- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

AI in Mental Health Market Size, Growth Analysis | CAGR 18.1%

Global AI in Mental Health Market Size, Share & Trends Report by Technology (Machine Learning, NLP, Computer Vision, Digital Phenotyping, Predictive Analytics), Component (Software, Apps, Tools, Wearables, Services), End-User (Providers, Payers, D2C, Employers, Institutions), Condition (Depression, Anxiety, PTSD, Bipolar, Substance Use), Region & Key Players – Market Overview, Dynamics, Trends & Forecast 2025–2034

Report Overview

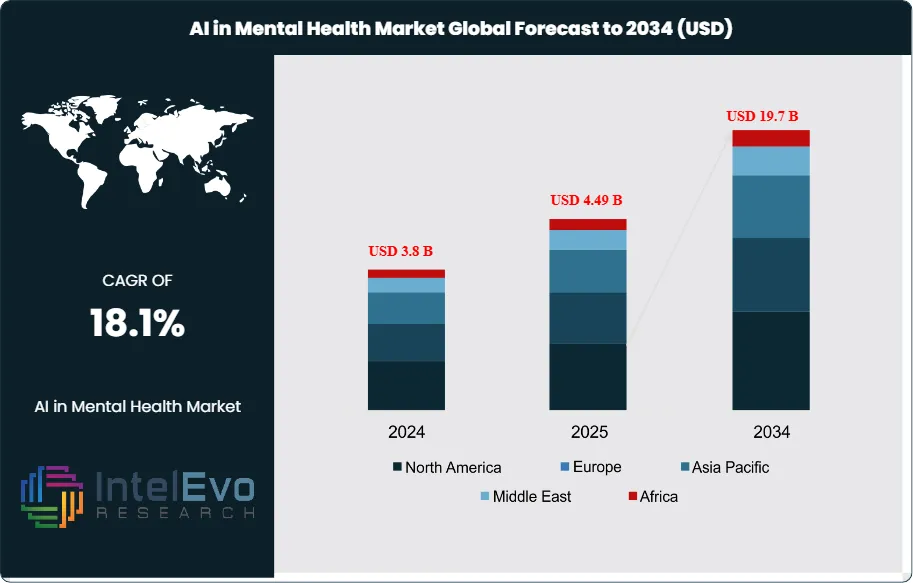

The AI in Mental Health Market size is expected to be worth around USD 19.7 Billion by 2034, up from USD 3.8 Billion in 2024, growing at a CAGR of 18.1% during the forecast period from 2024 to 2034. The AI in Mental Health market encompasses a broad ecosystem of digital solutions, platforms, and services that leverage artificial intelligence, machine learning, and advanced analytics to support mental health assessment, diagnosis, treatment, and ongoing care.

Get More Information about this report -

Request Free Sample ReportThis market includes AI-powered chatbots, virtual therapists, predictive analytics platforms, digital phenotyping tools, and integrated telehealth services designed to serve diverse mental health needs across clinical, community, and consumer settings. The ecosystem addresses a wide range of mental health conditions, including depression, anxiety, bipolar disorder, PTSD, substance use disorders, and more, enabling early detection, personalized intervention, and continuous monitoring.

The AI in Mental Health market is experiencing robust growth driven by the global mental health crisis, rising demand for accessible and scalable care, and the integration of AI into digital health platforms. Key growth catalysts include the proliferation of smartphones and wearable devices, advances in natural language processing (NLP) and sentiment analysis, and the increasing acceptance of telepsychiatry and digital therapeutics. The market benefits from growing awareness of mental health issues, the destigmatization of seeking help, and the need for cost-effective, data-driven solutions that can bridge gaps in traditional mental health care delivery.

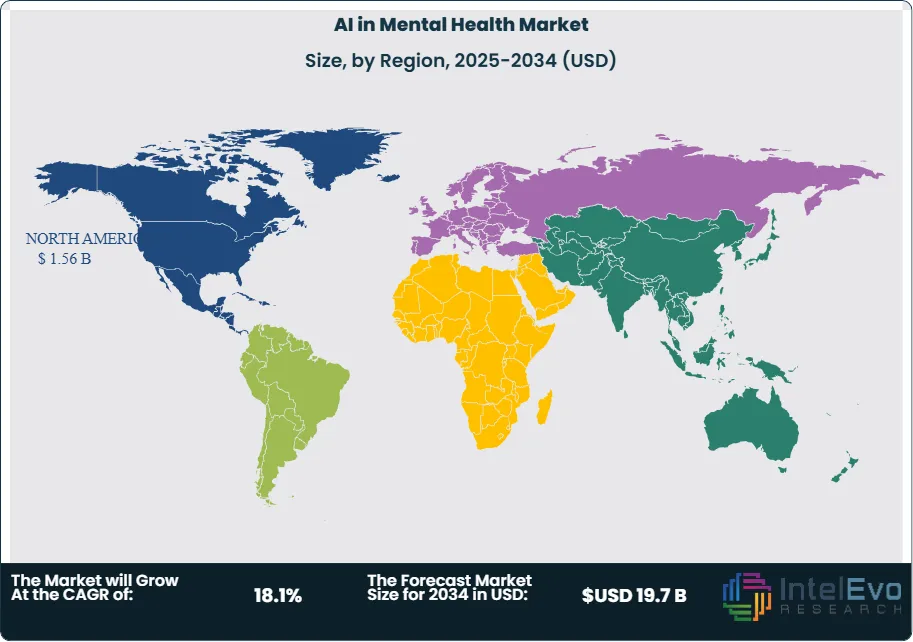

North America maintains its position as the leading regional market for AI in mental health, commanding the largest global market share and generating the highest revenues within the sector. This dominance is attributed to early adoption of digital health technologies, a well-established mental health care infrastructure, and significant investments in AI research and development. The United States serves as the primary contributor to North America's market leadership, with substantial revenue generation and strong growth projections driven by robust adoption rates. Meanwhile, the Asia-Pacific region emerges as the most rapidly expanding market segment, propelled by increasing mental health awareness, expanding digital infrastructure, and governmental policies that actively encourage the implementation of AI-driven health solutions.

The COVID-19 pandemic accelerated digital transformation initiatives across the mental health sector as individuals, providers, and organizations sought remote support and automated tools to address rising mental health needs during lockdowns and social distancing measures. The crisis highlighted the importance of AI-enabled systems for ensuring continuity of care, enabling remote assessment, and reducing dependency on in-person visits. While initial regulatory and privacy concerns posed challenges, the long-term impact has been positive, with increased recognition of digital technologies' value in expanding access and improving outcomes.

Rising demand for personalized care, workforce shortages in mental health professions, and the need for real-time monitoring and intervention have significantly influenced AI adoption patterns. International collaborations, public-private partnerships, and growing investment in mental health innovation are further accelerating market growth. Additionally, increasing focus on data privacy, ethical AI, and regulatory compliance is shaping the development and deployment of AI solutions in mental health.

, Component (Software, Apps, Tools, Wearables, Services), End-User (Providers, Payers, D2C, Employers, Institutions), Condition (Depression, Anxiety, PTSD, Bipolar, Substance Use), Region & Key Players – Market Overview, Dynamics, Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The AI in Mental Health Market is expected to reach USD 19.7 Billion by 2034, fueled by growing demand for accessible, scalable, and personalized mental health care, driven by advances in AI, digital therapeutics, and telehealth integration.

- Technology Dominance: Machine Learning and Natural Language Processing (NLP) lead the segment, due to their foundational role in AI-powered assessment, diagnosis, and conversational support.

- Component Dominance: Software platforms dominate the segment, driven by the essential role of digital tools in delivering AI-enabled mental health services.

- End-User Dominance: Healthcare providers and payers lead the end-user segment, primarily due to their investment capacity and need for scalable, data-driven care solutions.

- Condition Dominance: Depression and anxiety disorders hold the largest share, owing to their high prevalence and broad application scope for AI-driven screening and intervention.

- Driver: Key drivers accelerating growth include the global mental health crisis, workforce shortages, and the need for cost-effective, scalable care delivery.

- Restraint: Growth is hindered by data privacy concerns, regulatory complexity, and the need for clinical validation of AI tools.

- Opportunity: The market is poised for expansion due to opportunities like integration with wearable devices, development of multilingual AI models, and emerging market penetration.

- Trend: Emerging trends including digital phenotyping, real-time monitoring, and explainable AI are reshaping the market by enabling proactive, personalized, and transparent mental health care.

- Regional Analysis: North America leads owing to early technology adoption and established mental health infrastructure. Asia-Pacific shows high promise due to rapid digitalization and increasing mental health awareness.

Technology Analysis

Machine Learning and NLP Lead the Segment: Machine learning and natural language processing (NLP) technologies stand out as the leading force, serving as the essential infrastructure backbone that supports AI deployments in mental health care. These technologies enable automated assessment of speech, text, and behavioral data, supporting early detection of mental health conditions, risk stratification, and personalized intervention. The prominent role of machine learning and NLP is driven by ongoing advancements in sentiment analysis, emotion recognition, and conversational AI, all of which are crucial for enabling sophisticated digital mental health solutions.

Other enabling technologies include computer vision (for facial expression analysis), digital phenotyping (using smartphone and wearable data), and predictive analytics platforms that support real-time risk assessment and intervention.

Component Analysis

Software Platforms Dominate the Market: Software platforms hold a leading position in the market, highlighting their vital role in delivering AI-enabled mental health services. This category includes mobile apps, web-based platforms, virtual therapy tools, and integrated telehealth solutions that facilitate assessment, monitoring, and intervention. The prominence of software is driven by the growing need for scalable, user-friendly, and continuously updated digital tools that can reach diverse populations and support a wide range of mental health needs.

Hardware components, such as wearables and biosensors, are increasingly integrated with software platforms to enable real-time monitoring of physiological and behavioral indicators relevant to mental health.

End-User Analysis

Healthcare Providers and Payers Lead the Segment: Healthcare providers (including hospitals, clinics, and telehealth platforms) and payers (insurance companies, government agencies) dominate the market, reflecting their central role in delivering and reimbursing mental health care. These organizations have the financial capacity, technical knowledge, and regulatory responsibility to deploy AI solutions at scale, while also contending with the most rigorous clinical validation and data privacy requirements.

Direct-to-consumer (D2C) platforms and employers are rapidly adopting AI in mental health to support employee well-being, reduce absenteeism, and improve productivity. Educational institutions and community organizations are also emerging as important end-users, leveraging AI tools for early intervention and support.

Condition Analysis

Depression and Anxiety Disorders Lead the Market: Depression and anxiety disorders hold a leading position in the market, driven by their high prevalence, significant impact on quality of life, and broad application scope for AI-driven screening, monitoring, and intervention. AI-powered chatbots, digital cognitive behavioral therapy (CBT) tools, and sentiment analysis platforms are widely used to support individuals with depression and anxiety, providing accessible, stigma-free support and early detection.

Other key conditions addressed by AI in mental health include bipolar disorder, PTSD, substance use disorders, eating disorders, and schizophrenia. The versatility of AI tools enables tailored interventions for diverse mental health needs, supporting both acute and chronic care.

Region Analysis

North America Leads, Asia-Pacific Fastest-Growing: North America stands as the clear leader in the global AI in mental health market, supported by its highly advanced digital health infrastructure, proactive adoption of AI technologies, and significant investments by major healthcare organizations and technology companies. The region boasts a mature network of AI solution providers, robust research and development capabilities, and long-standing public-private partnerships that drive innovation and deployment of AI solutions across mental health care.

The United States, in particular, plays a pivotal role in shaping industry trends due to its focus on integrating AI into telepsychiatry, digital therapeutics, and population health management. Canada also demonstrates strong growth, supported by government initiatives and a focus on mental health innovation.

In contrast, the Asia-Pacific region is experiencing the fastest market growth, fueled by rapid digitalization, increasing mental health awareness, and strong government policies championing digital health. Countries such as China, India, Japan, and Australia are at the forefront of this expansion, with many organizations accelerating the adoption of AI-powered mental health platforms to address workforce shortages and improve access to care.

Europe continues to maintain a substantial presence through well-established healthcare systems, regulatory frameworks, and a focus on data privacy and ethical AI. The region's adoption of AI in mental health is significantly influenced by public health initiatives, cross-border collaborations, and the active involvement of leading technology providers.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

Technology

- Machine Learning

- Natural Language Processing (NLP)

- Computer Vision

- Digital Phenotyping

- Predictive Analytics

Component

- Software Platforms

- Mobile Apps

- Web-Based Tools

- Wearables & Biosensors

- Services

End-User

- Healthcare Providers

- Payers (Insurance, Government)

- Direct-to-Consumer (D2C)

- Employers

- Educational Institutions

- Community Organizations

Condition

- Depression

- Anxiety Disorders

- Bipolar Disorder

- PTSD

- Substance Use Disorders

- Eating Disorders

- Schizophrenia

Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.49 B |

| Forecast Revenue (2034) | USD 19.7 B |

| CAGR (2025-2034) | 18.1% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Technology (Machine Learning, Natural Language Processing (NLP), Computer Vision, Digital Phenotyping, Predictive Analytics),Component (Software Platforms, Mobile Apps, Web-Based Tools, Wearables & Biosensors, Services),End-User, (Healthcare Providers, Payers (Insurance, Government), Direct-to-Consumer (D2C), Employers, Educational Institutions, Community Organizations),Condition, (Depression, Anxiety Disorders, Bipolar Disorder, PTSD, Substance Use Disorders, Eating Disorders, Schizophrenia) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Woebot Health, Headspace Health (Ginger), Wysa, Spring Health, Quartet Health, Lyra Health, Mindstrong Health, Talkspace, BetterHelp, IBM Watson Health, Eleos Health, Limbix, SilverCloud Health, MindDoc Health, Ada Health |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Component (Software, Apps, Tools, Wearables, Services), End-User (Providers, Payers, D2C, Employers, Institutions), Condition (Depression, Anxiety, PTSD, Bipolar, Substance Use), Region & Key Players – Market Overview, Dynamics, Trends & Forecast 2025–2034")

, Component (Software, Apps, Tools, Wearables, Services), End-User (Providers, Payers, D2C, Employers, Institutions), Condition (Depression, Anxiety, PTSD, Bipolar, Substance Use), Region & Key Players – Market Overview, Dynamics, Trends & Forecast 2025–2034")

, Component (Software, Apps, Tools, Wearables, Services), End-User (Providers, Payers, D2C, Employers, Institutions), Condition (Depression, Anxiety, PTSD, Bipolar, Substance Use), Region & Key Players – Market Overview, Dynamics, Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the AI in Mental Health Market?

The global AI in mental health market is projected to grow from USD 3.8 billion in 2024 to USD 19.7 billion by 2034, expanding at a CAGR of 18.1%. Explore key drivers and trends.

Who are the major players in the AI in Mental Health Market?

Woebot Health, Headspace Health (Ginger), Wysa, Spring Health, Quartet Health, Lyra Health, Mindstrong Health, Talkspace, BetterHelp, IBM Watson Health, Eleos Health, Limbix, SilverCloud Health, MindDoc Health, Ada Health

Which segments covered the AI in Mental Health Market?

Technology (Machine Learning, Natural Language Processing (NLP), Computer Vision, Digital Phenotyping, Predictive Analytics),Component (Software Platforms, Mobile Apps, Web-Based Tools, Wearables & Biosensors, Services),End-User, (Healthcare Providers, Payers (Insurance, Government), Direct-to-Consumer (D2C), Employers, Educational Institutions, Community Organizations),Condition, (Depression, Anxiety Disorders, Bipolar Disorder, PTSD, Substance Use Disorders, Eating Disorders, Schizophrenia)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date