- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI Copilot Software Market Size & Forecast 2034 | CAGR 20.4%

Global AI Copilot Software Market Size, Share, Growth & Industry Analysis By Offering (Platform-Embedded Copilots, Standalone Copilot Applications, Copilot-as-a-Service API/SDK), By Application (Developer & Code Copilots, Productivity & Office Copilots, Customer Service & CRM Copilots, IT Operations & Security Copilots, Industry-Specific Copilots), By Deployment (Cloud-Based, Hybrid, On-Premise), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

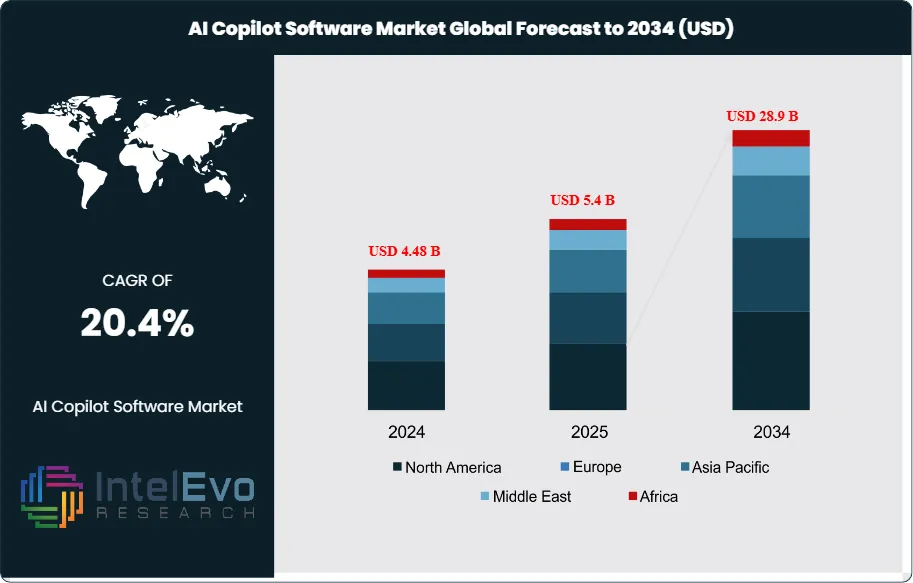

| USD 5.4 Billion | USD 28.9 Billion | 20.4% | North America, 44.5% |

The AI Copilot Software Market was valued at approximately USD 4.48 Billion in 2024 and reached USD 5.4 Billion in 2025. The market is projected to grow to USD 28.9 Billion by 2034, expanding at a CAGR of 20.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 23.5 billion over the analysis period. AI copilot software refers to intelligent assistants embedded in enterprise applications, developer environments, productivity suites, customer service platforms, and vertical business tools that use large language models to augment human decision-making, automate repetitive tasks, generate content, and surface contextual recommendations in real time.

Get More Information about this report -

Request Free Sample ReportDemand for AI copilot software is surging as enterprises seek measurable productivity gains from generative AI investments. A 2025 survey by the NIST AI Safety Institute found that 63% of Fortune 500 companies had deployed at least one copilot product, up from 22% in 2023. Microsoft 365 Copilot alone reached 1.3 million paid enterprise seats by Q1 2025, generating an estimated USD 1.8 billion in annualized recurring revenue. GitHub Copilot surpassed 2.5 million paid subscribers across individual developers and enterprise accounts. The EU AI Act, which entered phased enforcement beginning August 2025, introduced transparency and documentation requirements for AI systems operating in workplace contexts, creating a compliance-driven demand tier for auditable, explainable copilot architectures.

Technology effects are accelerating market expansion. Transformer-based large language models with retrieval-augmented generation (RAG) enable copilots to access enterprise knowledge bases in real time, improving response accuracy by 35–45% over standalone LLM outputs. Multi-modal copilots that process text, images, code, and structured data grew from 15% of deployments in 2023 to 38% in 2025. Agentic AI capabilities, where copilots autonomously execute multi-step workflows rather than simply suggesting actions, are the fastest-growing product category, representing 18% of new enterprise licenses in 2025.

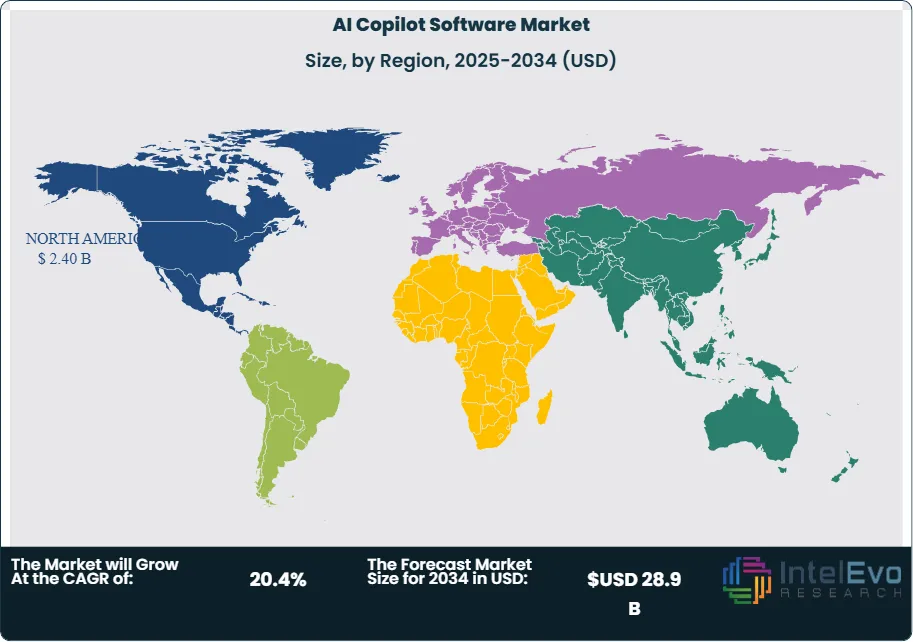

Regional investment patterns show North America leading with 44.5% share in 2025, driven by hyperscaler platform dominance and enterprise cloud maturity. Asia Pacific held 25.0%, powered by rapid enterprise AI adoption in China, India, and Japan. Europe accounted for 20.5%, shaped by AI Act compliance spending and sovereign AI infrastructure initiatives. Latin America contributed 5.5%, concentrated in Brazil's financial services sector. The Middle East and Africa held 4.5%, led by UAE government AI programs. Risk factors include enterprise data privacy concerns, model hallucination rates, vendor lock-in dynamics, and talent scarcity in prompt engineering and AI operations. The AI copilot software market outlook remains strong as every major software category integrates copilot functionality through 2034.

, By Application (Developer & Code Copilots, Productivity & Office Copilots, Customer Service & CRM Copilots, IT Operations & Security Copilots, Industry-Specific Copilots), By Deployment (Cloud-Based, Hybrid, On-Premise), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The AI copilot software market was valued at USD 5.4 billion in 2025 and is projected to reach USD 28.9 billion by 2034, registering a CAGR of 20.4% over the forecast period 2026–2034.

- Segment Dominance (By Offering): Platform-embedded copilots captured 56.0% of the market in 2025, valued at USD 3.02 billion, as major software vendors bundled AI assistants directly into existing enterprise applications and developer tools.

- Segment Dominance (By Application): Developer and code copilots accounted for 30.0% of market revenue in 2025, driven by GitHub Copilot's 2.5 million paid subscribers and growing adoption of code generation tools across enterprise engineering teams.

- Driver: Enterprise productivity gains drove adoption; organizations deploying AI copilots reported 28–40% reductions in task completion time across software development, content creation, and data analysis workflows in 2025.

- Restraint: Model hallucination and output reliability concerns limited deployment in regulated industries; 34% of enterprises reported pausing copilot rollouts pending accuracy improvements and explainability features.

- Opportunity: Vertical-specific copilots for healthcare, legal, and financial services represent a USD 6.8 billion incremental opportunity through 2034, as regulated industries demand domain-trained AI assistants with compliance safeguards.

- Trend: Agentic copilots capable of autonomous multi-step task execution grew to 18% of new enterprise licenses in 2025, up from 3% in 2023, signaling a shift from passive suggestion engines to active workflow automation.

- Regional Analysis: North America led with 44.5% market share, generating USD 2.40 billion in 2025; Microsoft, Google, and Salesforce platform dominance and concentrated enterprise cloud adoption anchored regional demand.

Competitive Landscape Overview

The AI copilot software market is highly consolidated, with the top four vendors collectively holding approximately 58% of global revenue in 2025. Competition is platform-driven, centering on LLM model quality, enterprise integration depth, data security guarantees, and vertical-specific customization. Hyperscaler platform companies dominate through bundled copilot offerings embedded in existing SaaS suites, creating strong switching cost barriers. Startup entrants compete on vertical specialization and pricing flexibility. Merger and acquisition activity surged through 2024–2025 as enterprise software companies acquired AI assistants to embed copilot capabilities into CRM, ERP, and ITSM platforms.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Microsoft | US | Leader | Microsoft 365 Copilot / GitHub Copilot | North America | Reached 1.3M paid enterprise Copilot seats (Q1 2025) |

| US | Leader | Gemini for Workspace / Duet AI | North America | Integrated Gemini copilot across all Workspace apps (Mar 2025) | |

| Salesforce | US | Leader | Einstein Copilot | North America | Launched Agentforce autonomous AI agents for CRM (Feb 2025) |

| GitHub (Microsoft) | US | Leader | GitHub Copilot Enterprise | Global | Surpassed 2.5M paid subscribers; added Copilot Workspace (Jan 2025) |

| Amazon Web Services | US | Challenger | Amazon Q / CodeWhisperer | Global | Released Amazon Q Business for enterprise knowledge (Apr 2025) |

| ServiceNow | US | Challenger | Now Assist | North America | Expanded Now Assist to IT, HR, and customer workflows (Jun 2025) |

| SAP SE | Germany | Challenger | SAP Joule | Europe | Embedded Joule copilot across all S/4HANA modules (Sep 2025) |

| Atlassian | Australia | Challenger | Atlassian Intelligence | Global | Launched AI assistant for Jira and Confluence (Dec 2024) |

| Cursor (Anysphere) | US | Niche Player | Cursor AI Code Editor | North America | Raised USD 900M Series C at USD 9B valuation (Jan 2026) |

| Jasper AI | US | Niche Player | Jasper Copilot for Marketing | North America | Expanded enterprise marketing copilot to 5,000+ clients (Aug 2025) |

By Offering:

Platform-embedded copilots dominated the market with a 56.0% share valued at USD 3.02 billion in 2025. These copilots ship as native features within established enterprise software suites; Microsoft 365 Copilot, Google Gemini for Workspace, Salesforce Einstein Copilot, and SAP Joule are the primary examples. Enterprises prefer embedded copilots because they require no separate procurement, integrate with existing identity and access management systems, and benefit from the vendor's native data layer. Microsoft's bundled pricing strategy, charging USD 30 per user per month for 365 Copilot, set the de facto market price anchor. Standalone copilot applications held 28.0% share, generating USD 1.51 billion in 2025. This segment includes purpose-built AI assistants such as GitHub Copilot, Cursor AI, and Jasper Copilot that operate as dedicated tools for specific workflow categories. Standalone copilots often deliver deeper functionality within their domain than embedded alternatives. Copilot-as-a-Service (API/SDK) captured 16.0%, valued at USD 0.86 billion. This segment provides enterprise developers with copilot building blocks; pre-trained models, prompt orchestration layers, and RAG frameworks; to construct custom AI assistants tailored to proprietary workflows.

By Application:

Developer and code copilots led with 30.0% market share, generating USD 1.62 billion in 2025. GitHub Copilot's 2.5 million paid subscribers anchor this segment, with Amazon CodeWhisperer, Cursor AI, and Tabnine as significant competitors. Enterprise developers using code copilots reported 40–55% faster code completion rates and 25% fewer production bugs in 2025 benchmarking studies. Productivity and office copilots held 26.5%, valued at USD 1.43 billion. Microsoft 365 Copilot and Google Gemini for Workspace dominate this segment, assisting with email drafting, document summarization, spreadsheet analysis, and meeting notes. Customer service and CRM copilots captured 18.0%, worth USD 0.97 billion, with Salesforce Einstein Copilot and Zendesk AI leading deployments for case resolution, knowledge retrieval, and sentiment analysis. IT operations and security copilots accounted for 13.5%, generating USD 0.73 billion, driven by ServiceNow Now Assist and Microsoft Security Copilot, which automate incident triage, threat analysis, and change management workflows. Industry-specific copilots held 12.0%, valued at USD 0.65 billion, covering healthcare clinical documentation (Nuance DAX Copilot), legal research, financial analysis, and manufacturing quality inspection assistants.

By Deployment:

Cloud-based deployment dominated with 74.0% share, valued at USD 4.00 billion in 2025. Cloud copilots benefit from continuous model updates, elastic GPU inference scaling, and lower upfront costs. Most enterprise copilot offerings from Microsoft, Google, and Salesforce operate exclusively in cloud environments. Hybrid deployment held 18.0%, generating USD 0.97 billion. Enterprises in regulated industries such as banking, healthcare, and government require hybrid architectures where sensitive data remains on-premise while copilot inference runs through private cloud endpoints. Hybrid adoption grew at 28% year-over-year in 2025 as privacy-conscious organizations expanded copilot usage. On-premise deployment captured 8.0%, valued at USD 0.43 billion. Defense contractors, intelligence agencies, and financial institutions with strict data sovereignty mandates deploy copilots on air-gapped infrastructure using locally hosted open-source models.

By Enterprise Size:

Large enterprises commanded 71.0% of market revenue in 2025, valued at USD 3.83 billion. Organizations with over 5,000 employees lead copilot adoption because they possess the IT infrastructure, data volumes, and change management resources to deploy copilots at scale. Fortune 500 copilot adoption reached 63% in 2025, with average annual spending per enterprise ranging from USD 2.5 million to USD 15 million depending on seat count and product mix. Small and medium enterprises (SMEs) held 29.0%, generating USD 1.57 billion. SME adoption accelerated in 2025 as cloud providers offered copilot access through existing subscription tiers, eliminating separate procurement cycles. Microsoft's inclusion of basic Copilot features in lower-tier Microsoft 365 Business plans broadened SME access. The SME segment grew at 26.3% year-over-year in 2025, outpacing the overall market rate.

Regional Analysis

North America:

North America led the AI copilot software market with 44.5% share, generating USD 2.40 billion in 2025. The United States accounted for over 92% of regional revenue, driven by the headquarters concentration of all four market leaders (Microsoft, Google, Salesforce, GitHub), the world's highest enterprise cloud penetration rate at 78%, and aggressive copilot adoption across technology, financial services, and healthcare verticals. Wall Street banks allocated an estimated USD 3.1 billion collectively to generative AI initiatives in 2025, with copilot licensing consuming 35–45% of those budgets. The NIST AI Risk Management Framework and Executive Order on AI Safety (October 2023) established documentation and testing standards that favor enterprise-grade copilot platforms with built-in compliance features. Canada contributed through its AI research hubs in Toronto and Montreal, with Cohere and other Canadian firms offering copilot building blocks. Mexico's growing IT services sector began integrating copilot tools into nearshore software development operations.

Europe:

Europe held 20.5% of the global market, valued at USD 1.11 billion in 2025. The EU AI Act classified many workplace AI copilots under transparency obligations for general-purpose AI systems, creating compliance spending that added 8–12% to copilot deployment budgets within the region. Germany led European demand through its manufacturing and automotive sectors, where SAP Joule and Siemens Industrial Copilot gained traction in production planning and engineering documentation. The United Kingdom maintained strong adoption through London's financial services cluster; FCA AI governance guidelines encouraged banks to deploy copilots with audit trail capabilities. France invested in sovereign copilot infrastructure, with Mistral AI providing domestically developed models for French government and defense copilot projects. The Netherlands emerged as a testing ground for multilingual copilot deployments serving pan-European enterprise clients. Overall, European copilot spending grew at 22.8% during 2025, slightly above the global average, driven by AI Act compliance preparation.

Asia Pacific:

Asia Pacific captured 25.0% market share, generating USD 1.35 billion in 2025. China represented the largest country-level market in the region, with Baidu Comate, Alibaba Tongyi Lingma, and ByteDance Doubao copilots serving enterprise clients across technology, e-commerce, and financial services. China's Cyberspace Administration regulations require all generative AI services to pass safety reviews, creating a distinct regulatory framework that favors domestically developed copilot solutions. Japan contributed through industrial AI copilots in manufacturing and logistics, with NEC and Fujitsu deploying Japanese-language workplace assistants. India's IT services sector, led by Infosys, TCS, and Wipro, built copilot integration practices serving global enterprise clients. South Korea's Samsung SDS and LG AI Research invested in copilots for semiconductor manufacturing and consumer electronics design. Australia allocated AUD 280 million for public sector AI modernization, including copilot deployments for healthcare and government services.

Latin America:

Latin America accounted for 5.5% of the global market, generating USD 0.30 billion in 2025. Brazil dominated regional demand, with Itau Unibanco, Nubank, and Banco Bradesco deploying customer service and internal productivity copilots across their operations. Mexico contributed through its expanding IT services and nearshore development sector, where developer copilots gained rapid adoption among software engineering teams. Argentina's technology community in Buenos Aires adopted code copilots at rates comparable to North American developers. Colombia invested in government digital transformation programs that included copilot pilots for public administration. Limited GPU inference infrastructure and reliance on US-hosted cloud services remain constraints; most Latin American enterprises run copilot workloads on AWS, Azure, or Google Cloud US regions, adding latency and data residency considerations.

Middle East and Africa:

The Middle East and Africa region held 4.5% market share, valued at USD 0.24 billion in 2025. The UAE led investment through its national AI strategy and partnerships with Microsoft and Google to deploy copilot solutions across government ministries and state-owned enterprises. Saudi Arabia's Vision 2030 program allocated AI spending across healthcare, education, and energy sectors, with SDAIA mandating Arabic-language copilot testing for public services. Israel contributed through its AI startup sector, with companies developing specialized copilots for cybersecurity operations and defense intelligence. South Africa represented the largest market in sub-Saharan Africa, with financial services and telecommunications firms piloting customer-facing copilot deployments. Hyperscaler data center expansions in Riyadh, Abu Dhabi, and Doha are expected to improve local copilot inference performance through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Platform-Embedded Copilots

- Standalone Copilot Applications

- Copilot-as-a-Service (API/SDK)

By Application

- Developer and Code Copilots

- Productivity and Office Copilots

- Customer Service and CRM Copilots

- IT Operations and Security Copilots

- Industry-Specific Copilots

By Deployment

- Cloud-Based

- Hybrid

- On-Premise

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.4 B |

| Forecast Revenue (2034) | USD 28.9 B |

| CAGR (2025-2034) | 20.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Platform-Embedded Copilots, Standalone Copilot Applications, Copilot-as-a-Service (API/SDK)), By Application, (Developer and Code Copilots, Productivity and Office Copilots, Customer Service and CRM Copilots, IT Operations and Security Copilots, Industry-Specific Copilots), By Deployment, (Cloud-Based, Hybrid, On-Premise), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises (SMEs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT, GOOGLE, SALESFORCE, GITHUB (MICROSOFT), AMAZON WEB SERVICES (AWS), SERVICENOW, SAP SE, ATLASSIAN, CURSOR (ANYSPHERE), JASPER AI, IBM (WATSONX), ANTHROPIC, OPENAI, NUANCE (MICROSOFT), ZOOM (AI COMPANION), DATABRICKS, TABNINE, REPLIT, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Developer & Code Copilots, Productivity & Office Copilots, Customer Service & CRM Copilots, IT Operations & Security Copilots, Industry-Specific Copilots), By Deployment (Cloud-Based, Hybrid, On-Premise), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

, By Application (Developer & Code Copilots, Productivity & Office Copilots, Customer Service & CRM Copilots, IT Operations & Security Copilots, Industry-Specific Copilots), By Deployment (Cloud-Based, Hybrid, On-Premise), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

, By Application (Developer & Code Copilots, Productivity & Office Copilots, Customer Service & CRM Copilots, IT Operations & Security Copilots, Industry-Specific Copilots), By Deployment (Cloud-Based, Hybrid, On-Premise), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI Copilot Software Market?

Global AI copilot software market valued at USD 4.48B in 2024, reaching USD 28.9B by 2034, growing at a CAGR of 20.4% from 2026–2034.

Who are the major players in the AI Copilot Software Market?

MICROSOFT, GOOGLE, SALESFORCE, GITHUB (MICROSOFT), AMAZON WEB SERVICES (AWS), SERVICENOW, SAP SE, ATLASSIAN, CURSOR (ANYSPHERE), JASPER AI, IBM (WATSONX), ANTHROPIC, OPENAI, NUANCE (MICROSOFT), ZOOM (AI COMPANION), DATABRICKS, TABNINE, REPLIT, Others

Which segments covered the AI Copilot Software Market?

By Offering, (Platform-Embedded Copilots, Standalone Copilot Applications, Copilot-as-a-Service (API/SDK)), By Application, (Developer and Code Copilots, Productivity and Office Copilots, Customer Service and CRM Copilots, IT Operations and Security Copilots, Industry-Specific Copilots), By Deployment, (Cloud-Based, Hybrid, On-Premise), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises (SMEs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date