- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Agrivoltaics Market Size, Share & Forecast 2034 | CAGR 13.5%

Global Agrivoltaics Market Size, Share, Growth Analysis By System Type (Fixed-Tilt, Tracking/Dynamic, Floating, Greenhouse Agrivoltaic Systems), By Application (Crop Cultivation, Animal Grazing, Aquaculture, Research Projects), By Technology (Bifacial Panels, Thin-Film Modules, Monocrystalline, Concentrated PV), By Installation Scale, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

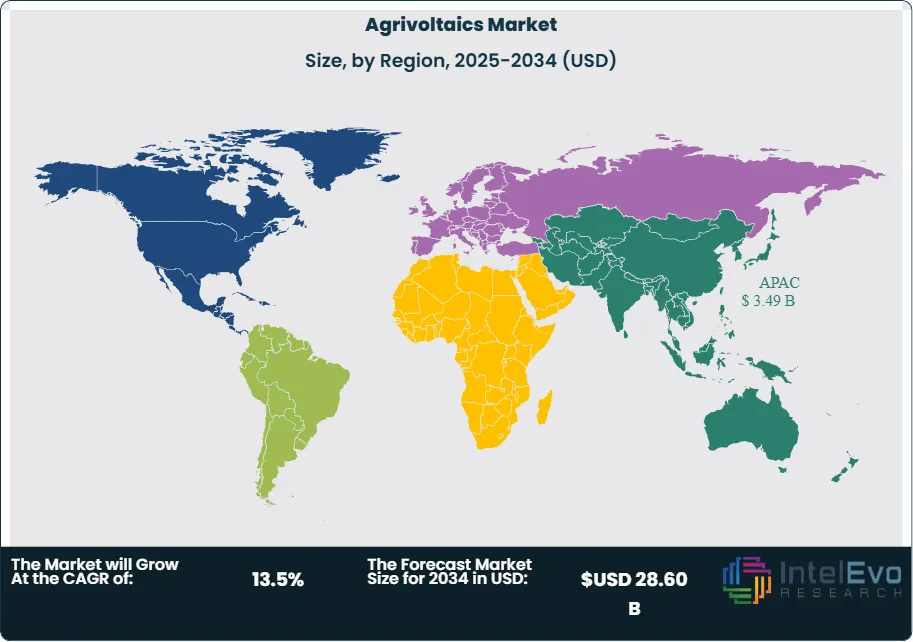

| USD 9.14 Billion | USD 28.60 Billion | 13.5% | Asia Pacific, 38.2% |

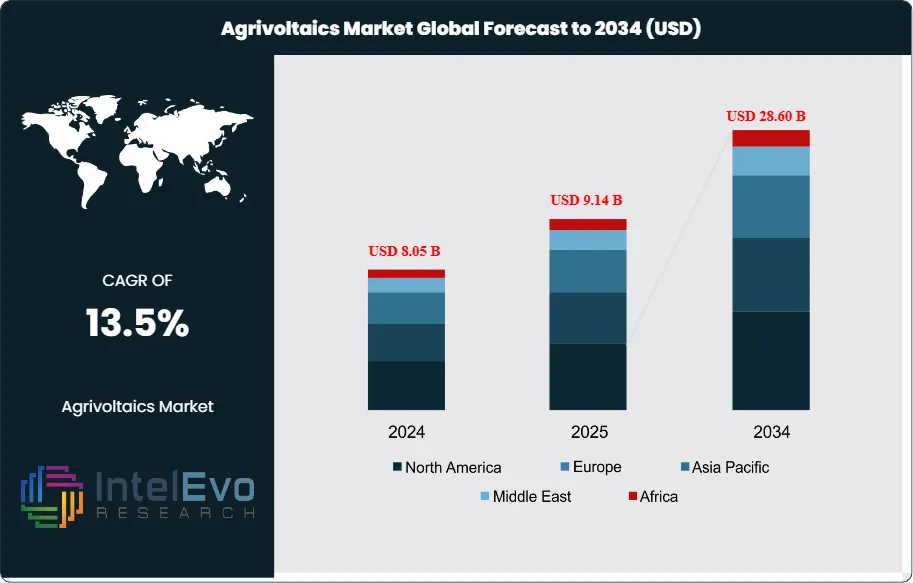

The Agrivoltaics Market was valued at approximately USD 8.05 Billion in 2024 and reached USD 9.14 Billion in 2025. The market is projected to grow to USD 28.60 Billion by 2034, expanding at a CAGR of 13.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 19.46 Billion over the analysis period, reflecting one of the most structurally significant convergences in energy and food-system planning witnessed in recent decades.

Get More Information about this report -

Request Free Sample ReportThe agrivoltaics market sits at the intersection of two critical global priorities: renewable energy generation and agricultural land productivity. Dual-use land systems that co-locate solar photovoltaic installations with active crop cultivation or animal husbandry operations are gaining rapid policy support, particularly as governments confront competing land-use pressures and energy security imperatives simultaneously. Industry analysis indicates that agrivoltaic installations delivered combined land productivity improvements of up to 60% compared to conventional single-use plots in multiple European and Asian pilot deployments through 2025.

Regulatory tailwinds are a defining force shaping the agrivoltaics market trajectory. The European Union Green Deal and its associated land-use reform directives have created structured incentive pathways for dual-use solar installations across member states, particularly in France, Germany, and Italy. In the United States, USDA initiatives including the Partnerships for Climate-Smart Commodities program have unlocked federal co-financing streams that specifically target agrivoltaic demonstration and commercialization. Japan's Ministry of Agriculture, Forestry and Fisheries has likewise revised electricity business act provisions to accelerate solar sharing adoption on agricultural land.

Technology maturation is reshaping the competitive dynamics of the agrivoltaics market. Dynamic tracking systems capable of adjusting panel tilt angles in real time based on crop light requirements have achieved commercial-scale readiness by 2025, enabling site-specific optimization that was not economically feasible prior to 2022. Bifacial panel adoption within agrivoltaic installations reached approximately 42% of new capacity additions in 2025, driven by superior energy yield performance under partially shaded crop-canopy conditions. AI-driven crop monitoring platforms integrated with solar management software represent the next frontier, enabling adaptive energy-agriculture management at the field level.

Regional investment hotspots in the agrivoltaics market include Asia Pacific, which commands 38.2% of global market revenue in 2025, driven by Japan's long-standing solar sharing framework and China's state-directed expansion of agricultural solar capacity. Europe follows with 28.5% share, anchored by Germany's APV program and France's robust agrivoltaic tender system. North America is emerging as the fastest-growing regional market through 2034 as utility-scale agrivoltaic project pipelines materialize across the Midwest, Southwest, and Southeast. Supply chain constraints related to tracker manufacturing and specialized mounting hardware remain near-term headwinds, though capacity expansion by leading hardware producers is expected to ease these pressures by 2027.

, By Application (Crop Cultivation, Animal Grazing, Aquaculture, Research Projects), By Technology (Bifacial Panels, Thin-Film Modules, Monocrystalline, Concentrated PV), By Installation Scale, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global agrivoltaics market reached USD 9.14 Billion in 2025 and is forecast to reach USD 28.60 Billion by 2034, at a CAGR of 13.5% during 2026–2034.

- Segment Dominance: Fixed-Tilt Agrivoltaic Systems held the largest share by system type at 47.3% of total market revenue in 2025, favored for lower capital costs and simpler integration with row-crop cultivation.

- Segment Dominance: The crop cultivation application segment commanded 54.8% of agrivoltaics market demand in 2025, underpinned by grain, vegetable, and specialty crop suitability across European and Asian installations.

- Driver: Accelerating renewable energy policy mandates and dual land-use incentives are the primary growth driver; EU member states committed over EUR 4.2 Billion in agrivoltaic-specific subsidies and tender allocations by end-2024.

- Restraint: High upfront capital expenditure per hectare, averaging USD 680,000–USD 1.1 Million per MW for integrated agrivoltaic structures, limits smallholder farmer adoption and constrains market penetration in low-income agricultural economies.

- Opportunity: Emerging markets in Sub-Saharan Africa and Southeast Asia present a combined addressable agrivoltaic deployment opportunity exceeding USD 3.8 Billion through 2034, driven by energy access gaps and agricultural modernization funding from multilateral development banks.

- Trend: Dynamic tracking and AI-integrated crop-energy management systems are the dominant technological trend, with adoption in new agrivoltaic installations rising from 12% in 2022 to approximately 31% in 2025.

- Regional Analysis: Asia Pacific led the agrivoltaics market in 2025 with a 38.2% share, equivalent to USD 3.49 Billion, driven by Japan's solar sharing framework, China's state-sponsored expansion, and South Korea's institutional agrivoltaic procurement programs.

Competitive Landscape Overview

The global agrivoltaics market is moderately fragmented in 2025, with the top four players — Enel Green Power, BayWa r.e., Ciel & Terre, and Sun'Agri — collectively accounting for approximately 31% of total market revenue. Competition is primarily technology-driven and project-development-oriented, with differentiation centered on system design capability, crop-yield optimization expertise, and project financing access. M&A activity intensified through 2024–2025, as utility-scale energy developers moved to acquire agrivoltaic EPC specialists and tracker manufacturers. New entrants from the precision agriculture and agricultural technology sector are introducing AI-enabled monitoring platforms that are reshaping competitive value propositions beyond hardware differentiation.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Enel Green Power | Italy | Leader | AgriSolar Integrated System | Europe, Latin America | Jan 2025 – Commissioned 150 MW agrivoltaic project in Sicily integrating viticulture with bifacial panel arrays. |

| BayWa r.e. | Germany | Leader | APV-System (Agrophotovoltaik) | Europe, Asia Pacific | Mar 2025 – Expanded APV pilot to 500 ha across Germany and Japan with crop-yield monitoring integration. |

| Ciel & Terre | France | Leader | Hydrelio Agri Float Platform | Asia Pacific, Europe | Nov 2024 – Signed 200 MW agrivoltaic EPC contract across South Korea rice paddies. |

| Sun'Agri | France | Leader | Dynamic Agrivoltaic Tracker | Europe | Feb 2025 – Raised EUR 30M Series C to commercialize AI-driven crop-shade optimization across vineyards. |

| Fraunhofer ISE | Germany | Niche Player | APV Research Platform | Europe | Jun 2025 – Published landmark dual-use yield efficiency study confirming 60% land productivity increase. |

| Cypress Creek Renewables | USA | Challenger | Pollinator-Friendly Solar Farm | North America | Apr 2025 – Closed 320 MW agrivoltaic pipeline deal with USDA partnership for Midwest grazing integration. |

| Lightsource bp | UK | Challenger | Integrated Agri-Solar Platform | North America, Europe | Sep 2025 – Acquired 110 MW agrivoltaic project portfolio in Australia expanding beyond two continents. |

| Insolight | Switzerland | Niche Player | Insolight Agrivoltaic Panel | Europe | Dec 2024 – Achieved commercial scale deployment of high-concentration agrivoltaic panels for greenhouse horticulture. |

By System Type

The agrivoltaics market segmentation by system type reveals that Fixed-Tilt Agrivoltaic Systems retained the dominant position with a 47.3% revenue share in 2025, equivalent to USD 4.32 Billion. Fixed systems benefit from lower structural costs and easier integration with broadacre and row-crop farming operations that do not require customized light management. These systems are particularly prevalent across Midwest US grain farms, European cereal cultivation zones, and Indian semi-arid agricultural belts, where consistent solar irradiance profiles make static orientations economically optimal. Competition in this sub-segment centers on mounting structure durability, soiling resistance, and compatibility with standard agricultural machinery operating clearances.

Tracking and Dynamic Agrivoltaic Systems represented 28.4% of agrivoltaics market revenue in 2025, valued at approximately USD 2.60 Billion. Dynamic systems equipped with single-axis or dual-axis trackers capable of real-time tilt adjustment based on crop light saturation algorithms are gaining traction in high-value crop cultivation contexts including viticulture, berry farming, and protected horticulture. Sun'Agri's dynamic tracker deployment in French and Spanish vineyards demonstrated 12% yield improvement alongside 35% energy generation uplift versus static installations, creating a compelling dual-value proposition for premium agricultural operators. Capital cost premiums of 25–40% over fixed systems limit broader adoption, but ongoing tracker price compression is improving project economics.

Floating Agrivoltaic Systems captured approximately 13.8% of the agrivoltaics market in 2025, valued at USD 1.26 Billion, with deployment concentrated in South Korean rice paddies, Japanese reservoirs, and Dutch inland waterways. Floating systems avoid terrestrial land-use trade-offs entirely by co-locating panels with aquaculture or rice cultivation on water surfaces. Ciel & Terre's Hydrelio platform is the category-defining product globally. Greenhouse Agrivoltaic Systems accounted for the remaining 10.5% of market revenue in 2025, with specialty crop production in controlled-environment horticulture driving adoption of semi-transparent and wavelength-selective photovoltaic glazing materials.

By Application

Crop cultivation represents the largest application segment in the agrivoltaics market, holding a 54.8% share in 2025 at USD 5.01 Billion. This dominance reflects the broad applicability of shading systems across vegetables, small grains, legumes, and specialty crops where partial shading reduces heat stress and water evaporation. Trade data and supply-chain evaluation confirm that agrivoltaic crop installations in water-stressed regions of Spain, India, and Morocco reduced irrigation requirements by 18–29%, significantly improving the economic viability of dual-use systems in arid zones.

Animal husbandry and grazing applications held a 22.6% share of the agrivoltaics market in 2025, valued at USD 2.06 Billion. Sheep grazing beneath solar arrays has emerged as the most cost-effective agrivoltaic model in the United States and Australia, with grazed sites reducing vegetation management costs by USD 2,000–USD 5,000 per MW annually. Aquaculture co-located with floating photovoltaic arrays represented 12.3% of the market in 2025, particularly in Asian rice-fish farming systems. Research and pilot project installations accounted for the remaining 10.3%, with academic institutions and national energy agencies funding structured dual-use trials across 34 countries as of 2025.

By Installation Scale

Utility-scale agrivoltaic installations exceeding 1 MW per site commanded 58.4% of the global market in 2025 at USD 5.34 Billion. The economics of utility-scale systems benefit from procurement leverage, grid interconnection priority, and access to project finance at competitive debt margins. Commercial-scale installations between 100 kW and 1 MW held 27.1% share, serving mid-sized agricultural enterprises and cooperative farming structures particularly in Europe. Small-scale installations below 100 kW represented 14.5% of the agrivoltaics market in 2025, supported by government subsidy programs targeting smallholder farmers in Japan, India, and France.

Regional Analysis

Asia Pacific

The Asia Pacific agrivoltaics market generated USD 3.49 Billion in revenue in 2025, representing a 38.2% global share and the world's most mature and policy-supported regional market. Japan pioneered the solar sharing concept through its 2013 agricultural land law amendment, and by 2025 accumulated over 3,200 registered solar sharing sites. China's state energy administration has designated agrivoltaic systems as a strategic component of its rural revitalization and clean energy access programs, committing CNY 18 Billion in dedicated financing facilities through 2030. South Korea's Ministry of Agriculture has institutionalized procurement of floating agrivoltaic capacity through national infrastructure funds. India represents the fastest-growing national market in the region, with the Ministry of New and Renewable Energy supporting agrivoltaic integration in PM-KUSUM solar pump programs across semi-arid states. Australia is emerging as a significant grazing agrivoltaic market driven by pastoral sector participation in renewable energy certificate programs.

Europe

Europe held 28.5% of the agrivoltaics market in 2025, generating USD 2.60 Billion in total revenue. Germany leads the European segment, with the Fraunhofer ISE-developed APV standard providing regulatory clarity for project permitting and grid connection across all sixteen federal states. France implemented its dedicated agrivoltaic law in 2023 providing legal definitions and priority permitting pathways, driving an estimated 420 MW of installed agrivoltaic capacity by end-2024. Italy's AGRI-PV incentive scheme under the national energy transition plan has catalyzed project development across southern agricultural regions. The United Kingdom's post-Brexit land-use strategy explicitly recognizes dual-use solar as compatible with productive agricultural designation, opening access to agricultural transition fund incentives for qualified agrivoltaic operators. Regulatory harmonization under the EU Solar Rooftop Initiative and revised Renewable Energy Directive III is expected to further accelerate European capacity deployment through 2034.

North America

The North American agrivoltaics market accounted for USD 1.87 Billion in 2025 at a 20.5% global share, with growth driven primarily by the United States. Federal support through USDA's Partnerships for Climate-Smart Commodities program and the DOE Solar Energy Technologies Office's InSPIRE initiative has co-funded over 60 agrivoltaic research and demonstration sites across 22 states. The Inflation Reduction Act's expanded investment tax credit provisions applicable to dual-use solar installations have materially improved project IRRs, triggering a pipeline acceleration that current market assessment shows exceeding 4.5 GW of planned agrivoltaic capacity in development as of mid-2025. Canada is developing provincial agrivoltaic frameworks in Ontario and British Columbia with agricultural land commission participation. Mexico's smallholder agricultural sector presents a nascent but expanding opportunity linked to NAFTA-successor trade framework energy agriculture provisions.

Latin America

Latin America contributed USD 0.64 Billion to the global agrivoltaics market in 2025, representing a 7.0% share. Brazil is the regional leader, with ANEEL's net-metering reform enabling agricultural landowners to monetize agrivoltaic generation through rural cooperative energy credit mechanisms. Chile's high solar irradiance combined with water-stressed agricultural zones in the Atacama and Coquimbo regions creates a compelling economic case for dual-use systems that optimize both energy production and crop evapotranspiration reduction. Argentina and Colombia are at early-stage regulatory development, with multilateral development bank technical assistance programs building regulatory capacity. Supply chain constraints and project finance access remain near-term barriers, though falling panel costs and increasing regional EPC capability are improving the investment case for Latin American agrivoltaic development through 2034.

Middle East & Africa

The Middle East and Africa region represented 5.8% of the agrivoltaics market in 2025 at USD 0.53 Billion. The UAE's Abu Dhabi Future Energy Company and Saudi Arabia's Vision 2030 agricultural technology program have both identified agrivoltaics as aligned with national food-water-energy nexus strategies. Pilot installations in Morocco's Souss-Massa agricultural region co-funded by the Green Climate Fund demonstrated 24% reduction in water demand and concurrent energy generation equivalent to 40% of farm operational requirements. Sub-Saharan Africa presents the largest long-term addressable opportunity in this region, particularly in Kenya, Nigeria, and Ethiopia where agricultural electrification deficits and food security imperatives align with agrivoltaic dual-use value propositions. Capacity development programs supported by the African Development Bank are building local project development expertise that will be critical to scaling the MEA agrivoltaics market through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By System Type

- Fixed-Tilt Agrivoltaic Systems

- Tracking/Dynamic Agrivoltaic Systems

- Floating Agrivoltaic Systems

- Greenhouse Agrivoltaic Systems

By Application

- Crop Cultivation

- Animal Husbandry & Grazing

- Aquaculture

- Research & Pilot Projects

By Installation Scale

- Utility-Scale (>1 MW)

- Commercial-Scale (100 kW–1 MW)

- Small-Scale (<100 kW)

By Technology

- Bifacial Solar Panels

- Thin-Film Modules

- High-Efficiency Monocrystalline

- Concentrated PV

By End-Use Industry

- Agriculture

- Energy Utilities

- Government & Public Sector

- Corporate & Industrial

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 9.14 B |

| Forecast Revenue (2034) | USD 28.60 B |

| CAGR (2025-2034) | 13.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By System Type, (Fixed-Tilt Agrivoltaic Systems; Tracking/Dynamic Agrivoltaic Systems; Floating Agrivoltaic Systems; Greenhouse Agrivoltaic Systems), By Application, (Crop Cultivation; Animal Husbandry & Grazing; Aquaculture; Research & Pilot Projects), By Installation Scale, (Utility-Scale (>1 MW); Commercial-Scale (100 kW–1 MW); Small-Scale (<100 kW)), By Technology, (Bifacial Solar Panels; Thin-Film Modules; High-Efficiency Monocrystalline; Concentrated PV), By End-Use Industry, (Agriculture; Energy Utilities; Government & Public Sector; Corporate & Industrial) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ENEL GREEN POWER, CIEL & TERRE, CYPRESS CREEK RENEWABLES, INSOLIGHT, NEXTRACKER, AGRI-PV TECH, SONNEDIX, ENERPARC, BAYWA R.E., SUN'AGRI, LIGHTSOURCE BP, FRAUNHOFER ISE, IDEEMATEC, TESLA ENERGY, BELECTRIC, JUWI AG, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Crop Cultivation, Animal Grazing, Aquaculture, Research Projects), By Technology (Bifacial Panels, Thin-Film Modules, Monocrystalline, Concentrated PV), By Installation Scale, Industry Trends & Forecast 2026-2034")

, By Application (Crop Cultivation, Animal Grazing, Aquaculture, Research Projects), By Technology (Bifacial Panels, Thin-Film Modules, Monocrystalline, Concentrated PV), By Installation Scale, Industry Trends & Forecast 2026-2034")

, By Application (Crop Cultivation, Animal Grazing, Aquaculture, Research Projects), By Technology (Bifacial Panels, Thin-Film Modules, Monocrystalline, Concentrated PV), By Installation Scale, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Agrivoltaics Market?

The Global Agrivoltaics Market was valued at USD 8.05 Billion in 2024 and is projected to reach USD 28.60 Billion by 2034, growing at a CAGR of 13.5% from 2026 to 2034, driven by rising adoption of dual land-use farming systems, increasing investments in renewable energy infrastructure, advancements in bifacial solar panel technologies, and growing focus on sustainable agriculture, water conservation, and climate-resilient farming practices worldwide.

Who are the major players in the Agrivoltaics Market?

ENEL GREEN POWER, CIEL & TERRE, CYPRESS CREEK RENEWABLES, INSOLIGHT, NEXTRACKER, AGRI-PV TECH, SONNEDIX, ENERPARC, BAYWA R.E., SUN'AGRI, LIGHTSOURCE BP, FRAUNHOFER ISE, IDEEMATEC, TESLA ENERGY, BELECTRIC, JUWI AG, Others

Which segments covered the Agrivoltaics Market?

By System Type, (Fixed-Tilt Agrivoltaic Systems; Tracking/Dynamic Agrivoltaic Systems; Floating Agrivoltaic Systems; Greenhouse Agrivoltaic Systems), By Application, (Crop Cultivation; Animal Husbandry & Grazing; Aquaculture; Research & Pilot Projects), By Installation Scale, (Utility-Scale (>1 MW); Commercial-Scale (100 kW–1 MW); Small-Scale (<100 kW)), By Technology, (Bifacial Solar Panels; Thin-Film Modules; High-Efficiency Monocrystalline; Concentrated PV), By End-Use Industry, (Agriculture; Energy Utilities; Government & Public Sector; Corporate & Industrial)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date