- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Agentic AI Platform Market Size & Forecast 2034 | CAGR 33.9%

Global Agentic AI Platform Market Size, Share, Growth & Industry Analysis By Offering (Platform/Solution, Services Including Consulting, Implementation & Managed Services), By Deployment (Cloud, On-Premise & Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Vertical (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Retail & E-Commerce, Manufacturing, Government & Defense, Others) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 7.8 Billion | USD 108.2 Billion | 33.9% | North America, 44.2% |

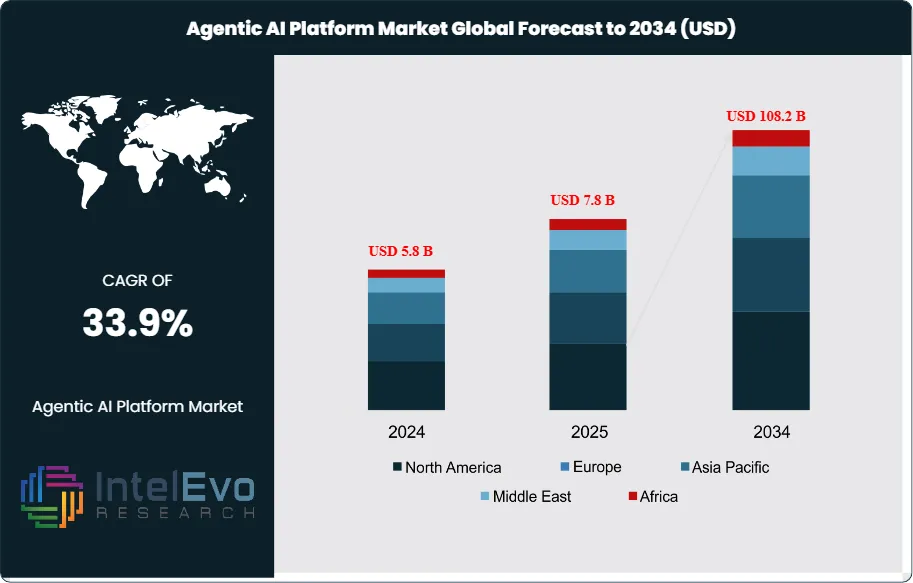

The Agentic AI Platform Market was valued at approximately USD 5.8 Billion in 2024 and reached USD 7.8 Billion in 2025. The market is projected to grow to USD 108.2 Billion by 2034, expanding at a CAGR of 33.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 100.4 Billion over the analysis period. Agentic AI platforms represent a fundamental shift from prompt-response generative AI systems toward autonomous, goal-directed software agents capable of reasoning, planning, executing multi-step tasks, and self-correcting without continuous human intervention. These platforms combine large language models, retrieval-augmented generation, tool-use APIs, memory persistence, and orchestration layers to create AI agents that operate independently across enterprise workflows.

Get More Information about this report -

Request Free Sample ReportEnterprise demand for the agentic AI platform market accelerated sharply from 2024 onward as organizations recognized that static chatbot interfaces capture less than 15% of the productivity gains available from AI. Agentic architectures unlock the remaining value by enabling AI to operate as an autonomous workforce member, completing end-to-end processes in customer service, IT operations, sales prospecting, financial reconciliation, and supply chain management. Gartner estimates that by 2028, 33% of enterprise software applications will include agentic AI, up from less than 1% in 2024. This adoption curve is the primary engine behind the market's 33.9% CAGR.

Regulatory frameworks are forming around agentic AI in both the United States and Europe. The EU AI Act classifies certain autonomous agent deployments as high-risk, requiring conformity assessments and human oversight mechanisms. In the US, Executive Orders on AI safety have prompted NIST to publish evaluation frameworks for autonomous agent reliability. These regulations add compliance costs but also create a market for governance, observability, and guardrail tooling estimated at USD 2.1 Billion by 2034. SOC 2, ISO 27001, and FedRAMP certifications serve as competitive differentiators for platform vendors targeting regulated industries such as financial services, healthcare, and defense.

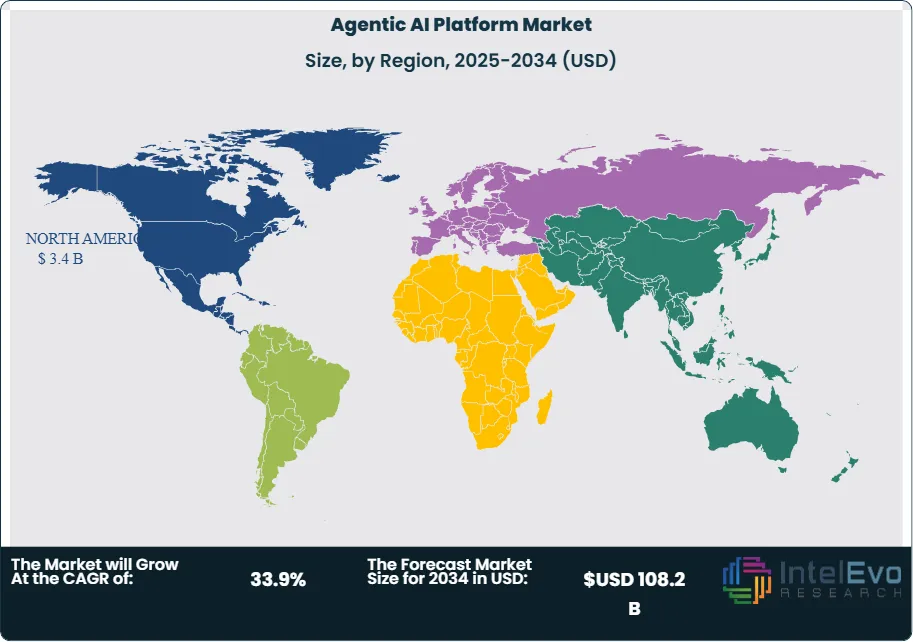

North America commanded 44.2% of global agentic AI platform revenue in 2025, generating USD 3.4 Billion. The region benefits from concentrated venture capital funding, the presence of hyperscale cloud providers, and early enterprise adoption across Fortune 500 companies. Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 37.8% through 2034, driven by government AI strategies in China, India, Japan, and South Korea. Europe holds 24.6% market share, with strong demand from automotive, manufacturing, and financial services sectors. Investment in agentic AI infrastructure, including specialized inference hardware and low-latency agent-serving architectures, surpassed USD 6 Billion globally in 2025 across public and private channels.

, By Deployment (Cloud, On-Premise & Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Vertical (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Retail & E-Commerce, Manufacturing, Government & Defense, Others) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The agentic AI platform market was valued at USD 7.8 Billion in 2025 and is projected to reach USD 108.2 Billion by 2034, expanding at a CAGR of 33.9% over the 2026–2034 forecast period.

- Segment Dominance (By Offering): The platform/solution segment held 62.4% market share in 2025, valued at USD 4.9 Billion, as enterprises prioritize turnkey agent development environments over standalone services.

- Segment Dominance (By Vertical): Banking, financial services, and insurance (BFSI) led vertical adoption with a 22.8% share in 2025, driven by use cases in fraud detection, claims processing, and autonomous trading support.

- Driver: Enterprise productivity pressure is the primary growth driver; organizations deploying agentic AI report 35–45% reductions in task completion time and 20–30% cuts in operational costs for targeted workflows.

- Restraint: Data privacy and security concerns constrain adoption, with 58% of enterprises citing autonomous agent access to sensitive systems as a top-three barrier to deployment in 2025.

- Opportunity: Small and medium enterprises represent an underpenetrated segment; only 8% of SMEs had deployed agentic AI by 2025, opening a USD 12.5 Billion addressable market by 2034 as no-code agent builders mature.

- Trend: Multi-agent orchestration is the dominant architectural trend, with 41% of enterprise agent deployments in 2025 involving two or more agents collaborating on shared objectives, up from 12% in 2024.

- Regional Analysis: North America led the global agentic AI platform market with 44.2% share and USD 3.4 Billion in revenue in 2025, anchored by hyperscaler investment and early enterprise adoption.

Competitive Landscape Overview

The agentic AI platform market is moderately consolidated at the top but highly fragmented in its lower tiers. The top four players, Microsoft, Google, Salesforce, and Amazon Web Services, collectively accounted for approximately 48% of global revenue in 2025. Competition is technology-driven and platform-based, with differentiation hinging on model quality, agent orchestration capabilities, enterprise integration depth, and vertical-specific solutions. Mergers and acquisitions intensified throughout 2025 as established cloud and enterprise software vendors acquired agent framework startups to fill capability gaps. Over 35 M&A transactions exceeding USD 50 Million each were completed in the agent AI space between January 2025 and January 2026.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Microsoft | US | Leader | Azure AI Agent Service | North America | Expanded Copilot Studio agentic capabilities with 1,800+ enterprise clients (Feb 2025) |

| Google (Alphabet) | US | Leader | Vertex AI Agent Builder | Global | Launched Agentspace for enterprise multi-agent orchestration (Jan 2026) |

| Salesforce | US | Leader | Agentforce Platform | North America | Released Agentforce 2.0 with autonomous CRM agents; USD 900M bookings (Dec 2024) |

| Amazon Web Services | US | Leader | Amazon Bedrock Agents | Global | Integrated multi-agent collaboration in Bedrock; 100K+ agent deployments (Mar 2025) |

| IBM | US | Challenger | watsonx Orchestrate | North America | Acquired Apptio agentic workflow assets for USD 4.6B (Jun 2025) |

| ServiceNow | US | Challenger | Now Assist AI Agents | North America | Deployed 50,000+ autonomous IT agents across Fortune 500 clients (Sep 2025) |

| UiPath | US | Challenger | Autopilot Agent Platform | Europe | Launched agentic process automation framework with 300+ pre-built agents (Mar 2025) |

| Palantir Technologies | US | Niche Player | AIP Agent Framework | North America | Secured USD 480M US defense contract for agentic decision systems (Jan 2026) |

| Cohere | Canada | Niche Player | Command R+ Agent Toolkit | North America | Raised USD 500M Series D for enterprise agent platform expansion (May 2025) |

| CrewAI | US | Niche Player | CrewAI Multi-Agent Framework | North America | Reached 20M+ open-source downloads; launched enterprise tier (Aug 2025) |

By Offering

The platform/solution segment dominated the agentic AI platform market with a 62.4% share in 2025, generating USD 4.9 Billion in revenue. This segment encompasses agent development environments, orchestration engines, memory and state management layers, tool-use integration frameworks, and pre-built agent templates. Microsoft Azure AI Agent Service, Google Vertex AI Agent Builder, and Salesforce Agentforce represent the leading commercial platforms. Enterprise buyers prefer integrated platforms that reduce time-to-deployment; the average implementation cycle for a platform-based agent deployment was 6–8 weeks in 2025, compared to 4–6 months for custom-built alternatives. Platform vendors are embedding guardrail tooling, observability dashboards, and compliance modules directly into their offerings, raising switching costs and deepening customer lock-in.

The services segment captured 37.6% of the market in 2025, valued at USD 2.9 Billion. This category includes consulting, implementation, integration, training, and managed agent operations. Systems integrators such as Accenture, Deloitte, and Wipro have established dedicated agentic AI practices. Demand for agent fine-tuning, prompt engineering, and custom tool-calling configurations continues to rise as enterprises scale from pilot programs to production deployments. Managed services for ongoing agent monitoring, performance tuning, and incident response accounted for approximately 40% of services revenue in 2025.

By Deployment

Cloud-based deployment held 71.3% of the agentic AI platform market in 2025, reflecting enterprise preference for scalable, pay-as-you-go agent infrastructure. Cloud-native agent platforms benefit from elastic compute resources essential for inference-heavy workloads, seamless integration with existing SaaS applications, and rapid model updates without on-premise hardware refreshes. AWS, Azure, and Google Cloud serve as the primary hosting environments for the majority of commercial agent deployments. The average enterprise spent USD 380,000 annually on cloud-hosted agent infrastructure in 2025.

On-premise and hybrid deployments captured the remaining 28.7% share, valued at USD 2.2 Billion in 2025. Financial services institutions, defense agencies, healthcare providers, and government bodies favor on-premise deployments due to data sovereignty, regulatory compliance, and latency requirements. Hybrid architectures, where agent orchestration occurs in the cloud while sensitive data processing stays on-premise, grew 52% year-over-year in 2025. IBM watsonx Orchestrate and Palantir AIP are the strongest contenders in the on-premise and hybrid segment.

By Enterprise Size

Large enterprises accounted for 78.5% of the agentic AI platform market in 2025, spending USD 6.1 Billion on agent infrastructure, development, and services. These organizations deploy agents across multiple departments, including IT helpdesk automation, financial close processes, HR onboarding, and customer support resolution. The average Fortune 500 company operated 12 distinct AI agents in production by the end of 2025. Budget allocation for agentic AI within large enterprise IT spending grew from 2.1% in 2024 to 5.8% in 2025.

Small and medium enterprises contributed 21.5% of market revenue in 2025, totaling USD 1.7 Billion. Adoption among SMEs is accelerating as no-code and low-code agent builders reduce technical barriers. Platforms such as CrewAI, LangChain-based solutions, and Salesforce Agentforce Starter enable SME deployment without dedicated AI engineering teams. The average SME agent deployment cost was USD 2,400 per month in 2025, a 60% reduction from 2024 pricing levels.

By Vertical

BFSI led vertical adoption in the agentic AI platform market with a 22.8% share and USD 1.8 Billion in revenue in 2025. Autonomous agents perform fraud detection, anti-money laundering screening, claims adjudication, loan underwriting assessment, and client portfolio rebalancing. JPMorgan Chase reported that its agentic AI deployments reduced document review time by 55% across investment banking operations. Regulatory technology agents that monitor compliance in real time represent the fastest-growing sub-use-case within BFSI.

IT and telecommunications held 18.4% of the market in 2025, generating USD 1.4 Billion. Agents handle incident resolution, infrastructure monitoring, network optimization, and automated ticket routing. ServiceNow and BMC Software have embedded agentic capabilities into their ITSM platforms. Healthcare and life sciences accounted for 14.2% at USD 1.1 Billion, with agents deployed for clinical trial data management, patient scheduling, prior authorization, and drug interaction checking. Retail and e-commerce captured 12.6% at USD 0.98 Billion through agents managing inventory optimization, dynamic pricing, and personalized customer engagement. Manufacturing (11.3%), government and defense (10.5%), and other verticals (10.2%) completed the vertical distribution.

Regional Analysis

North America

North America dominated the agentic AI platform market with a 44.2% share and USD 3.4 Billion in revenue in 2025. The United States alone generated USD 3.0 Billion, representing 88% of regional revenue. Silicon Valley, Seattle, and New York serve as primary innovation centers, housing the headquarters of Microsoft, Google, Salesforce, AWS, and dozens of agent-focused startups. US venture capital firms deployed over USD 4.2 Billion into agentic AI companies during 2025. Federal government spending on AI agents, particularly through the Department of Defense and intelligence community, exceeded USD 1.1 Billion in fiscal year 2025. Canada contributed USD 280 Million, with Montreal, Toronto, and Vancouver forming a strong AI research corridor. Cohere and other Canadian-origin companies are scaling enterprise agent platforms globally. Mexico accounted for USD 120 Million, driven by nearshoring-related IT modernization.

Europe

Europe held 24.6% of the agentic AI platform market in 2025, generating USD 1.9 Billion. Germany led the region at USD 520 Million, with strong adoption in automotive manufacturing, industrial automation, and financial services. BMW, Siemens, and Deutsche Bank have each deployed multi-agent systems across their operations. The United Kingdom contributed USD 460 Million, anchored by London's fintech sector and growing government investment in AI-powered public services. France generated USD 310 Million, driven by Mistral AI's agent platform offerings and enterprise adoption in luxury retail and aerospace. The EU AI Act's risk-based classification system has created compliance tooling demand estimated at USD 180 Million across Europe in 2025. SAP, Siemens, and UiPath are the strongest European-headquartered competitors.

Asia Pacific

Asia Pacific captured 22.5% of the global agentic AI platform market in 2025, valued at USD 1.8 Billion, and is projected to grow at 37.8% CAGR through 2034. China led the region with USD 680 Million, supported by Baidu, Alibaba, and ByteDance investing in autonomous agent platforms for e-commerce, logistics, and smart city applications. The Chinese government allocated over USD 2 Billion in AI infrastructure spending for 2025. Japan generated USD 380 Million, with adoption concentrated in manufacturing, robotics coordination, and financial services. SoftBank and NTT Data are building enterprise agent solutions for the domestic market. India contributed USD 340 Million, propelled by IT services firms such as Infosys, TCS, and Wipro building agentic AI practices for global clients. South Korea added USD 220 Million, driven by Samsung, LG, and government-funded AI acceleration programs.

Latin America

Latin America represented 4.8% of the agentic AI platform market in 2025 with USD 370 Million in revenue. Brazil accounted for USD 180 Million, led by financial institutions such as Itau Unibanco and Nubank deploying AI agents for customer service and fraud prevention. Mexico contributed USD 110 Million, with agent adoption accelerating in the banking, retail, and manufacturing sectors. Colombia generated USD 42 Million as a growing technology hub. Regional growth is constrained by lower cloud infrastructure penetration compared to developed markets, but improving internet connectivity and digital transformation mandates from governments are creating favorable conditions. The region is expected to reach 6.2% global share by 2034.

Middle East and Africa

The Middle East and Africa held 3.9% of the agentic AI platform market in 2025, generating USD 310 Million. The UAE led the region at USD 130 Million, driven by ambitious national AI strategies including the Abu Dhabi AI investment program and Dubai's autonomous government services initiative. Saudi Arabia contributed USD 100 Million, supported by NEOM, Vision 2030 digital transformation investments, and sovereign wealth fund allocations to AI infrastructure. South Africa generated USD 45 Million, primarily through financial services and mining sector adoption. The region benefits from government-led digital transformation but faces challenges in talent availability and data center capacity. Defense and smart city applications represent the most active use cases across MEA.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Platform/Solution

- Services (Consulting, Implementation, Managed Services)

By Deployment

- Cloud

- On-Premise/Hybrid

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

By Vertical

- BFSI

- IT and Telecommunications

- Healthcare and Life Sciences

- Retail and E-Commerce

- Manufacturing

- Government and Defense

- Others

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.8 B |

| Forecast Revenue (2034) | USD 108.2 B |

| CAGR (2025-2034) | 33.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Platform/Solution, Services (Consulting, Implementation, Managed Services)), By Deployment, (Cloud, On-Premise/Hybrid), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises), By Vertical, (BFSI, IT and Telecommunications, Healthcare and Life Sciences, Retail and E-Commerce, Manufacturing, Government and Defense, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT, GOOGLE (ALPHABET), SALESFORCE, AMAZON WEB SERVICES, IBM, SERVICENOW, UIPATH, PALANTIR TECHNOLOGIES, COHERE, CREWAI, LANGCHAIN (LANGSMITH), SAP, ORACLE, ACCENTURE, ANTHROPIC, DATABRICKS, SNOWFLAKE, WORKATO, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud, On-Premise & Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Vertical (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Retail & E-Commerce, Manufacturing, Government & Defense, Others) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Deployment (Cloud, On-Premise & Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Vertical (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Retail & E-Commerce, Manufacturing, Government & Defense, Others) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Deployment (Cloud, On-Premise & Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Vertical (BFSI, IT & Telecommunications, Healthcare & Life Sciences, Retail & E-Commerce, Manufacturing, Government & Defense, Others) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the Agentic AI Platform Market?

Global agentic AI platform market valued at USD 5.8B in 2024, reaching USD 108.2B by 2034, growing at a CAGR of 33.9% from 2026–2034.

Who are the major players in the Agentic AI Platform Market?

MICROSOFT, GOOGLE (ALPHABET), SALESFORCE, AMAZON WEB SERVICES, IBM, SERVICENOW, UIPATH, PALANTIR TECHNOLOGIES, COHERE, CREWAI, LANGCHAIN (LANGSMITH), SAP, ORACLE, ACCENTURE, ANTHROPIC, DATABRICKS, SNOWFLAKE, WORKATO, OTHERS

Which segments covered the Agentic AI Platform Market?

By Offering, (Platform/Solution, Services (Consulting, Implementation, Managed Services)), By Deployment, (Cloud, On-Premise/Hybrid), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises), By Vertical, (BFSI, IT and Telecommunications, Healthcare and Life Sciences, Retail and E-Commerce, Manufacturing, Government and Defense, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date