- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI Data Labeling Market Size & Forecast 2034 | CAGR 24.4%

Global AI Data Labeling Market Size, Share, Growth & Industry Analysis By Service Type (Data Annotation Services, Annotation Platform-as-a-Service, Consulting & Integration Services), By Data Type (Image & Video, Text & NLP, Audio & Speech, LiDAR & Sensor Data, Others), By Annotation Technique (Manual, Semi-Automated, AI-Assisted), By End-Use Industry (Automotive, IT & Telecom, Healthcare, Retail, BFSI, Government) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

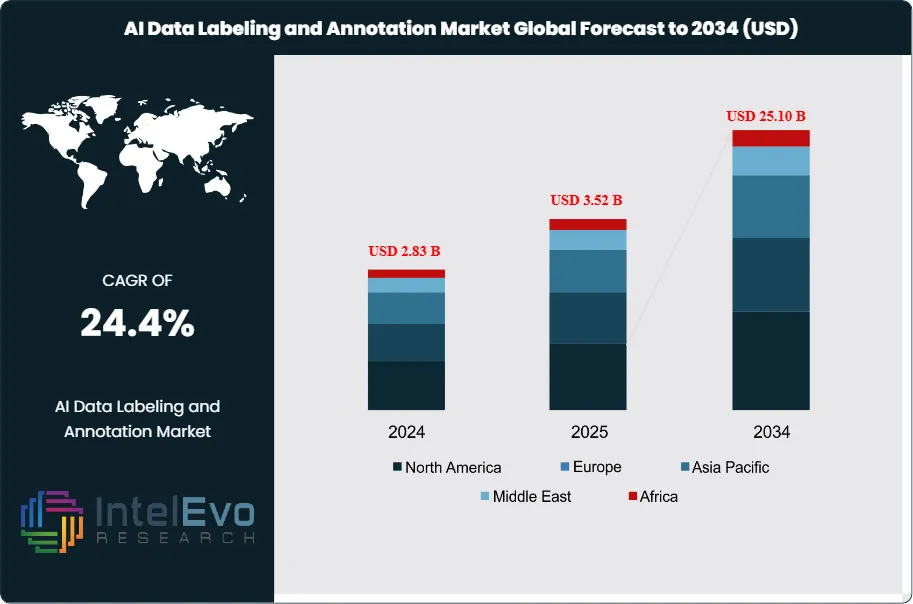

| USD 3.52 Billion | USD 25.1 Billion | 24.4% | North America, 36.2% |

The AI Data Labeling and Annotation Market was valued at approximately USD 2.83 Billion in 2024 and reached USD 3.52 Billion in 2025. The market is projected to grow to USD 25.10 Billion by 2034, expanding at a CAGR of 24.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 21.6 Billion over the analysis period, making AI data labeling and annotation one of the highest-growth segments within the broader artificial intelligence infrastructure supply chain.

Get More Information about this report -

Request Free Sample ReportThe AI data labeling and annotation market occupies a structurally non-negotiable position in commercial AI development. Every supervised learning model, from computer vision systems in autonomous vehicles to large language models powering enterprise chatbots, requires precisely labeled training data as its primary input. Without high-quality annotated datasets, machine learning models cannot achieve the accuracy thresholds required for production deployment. This dependency has evolved into a persistent, expanding demand signal that scales in direct proportion to AI adoption across all vertical industries. Industry analysis indicates that data quality and annotation precision now rank among the top three constraints on AI model performance for enterprise development teams, underscoring the strategic importance of annotation infrastructure investment.

Several structural forces sustain the market's exceptional growth rate. Global private-sector investment in generative AI and foundation model training exceeded USD 100 Billion in 2024, with training data operations, including annotation, representing a primary cost center for model developers. Each large language model pre-training run requires billions of annotated text tokens. Instruction fine-tuning and reinforcement learning from human feedback (RLHF) workflows require ongoing expert human annotation at scale, creating a recurring revenue stream that grows with each generation of model development. Scale AI, the market's leading specialist provider, reported an annualized revenue run rate of USD 1.5 Billion by end-2024 and projected USD 2.0 Billion in 2025, reflecting the acceleration in enterprise and government demand.

Technology transitions are reshaping how annotation work is structured. AI-assisted and semi-automated annotation tools now handle routine labeling tasks, compressing per-label costs and reducing project turnaround times. Pre-trained computer vision models generate initial bounding box and segmentation labels with greater than 85% accuracy for standard object categories, requiring human annotators only for verification, correction, and edge-case resolution. Synthetic data generation, as a complement to traditional annotation, is beginning to influence competitive structure, with platforms integrating synthetic pipelines to reduce dependency on scarce real-world training data.

Regulatory frameworks are creating additional demand. The EU AI Act, applicable from August 2026, legally mandates that high-risk AI systems demonstrate training dataset quality, representativeness, and bias documentation. The NIST AI Risk Management Framework in the United States specifies data quality benchmarks that directly affect annotation specifications and enterprise procurement practices. These requirements have formalized annotation procurement across regulated industries, expanding addressable spend in healthcare, financial services, and government.

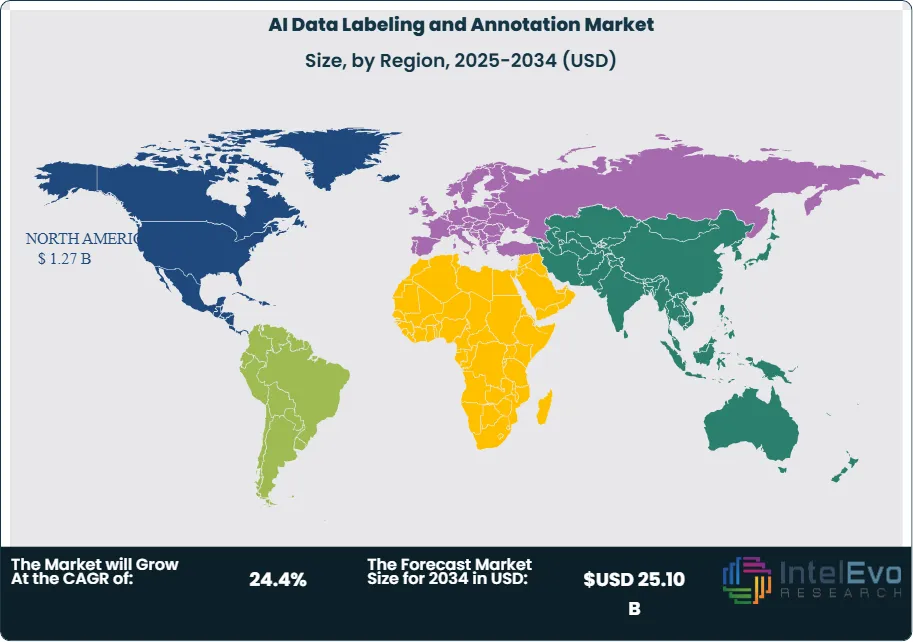

North America held 36.2% of global AI data labeling and annotation market revenues in 2025, driven by concentrated technology investment and the presence of dominant platform providers. Asia Pacific is the fastest-growing region, with China, India, and South Korea scaling AI model development under significant government backing. The absolute dollar opportunity of USD 21.6 Billion, coupled with demand growth across all five major regions, positions the AI data labeling and annotation market as a critical investment priority for technology vendors, AI developers, and institutional capital through 2034.

, By Data Type (Image & Video, Text & NLP, Audio & Speech, LiDAR & Sensor Data, Others), By Annotation Technique (Manual, Semi-Automated, AI-Assisted), By End-Use Industry (Automotive, IT & Telecom, Healthcare, Retail, BFSI, Government) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The AI data labeling and annotation market was valued at USD 3.52 Billion in 2025 and is projected to reach USD 25.1 Billion by 2034, expanding at a CAGR of 24.4% during 2026–2034.

- Segment Dominance: By service type, the data annotation services segment held the largest share at 57.5% of the AI data labeling and annotation market in 2025, generating approximately USD 2.02 Billion, supported by high-volume managed annotation programs across automotive and healthcare AI verticals.

- Segment Dominance: By data type, the image and video annotation sub-segment accounted for 43.5% of market revenues in 2025, generating USD 1.53 Billion, driven by computer vision applications in autonomous driving, retail surveillance, and medical imaging AI.

- Driver: The rapid expansion of generative AI and large language model development is the primary growth driver, with global LLM training infrastructure investment exceeding USD 100 Billion in 2024 and enterprise AI adoption rates reaching 72% among Fortune 500 companies, directly increasing demand for high-volume annotated training datasets.

- Restraint: Data privacy regulations, including the EU's GDPR and California's CCPA, restrict the cross-border transfer and commercial processing of sensitive personal data, limiting the scalability of offshore annotation services for healthcare, finance, and legal verticals that collectively represent 29% of market revenues in 2025.

- Opportunity: The integration of AI-assisted annotation tools within enterprise MLOps platforms represents an addressable expansion opportunity estimated at USD 8.4 Billion by 2034, as organizations seek to internalize data preparation workflows within training pipeline infrastructure.

- Trend: The adoption of AI-assisted annotation techniques is accelerating, with automated annotation tools accounting for 24.5% of the market in 2025 and growing at an estimated 33% CAGR through 2034 as per-label economics improve and foundation model pre-annotation accuracy surpasses 85% for standard categories.

- Regional Analysis: North America leads the AI data labeling and annotation market with a 36.2% share and USD 1.27 Billion in revenues in 2025, supported by dominant enterprise AI spending, concentrated hyperscaler investment, and the presence of leading annotation platform providers.

Competitive Landscape Overview

The AI data labeling and annotation market is moderately fragmented, with the top four players, Scale AI, Appen Limited, Amazon Web Services, and TELUS International AI, collectively accounting for approximately 42% of global revenues in 2025. Competition is primarily technology-driven and capability-differentiated, with providers competing on annotation accuracy rates, turnaround speed, data type coverage, platform integration depth, and compliance certifications. M&A activity intensified significantly through 2024 and 2025, with data annotation tools companies raising USD 222 Million in equity funding across 11 rounds in the first half of 2025 alone, a 199% increase over the same period in 2024. Strategic acquisitions by hyperscalers and enterprise software firms are vertically integrating training data pipelines, creating competitive pressure on pure-play annotation service providers.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Scale AI | United States | Leader | Scale Data Engine | North America | Meta stake acquisition 49%, Jun 2025 |

| Appen Limited | Australia | Leader | Appen Data Platform | Asia Pacific, NA | AI-assisted quality review, Mar 2025 |

| Amazon Web Services | United States | Leader | SageMaker Ground Truth | Global | Bedrock integration, Feb 2025 |

| TELUS International AI | Canada | Challenger | TELUS AI Annotate | NA, Europe | 50+ languages support, Apr 2025 |

| Google Cloud | United States | Leader | Vertex AI Data Labeling | Global | ISO/IEC 42001 benchmarks, Jun 2025 |

| Labelbox | United States | Challenger | Labelbox Annotate | NA | Databricks MLflow integration, Sep 2025 |

| SuperAnnotate | United States | Niche Player | SuperAnnotate Platform | Europe, NA | DICOM medical module, Nov 2025 |

| CloudFactory | New Zealand | Niche Player | CloudFactory ML Data | Asia Pacific | Philippines expansion, Jan 2026 |

| iMerit | United States | Niche Player | iMerit Annotation Services | NA, India | LiDAR partnership, Dec 2024 |

| Snorkel AI | United States | Niche Player | Snorkel Flow | North America | USD 100M Series D, May 2025 |

By Service Type

The AI data labeling and annotation market by service type divides into data annotation services, annotation platform-as-a-service, and consulting and integration services. Data annotation services commanded 57.5% of the market in 2025, generating revenues of approximately USD 2.02 Billion. This segment encompasses managed human annotation, crowdsourced labeling, and hybrid human-in-the-loop workflows delivered by specialist providers across global delivery centers. Demand is highest from automotive OEMs building autonomous driving perception datasets, healthcare organizations developing diagnostic AI models, and technology firms training foundation models requiring iterative RLHF rounds. The segment benefits from the scalability of global annotation workforces across India, the Philippines, Kenya, and Eastern Europe, which deliver cost-effective high-volume annotation with multi-shift operational capacity. Quality control mechanisms, including multi-pass review, inter-annotator agreement scoring, and platform-native consensus tools, have become baseline differentiators among leading service providers, with top-tier managed services commanding per-label premiums of 40–60% over commodity crowdsourced alternatives.

The annotation platform-as-a-service sub-segment held 28.5% of market revenues in 2025, equating to USD 1.00 Billion. Cloud-based annotation platforms allow data science teams to manage labeling workflows, track annotation progress, assign tasks to internal or external annotators, and integrate labeled outputs directly into training pipelines without building proprietary tooling. Adoption is accelerating among mid-market enterprises that previously relied on manual processes or fragmented tooling, with cloud delivery eliminating infrastructure management overhead and enabling pay-as-you-go pricing that lowers the entry barrier for smaller AI development teams. Platform vendors are differentiating through native integrations with MLOps frameworks including MLflow, Kubeflow, and Databricks, as well as through pre-built ontology libraries for domain-specific annotation tasks in medical imaging, legal documents, and financial instruments. Consulting and integration services accounted for the remaining 14.0% of the market in 2025, serving large enterprises requiring custom annotation taxonomy design, quality framework development, and full-program implementation managed by domain specialists.

By Data Type

The AI data labeling and annotation market by data type segments into image and video, text and NLP, audio and speech, sensor/LiDAR/point cloud, and other modalities. Image and video annotation held 43.5% of total market revenues in 2025, generating USD 1.53 Billion. Computer vision applications across autonomous vehicles, retail checkout automation, industrial defect inspection, and medical diagnostics drive this segment as the dominant data type category. Bounding box, polygon, semantic segmentation, instance segmentation, and keypoint annotation techniques represent the most widely deployed workflows. The expansion of video-based AI training for real-time object detection and behavioral analysis has increased average annotation complexity per project, sustaining per-project revenue growth even as per-label costs decline with automation adoption.

Text and NLP annotation accounted for 28.0% of the market in 2025, generating approximately USD 0.99 Billion. The proliferation of large language models has made intent classification, named entity recognition, sentiment labeling, and instruction fine-tuning among the highest-volume annotation tasks globally. LLM developers require diverse, multilingual, domain-specific text datasets at scale, creating sustained demand for expert human labelers with linguistic and subject-matter expertise. Audio and speech annotation held 14.5% of market share in 2025, underpinned by voice assistant development, speech-to-text model training, emotion detection, and audio event classification. Sensor/LiDAR/point cloud annotation contributed 10.5% of revenues in 2025, with autonomous vehicle programs from automotive OEMs and robotics firms driving demand for 3D bounding box, semantic segmentation, and object tracking annotation on multi-sensor datasets. Other data types, including tabular and time-series data annotation for financial and industrial AI, comprised the remaining 3.5% of the market.

By Annotation Technique

The AI data labeling and annotation market by annotation technique is structured across manual annotation, semi-automated annotation, and automated/AI-assisted annotation. Manual annotation retained the largest share at 41.0% of the market in 2025, reflecting the continued necessity of expert human judgment in high-stakes domains including radiology image interpretation, legal document analysis, and complex autonomous driving edge cases involving occlusion, adverse weather, and unusual object configurations. Despite the growth of automation tools, manual annotation commands a price premium per label, sustaining high revenue contribution even as labeled-output volume grows with technology adoption. Quality considerations in regulated industries, where annotation errors carry direct compliance and safety consequences, further entrench manual annotation as the baseline for mission-critical dataset creation.

Semi-automated annotation, which combines algorithmic pre-labeling with human verification and correction, held 32.5% of the market in 2025 and represents the fastest-growing conventional technique among enterprise buyers seeking to balance cost efficiency with output quality. Automated and AI-assisted annotation accounted for 24.5% of the market in 2025, growing at approximately 33% CAGR as pre-trained models generate reliable initial labels that require only spot-check validation for standard categories. This structural shift compresses total annotation hours per project substantially for high-volume, well-defined annotation tasks. Synthetic data generation, emerging as a complementary technique, is beginning to reduce dependency on real-world annotation for controlled domains including warehouse robotics, traffic simulation, and pharmaceutical imaging, and is expected to contribute meaningfully to technique diversification by 2034.

By End-Use Industry

The AI data labeling and annotation market by end-use industry spans automotive and autonomous vehicles, IT and telecommunications, healthcare and life sciences, retail and e-commerce, banking and financial services, government and defense, and others. Automotive and autonomous vehicles held 22.5% of market revenues in 2025, or approximately USD 0.79 Billion, supported by multi-billion-dollar programs requiring continuous LiDAR, camera, and radar dataset creation and refresh across Level 3 and Level 4 autonomous system development programs. IT and telecommunications contributed 20.0% of market revenues in 2025, driven by enterprise AI deployment in customer service automation, network optimization, and cybersecurity threat detection. Healthcare and life sciences held 18.5% in 2025, generating USD 0.65 Billion, with medical imaging AI, clinical NLP, and genomics data labeling as primary demand sources, growing at a notable 29.7% CAGR through 2034. Retail and e-commerce represented 12.5%, BFSI accounted for 10.5%, and government and defense held 8.0%, and other verticals comprised the remaining 8.0%.

Regional Analysis

North America

North America accounted for 36.2% of the global AI data labeling and annotation market in 2025, generating USD 1.27 Billion. The United States dominates regional revenues, driven by the world's largest concentration of AI research institutions, technology hyperscalers, autonomous vehicle programs, and enterprise AI deployments. Federal investment through the National AI Initiative Act and DARPA-funded research programs sustains institutional demand for annotated datasets in defense and intelligence applications. Scale AI's landmark Department of Defense contracts, reportedly exceeding USD 1 Billion in cumulative value as of early 2025, exemplify the growing role of government procurement in market revenue. Compliance frameworks derived from Executive Orders on AI Safety and the NIST AI Risk Management Framework have prompted regulated U.S. industries, including healthcare and financial services, to formalize training data quality standards, accelerating spend on professionally managed annotation services. Canada contributes meaningfully through TELUS International AI's annotation operations and Montreal's and Toronto's AI research clusters. Mexico is emerging as a bilingual nearshore annotation center, benefiting from proximity to U.S. enterprise buyers and competitive delivery costs.

Europe

Europe held 24.1% of global market revenues in 2025, equating to USD 0.85 Billion. Germany is the largest national market within the region, supported by automotive industry investment in sensor fusion and ADAS annotation projects from BMW, Mercedes-Benz, and Volkswagen, which maintain multi-year contracts with specialist annotation providers for LiDAR and camera dataset creation. The United Kingdom maintains a strong position in NLP annotation for fintech, legal AI, and pharmaceutical applications. France is accelerating AI investment following national strategic initiatives aligned with the European Commission's Horizon Europe program. The EU AI Act, entering full application in August 2026, is the most structurally significant regulatory driver for the European annotation market: high-risk AI system operators face legal requirements to demonstrate training dataset quality, representativeness, and bias documentation, formalizing procurement across financial services, healthcare, and public-sector AI programs. GDPR-compliant annotation infrastructure, which restricts the transfer of personal data to non-EEA jurisdictions for commercial processing, has created demand for European-resident annotation workforce capacity, improving competitive positioning for regional service providers. The Netherlands is a meaningful contributor through its financial services AI development activity.

Asia Pacific

Asia Pacific represented 29.5% of global market revenues in 2025, generating USD 1.04 Billion, and is the fastest-growing region in the AI data labeling and annotation market. China is the largest national market within the region, where national AI development plans including the New Generation Artificial Intelligence Development Plan fund large-scale dataset creation programs across smart city, healthcare, and financial AI applications. The National Development and Reform Commission has designated AI training data quality as a strategic national priority, generating direct government procurement demand for annotation services and platforms. India is the largest source of annotation labor globally, with the IT services sector employing an estimated 200,000 or more data annotation professionals. Indian specialist firms are advancing from commodity crowdsourcing toward high-skill expert annotation in medical imaging, legal NLP, and multilingual voice datasets. South Korea's semiconductor and automotive AI programs generate growing demand for LiDAR, image, and sensor annotation, while Japan's industrial and robotics AI deployments are creating sustained requirements for precision manufacturing and quality-control annotation datasets.

Latin America

Latin America accounted for 5.8% of the global AI data labeling and annotation market in 2025, generating USD 0.20 Billion. Brazil is the regional leader, with São Paulo-based technology firms and financial institutions driving NLP annotation demand for credit risk modeling, fraud detection, and customer service AI. Mexico is establishing itself as a nearshore annotation delivery hub for U.S.-based buyers, offering Spanish and English bilingual capabilities at competitive cost points, with proximity facilitating real-time collaboration on complex taxonomy design. Regional growth is constrained by limited enterprise AI budgets among mid-market buyers, fragmented cloud infrastructure outside major cities, and relatively shallow talent pools for specialized annotation disciplines including medical imaging and LiDAR. Government digitalization programs across Brazil, Colombia, and Chile are beginning to generate institutional AI procurement requirements, creating an emerging public-sector demand segment that is expected to expand through the forecast period as regulatory frameworks for AI deployment mature across the region.

Middle East & Africa

The Middle East and Africa region held 4.4% of global market revenues in 2025, generating USD 0.15 Billion. The United Arab Emirates is the dominant single market within the region, backed by the UAE National AI Strategy 2031 and government investment in AI model development for smart city operations, healthcare diagnostics, and financial infrastructure. The UAE Artificial Intelligence Office's active procurement of AI capabilities has positioned Abu Dhabi and Dubai as emerging enterprise annotation buyers with growing sovereign AI training data requirements. Saudi Arabia's Vision 2030 program includes digital transformation mandates that are generating AI training data requirements across government-operated sectors including transportation, health, and financial services. South Africa serves as the primary African market, with Cape Town and Johannesburg hosting growing technology sectors that include early-stage AI development activity. The region's annotation market is primarily import-dependent, with most services procured from North American and Asian providers, representing a substantial localization and workforce development opportunity as domestic AI investment scales through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- Data Annotation Services

- Annotation Platform-as-a-Service

- Consulting and Integration Services

By Data Type

- Image and Video Annotation

- Text and NLP Annotation

- Audio and Speech Annotation

- Sensor/LiDAR/Point Cloud Annotation

- Other Data Types

By Annotation Technique

- Manual Annotation

- Semi-Automated Annotation

- Automated/AI-Assisted Annotation

By End-Use Industry

- Automotive and Autonomous Vehicles

- IT and Telecommunications

- Healthcare and Life Sciences

- Retail and E-Commerce

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense

- Others

By Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises (SMEs)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.52 B |

| Forecast Revenue (2034) | USD 25.10 B |

| CAGR (2025-2034) | 24.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type, (Data Annotation Services, Annotation Platform-as-a-Service, Consulting and Integration Services), By Data Type, (Image and Video Annotation, Text and NLP Annotation, Audio and Speech Annotation, Sensor/LiDAR/Point Cloud Annotation, Other Data Types), By Annotation Technique, (Manual Annotation, Semi-Automated Annotation, Automated/AI-Assisted Annotation), By End-Use Industry, (Automotive and Autonomous Vehicles, IT and Telecommunications, Healthcare and Life Sciences, Retail and E-Commerce, Banking, Financial Services and Insurance (BFSI), Government and Defense, Others), By Enterprise Size, (Large Enterprises, Small and Medium-Sized Enterprises (SMEs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Scale AI, Appen Limited, Amazon Web Services (Amazon SageMaker Ground Truth), TELUS International AI, Google Cloud (Vertex AI Data Labeling), Labelbox, SuperAnnotate, CloudFactory, iMerit, Encord, Snorkel AI, Sama (formerly Samasource), Dataloop, Kili Technology, Microsoft Azure (Azure Machine Learning Data Labeling), Lionbridge AI, Playment, V7 Labs, Alegion, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Data Type (Image & Video, Text & NLP, Audio & Speech, LiDAR & Sensor Data, Others), By Annotation Technique (Manual, Semi-Automated, AI-Assisted), By End-Use Industry (Automotive, IT & Telecom, Healthcare, Retail, BFSI, Government) Industry Trends & Forecast 2026–2034")

, By Data Type (Image & Video, Text & NLP, Audio & Speech, LiDAR & Sensor Data, Others), By Annotation Technique (Manual, Semi-Automated, AI-Assisted), By End-Use Industry (Automotive, IT & Telecom, Healthcare, Retail, BFSI, Government) Industry Trends & Forecast 2026–2034")

, By Data Type (Image & Video, Text & NLP, Audio & Speech, LiDAR & Sensor Data, Others), By Annotation Technique (Manual, Semi-Automated, AI-Assisted), By End-Use Industry (Automotive, IT & Telecom, Healthcare, Retail, BFSI, Government) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI Data Labeling and Annotation Market?

Global AI data labeling market valued at USD 2.83B in 2024, reaching USD 25.1B by 2034, growing at a CAGR of 24.4% from 2026–2034.

Who are the major players in the AI Data Labeling and Annotation Market?

Scale AI, Appen Limited, Amazon Web Services (Amazon SageMaker Ground Truth), TELUS International AI, Google Cloud (Vertex AI Data Labeling), Labelbox, SuperAnnotate, CloudFactory, iMerit, Encord, Snorkel AI, Sama (formerly Samasource), Dataloop, Kili Technology, Microsoft Azure (Azure Machine Learning Data Labeling), Lionbridge AI, Playment, V7 Labs, Alegion, Others

Which segments covered the AI Data Labeling and Annotation Market?

By Service Type, (Data Annotation Services, Annotation Platform-as-a-Service, Consulting and Integration Services), By Data Type, (Image and Video Annotation, Text and NLP Annotation, Audio and Speech Annotation, Sensor/LiDAR/Point Cloud Annotation, Other Data Types), By Annotation Technique, (Manual Annotation, Semi-Automated Annotation, Automated/AI-Assisted Annotation), By End-Use Industry, (Automotive and Autonomous Vehicles, IT and Telecommunications, Healthcare and Life Sciences, Retail and E-Commerce, Banking, Financial Services and Insurance (BFSI), Government and Defense, Others), By Enterprise Size, (Large Enterprises, Small and Medium-Sized Enterprises (SMEs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI Data Labeling and Annotation Market

Published Date : 13 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date