- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI Agent Orchestration Software Market Forecast | CAGR 18.8%

Global AI Agent Orchestration Software Market Size, Share, Growth & Industry Analysis By Offering (Platform/Software, Services Including Consulting, Integration & Managed Services), By Deployment (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Vertical (BFSI, Technology & Telecom, Healthcare & Life Sciences, Retail & E-Commerce, Government & Defense, Manufacturing, Others) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 5.6 Billion | USD 26.3 Billion | 18.8% | North America, 44.2% |

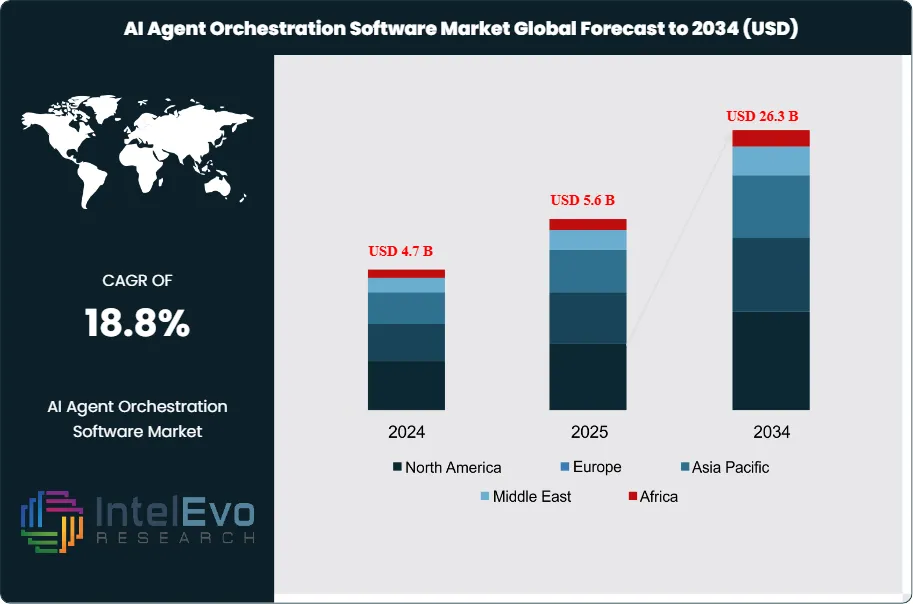

The AI Agent Orchestration Software Market was valued at approximately USD 4.7 Billion in 2024 and reached USD 5.6 Billion in 2025. The market is projected to grow to USD 26.3 Billion by 2034, expanding at a CAGR of 18.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 20.7 Billion over the analysis period. AI agent orchestration software enables enterprises to design, deploy, coordinate, and monitor autonomous AI agents that execute complex, multi-step workflows across business functions. The market’s rapid expansion reflects the convergence of generative AI capabilities, enterprise automation demand, and a shift from single-model inference toward multi-agent systems that can reason, collaborate, and act.

Get More Information about this report -

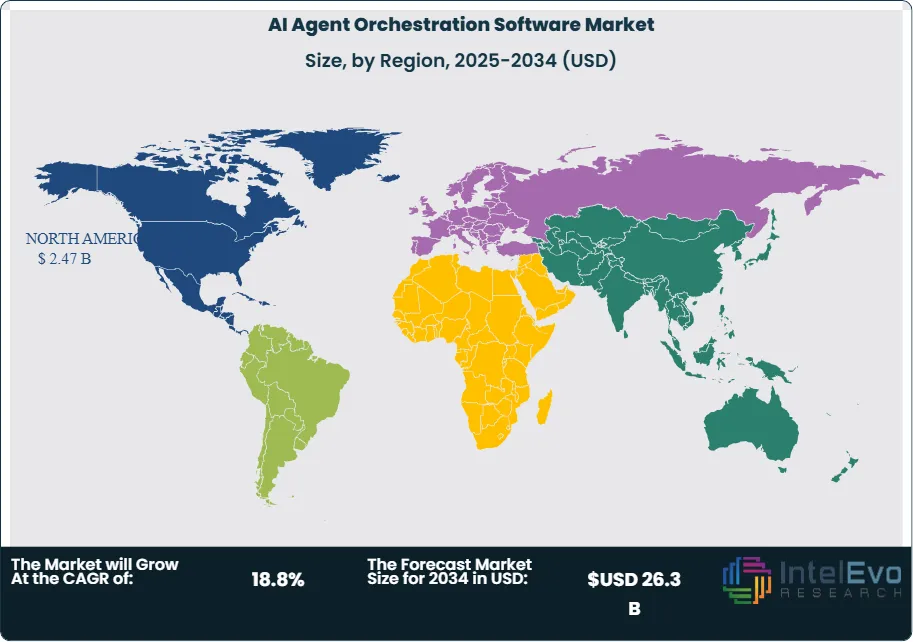

Request Free Sample ReportNorth America accounted for 44.2% of total revenue in 2025, valued at approximately USD 2.47 Billion. Enterprises across finance, healthcare, retail, and technology are deploying agent frameworks to automate customer service, software development, supply chain coordination, and data analysis tasks. The U.S. dominates spending, driven by hyperscaler platform investments from Microsoft, Google, and Amazon Web Services. Europe held 24.6% market share in 2025, with Germany and the United Kingdom leading adoption within regulated industries such as banking and insurance. The EU AI Act, which imposes compliance requirements on high-risk AI systems, has accelerated demand for orchestration platforms with built-in governance, audit trails, and explainability modules.

Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 22.1% through 2034. China, Japan, India, and South Korea are investing heavily in AI infrastructure and national AI strategies. Japan’s manufacturing sector, for instance, is piloting multi-agent systems for predictive maintenance and quality control. India’s IT services industry is embedding orchestration layers into client-facing automation solutions. Cloud-native deployment accounted for 68.3% of total installations in 2025, reflecting enterprise preference for elastic scalability and rapid iteration. On-premise and hybrid configurations served approximately 31.7%, concentrated in defense, government, and banking sectors with strict data sovereignty mandates. Technology advances including retrieval-augmented generation, function-calling LLMs, and tool-use protocols have reduced agent hallucination rates and improved task completion accuracy. The NIST AI Risk Management Framework and ISO/IEC 42001 are emerging as compliance benchmarks for enterprise AI deployments. Venture capital investment in agentic AI startups exceeded USD 4.8 Billion globally in 2025, signaling strong investor confidence in the market’s growth trajectory.

, By Deployment (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Vertical (BFSI, Technology & Telecom, Healthcare & Life Sciences, Retail & E-Commerce, Government & Defense, Manufacturing, Others) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The AI agent orchestration software market was valued at USD 5.6 Billion in 2025 and is projected to reach USD 26.3 Billion by 2034, expanding at a CAGR of 18.8% over the 2025–2034 forecast period.

- Segment Dominance (By Offering): The platform/software segment commanded 62.4% of total market revenue in 2025, as enterprises prioritized turnkey orchestration solutions with pre-built agent templates and low-code interfaces.

- Segment Dominance (By Vertical): Banking, financial services, and insurance (BFSI) represented the largest vertical at 22.8% share in 2025, driven by regulatory compliance automation and fraud detection agent deployments.

- Driver: Enterprise demand for autonomous workflow automation contributed an estimated USD 1.9 Billion in incremental revenue in 2025, reducing average process cycle times by 35–45%.

- Restraint: Data privacy concerns and regulatory fragmentation across jurisdictions limited adoption among 28% of surveyed enterprises in 2025, adding 4–6 months to procurement timelines.

- Opportunity: Small and medium enterprises represent a USD 7.2 Billion addressable market by 2034, enabled by usage-based pricing models and managed orchestration services.

- Trend: Multi-agent collaboration frameworks, where specialized agents negotiate and delegate sub-tasks, reached 38.5% adoption among enterprise AI teams in 2025, up from 12% in 2023.

- Regional Analysis: North America led with 44.2% market share and USD 2.47 Billion in revenue in 2025, anchored by hyperscaler investments and early enterprise adoption across the United States and Canada.

Competitive Landscape Overview

The AI agent orchestration software market is moderately consolidated, with the top four players (Microsoft, Amazon Web Services, Google Cloud, and LangChain) collectively holding approximately 48% of global revenue in 2025. Competition is primarily technology-driven, centered on framework flexibility, model-agnosticism, and enterprise governance features. The period from late 2024 through early 2026 saw intense M&A activity, with at least 14 acquisitions targeting agent framework startups. Open-source entrants such as CrewAI and AutoGen are pressuring incumbents on pricing while enterprise-grade vendors differentiate through compliance tooling, SLA guarantees, and pre-built industry-specific agent workflows.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Microsoft | US | Leader | Azure AI Agent Service | North America | Launched Copilot Studio agent builder (Feb 2025) |

| LangChain (LangSmith) | US | Leader | LangGraph Platform | North America | Raised USD 30M Series A; launched LangGraph Cloud (Jan 2025) |

| CrewAI | US | Challenger | CrewAI Enterprise | North America | Secured USD 18M seed round (Mar 2025) |

| Amazon Web Services | US | Leader | Amazon Bedrock Agents | Global | Added multi-agent orchestration to Bedrock (Dec 2024) |

| Google Cloud | US | Leader | Vertex AI Agent Builder | Global | Launched Agent Space in Google Cloud (Jan 2026) |

| IBM | US | Challenger | watsonx Orchestrate | North America, Europe | Integrated watsonx agents with SAP S/4HANA (Sep 2025) |

| Salesforce | US | Challenger | Agentforce Platform | North America | Shipped Agentforce 2.0 with multi-agent support (Feb 2025) |

| AutoGen (Microsoft Research) | US | Niche Player | AutoGen Framework | Global | Released AutoGen v0.4 with event-driven agents (Jun 2025) |

| UiPath | US | Challenger | UiPath Autopilot Agents | Europe, North America | Acquired AI orchestration startup ReAct Labs (Apr 2025) |

| Oracle | US | Challenger | OCI AI Agents | North America | Embedded AI agents across Fusion Cloud suite (Oct 2025) |

By Offering

The platform/software segment captured 62.4% of market revenue in 2025, valued at approximately USD 3.49 Billion. Enterprise buyers prefer integrated platforms that provide visual workflow builders, agent lifecycle management, memory and context persistence, and monitoring dashboards. Microsoft Azure AI Agent Service, Google Vertex AI Agent Builder, and Amazon Bedrock Agents anchor this category, each offering native integration with their respective cloud infrastructure. LangChain’s LangGraph and CrewAI represent open-source-rooted alternatives that appeal to developer-first organizations. The platform segment is growing at 19.4% CAGR as vendors expand template libraries and pre-configured industry agents that reduce deployment time from weeks to days.

The services segment held 37.6% share in 2025, valued at USD 2.11 Billion. This includes implementation consulting, system integration, custom agent development, and managed orchestration services. Global IT consultancies such as Accenture, Deloitte, and Wipro have established dedicated agentic AI practices. Demand is strongest in BFSI, healthcare, and government sectors where workflow complexity requires domain-specific agent configuration. Managed services are gaining traction among mid-market firms that lack in-house AI engineering capacity. The services segment is expected to grow at 17.8% CAGR through 2034.

By Deployment

Cloud deployment dominated with 68.3% market share in 2025, generating USD 3.82 Billion. The elastic compute requirements of multi-agent systems, combined with the need for frequent model updates and real-time scaling, make cloud infrastructure the natural fit. Vendors offer both multi-tenant SaaS and single-tenant virtual private cloud options. Adoption is highest in technology, retail, and media verticals where data sensitivity is moderate and speed-to-deployment is critical. Cloud-based orchestration platforms typically reduce initial deployment costs by 40–55% compared with on-premise alternatives.

On-premise and hybrid models accounted for 31.7% of the market in 2025, valued at USD 1.78 Billion. Defense agencies, central banks, and healthcare systems with strict data residency requirements drive this segment. Hybrid architectures, where the orchestration control plane runs on-premise while agents access cloud-hosted LLMs through secure API gateways, are growing rapidly at an estimated 21.3% CAGR. This configuration addresses both performance and compliance objectives.

By Enterprise Size

Large enterprises represented 71.5% of market revenue in 2025, equaling approximately USD 4.0 Billion. These organizations deploy agent orchestration across multiple departments, integrating with ERP, CRM, ITSM, and data warehouse systems. Budget allocation for agentic AI within Fortune 500 IT spending rose from 3.2% in 2024 to 8.7% in 2025. Large enterprises prioritize platforms with role-based access control, audit logging, and enterprise-grade SLAs.

Small and medium enterprises held 28.5% share in 2025, valued at USD 1.6 Billion. SME adoption is accelerating as vendors introduce consumption-based pricing, pre-packaged agent bundles, and low-code interfaces. Salesforce Agentforce and HubSpot AI agent features specifically target the mid-market segment. The SME segment is projected to grow at 21.9% CAGR through 2034, outpacing the large enterprise segment.

By Vertical

BFSI led all verticals with 22.8% share in 2025, valued at USD 1.28 Billion. Agent orchestration platforms automate loan processing, regulatory reporting, fraud detection, and customer onboarding. JPMorgan Chase, Goldman Sachs, and HSBC have deployed multi-agent systems for trade surveillance and compliance workflows. Technology and telecom followed at 19.5% share (USD 1.09 Billion), driven by internal DevOps automation, code review agents, and IT incident resolution bots. Healthcare and life sciences accounted for 14.2% (USD 0.80 Billion), with agent systems supporting clinical trial management, prior authorization, and medical records summarization. Retail and e-commerce held 13.1% (USD 0.73 Billion), deploying agents for personalized merchandising, dynamic pricing, and supply chain coordination. Government and defense represented 10.8% (USD 0.60 Billion), manufacturing contributed 9.9% (USD 0.55 Billion), and other verticals composed the remaining 9.7%.

Regional Analysis

North America AI Agent Orchestration Software Market

North America commanded 44.2% of the global AI agent orchestration software market in 2025, generating USD 2.47 Billion. The United States alone accounted for approximately 86% of regional revenue, driven by the concentration of hyperscaler platforms, a mature venture capital infrastructure, and aggressive enterprise adoption timelines. Microsoft, Google, Amazon, Salesforce, and a dense cluster of AI-native startups including LangChain, CrewAI, and Fixie are headquartered in the U.S. Canada contributed USD 0.24 Billion, with financial institutions in Toronto and Montreal emerging as early adopters of agentic AI for wealth management and compliance. Mexico’s share remained nascent at approximately USD 0.11 Billion, concentrated in nearshore BPO operations deploying customer service agents. The NIST AI Risk Management Framework serves as a de facto governance standard for U.S. enterprises.

Europe AI Agent Orchestration Software Market

Europe held 24.6% of the market in 2025, valued at USD 1.38 Billion. Germany led the region at USD 0.39 Billion, with automotive and industrial manufacturers integrating agent orchestration into production planning and supply chain logistics. The United Kingdom generated USD 0.34 Billion, anchored by London’s financial services sector deploying compliance and risk management agents. France contributed USD 0.22 Billion, with strong government-backed AI investment programs. The EU AI Act, effective from August 2025, has created a distinct compliance-driven market segment. Vendors offering built-in risk classification, transparency logging, and human-in-the-loop controls gained 15–20% pricing premiums in regulated European industries.

Asia Pacific AI Agent Orchestration Software Market

Asia Pacific accounted for 21.4% of the market in 2025, with revenue of USD 1.20 Billion, and is projected to be the fastest-growing region at 22.1% CAGR through 2034. China represented the largest national market at USD 0.44 Billion, with Alibaba Cloud, Baidu, and Tencent all launching agent orchestration services. Japan generated USD 0.28 Billion, with manufacturing and logistics firms deploying multi-agent coordination for factory automation. India contributed USD 0.24 Billion, propelled by IT services companies building orchestration capabilities into their client delivery models. South Korea added USD 0.14 Billion, with Samsung and LG investing in industrial agentic AI. National AI strategies across the region, including Japan’s Society 5.0 and India’s IndiaAI mission, are channeling billions into foundational AI infrastructure.

Latin America AI Agent Orchestration Software Market

Latin America represented 5.6% of the global market in 2025, valued at USD 0.31 Billion. Brazil led the region at USD 0.14 Billion, with banks and fintechs adopting agent systems for credit decisioning and customer service automation. Mexico contributed USD 0.09 Billion, primarily through contact center modernization and nearshore IT services. Colombia and Chile together added approximately USD 0.05 Billion. Cloud-first deployment patterns dominate the region due to limited on-premise AI infrastructure. Growth is expected at 20.4% CAGR through 2034 as digital transformation programs accelerate across government and financial services.

Middle East and Africa AI Agent Orchestration Software Market

The Middle East and Africa held 4.2% of the global AI agent orchestration software market in 2025, generating USD 0.24 Billion. The UAE led at USD 0.09 Billion, with Dubai’s AI strategy and Abu Dhabi’s Technology Innovation Institute driving public and private sector adoption. Saudi Arabia contributed USD 0.08 Billion, aligned with Vision 2030 technology investments and NEOM smart city development. South Africa generated USD 0.04 Billion, concentrated in banking and mining automation. Government-led digital transformation, sovereign wealth fund investments in AI, and a young demographic profile position the region for 21.8% CAGR growth through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Platform/Software

- Services (Consulting, Integration, Managed Services)

By Deployment

- Cloud

- On-Premise

- Hybrid

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

By Vertical

- BFSI

- Technology and Telecom

- Healthcare and Life Sciences

- Retail and E-Commerce

- Government and Defense

- Manufacturing

- Others

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.6 B |

| Forecast Revenue (2034) | USD 26.3 B |

| CAGR (2025-2034) | 18.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Platform/Software, Services (Consulting, Integration, Managed Services)), By Deployment, (Cloud, On-Premise, Hybrid), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises (SMEs)), By Vertical, (BFSI, Technology and Telecom, Healthcare and Life Sciences, Retail and E-Commerce, Government and Defense, Manufacturing, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT, AMAZON WEB SERVICES (AWS), GOOGLE CLOUD, LANGCHAIN, SALESFORCE, IBM, CREWAI, UIPATH, ORACLE, SAP, AUTOGEN (MICROSOFT RESEARCH), ACCENTURE, PALANTIR TECHNOLOGIES, DATAROBOT, C3.AI, SERVICENOW, SNOWFLAKE, DATABRICKS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Vertical (BFSI, Technology & Telecom, Healthcare & Life Sciences, Retail & E-Commerce, Government & Defense, Manufacturing, Others) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Deployment (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Vertical (BFSI, Technology & Telecom, Healthcare & Life Sciences, Retail & E-Commerce, Government & Defense, Manufacturing, Others) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Deployment (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, Small & Medium Enterprises), By Vertical (BFSI, Technology & Telecom, Healthcare & Life Sciences, Retail & E-Commerce, Government & Defense, Manufacturing, Others) Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI Agent Orchestration Software Market?

Global AI agent orchestration software market valued at USD 4.7B in 2024, reaching USD 26.3B by 2034, growing at a CAGR of 18.8% from 2026–2034.

Who are the major players in the AI Agent Orchestration Software Market?

MICROSOFT, AMAZON WEB SERVICES (AWS), GOOGLE CLOUD, LANGCHAIN, SALESFORCE, IBM, CREWAI, UIPATH, ORACLE, SAP, AUTOGEN (MICROSOFT RESEARCH), ACCENTURE, PALANTIR TECHNOLOGIES, DATAROBOT, C3.AI, SERVICENOW, SNOWFLAKE, DATABRICKS, Others

Which segments covered the AI Agent Orchestration Software Market?

By Offering, (Platform/Software, Services (Consulting, Integration, Managed Services)), By Deployment, (Cloud, On-Premise, Hybrid), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises (SMEs)), By Vertical, (BFSI, Technology and Telecom, Healthcare and Life Sciences, Retail and E-Commerce, Government and Defense, Manufacturing, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI Agent Orchestration Software Market

Published Date : 27 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date