non-sensitive workloads move to cloud environments while core evidence systems remain on premises.

Despite growing cloud capabilities, operational risk and compliance hurdles slow adoption in certain markets. You see agencies conducting multi-year transition planning to avoid disruption of mission-critical processes.

By Enterprise Size

Large enterprises continue to represent the leading customer segment. These organizations control broader jurisdictions, larger staff counts, and wider surveillance networks that generate substantial data streams. They invest in complex AI ecosystems that unify crime analytics, mobility systems, automated monitoring, and evidence repositories. Their financial capacity supports long planning cycles, multi-site deployment, and specialized personnel training.

Small and medium-sized agencies gradually increase AI adoption, supported by lower-cost analytics modules and cloud-based subscription models. Their adoption path focuses on targeted applications such as video analytics or records automation. Vendors respond by offering smaller packages that reduce integration complexity and shorten implementation timelines.

The market sees rising demand from regional clusters of SMEs that share infrastructure and coordinate technology procurement across districts. These models help smaller agencies reach performance levels previously restricted to large institutions.

By Region

North America maintains its lead in 2025, supported by high spending on public safety modernization and mature digital infrastructure. U.S. agencies deploy advanced surveillance, identity systems, and automated analytics across urban environments. Canada increases adoption of AI-assisted monitoring tools to support border security and emergency response operations. The region benefits from a strong vendor base and continuous pilot programs that test new applications at scale.

Europe advances at a steady pace. Strict privacy rules shape procurement decisions, pushing agencies toward transparent audit systems and compliant data architectures. Investment grows across Western Europe, while Eastern Europe accelerates deployments in border control and mobility security.

Asia Pacific records the fastest expansion. Rapid urbanization, extensive camera networks, and government security initiatives underpin demand. Markets such as China, Japan, South Korea, and Australia scale AI platforms to support city-wide surveillance and operational analytics. Latin America and the Middle East increase adoption with a focus on crime pattern detection, perimeter security, and crowd monitoring in high-density zones. Both regions turn to AI to address rising security risks and build centralized monitoring hubs.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Solution

- Security and Surveillance AI

- Facial Recognition

- Video Analytics

- Threat Detection Systems

- Others

- Law Enforcement Software Solutions

- Crime Analytics

- Records Management

- Digital Evidence Management

- Predictive Policing

- Resource Allocation

- Incident Management

- Others

- Services

- Implementation and Integration Services

- Consulting & Training

- Support & Maintenance Services

By Technology

- Natural Language Processing (NLP)

- Computer Vision

- Machine Learning

- Deep Learning

- Others (Reinforcement Learning, Neural Networks, etc.)

By Deployment Model

- Cloud-based

- On-premises

By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.4 billion |

| Forecast Revenue (2034) | USD 79.6 billion |

| CAGR (2025-2034) | 39.1% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering (Solution, Law Enforcement Software Solutions, Services), By Technology (Natural Language Processing (NLP), Computer Vision, Machine Learning, Deep Learning, Others (Reinforcement Learning, Neural Networks, etc.)), By Deployment Model (Cloud-based, On-premises), By Enterprise Size (Small and Medium Enterprises (SMEs), Large Enterprises) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Cognitiv, Microsoft Corporation, Genetec Inc., OpenAI, Clearview AI, Inc., International Business Machines Corporation (IBM), Motorola Solutions, Inc., Nvidia Corporation, Amazon Web Services Inc. (AWS), IntelliVision, Palantir Technologies Inc., C3.ai Inc., Google LLC, NEC Corporation, Veritone Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Computer Vision, Machine Learning, Deep Learning, NLP), By Deployment Model (Cloud-Based, On-Premises), By Enterprise Size (SMEs, Large Enterprises), By Region & Key Players – Industry Overview, Regulatory Landscape, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2026–2034")

, By Technology (Computer Vision, Machine Learning, Deep Learning, NLP), By Deployment Model (Cloud-Based, On-Premises), By Enterprise Size (SMEs, Large Enterprises), By Region & Key Players – Industry Overview, Regulatory Landscape, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2026–2034")

, By Technology (Computer Vision, Machine Learning, Deep Learning, NLP), By Deployment Model (Cloud-Based, On-Premises), By Enterprise Size (SMEs, Large Enterprises), By Region & Key Players – Industry Overview, Regulatory Landscape, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Agentic AI in Law Enforcement & Surveillance Market?

The Agentic AI in Law Enforcement & Surveillance Market is projected to grow from USD 3.4 billion in 2025 to USD 79.6 billion by 2034, expanding at a CAGR of 39.1% during 2026–2034, driven by AI-powered surveillance, predictive policing, facial recognition, and smart city security deployments.

Who are the major players in the Agentic AI in Law Enforcement & Surveillance Market?

Cognitiv, Microsoft Corporation, Genetec Inc., OpenAI, Clearview AI, Inc., International Business Machines Corporation (IBM), Motorola Solutions, Inc., Nvidia Corporation, Amazon Web Services Inc. (AWS), IntelliVision, Palantir Technologies Inc., C3.ai Inc., Google LLC, NEC Corporation, Veritone Inc., Others

Which segments covered the Agentic AI in Law Enforcement & Surveillance Market?

By Offering (Solution, Law Enforcement Software Solutions, Services), By Technology (Natural Language Processing (NLP), Computer Vision, Machine Learning, Deep Learning, Others (Reinforcement Learning, Neural Networks, etc.)), By Deployment Model (Cloud-based, On-premises), By Enterprise Size (Small and Medium Enterprises (SMEs), Large Enterprises)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Agentic AI in Law Enforcement & Surveillance Market

Published Date : 02 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date