- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

AI in Art and Creativity Market Size, Share & Forecast | CAGR 28.7%

Global AI in Art and Creativity Market Size, Share, Analysis By Component (Software, Services), By Technology (Generative Adversarial Networks, Transformer-Based Models, Neural Style Transfer, AI-Assisted Design Tools), By Application (Image Generation, Music, Writing, Video, Game Design), By End-User, Deployment Mode, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

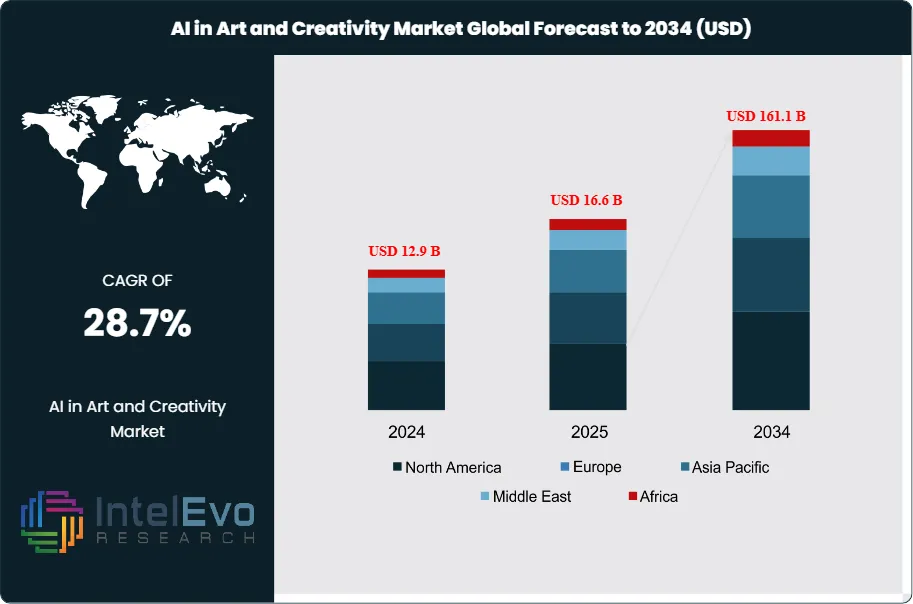

| USD 16.6 Billion | USD 161.1 Billion | 28.7% | North America, 34.26% |

The Global AI in Art and Creativity Market was valued at approximately USD 12.9 Billion in 2024 and USD 16.6 Billion in 2025 and is projected to reach nearly USD 161.1 Billion by 2034, expanding at a compound annual growth rate (CAGR) of around 28.7% during the forecast period from 2026 to 2034. This rapid growth is driven by the increasing adoption of generative AI tools in digital content creation, rising demand for automated design and media production, and expanding use of AI across entertainment, gaming, advertising, and creative industries. Additionally, advancements in machine learning models and growing creator economy platforms are further accelerating market expansion globally.

Get More Information about this report -

Request Free Sample ReportThis market covers AI-native and AI-assisted tools that generate or refine images, video, music, copy, and interactive media across professional studios, prosumers, and enterprises. Demand concentrates in marketing, gaming, film/animation, and e-commerce content operations that need faster iteration, more variants, and consistent brand execution across channels. Enterprises account for an estimated 45% of 2024 spending, driven by campaign localization and always-on content calendars. Supply is led by foundation-model providers, creative software suites, and platform marketplaces that embed generation into workflows, with pricing models shifting toward usage-based credits and seat-plus-consumption hybrids as adoption expands.

Model capability improvements remain the primary accelerator. OpenAI’s March 2025 launch of GPT-4o image generation highlighted sharper text rendering, stronger prompt adherence, and better multi-turn refinement, which directly supports design, diagramming, and production-grade creative iteration.

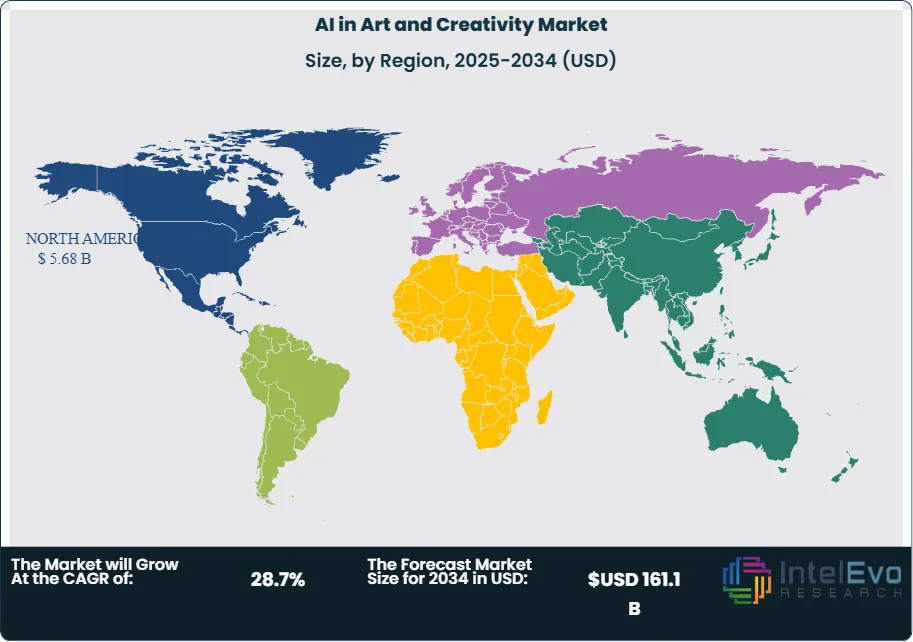

North America remains the largest revenue pool, holding over 34.26% share; on a 2024 basis, this implies roughly USD 4.4 billion in regional revenue, supported by dense creator ecosystems, high cloud spend, and early enterprise procurement. Europe follows with policy-driven demand for governance features, while Asia-Pacific is the fastest-growing region, supported by mobile-first creator economies and expanding media-tech investment in India, Southeast Asia, and South Korea; APAC’s share is plausibly on track to rise from about 24% in 2024 to ~30% by 2034 as localization and creator monetization scale. Key risks include copyright and training-data disputes, brand-safety exposure, deepfake-enabled fraud, and GPU-linked cost volatility, which can compress margins for smaller platforms. Over the forecast, winners are likely to pair strong models with rights-aware data strategies, enterprise-grade controls, and integrated automation that reduces end-to-end creative cycle time without sacrificing quality.

, By Technology (Generative Adversarial Networks, Transformer-Based Models, Neural Style Transfer, AI-Assisted Design Tools), By Application (Image Generation, Music, Writing, Video, Game Design), By End-User, Deployment Mode, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The U.S. market reached 5.02 billion USD, 2025 and sustained 22.3% CAGR, 2024-2034 on creator-economy expansion and rapid AI innovation.

- Segment Dominance: Software led adoption with 89.3%, 2025 as organizations standardized on AI-driven creative platforms and tooling.

- Segment Dominance: Visual art and image generation captured 61.8%, 2025 and transformer-based models led with 52.7%, 2025 due to superior generative performance.

- Driver: Cloud-based deployment secured 83.5%, 2025 as teams scaled production with faster provisioning and lower infrastructure friction.

- Restraint: Rights management and compliance uncertainty constrained enterprise rollouts at estimated: 14.0% of projects delayed, 2025.

- Opportunity: Vendors can monetize professional workflows where creators accounted for 42.6%, 2025, with estimated: 3.6 billion USD, 2024 incremental spend tied to licensing-safe generation and brand controls.

- Trend: Platforms prioritized multimodal generation and rapid iteration, with transformer adoption at 52.7%, 2025 and estimated: 2.0x faster creative cycle times, 2025.

- Regional Analysis: North America held 34.3%, 2025 share, supported by mature AI ecosystems and investment depth, translating to estimated: 4.4 billion USD, 2024 regional revenue.

Competitive Landscape

The Global AI in Art and Creativity Market is moderately concentrated, with the top five technology platforms and tool providers accounting for an estimated 45.0%–52.0% of 2025 market revenue. Competition is innovation-driven and ecosystem-based, with model performance, creator adoption, platform integration, and data scale shaping market share more than pricing. Competitive intensity accelerated in 2025–2026 as companies expanded multimodal AI capabilities, integrated tools into creative workflows, and formed partnerships across media, gaming, and enterprise content platforms.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| OPENAI | US | Leader | Generative AI models (DALL·E, GPT-based creative tools) | North America, Europe, Global SaaS | Expanded multimodal creative capabilities and API ecosystem integrations in 2025. |

| ADOBE | US | Leader | Firefly AI, Creative Cloud AI integration for design and media | North America, Europe, Enterprise global | Deepened AI integration across Photoshop, Illustrator, and video tools in 2025. |

| GOOGLE (DEEPMIND) | US/UK | Leader | Imagen, Gemini multimodal AI for creative generation | Global | Advanced multimodal AI models and integrated generative tools into Workspace and YouTube in 2025. |

| MICROSOFT | US | Leader | Copilot, Designer, AI-powered creative and productivity tools | North America, Europe, Enterprise | Expanded Copilot across creative and enterprise platforms with OpenAI integration in 2025. |

| MIDJOURNEY | US | Challenger | AI image generation platform for artists and designers | North America, Global creator community | Released new high-fidelity image models and expanded subscription base in 2025. |

| RUNWAY AI | US | Challenger | AI video generation and editing tools for creators | North America, Media industry | Launched Gen-3 video models and partnered with studios in 2025. |

| STABILITY AI | UK | Challenger | Stable Diffusion open-source generative models | Europe, Global developer ecosystem | Focused on enterprise licensing and open model improvements in 2025. |

| CANVA | Australia | Challenger | AI-powered design tools for mass-market creators | Asia-Pacific, Global SMBs | Expanded Magic Design and AI editing tools across platform in 2025. |

| NVIDIA | US | Niche Player | AI infrastructure, generative models, Omniverse for creative workflows | Global | Strengthened AI hardware-software stack for creative industries in 2025. |

| SHUTTERSTOCK | US | Niche Player | AI-generated content platform and licensed datasets | North America, Europe | Expanded AI-generated media marketplace and partnerships with model providers in 2025. |

By Component

Software continues to define the AI in art and creativity market structure in 2025, accounting for approximately 89.3% of total adoption. Creative value delivery is concentrated in digital platforms that support ideation, generation, editing, and refinement of visual, audio, and multimedia content. Software-led tools appeal to creators because they allow rapid experimentation, iterative design, and immediate output without dependence on dedicated hardware environments.

This dominance reflects broad compatibility across devices and operating systems, which allows artists and enterprises to embed AI directly into existing creative workflows. Continuous software updates expand model capabilities and feature depth, supporting sustained usage across professional and commercial contexts. Lower entry costs compared to hardware-based solutions further reinforce software preference among independent creators and small studios.

In late 2025, Adobe expanded Firefly capabilities across its Creative Cloud suite by introducing AI avatar creation and sound effect generation. Tight integration with Photoshop and Illustrator enabled commercially safe visual production, strengthening Adobe’s position in professional-grade creative software and reinforcing software’s central role in AI-driven creativity.

By Technology

Transformer-based models remain the leading technological foundation in 2025, representing about 52.7% of total technology adoption. These architectures enable strong contextual understanding of prompts, styles, and compositional structure, which is critical for high-quality creative output. Their ability to maintain consistency across complex visual and narrative elements has positioned transformers as the preferred choice for advanced generative tasks.

Adoption growth is supported by steady improvements in model efficiency, interpretability, and output reliability. Creators benefit from finer control over style, layout, and thematic coherence, particularly in professional design and media production. Ongoing refinement of transformer architectures sustains their relevance across both visual and multimodal creative use cases.

In September 2025, Stability AI expanded commercial licensing for transformer-based foundations in Stable Diffusion 3. Creators reported improved image coherence and stronger stylistic control, supporting wider enterprise acceptance of transformer-driven creative pipelines.

By Application

Visual art and image generation dominate application demand in 2025, capturing roughly 61.8% of total market usage. AI tools support illustration, concept art, branding visuals, and digital artwork at speed and scale. Automation reduces manual production time and enables creators to explore multiple design variations within compressed timelines.

Growth in this segment aligns with rising demand for digital content across advertising, social media, gaming, and immersive media. Visual AI tools enable rapid prototyping and stylistic experimentation, which supports both commercial efficiency and artistic exploration. Image generation remains the primary entry point for creators adopting AI.

In March 2025, Runway introduced Gen-4, delivering consistent characters and environments for high-fidelity image and video creation. Designers and filmmakers adopted the platform for narrative-driven visuals, reinforcing visual generation as the core AI application.

By End-Use

Professional artists and creators account for approximately 42.6% of total usage in 2025, reflecting growing acceptance of AI as a creative co-production tool. These users demand precision, customization, and quality control, integrating AI into established workflows rather than replacing manual craft. AI supports concept development, refinement, and production efficiency.

Adoption among professionals is driven by time savings and expanded creative range. Advanced users prioritize tools that respect artistic intent and originality while enabling faster execution. Consistent professional demand supports continued platform investment in creator-focused features.

In November 2025, Runway released Gen-4.5, which professional artists praised for improved motion fidelity and cinematic control. The update enabled complex visual storytelling and reinforced AI’s role as a productivity enhancer for professionals.

By Region

North America remains the leading regional market in 2025, holding approximately 34.26% of global share. The region benefits from a dense concentration of creative professionals, advanced cloud infrastructure, and strong investment in AI platforms. High adoption across media, advertising, and digital content sectors sustains regional leadership.

The United States reached about USD 5.02 billion in market value in 2025, expanding at a CAGR of roughly 22.33%. Growth is driven by creator economy expansion, enterprise content demand, and rapid integration of AI into creative software. Investment momentum remains strong across startups and established platforms.

In March 2025, OpenAI launched native image generation within GPT-4o, enabling photorealistic visuals, consistent styles, and multi-step editing. This development underscored U.S. leadership in AI-powered creative tools and reinforced North America’s influence on global market direction.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software

- Services

By Technology

- Generative Adversarial Networks (GANs)

- Transformer-based Models

- Neural Style Transfer

- Creative Coding & AI-assisted Design Tools

- Others

By Application

- Visual Art & Image Generation

- Music & Audio Composition

- Writing & Story Generation

- Video & Animation Creation

- Game Asset & Design Creation

- Others

By End-User

- Professional Artists & Creators

- Media & Entertainment Companies

- Advertising & Marketing Agencies

- Hobbyists & Enthusiasts

By Deployment Mode

- Cloud-based

- On-premises

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 16.6 B |

| Forecast Revenue (2034) | USD 161.1 B |

| CAGR (2025-2034) | 28.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Software, Services), By Technology, (Generative Adversarial Networks (GANs), Transformer-based Models, Neural Style Transfer, Creative Coding & AI-assisted Design Tools, Others), By Application, (Visual Art & Image Generation, Music & Audio Composition, Writing & Story Generation, Video & Animation Creation, Game Asset & Design Creation, Others), By End-User, (Professional Artists & Creators, Media & Entertainment Companies, Advertising & Marketing Agencies, Hobbyists & Enthusiasts), By Deployment Mode, (Cloud-based, On-premises) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Adobe, Inc., Runway ML, Inc., AIVA Technologies SA, Nvidia Corporation, Writesonic, Ltd., OpenAI, L.L.C., Shutterstock, Inc., Artbreeder, Jasper, Inc., Stability AI, Ltd., DeepDream Generator, Midjourney, Inc., Others, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Generative Adversarial Networks, Transformer-Based Models, Neural Style Transfer, AI-Assisted Design Tools), By Application (Image Generation, Music, Writing, Video, Game Design), By End-User, Deployment Mode, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

, By Technology (Generative Adversarial Networks, Transformer-Based Models, Neural Style Transfer, AI-Assisted Design Tools), By Application (Image Generation, Music, Writing, Video, Game Design), By End-User, Deployment Mode, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

, By Technology (Generative Adversarial Networks, Transformer-Based Models, Neural Style Transfer, AI-Assisted Design Tools), By Application (Image Generation, Music, Writing, Video, Game Design), By End-User, Deployment Mode, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI in Art and Creativity Market?

The Global AI in Art and Creativity Market was valued at USD 16.6 Billion in 2025 and is projected to reach USD 161.1 Billion by 2034, growing at a CAGR of 28.7% from 2026–2034, driven by generative AI adoption, digital content demand, and growth in creative industries and platforms.

Who are the major players in the AI in Art and Creativity Market?

Adobe, Inc., Runway ML, Inc., AIVA Technologies SA, Nvidia Corporation, Writesonic, Ltd., OpenAI, L.L.C., Shutterstock, Inc., Artbreeder, Jasper, Inc., Stability AI, Ltd., DeepDream Generator, Midjourney, Inc., Others,

Which segments covered the AI in Art and Creativity Market?

By Component (Software, Services), By Technology, (Generative Adversarial Networks (GANs), Transformer-based Models, Neural Style Transfer, Creative Coding & AI-assisted Design Tools, Others), By Application, (Visual Art & Image Generation, Music & Audio Composition, Writing & Story Generation, Video & Animation Creation, Game Asset & Design Creation, Others), By End-User, (Professional Artists & Creators, Media & Entertainment Companies, Advertising & Marketing Agencies, Hobbyists & Enthusiasts), By Deployment Mode, (Cloud-based, On-premises)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI in Art and Creativity Market

Published Date : 23 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date