- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

AI Image Enhancer Market Size, Share & Forecast 2034 | CAGR 34.6%

Global AI Image Enhancer Market Size, Share & Industry Analysis By Solution (Software – Cloud-Based, On-Premise; Services – Implementation & Integration, Consulting & Training, Support & Maintenance), By Type (Real-Time Image Enhancement, Batch Image Enhancement), By Technology (Deep Learning, GAN-Based, Traditional AI), By End-User (Consumer Electronics, Media & Entertainment, Healthcare, Automotive, E-Commerce & Retail) – Market Trends, Competitive Landscape & Forecast 2025–2034

Report Overview

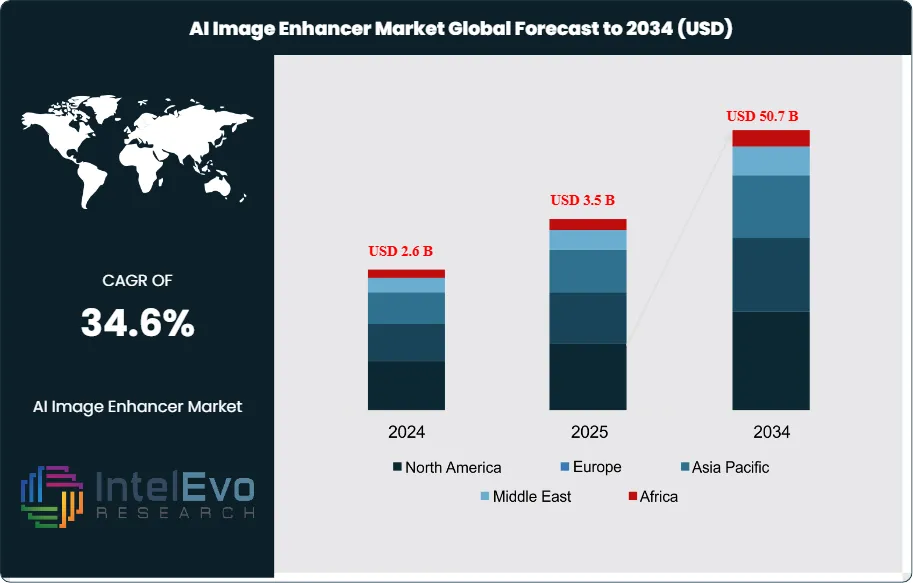

The AI Image Enhancer Market was valued at approximately USD 2.6 billion in 2024 and is projected to reach nearly USD 50.7 billion by 2034, reflecting strong long-term expansion. Based on the projected growth trajectory, the market size for 2025 is estimated at around USD 3.5 billion. Beginning in 2026, the market is expected to grow at a compound annual growth rate (CAGR) of about 34.6% from 2026 to 2034, ultimately achieving a valuation of approximately USD 50.7 billion by 2034.

Get More Information about this report -

Request Free Sample ReportRapid advances in deep learning, computer vision, and cloud infrastructure drive this expansion as enterprises automate image optimization across digital channels. Vendors embed enhancement engines into content management, design, and workflow platforms, which raises processing throughput and lowers manual editing costs. As organizations scale digital assets for omnichannel engagement, demand rises for tools that deliver consistent quality, higher resolution, and improved visual clarity at speed and volume.

The market’s core value proposition lies in its ability to refine details, remove noise, correct exposure, and adapt images to diverse formats with minimal human intervention. Adoption is accelerating in e-commerce and advertising, where enhanced visuals improve click-through rates, conversion, and brand perception. Healthcare providers deploy AI-based enhancement to support diagnostic imaging workflows, while media and entertainment companies apply these tools to remaster content, upscale video, and streamline post-production. This demand side meets a supply base of software firms, cloud hyperscalers, and specialist start-ups that compete on model accuracy, processing latency, integration depth, and pricing flexibility. Data protection rules, AI governance frameworks, and content authenticity regulations shape product design, pushing vendors to incorporate auditability, watermarking, and responsible data practices.

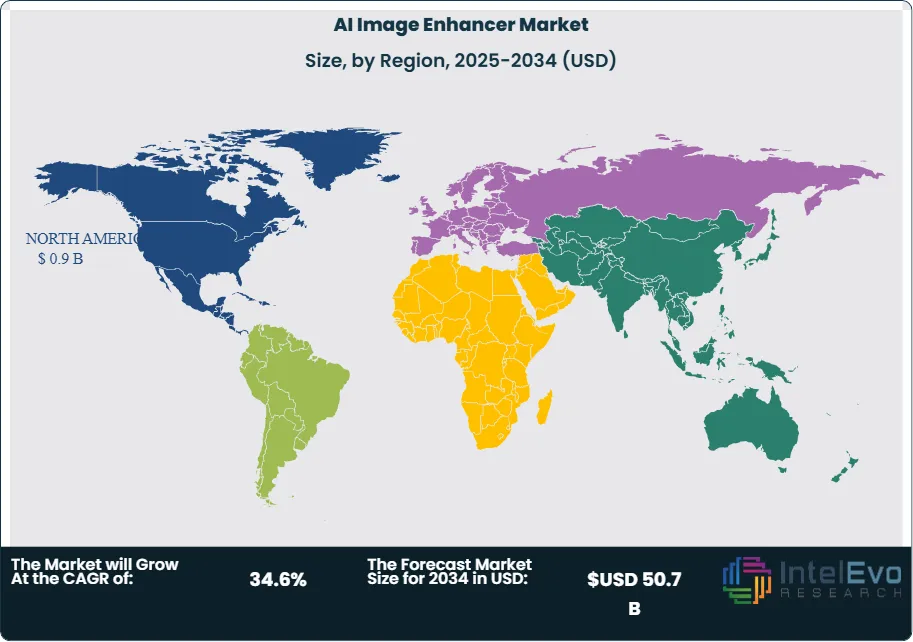

In 2024, North America accounts for about 35.3% of global revenue, or approximately USD 0.9 billion, supported by strong technology infrastructure, high digital ad spend, and early enterprise AI adoption. Europe follows with rising investment in compliant AI solutions, while Asia Pacific emerges as the fastest-growing region, driven by large online retail ecosystems and mobile-first consumers. Key risk factors include bias in training data, IP disputes over generated or altered content, and dependence on third-party cloud platforms. However, continuing advances in generative models, edge deployment, and real-time enhancement capabilities expand use cases across retail, fintech, automotive, and smart cities. Investment activity intensifies in platforms that combine enhancement with asset management, analytics, and workflow orchestration to capture value from end-to-end visual content lifecycles. As budgets shift toward automated content production and personalization, AI image enhancement becomes a foundational layer in the broader digital experience and visual computing stack.

, By Type (Real-Time Image Enhancement, Batch Image Enhancement), By Technology (Deep Learning, GAN-Based, Traditional AI), By End-User (Consumer Electronics, Media & Entertainment, Healthcare, Automotive, E-Commerce & Retail) – Market Trends, Competitive Landscape & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global AI image enhancer market grows from 2.6 billion USD, 2024 to 50.7 billion USD, 2034, reflecting a compound annual growth rate of 34.6%, 2024-2034. This expansion indicates strong monetization of AI-driven visual workflows across industries.

- Segment Dominance : Software solutions lead the offering landscape with a 73.7% revenue share, 2024, as enterprises favor flexible, scalable enhancement tools over hardware-heavy deployments. This dominance supports recurring license and subscription models with estimated: 2.0 billion USD, 2026 in cumulative software billings.

- Segment Dominance: Real-time image enhancement commands 80.5% share, 2024, as customers prioritize instant visual processing for streaming, capture, and in-app experiences. Batch processing solutions retain a smaller but relevant role with estimated: 19.5% share, 2024.

- Driver: Deep learning-based technologies account for 38.8% of deployments, 2024, and drive automation of complex enhancement tasks at scale. Rising integration into consumer devices and platforms could lift deep learning-based penetration to estimated: 55.0%, 2030.

- Restraint: High compute requirements and model deployment costs create barriers for smaller vendors, with an estimated: 0.5 billion USD, 2024 in incremental infrastructure spend across the ecosystem. These cost pressures may compress provider margins by estimated: 5.0%, 2024 in highly competitive segments.

- Opportunity: Consumer electronics holds 28.5% market share, 2024, as smartphones and smart devices embed AI enhancement engines natively. Expansion into mid-range devices and emerging markets could raise this share to estimated: 40.0%, 2030, unlocking new licensing and chipset design opportunities.

- Trend: Vendors shift toward integrated, real-time enhancement pipelines, leveraging 80.5% real-time adoption, 2024 to support live streaming, AR, and social content. Over 2024-2034, platform roadmaps increasingly bundle enhancement with analytics and creation tools, targeting estimated: 60.0% of digital content workflows, 2034.

- Regional Analysis: North America leads with a 35.3% share and 0.9 billion USD revenue, 2024, underpinned by high AI and cloud adoption. Within this, the US contributes 0.78 billion USD, 2024 and advances at a 32.7% CAGR, 2024-2034, while other regions collectively account for an estimated: 1.8 billion USD, 2024 in revenue and catch-up growth potential.

By Solution

The solution landscape continues to tilt strongly toward software as you enter 2025. Software platforms accounted for about 73.7% of global AI image enhancer revenue in 2024 and are projected to retain well above a 70% share through 2030 as adoption deepens across marketing, media, healthcare, and retail workflows. Cloud-based deployment leads within this segment, often representing 60–65% of software revenue, as organizations prefer browser-based access, elastic compute, and rapid feature updates. On-premise software still plays a role in sectors such as healthcare, banking, and public safety, where data residency and latency remain critical; here you see more controlled rollouts and longer upgrade cycles.

Services form a smaller but faster-growing part of the market. Implementation and integration services expand at an estimated CAGR of 20–25% from 2025 to 2030 as enterprises tie AI image enhancement into content management, DAM platforms, and creative suites. Consulting and training services help your teams standardize workflows, manage change, and set governance rules for AI use, particularly in regulated industries. Support and maintenance contracts also gain importance as you scale models across regions and devices, with recurring service revenue increasingly bundled into multi-year software agreements.

By Type

Real-time image enhancement dominates the market as of 2024, with an estimated 80.5% share, and is expected to remain the primary growth engine through 2030. This type supports live streaming, social video, virtual events, and interactive commerce, where your customers expect sharp, well-lit visuals in milliseconds. As 5G and fiber broadband expand, more platforms embed live enhancement directly into cameras, conferencing tools, and streaming pipelines, driving double-digit growth in this segment.

Batch image enhancement continues to serve critical use cases, particularly in large-scale content libraries and archival processes. You see it applied in media restoration, bulk product catalog updates, insurance claims processing, and satellite imagery. While batch workloads grow more slowly, often in the high single digits annually, they remain important where you need consistent quality for high volumes of images processed overnight or in scheduled workflows. Many vendors now offer hybrid models that combine real-time processing at the edge with batch jobs in the cloud to align with your operational and cost priorities.

By Technology

Deep learning-based enhancers held around 38.8% share in 2024 and set the technical benchmark for image quality. Convolutional neural networks and transformer-based models now deliver strong gains in sharpness, noise reduction, and low-light performance with minimal manual tuning. As training datasets expand and model architectures improve, you can expect deep learning to approach or exceed 50% share by 2030, especially in high-value segments like healthcare imaging, premium consumer devices, and professional content production.

Traditional AI image enhancement, including rule-based and classical computer vision approaches, retains relevance in constrained environments. These methods often require less compute and suit lower-cost devices or applications with strict latency and reliability requirements. At the same time, Generative Adversarial Networks and related generative models grow quickly from a smaller base. They support advanced use cases such as super-resolution, smart inpainting, and style transfer for retail, entertainment, and design. By 2030, GAN-based solutions could account for 20–25% of technology share, particularly in your applications that focus on creative quality and personalization.

By End-User Industry

Consumer electronics remains the largest end-user segment, with about 28.5% share in 2024, and continues to set expectations for visual quality in 2025 and beyond. Smartphone makers, PC vendors, smart TV brands, and camera manufacturers embed AI image enhancers directly into devices to improve low-light shots, video calls, and real-time filters. As unit shipments of AI-capable smartphones and connected devices grow, you can expect this segment to maintain a strong mid-20s to low-30s percentage share over the next five years.

E-commerce and retail represent another core growth area as your product teams seek higher conversion rates and reduced content production costs. AI image enhancers support consistent product imagery, automated background cleaning, and rapid adaptation of visuals for different channels and regions. Automotive, including in-cabin monitoring and advanced driver assistance systems, adds further demand for robust, low-latency enhancement. Other industries, such as healthcare, security, and industrial inspection, contribute a growing share as you adapt AI imaging to specialized operational requirements.

By Region

North America led the market in 2024 with roughly 35.3% share and around 0.9 billion USD in revenue, supported by strong investment from technology companies and early enterprise adoption. The United States remains the anchor market, with large installed bases in cloud infrastructure, creative software, and digital media. As you plan for 2025–2030, North America is expected to sustain a high-teens CAGR, driven by expanded use across marketing, streaming, and healthcare imaging.

Europe follows with a sizeable share, supported by demand from media, automotive, and industrial firms, but it grows within a stricter regulatory environment focused on AI transparency and data protection. Asia Pacific emerges as the fastest-growing region, often projected to expand at above 20% CAGR through 2030, powered by large online marketplaces, social commerce platforms, and high smartphone penetration in China, India, and Southeast Asia. Latin America and the Middle East & Africa start from smaller bases but show rising adoption as connectivity improves and local content ecosystems mature, giving you a set of emerging markets with strong medium-term upside.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Solution

- Software

- Cloud-Based

- On-Premise

- Services

- Implementation & Integration Services

- Consulting & Training Services

- Support & Maintenance Services

By Type

- Real-Time Image Enhancement

- Batch Image Enhancement

By Technology

- Deep Learning-Based Enhancers

- Traditional AI Image Enhancement

- Generative Adversarial Networks (GANs)

- Others

By End-User Industry

- Consumer Electronics

- Media and Entertainment

- Healthcare

- Automotive

- E-Commerce and Retail

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.5 B |

| Forecast Revenue (2034) | USD 50.7 B |

| CAGR (2025-2034) | 34.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Solution (Software, Services), By Type (Real-Time Image Enhancement, Batch Image Enhancement), By Technology (Deep Learning-Based Enhancers, Traditional AI Image Enhancement, Generative Adversarial Networks (GANs), Others), By End-User Industry (Consumer Electronics, Media and Entertainment, Healthcare, Automotive, E-Commerce and Retail, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Movavi Software, Lets Enhance, Prisma Data, PixBim, Bigjpg, Meero, Icons8, Upscale.media, VanceAI Technology, NETFLAIRS TECHNOLOGY, Leawo Software, PIXLR (INMAGINE), DEEP-IMAGE.AI, Topaz Labs, RADIUS5, HitPaw, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Type (Real-Time Image Enhancement, Batch Image Enhancement), By Technology (Deep Learning, GAN-Based, Traditional AI), By End-User (Consumer Electronics, Media & Entertainment, Healthcare, Automotive, E-Commerce & Retail) – Market Trends, Competitive Landscape & Forecast 2025–2034")

, By Type (Real-Time Image Enhancement, Batch Image Enhancement), By Technology (Deep Learning, GAN-Based, Traditional AI), By End-User (Consumer Electronics, Media & Entertainment, Healthcare, Automotive, E-Commerce & Retail) – Market Trends, Competitive Landscape & Forecast 2025–2034")

, By Type (Real-Time Image Enhancement, Batch Image Enhancement), By Technology (Deep Learning, GAN-Based, Traditional AI), By End-User (Consumer Electronics, Media & Entertainment, Healthcare, Automotive, E-Commerce & Retail) – Market Trends, Competitive Landscape & Forecast 2025–2034")

Frequently Asked Questions

How big is the AI Image Enhancer Market?

The AI Image Enhancer Market was valued at USD 2.6 Billion in 2024 and is projected to reach USD 50.7 Billion by 2034, growing at a CAGR of 34.6%. The market is estimated at USD 3.5 Billion in 2025, driven by rising demand for AI-powered image upscaling, restoration, and real-time enhancement solutions.

Who are the major players in the AI Image Enhancer Market?

Movavi Software, Lets Enhance, Prisma Data, PixBim, Bigjpg, Meero, Icons8, Upscale.media, VanceAI Technology, NETFLAIRS TECHNOLOGY, Leawo Software, PIXLR (INMAGINE), DEEP-IMAGE.AI, Topaz Labs, RADIUS5, HitPaw, Others

Which segments covered the AI Image Enhancer Market?

By Solution (Software, Services), By Type (Real-Time Image Enhancement, Batch Image Enhancement), By Technology (Deep Learning-Based Enhancers, Traditional AI Image Enhancement, Generative Adversarial Networks (GANs), Others), By End-User Industry (Consumer Electronics, Media and Entertainment, Healthcare, Automotive, E-Commerce and Retail, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date