AI-driven Precision Medicine Market Size, Share, Growth | 16.8% CAGR

Global AI-driven Precision Medicine Market Size, Share, Analysis Report By Technology (Machine Learning, Natural Language Processing, Deep Learning), By Component (Software, Services), By Application (Oncology, Neurology, Cardiovascular, Infectious Diseases), By End User (Hospitals, Research Institutions, Pharmaceutical Companies), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

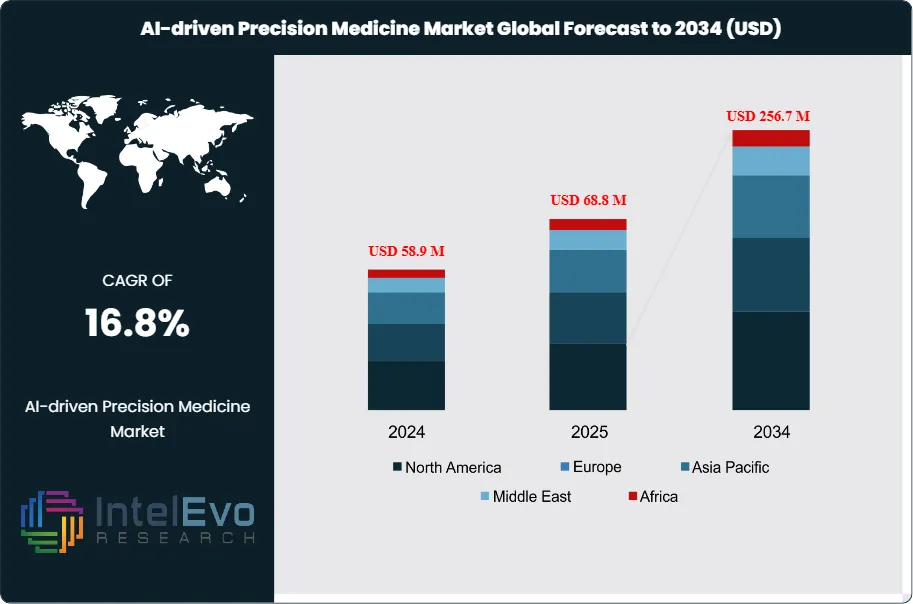

The AI-driven Precision Medicine Market size is expected to be worth around USD 256.7 Million by 2034, up from USD 58.9 Million in 2024, growing at a CAGR of 16.8% during the forecast period from 2025 to 2034. The market is witnessing rapid adoption of AI-based genomics, drug discovery, and personalized healthcare solutions, transforming patient outcomes. With increasing R&D investments and the rise of predictive analytics in healthcare, the AI-driven precision medicine industry is set to revolutionize modern medical practices.

This growth is fueled by rising demand for personalized treatments, integration of advanced AI algorithms in genomics and diagnostics, and increasing investments from healthcare providers and biotech firms. Moreover, supportive government initiatives and strategic collaborations are expected to accelerate adoption across developed and emerging regions.

The AI-driven Precision Medicine market focuses on the application of artificial intelligence technologies to tailor medical treatments and diagnostics to individual patients. This approach combines advanced algorithms and machine learning with clinical data to enhance decision-making processes in healthcare. Currently, the market is experiencing significant growth, driven by the increasing prevalence of chronic diseases and the aging population. Major players are investing heavily in AI solutions that enable better patient outcomes, streamlined clinical workflows, and improved accuracy in treatment plans. The rising demand for personalized healthcare solutions is fueling the expansion of this market, leading to innovations in drug development, genomics, and patient care.

The growth dynamics of the AI-driven Precision Medicine market are robust, with a projected CAGR of 16.1% from 2024 to 2034. Key growth drivers include the rising incidence of cancer, neurological disorders, and other chronic diseases, which necessitate more precise and tailored treatment strategies. Additionally, advancements in AI technologies, such as natural language processing and deep learning, are making it possible to analyze vast amounts of patient data rapidly, thereby enhancing the predictive capabilities of healthcare providers. The market is also bolstered by increased funding from both public and private sectors aimed at developing innovative AI applications in healthcare, as well as collaborations among leading technology companies and healthcare institutions.

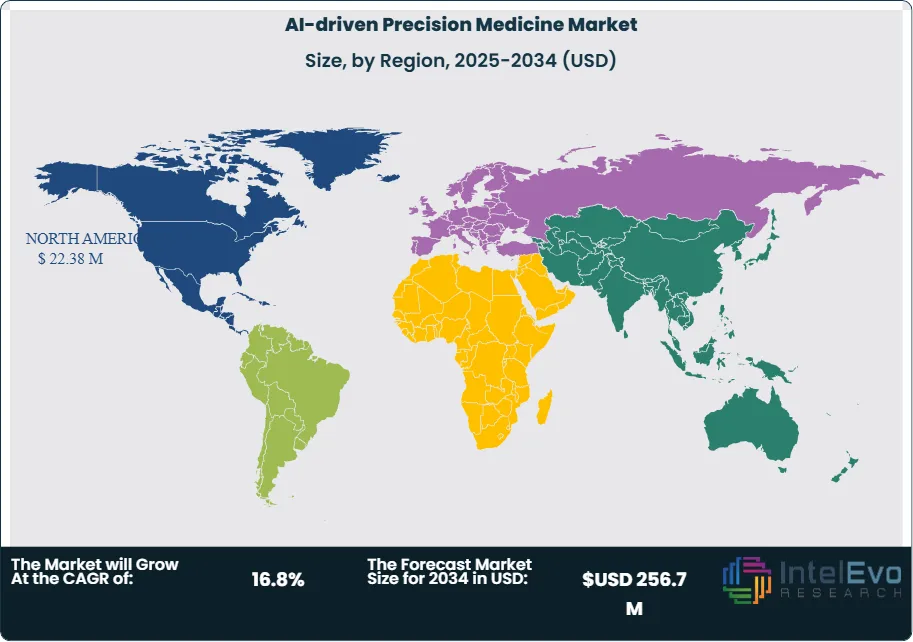

Regionally, North America currently dominates the AI-driven Precision Medicine market due to the presence of established healthcare infrastructure, high investment in research and development, and a strong focus on personalized medicine initiatives. The United States, in particular, is leading in AI healthcare applications, with numerous startups and established companies driving innovation. Europe is also witnessing considerable growth, fueled by increasing healthcare expenditure and the rising demand for advanced diagnostic tools. Meanwhile, the Asia-Pacific region is expected to experience the fastest growth during the forecast period, attributed to an increasing population, rising prevalence of chronic diseases, and improvements in healthcare systems.

The COVID-19 pandemic has significantly impacted the AI-driven Precision Medicine market, accelerating the adoption of AI technologies in healthcare. During the pandemic, AI played a crucial role in managing patient data, predicting patient outcomes, and optimizing resource allocation. The need for rapid diagnostics and effective treatment strategies during this health crisis highlighted the importance of precision medicine. As a result, healthcare providers and researchers increasingly embraced AI-driven solutions, which is expected to sustain growth in the market long after the pandemic subsides.

Key Takeaways

Market Growth: The AI-driven Precision Medicine market is expected to reach USD 256.7 million by 2034, growing at a robust CAGR of 16.8%, indicating strong market expansion driven by technological advancements and rising demand for personalized healthcare solutions.

Technology Segment Analysis: The machine learning segment is anticipated to lead the AI-driven Precision Medicine market, as it enables the analysis of vast amounts of patient data, improving diagnostic accuracy and treatment efficacy, thereby enhancing patient outcomes.

Component Segment Analysis: The software component of the market is projected to hold the largest share, driven by the increasing implementation of AI solutions in healthcare settings to streamline operations, enhance decision-making processes, and facilitate better patient care.

Driver: The rise in chronic diseases and the growing need for personalized healthcare are significant drivers for the market. Advanced AI technologies enhance diagnostics and treatment strategies, improving healthcare delivery and patient management.

Restraint: High implementation costs and concerns regarding data privacy may hinder market growth. Additionally, regulatory challenges and the need for skilled professionals to operate advanced AI systems can impact market dynamics.

Opportunity: The growing demand for AI-driven solutions in developing regions, particularly in Asia-Pacific, presents significant opportunities for market expansion. Increasing investments in healthcare infrastructure will further facilitate the adoption of precision medicine technologies.

Trend: There is a growing trend towards integrating AI technologies in clinical settings, enhancing real-time decision-making and patient management, which is likely to shape the future of healthcare delivery.

Regional Analysis: North America is projected to dominate the market, driven by established healthcare infrastructure and significant investment in research and development. Asia-Pacific is expected to experience the highest growth rate due to rising healthcare demands and advancements in technology.

Technology Analysis:

The AI-driven Precision Medicine market is significantly influenced by advancements in technology, particularly through machine learning, natural language processing, and deep learning. Machine learning algorithms analyze vast datasets to identify patterns and predict patient outcomes, enhancing diagnostic accuracy and treatment effectiveness. Natural language processing is instrumental in extracting valuable insights from unstructured clinical data, such as patient records and research articles, thereby facilitating better decision-making. Deep learning, a subset of machine learning, focuses on processing complex data types, including medical images, enabling early detection of diseases like cancer. The continuous evolution of these technologies is driving innovation in precision medicine, leading to more personalized healthcare solutions and improving patient management and outcomes.

Component Analysis:

The AI-driven Precision Medicine market comprises two main components: software and services. The software segment is projected to dominate the market, as healthcare providers increasingly adopt AI solutions to enhance clinical workflows, improve patient care, and streamline data management. These software solutions enable advanced analytics, real-time decision-making, and integration of AI technologies into existing healthcare systems. Meanwhile, the services segment includes consulting, implementation, and maintenance services essential for effective software deployment. This segment is also witnessing growth due to rising demand for training and support as healthcare professionals adapt to AI technologies. Together, these components are crucial for the successful implementation of AI-driven precision medicine in healthcare settings.

Application Analysis:

The application of AI in precision medicine spans various medical fields, including oncology, neurology, cardiovascular, and infectious diseases. In oncology, AI algorithms assist in analyzing genomic data, facilitating targeted therapies and personalized treatment plans. Neurology applications leverage AI to enhance diagnostic accuracy for conditions such as Alzheimer’s and multiple sclerosis through improved imaging techniques and patient monitoring. The cardiovascular sector benefits from predictive analytics to assess risks and optimize treatment strategies. In infectious diseases, AI technologies help in outbreak prediction and managing patient data during pandemics. Each application area is witnessing increased investment and research, reflecting the growing recognition of AI's potential to revolutionize patient care and treatment outcomes.

End User Analysis:

The end users of AI-driven Precision Medicine primarily include hospitals, research institutions, and pharmaceutical companies. Hospitals are rapidly adopting AI technologies to improve patient outcomes and optimize operational efficiency, particularly in areas like diagnostics, treatment planning, and personalized care strategies. Research institutions leverage AI for advanced data analysis, enabling breakthroughs in medical research and drug development. Pharmaceutical companies utilize AI-driven precision medicine to enhance drug discovery processes, targeting specific patient populations based on genetic and phenotypic data. The collaboration between these end users is crucial for advancing precision medicine, as they share knowledge, data, and resources to drive innovation and improve healthcare delivery.

Region Analysis:

North America Leads with Significant Market Share in AI-driven Precision Medicine: North America dominates the AI-driven Precision Medicine market, accounting for over 40% of the global market share. This leadership position is attributed to several factors, including advanced healthcare infrastructure, high healthcare expenditure, and robust research and development activities. The presence of key players, such as pharmaceutical and biotechnology companies, further fuels innovation and adoption of AI technologies in healthcare. Additionally, the increasing prevalence of chronic diseases and a strong focus on personalized medicine enhance demand for AI-driven solutions. The regulatory environment in the U.S. also supports rapid advancements in precision medicine, making North America a fertile ground for market growth.

In contrast, the Asia-Pacific region is recognized as the fastest-growing market for AI-driven Precision Medicine, with a projected CAGR exceeding 20% during the forecast period. Key drivers of growth include rising healthcare demands due to population growth and urbanization, along with increasing investments in healthcare infrastructure and technology. Countries like China and India are rapidly adopting AI solutions to enhance healthcare delivery and patient management. The growing awareness of personalized medicine among healthcare providers and patients also contributes to market expansion. Meanwhile, Europe and Latin America show steady growth, supported by government initiatives promoting digital health, while the Middle East and Africa are gradually adopting AI technologies, albeit at a slower pace.

By Component (Hardware, Software & AI Platforms, Services), By Technology (Machine Learning, Deep Learning, Natural Language Processing (NLP), Computer Vision), By Application (Oncology, Cardiology, Neurology, Immunology, Rare Diseases, Others), By End User (Hospitals & Clinics, Research & Academic Institutions, Pharmaceutical & Biotechnology Companies, Diagnostic Centers)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

IBM Corporation, Siemens Healthineers, GE Healthcare, Illumina Inc., Philips Healthcare, Merck & Co. Inc., Tempus Labs Inc., Roche Diagnostics, Oracle Corporation, 23andMe Inc., Bio-Rad Laboratories Inc., Invitae Corporation, GRAIL Inc., Foundation Medicine Inc., Flatiron Health, PathAI, F. Hoffmann-La Roche AG, Guardant Health, Syapse Inc., Adaptive Biotechnologies Corporation

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL AI-DRIVEN PRECISION MEDICINE CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Players Analysis:

IBM Corporation: IBM is a global leader in technology and consulting, focusing on AI and data analytics in healthcare. Their Watson Health platform utilizes AI to analyze vast healthcare data, aiding in personalized treatment plans. Headquartered in Armonk, New York, IBM collaborates with healthcare institutions to enhance patient outcomes and reduce costs through AI-driven insights.

Siemens Healthineers: Siemens Healthineers, based in Erlangen, Germany, specializes in medical technology and diagnostic imaging. Their products include imaging systems and laboratory diagnostics, supported by AI-driven solutions that enhance clinical workflows. Siemens aims to empower healthcare providers with advanced technologies to improve precision medicine and patient care, focusing on digitalization and personalized healthcare strategies.

GE Healthcare: Headquartered in Chicago, Illinois, GE Healthcare offers medical imaging, monitoring, biomanufacturing, and digital solutions. Their AI capabilities enhance imaging analysis, enabling personalized treatments and improving patient outcomes. GE Healthcare's strategy emphasizes innovation and partnerships, collaborating with healthcare providers to integrate AI in clinical workflows and expand precision medicine applications.

Illumina, Inc.: Illumina, based in San Diego, California, is a leader in genomics and sequencing technologies. Their advanced sequencing platforms enable researchers and clinicians to explore genetic information for personalized medicine. Illumina's strategy focuses on innovation, offering comprehensive genomic solutions and driving adoption across various healthcare sectors to enhance patient care and outcomes.

Philips Healthcare: Philips Healthcare, headquartered in Amsterdam, Netherlands, provides advanced imaging, patient monitoring, and health informatics solutions. Their AI-driven platforms improve diagnostic accuracy and treatment planning in precision medicine. Philips focuses on patient-centric solutions and collaborates with healthcare providers to drive innovation and digital transformation in the healthcare landscape.

Merck & Co., Inc.: Merck, based in Kenilworth, New Jersey, is a global healthcare company involved in pharmaceuticals and vaccines. The company invests in precision medicine through research and development, targeting personalized therapies for various diseases. Merck's strategy emphasizes collaboration with biotech firms and healthcare institutions to accelerate drug discovery and enhance patient outcomes through innovative therapies.

Tempus Labs, Inc.: Tempus, headquartered in Chicago, Illinois, specializes in data-driven precision medicine, focusing on cancer care. Their platform integrates genomic data, clinical data, and AI algorithms to provide personalized treatment options. Tempus aims to improve patient outcomes by facilitating collaboration between healthcare providers and researchers, enhancing the understanding of cancer treatments through data insights.

Roche Diagnostics: Roche Diagnostics, based in Basel, Switzerland, is a leader in diagnostics and personalized healthcare. Their advanced diagnostics tools, including companion diagnostics, leverage genetic insights for tailored therapies. Roche focuses on innovation and partnerships, driving the integration of AI in diagnostics to enhance personalized treatment strategies and improve patient care globally.

Oracle Corporation: Oracle, headquartered in Austin, Texas, provides cloud solutions and software for healthcare and life sciences. Their healthcare data analytics solutions empower organizations to leverage AI for precision medicine, enabling better decision-making and improved patient outcomes. Oracle's strategy emphasizes cloud-based solutions, enhancing data interoperability and collaboration within healthcare systems.

23andMe, Inc.: 23andMe, based in Mountain View, California, is a consumer genetics company that provides genetic testing services. Their platform offers insights into ancestry and health-related traits, enabling personalized health recommendations. The company focuses on empowering individuals with genetic information, collaborating with research institutions to advance precision medicine and drive innovation in genomics.

Market Key Players

IBM Corporation

Siemens Healthineers

GE Healthcare

Illumina, Inc.

Philips Healthcare

Merck & Co., Inc.

Tempus Labs, Inc.

Roche Diagnostics

Oracle Corporation

23andMe, Inc.

Bio-Rad Laboratories, Inc.

Invitae Corporation

GRAIL, Inc.

Foundation Medicine, Inc.

Flatiron Health

PathAI

F. Hoffmann-La Roche AG

Guardant Health

Syapse, Inc.

Adaptive Biotechnologies Corporation

Drivers:

Rising Prevalence of Chronic Diseases

The increasing prevalence of chronic diseases, such as cancer, diabetes, and cardiovascular disorders, is a significant driver for the AI-driven Precision Medicine market. With the growing aging population worldwide, healthcare systems face immense pressure to provide effective and personalized treatment solutions. AI technologies play a crucial role in analyzing large datasets from patient histories, genetic information, and treatment responses, enabling healthcare providers to develop tailored treatment plans. This demand for personalized healthcare solutions not only enhances patient outcomes but also reduces healthcare costs, making AI-driven precision medicine an attractive option for healthcare providers and patients alike.

Advancements in Technology

Technological advancements, particularly in AI, machine learning, and big data analytics, are pivotal in driving the growth of the AI-driven Precision Medicine market. These technologies enhance the ability to analyze complex datasets, leading to improved diagnostics and treatment planning. For instance, machine learning algorithms can identify patterns in genomic data, facilitating targeted therapies based on individual genetic profiles. Additionally, natural language processing allows for efficient extraction of information from unstructured clinical data, improving decision-making in healthcare. As technology continues to evolve, its integration into precision medicine will likely lead to more effective and efficient healthcare solutions.

Increased Investment in Healthcare Infrastructure

The growing investment in healthcare infrastructure, particularly in developing regions, is another key driver for the AI-driven Precision Medicine market. Governments and private organizations are recognizing the importance of enhancing healthcare services and are allocating significant resources to modernize facilities and implement advanced technologies. This investment fosters the adoption of AI-driven solutions in precision medicine, as healthcare providers seek to improve patient care and operational efficiency. Additionally, partnerships between technology firms and healthcare institutions are emerging, further facilitating the integration of AI technologies into healthcare practices, thus driving market growth.

Restraints

High Implementation Costs

One of the primary restraints facing the AI-driven Precision Medicine market is the high implementation costs associated with integrating advanced technologies into existing healthcare systems. The development and deployment of AI algorithms, data storage solutions, and necessary hardware can require substantial financial investment, which may deter smaller healthcare providers from adopting these innovations. Additionally, ongoing maintenance, updates, and the need for specialized personnel to manage and interpret AI-driven insights contribute to the overall costs. This financial burden can limit accessibility to advanced precision medicine solutions, particularly in low-resource settings, ultimately affecting the market's growth potential.

Data Privacy and Security Concerns

Data privacy and security concerns present significant challenges to the AI-driven Precision Medicine market. The sensitive nature of healthcare data, including patient information and genetic data, necessitates strict compliance with regulations such as HIPAA in the United States and GDPR in Europe. Healthcare providers must ensure robust data protection measures are in place to mitigate risks associated with data breaches and unauthorized access. Concerns about data misuse or mishandling can lead to patient apprehension regarding the use of AI-driven technologies in healthcare, hindering market growth as providers navigate the complexities of maintaining patient trust while implementing innovative solutions.

Opportunities

Expanding Applications in Developing Regions

The increasing demand for precision medicine solutions in developing regions presents a significant opportunity for market growth. As healthcare systems in countries like India, China, and Brazil continue to evolve, there is a rising awareness of the benefits of personalized healthcare. Governments and private sector stakeholders are investing in modernizing healthcare infrastructure and integrating advanced technologies, including AI and machine learning. This trend creates a favorable environment for the adoption of AI-driven precision medicine solutions, allowing healthcare providers to offer more effective treatments and improve patient outcomes. Targeting these emerging markets can lead to substantial growth opportunities for industry players.

Collaboration Between Technology and Healthcare Sectors

Another promising opportunity lies in the collaboration between technology companies and healthcare providers to drive innovation in AI-driven Precision Medicine. Partnerships can facilitate the sharing of knowledge, resources, and expertise, leading to the development of more effective AI solutions tailored to the unique needs of healthcare systems. Such collaborations can enhance the integration of AI technologies into clinical workflows, improve diagnostic accuracy, and optimize treatment plans. By fostering an ecosystem that encourages innovation, stakeholders can accelerate the adoption of precision medicine, ultimately improving patient care and driving growth in the AI-driven Precision Medicine market.

Trends:

Integration of AI with Genomics

One significant trend in the AI-driven Precision Medicine market is the integration of AI technologies with genomics. As genomic data becomes increasingly available through advances in sequencing technologies, AI tools are being utilized to analyze and interpret this vast amount of genetic information. By leveraging machine learning algorithms, healthcare providers can identify genetic variants linked to specific diseases, predict patient responses to treatments, and develop personalized therapeutic strategies. This trend is not only enhancing diagnostic accuracy but also facilitating the discovery of new drug targets, ultimately transforming how diseases are treated and paving the way for more effective, individualized care.

Recent Development

In July 2024: Visiopharm revealed a collaboration with Glint Lab, Inc., which aims to enhance pathology solutions and drive scientific discovery. This partnership will combine Visiopharm's expertise in digital pathology with Glint Lab's innovative approaches to provide more advanced tools for pathologists.

In June 2024: Visiopharm and UMC Utrecht achieved a significant breakthrough in AI-powered detection of breast cancer lymph node metastases. This development showcases the potential of AI technology in improving the accuracy of cancer diagnostics, reinforcing the importance of digital pathology in modern medical practices.

Frequently Asked Questions

How big is the AI-driven Precision Medicine Market?

Discover insights on the AI-driven Precision Medicine Market — projected to reach USD 256.7 Million by 2034, growing at a CAGR of 16.8%. Explore trends, key players & innovations.

Who are the major players in the AI-driven Precision Medicine Market?

IBM Corporation, Siemens Healthineers, GE Healthcare, Illumina Inc., Philips Healthcare, Merck & Co. Inc., Tempus Labs Inc., Roche Diagnostics, Oracle Corporation, 23andMe Inc., Bio-Rad Laboratories Inc., Invitae Corporation, GRAIL Inc., Foundation Medicine Inc., Flatiron Health, PathAI, F. Hoffmann-La Roche AG, Guardant Health, Syapse Inc., Adaptive Biotechnologies Corporation

Which segments covered the AI-driven Precision Medicine Market?

By Component (Hardware, Software & AI Platforms, Services), By Technology (Machine Learning, Deep Learning, Natural Language Processing (NLP), Computer Vision), By Application (Oncology, Cardiology, Neurology, Immunology, Rare Diseases, Others), By End User (Hospitals & Clinics, Research & Academic Institutions, Pharmaceutical & Biotechnology Companies, Diagnostic Centers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, By Component (Software, Services), By Application (Oncology, Neurology, Cardiovascular, Infectious Diseases), By End User (Hospitals, Research Institutions, Pharmaceutical Companies), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, By Component (Software, Services), By Application (Oncology, Neurology, Cardiovascular, Infectious Diseases), By End User (Hospitals, Research Institutions, Pharmaceutical Companies), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, By Component (Software, Services), By Application (Oncology, Neurology, Cardiovascular, Infectious Diseases), By End User (Hospitals, Research Institutions, Pharmaceutical Companies), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, By Component (Software, Services), By Application (Oncology, Neurology, Cardiovascular, Infectious Diseases), By End User (Hospitals, Research Institutions, Pharmaceutical Companies), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")