- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI Governance & Compliance Software Market 2034 | CAGR 23.3%

Global AI Governance and Compliance Software Market Size, Share, Growth & Industry Analysis By Offering (Software/Platform, Services), By Deployment (Cloud, On-Premise), By Application (Risk Management, Compliance Management, Audit & Reporting, Model Monitoring & Explainability) Industry Trends, Competitive Landscape, Regulatory Insights, Market Dynamics & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 2.80 Billion | USD 18.50 Billion | 23.3% | North America, 42.1% |

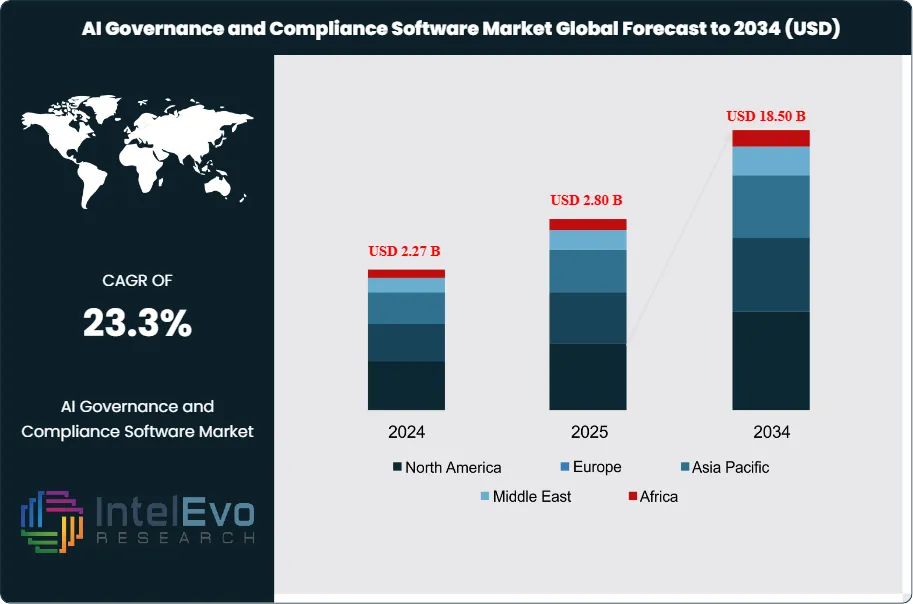

The AI Governance and Compliance Software Market was valued at approximately USD 2.27 Billion in 2024 and reached USD 2.80 Billion in 2025. The market is projected to grow to USD 18.50 Billion by 2034, expanding at a CAGR of 23.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 15.70 Billion over the analysis period. The rapid proliferation of generative artificial intelligence and large language models (LLMs) has necessitated a fundamental shift from experimental AI to regulated, enterprise-grade deployments. Organizations are increasingly adopting specialized software to manage the ethical, legal, and operational risks associated with automated decision-making. Current market assessment shows that the demand for these solutions is primarily catalyzed by the stringent requirements of the EU AI Act and the evolving NIST AI Risk Management Framework in the United States.

Get More Information about this report -

Request Free Sample ReportMarket patterns indicate a significant transition toward "governance-by-design," where compliance checks are integrated directly into the machine learning lifecycle rather than treated as an afterthought. Demand is surging for platforms that provide transparency into "black-box" models, offering features such as bias detection, drift monitoring, and explainability. Supply-side evaluation suggests that hyperscalers and pure-play AI governance startups are competing to provide unified platforms that bridge the gap between technical data science teams and legal compliance departments. Regulatory influences remain the strongest catalyst for investment; the implementation of tiered risk categories for AI systems has forced enterprises to catalog and audit their entire AI inventory, driving high-volume software license acquisitions.

Risk factors including data privacy breaches, algorithmic bias, and the potential for "hallucinations" in generative models have made AI governance a board-level priority. Technology effects, particularly the rise of Retrieval-Augmented Generation (RAG) and agentic AI systems, have introduced new complexities in tracking data lineage and ensuring model safety. Regional highlights show that North America maintains a dominant position due to early enterprise adoption and high venture capital activity, while Europe is emerging as a critical investment hotspot as companies scramble to meet compliance deadlines for regional mandates. In the Asia Pacific region, rapid digitalization in financial services and healthcare is expected to fuel the highest growth rates toward the end of the forecast period. Trade data and regulatory filings suggest that industries such as BFSI and healthcare are currently allocating 12% to 15% of their total AI budgets specifically to governance and compliance tools to mitigate potential litigation and brand damage.

, By Deployment (Cloud, On-Premise), By Application (Risk Management, Compliance Management, Audit & Reporting, Model Monitoring & Explainability) Industry Trends, Competitive Landscape, Regulatory Insights, Market Dynamics & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Global AI Governance and Compliance Software Market is projected to expand from USD 2.80 Billion in 2025 to USD 18.50 Billion by 2034, representing a robust CAGR of 23.3%.

- Segment Dominance: The Software/Platform offering held a dominant 68.4% market share in 2025, valued at USD 1.91 Billion, driven by the shift toward automated risk assessment tools.

- Segment Dominance: The BFSI vertical emerged as the leading end-user segment in 2025 with a 28.2% share, as banks prioritize anti-money laundering (AML) and bias mitigation in lending algorithms.

- Driver: Global regulatory mandates, led by the enforcement of the EU AI Act, are projected to drive a 35% year-over-year increase in compliance-related software spending through 2027.

- Restraint: A critical shortage of AI ethics and compliance professionals acts as a bottleneck, potentially slowing implementation timelines for 40% of large-scale enterprise deployments.

- Opportunity: The emergence of specialized GenAI auditing tools presents a USD 4.2 Billion untapped opportunity as firms seek to validate the safety of large language model outputs.

- Trend: Integration of "Agentic Governance" is a primary trend, where AI agents autonomously monitor other AI systems for drift and compliance violations in real-time.

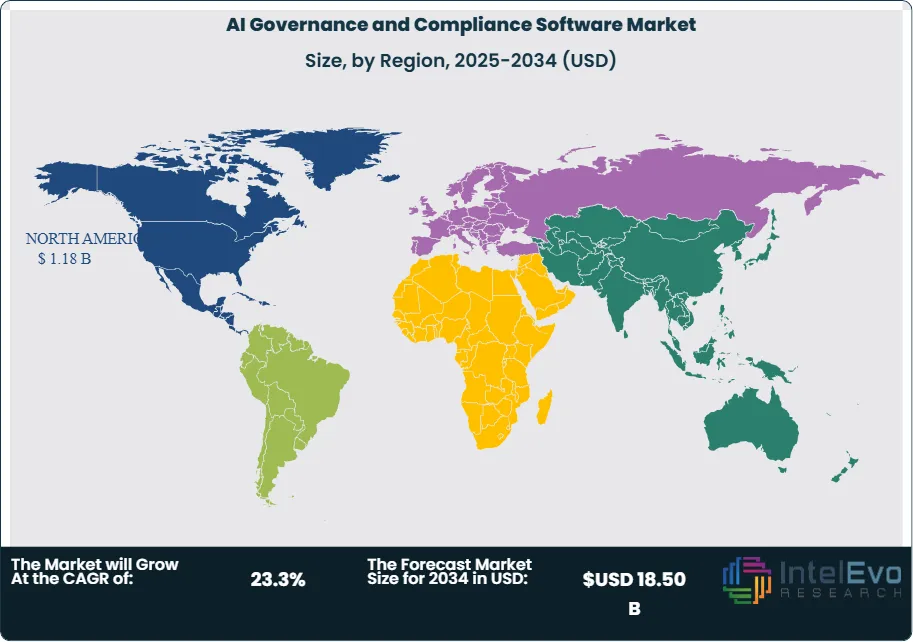

- Regional Analysis: North America remains the leading market with a 42.1% share in 2025, contributing USD 1.18 Billion in revenue due to heavy investment in enterprise AI safety frameworks.

Competitive Landscape Overview

The Global AI Governance and Compliance Software Market is currently moderately consolidated, with the top four players commanding a combined market share of approximately 46.5% in 2025. Competition is increasingly platform-based, with major cloud providers integrating governance modules into their existing AI stacks, while pure-play vendors focus on deep ethical auditing and multi-cloud interoperability. Strategic pivots toward "Generative AI Guardrails" have become the primary focus of 2025-2026 product roadmaps. Competitive intensity has shifted toward providing seamless integration with MLOps pipelines to ensure that compliance does not hinder development velocity.

| Company Name | Headquarters | Market Position | Key Product | Geographic Strength | Recent Strategic Move |

| IBM Corporation | USA | Leader | watsonx.governance | Global | Launched upgraded RAG auditing features in Q4 2025 |

| Microsoft Corp. | USA | Leader | Azure AI Content Safety | North America | Integrated Purview with Azure AI for end-to-end compliance |

| OneTrust | USA | Leader | AI Governance Cloud | Europe/North America | Acquired specialized AI risk startup in mid-2025 |

| Google (Alphabet) | USA | Leader | Vertex AI Governance | Global | Released automated model card generation tools in Jan 2026 |

| DataRobot | USA | Challenger | AI Production Governance | North America | Partnered with consulting firms for EU AI Act readiness |

| Collibra | Belgium | Challenger | AI Governance Platform | Europe | Expanded data lineage for unstructured data |

| Credo AI | USA | Niche Player | Responsible AI Platform | North America | Secured Series C funding for risk modules |

| Arthur AI | USA | Niche Player | Arthur Bench | North America | Launched benchmarking for LLM hallucinations in 2025 |

| BigID | USA | Challenger | AI Data Governance | Global | Integrated DSPM with AI compliance |

| Trustible | USA | Niche Player | Trustible Compliance | Europe | Focused on SME-specific compliance for EU AI Act |

By Offering

Based on supply-chain evaluation, the software and platform segment dominated the market in 2025 with a revenue value of USD 1.91 Billion, accounting for 68.4% of the total market. This dominance is attributed to the urgent need for scalable, automated tools that can inventory AI assets and perform real-time monitoring across distributed model deployments. Enterprises are prioritizing platforms that offer a centralized dashboard for risk management, bias detection, and compliance reporting to satisfy both internal audits and external regulatory inquiries. The recurring revenue model associated with cloud-native SaaS platforms provides a stable growth trajectory for vendors in this space.

The services segment, including consulting, integration, and managed services, accounted for the remaining 31.6% of the market in 2025, valued at USD 0.89 Billion. While software provides the technical framework, the high complexity of evolving regulations like the EU AI Act has created a massive demand for professional services. Organizations frequently require expert guidance to interpret legal requirements into technical specifications. This segment is expected to maintain a steady growth rate as mid-sized enterprises, lacking in-house AI ethics teams, seek third-party assistance for initial setup and ongoing compliance monitoring through 2034.

By Deployment

Cloud-based deployment held a significant 72.5% market share in 2025, representing USD 2.03 Billion in revenue. The inherent flexibility and scalability of the cloud are essential for managing the high compute requirements of model auditing and drift analysis. Furthermore, most AI development currently occurs in cloud environments like Azure, AWS, and Google Cloud, making it logical to deploy governance layers within the same infrastructure. The rapid adoption of serverless governance functions and API-driven compliance checks is a key driver for this segment’s expansion through the forecast period.

On-premise deployment accounted for 27.5% of the market in 2025, valued at USD 0.77 Billion. This segment remains critical for highly regulated industries such as defense, national security, and specific sub-sectors of healthcare where data sovereignty and extreme privacy are paramount. These organizations prefer maintaining governance tools behind their own firewalls to prevent sensitive model metadata or training data samples from leaving their controlled environment. While the overall share of on-premise solutions is expected to decline slightly as hybrid cloud security matures, the absolute revenue from this segment will continue to grow due to high-value contracts with government entities.

By Vertical

The Banking, Financial Services, and Insurance (BFSI) sector led the market in 2025 with a 28.2% share, valued at USD 0.79 Billion. Financial institutions utilize AI for high-stakes decisions, including credit scoring, fraud detection, and algorithmic trading, making them primary targets for regulatory scrutiny. The need to provide "right to explanation" for denied loans and to ensure that anti-money laundering models do not unfairly target specific demographics drives significant investment in governance software. As central banks worldwide introduce specific AI guidelines, BFSI spend is projected to remain at the forefront of the market.

Healthcare and Life Sciences represented the second-largest vertical with a 19.5% share in 2025, worth USD 0.55 Billion. The use of AI in clinical trial recruitment, diagnostic imaging, and drug discovery requires rigorous validation to ensure patient safety and data privacy (HIPAA/GDPR compliance). In clinical settings, the "black-box" nature of AI is a major hurdle; therefore, governance software that provides high levels of interpretability and transparency is in high demand. Other significant verticals include Government and Defense (15.1%), Retail and E-commerce (12.4%), and IT and Telecommunications (14.8%), each driven by unique risk profiles.

Regional Analysis

North America

North America dominated the Global AI Governance and Compliance Software Market in 2025, capturing a 42.1% share with a revenue value of USD 1.18 Billion. The United States is the primary engine of growth, characterized by an mature ecosystem of AI developers and high enterprise spending on risk mitigation. While the U.S. lacks a single federal AI law comparable to Europe's, the proliferation of sector-specific regulations from the SEC, FTC, and the adoption of the NIST AI Risk Management Framework have created a complex compliance environment. Canadian organizations are also increasing investment in response to the Artificial Intelligence and Data Act (AIDA). The presence of major hyperscalers and a dense concentration of AI startups ensures that North America remains the leader in technical innovation and market volume through 2034.

Europe

Europe held a 26.4% market share in 2025, valued at USD 0.74 Billion, and is positioned as the regulatory heart of the global market. The enforcement of the EU AI Act has created an immediate mandate for companies operating within the Union to implement comprehensive governance systems. High-risk AI applications must undergo rigorous conformity assessments, driving a surge in software demand for technical documentation and logging. Germany, France, and the UK are the top three regional markets, with German automotive and manufacturing sectors heavily investing in ethical AI to maintain global competitiveness. European firms are increasingly prioritizing "Sovereign AI" solutions that emphasize data privacy, positioning the region as a pioneer in regulated AI adoption.

Asia Pacific

The Asia Pacific region accounted for 18.2% of the market in 2025, representing USD 0.51 Billion, but it is expected to exhibit the fastest CAGR of 26.8% through 2034. China is a major contributor, with strict domestic regulations regarding generative AI and recommendation algorithms driving rapid software adoption. In India, the massive IT services sector is integrating AI governance into its global delivery models to meet the compliance needs of international clients. Japan and South Korea are focusing on "Human-Centric AI" frameworks, particularly in healthcare and robotics. The rapid digitalization of Southeast Asian economies and increasing government initiatives for national AI strategies provide significant long-term growth potential.

Latin America

Latin America held a 6.8% share in 2025 (USD 0.19 Billion), with Brazil and Mexico leading the adoption as financial institutions modernize their compliance stacks. In these markets, the focus is increasingly on bridging the gap between digital transformation and regulatory preparedness. The use of AI in fintech for credit scoring and anti-fraud measures is a key driver for software uptake, as local regulators begin to draft national AI strategies modeled after international frameworks.

Middle East & Africa

The Middle East & Africa held a 6.5% share in 2025 (USD 0.18 Billion), with growth concentrated in the UAE and Saudi Arabia. These nations are investing heavily in AI as part of their national vision programs (e.g., Saudi Vision 2030), with a strong focus on creating "smart cities" that require robust ethical AI oversight. Infrastructure development and a shift toward knowledge-based economies are the primary drivers for governance software in these emerging markets, where government entities are the largest early adopters.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software/Platform

- Services

By Deployment

- Cloud

- On-Premise

By Application

- Risk Management

- Compliance Management

- Audit and Reporting

- Model Monitoring and Explainability

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.80 B |

| Forecast Revenue (2034) | USD 18.50 B |

| CAGR (2025-2034) | 23.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software/Platform, Services), By Deployment, (Cloud, On-Premise), By Application, (Risk Management, Compliance Management, Audit and Reporting, Model Monitoring and Explainability) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | IBM CORPORATION, MICROSOFT CORP., ONETRUST, GOOGLE (ALPHABET), DATAROBOT, COLLIBRA, CREDO AI, ARTHUR AI, BIGID, TRUSTIBLE, H2O.AI, FIDDLER AI, MONA LABS, TRUERA, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud, On-Premise), By Application (Risk Management, Compliance Management, Audit & Reporting, Model Monitoring & Explainability) Industry Trends, Competitive Landscape, Regulatory Insights, Market Dynamics & Forecast 2026–2034")

, By Deployment (Cloud, On-Premise), By Application (Risk Management, Compliance Management, Audit & Reporting, Model Monitoring & Explainability) Industry Trends, Competitive Landscape, Regulatory Insights, Market Dynamics & Forecast 2026–2034")

, By Deployment (Cloud, On-Premise), By Application (Risk Management, Compliance Management, Audit & Reporting, Model Monitoring & Explainability) Industry Trends, Competitive Landscape, Regulatory Insights, Market Dynamics & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI Governance and Compliance Software Market?

Global AI governance & compliance software market valued at USD 2.27B in 2024, reaching USD 18.50B by 2034, growing at a CAGR of 23.3% from 2026–2034.

Who are the major players in the AI Governance and Compliance Software Market?

IBM CORPORATION, MICROSOFT CORP., ONETRUST, GOOGLE (ALPHABET), DATAROBOT, COLLIBRA, CREDO AI, ARTHUR AI, BIGID, TRUSTIBLE, H2O.AI, FIDDLER AI, MONA LABS, TRUERA, Others

Which segments covered the AI Governance and Compliance Software Market?

By Offering, (Software/Platform, Services), By Deployment, (Cloud, On-Premise), By Application, (Risk Management, Compliance Management, Audit and Reporting, Model Monitoring and Explainability)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI Governance and Compliance Software Market

Published Date : 08 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date