- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

AI in Oil and Gas Exploration Market Size, Share & Growth | CAGR 12.6%

Global AI in Oil and Gas Exploration Market Size, Share & Industry Analysis By Offering (Software, Services, Hardware), By Technology (Machine Learning, Deep Learning and Neural Networks, Natural Language Processing, Computer Vision, Other Technologies including Reinforcement Learning and Federated Learning), By Application (Seismic Data Interpretation, Reservoir Characterization & Modeling, Drilling Optimization, Production Forecasting, Environmental & Supply Chain Analytics), By Deployment Mode (Cloud-Based, On-Premise, Edge Deployment), By End-User (International Oil Companies, National Oil Companies, Independent Operators, Oilfield Service Companies) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size, 2025 | Forecast Value, 2034 | CAGR, 2026-2034 | Leading Region, 2025 |

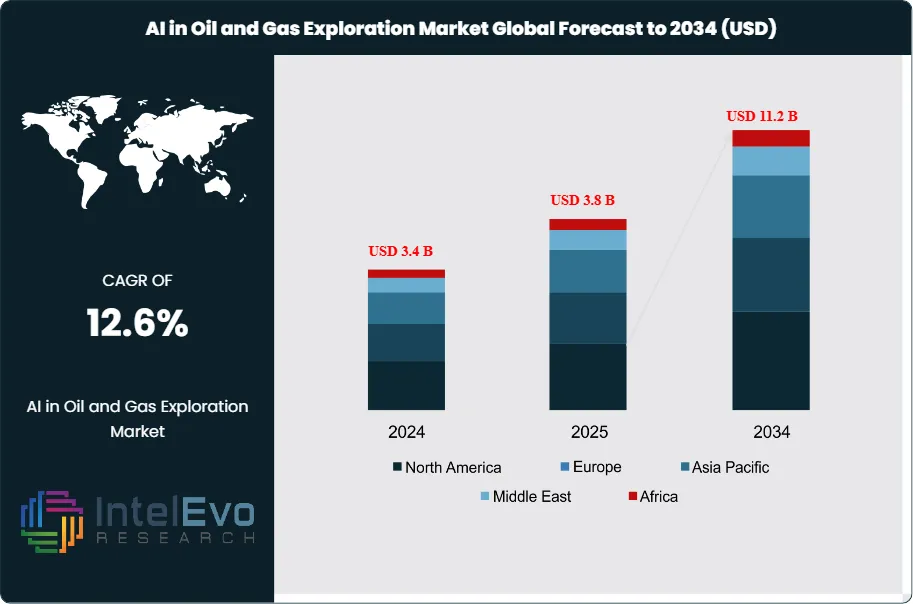

| USD 3.8 Billion | USD 11.2 Billion | 12.6% | North America, 38.2% |

The AI in Oil and Gas Exploration Market was valued at approximately USD 3.4 Billion in 2024 and increased to USD 3.8 Billion in 2025. The market is projected to reach nearly USD 11.2 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 12.6% during the forecast period from 2026 to 2034. The AI in oil and gas exploration market has entered a period of accelerated adoption, driven by the convergence of advanced machine learning algorithms, seismic data processing capabilities, and rising operational efficiency demands across upstream activities. Energy companies globally are deploying AI-driven platforms to reduce exploration risk, improve hydrocarbon discovery rates, and manage subsurface uncertainty in increasingly complex geological environments.

Get More Information about this report -

Request Free Sample ReportThe AI in oil and gas exploration market is shaped by powerful demand-side forces including the growing volume of seismic and well log data that exceeds human analytical capacity, the sustained pressure on exploration budgets, and the need for faster decision cycles in competitive asset environments. On the supply side, technology vendors are maturing their platforms with pre-trained geological models, cloud-native architectures, and real-time analytics capabilities tailored specifically for upstream oil and gas workflows. The AI in oil and gas exploration market reflects a broader digital transformation wave that is redefining how petroleum engineers, geoscientists, and reservoir analysts approach subsurface characterization.

Regulatory frameworks across major producing regions are increasingly supporting data standardization and digital reporting, which accelerates AI adoption. In the United States, the Bureau of Ocean Energy Management has expanded requirements for digital well data submission, while the European Union's energy transition mandates are compelling operators to extract maximum value from existing assets through AI-enabled enhanced recovery programs. Geopolitical volatility and energy security concerns are further incentivizing national oil companies in the Middle East and Asia Pacific to invest in AI tools that reduce dependence on foreign technical expertise.

Risk factors include cybersecurity vulnerabilities associated with connected subsurface systems, integration complexity with legacy seismic interpretation software, and the shortage of geoscience professionals who can bridge petroleum engineering and machine learning domains. Despite these challenges, the AI in oil and gas exploration market is attracting significant venture capital and corporate R&D investment, particularly in generative AI applications for geological modeling and autonomous drilling optimization. North America accounts for approximately 38.2% of global market revenue in 2025, driven by the active shale basin activity in the Permian, Eagle Ford, and Bakken formations. Asia Pacific represents the fastest-growing regional segment, with national oil companies in China, India, and Australia accelerating digital field programs. By 2034, AI-native exploration workflows are expected to become the operational standard across major international oil companies, reshaping competitive dynamics across the upstream energy value chain.

, By Technology (Machine Learning, Deep Learning and Neural Networks, Natural Language Processing, Computer Vision, Other Technologies including Reinforcement Learning and Federated Learning), By Application (Seismic Data Interpretation, Reservoir Characterization & Modeling, Drilling Optimization, Production Forecasting, Environmental & Supply Chain Analytics), By Deployment Mode (Cloud-Based, On-Premise, Edge Deployment), By End-User (International Oil Companies, National Oil Companies, Independent Operators, Oilfield Service Companies) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global AI in oil and gas exploration market was valued at USD 3.8 Billion in 2025 and is projected to reach USD 11.2 Billion by 2034, registering a CAGR of 12.6% during the forecast period 2025–2034. This growth is underpinned by rising upstream digitalization investment and expanding AI platform capabilities.

- Segment Dominance (By Offering): The software segment leads the AI in oil and gas exploration market with a 54.3% share in 2025, equivalent to USD 2.06 Billion, driven by demand for seismic interpretation platforms, reservoir simulation tools, and cloud-based geoscience analytics suites.

- Segment Dominance (By Application): Seismic data interpretation is the dominant application segment, commanding 38.7% of market revenue in 2025, as operators prioritize AI-driven processing to reduce cycle times and improve subsurface imaging accuracy in complex geological settings.

- Driver: The exponential growth of subsurface data volumes, with global seismic data generation increasing at approximately 22.4% annually, is compelling operators to adopt AI platforms that can process and interpret data orders of magnitude faster than conventional workflows.

- Restraint: High implementation costs and integration challenges with legacy geoscience software platforms limit adoption among mid-sized and independent operators. Integration projects typically require 12–24 months and USD 2–8 Million in upfront investment, constraining market penetration.

- Opportunity: Generative AI applications for synthetic well log generation and geological model augmentation represent a USD 1.4 Billion addressable opportunity by 2034. Early-stage deployments in 2025 cover less than 8% of technically viable upstream workflows, signaling significant untapped potential.

- Trend: Edge AI deployment in remote and offshore drilling environments is accelerating, with adoption growing at 31.5% annually in 2025. Real-time downhole analytics and autonomous wellbore management systems are transitioning from pilot projects to commercial-scale deployments across major basins.

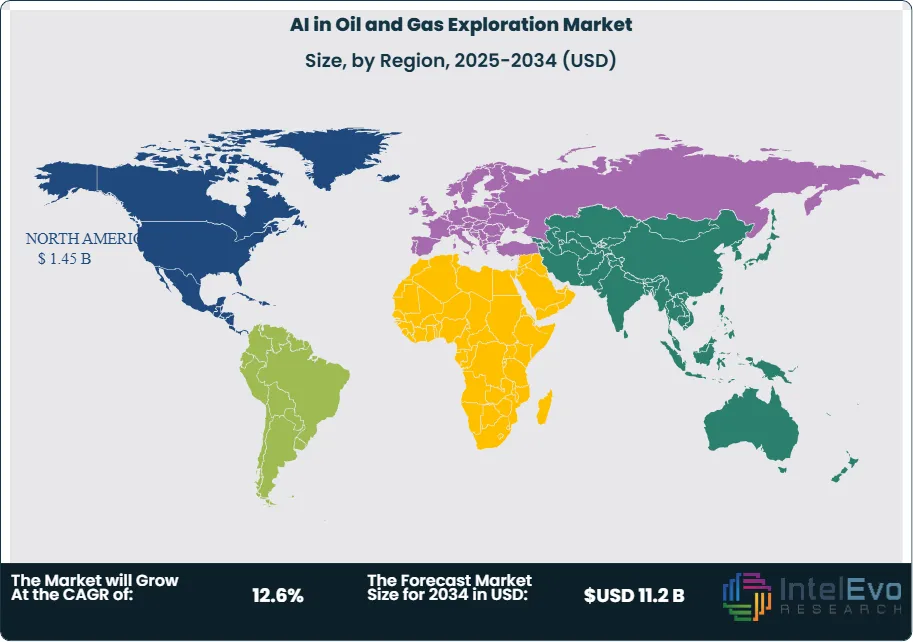

- Regional Analysis: North America leads the global AI in oil and gas exploration market with a 38.2% share in 2025, equivalent to USD 1.45 Billion, anchored by high shale basin activity, mature digital infrastructure, and strong venture-backed AI startup ecosystems in Texas and California.

Segmentation Analysis

The AI in oil and gas exploration market segmentation analysis examines the market across five dimensions: By Offering, By Technology, By Application, By Deployment Mode, and By End-User. Each segment carries distinct growth dynamics, competitive positioning factors, and technology adoption patterns that collectively define the market structure through 2034.

By Offering

The software segment dominates the AI in oil and gas exploration market by offering with a 54.3% share in 2025, generating USD 2.06 Billion in annual revenue. Software platforms encompass AI-powered seismic interpretation suites, reservoir characterization tools, production optimization engines, and integrated geoscience analytics environments. Leading vendors including Halliburton, Schlumberger (SLB), and specialist firms such as Earthworks AI have developed proprietary machine learning models trained on billions of subsurface data points, creating significant switching costs and data moats. The software segment benefits from subscription-based pricing models that provide recurring revenue streams and facilitate continuous model retraining on client-specific geological datasets, enhancing predictive accuracy over time.

The services segment holds a 31.2% share of the AI in oil and gas exploration market in 2025, valued at USD 1.19 Billion. Services include AI model deployment and integration consulting, geoscience data management, custom algorithm development, and managed analytics services. Oilfield services giants leverage existing client relationships to bundle AI services with traditional seismic acquisition and interpretation contracts. Independent AI consultancies are gaining traction particularly among national oil companies seeking to build internal capabilities rather than perpetual vendor dependency. The services segment is expected to grow at above-market rates through 2030 as operators transition from pilot programs to full-scale AI integration requiring ongoing technical support.

The hardware segment accounts for 14.5% of the market in 2025, totaling USD 551 Million. Hardware includes high-performance computing clusters, GPU-accelerated workstations, edge computing nodes deployed at wellsites and offshore platforms, and specialized seismic data acquisition sensors with embedded AI processing chips. The shift toward cloud-native AI platforms is moderating hardware growth relative to software and services, but edge AI hardware demand is accelerating as operators seek real-time downhole analytics without latency-intensive data transmission to central servers. Semiconductor manufacturers including NVIDIA and Intel are developing oilfield-grade AI accelerator chips optimized for subsurface signal processing workloads.

By Technology

Machine learning constitutes the foundational technology layer of the AI in oil and gas exploration market, accounting for 42.1% of technology segment revenue in 2025 at USD 1.60 Billion. Supervised and unsupervised learning algorithms are deployed extensively for lithology classification, fault detection, pore pressure prediction, and production decline curve analysis. Ensemble methods and gradient boosting models dominate in structured well log and petrophysical data analysis, while deep neural networks are preferred for seismic facies classification and direct hydrocarbon indicator identification. The maturity of open-source frameworks including TensorFlow and PyTorch has lowered barriers to internal model development for larger operators with data science teams.

Deep learning and neural network technologies command a 28.4% share in 2025, valued at USD 1.08 Billion. Convolutional neural networks applied to 3D seismic volumes have demonstrated 40–60% reductions in interpretation cycle times compared to manual workflows in field deployments across North Sea and Gulf of Mexico assets. Recurrent neural networks and transformer architectures are gaining adoption for time-series production data analysis and predictive maintenance applications. Generative adversarial networks are emerging as tools for synthetic seismic data augmentation, addressing the data scarcity challenge in frontier basin exploration where training datasets are limited.

Natural language processing holds 12.8% of the technology segment in 2025 at USD 486 Million, primarily applied to unstructured geological report mining, regulatory filing analysis, and automated well history digitization. Computer vision technologies contribute 10.2% at USD 388 Million, used in core sample analysis, formation image log interpretation, and wellsite safety monitoring. Other emerging technologies including reinforcement learning for drilling parameter optimization and federated learning for multi-operator data collaboration account for the remaining 6.5% of the technology segment in 2025.

By Application

Seismic data interpretation is the largest application within the AI in oil and gas exploration market, representing 38.7% of revenue in 2025 at USD 1.47 Billion. AI systems for seismic interpretation automate fault identification, horizon picking, stratigraphic analysis, and amplitude anomaly detection across massive 3D seismic datasets. Major operators report that AI-assisted interpretation workflows reduce cycle times from months to weeks, enabling faster exploration decisions and more frequent drilling target updates. The application has benefited from the accumulation of decades of digitized seismic surveys that provide rich training datasets for geologically aware neural networks.

Reservoir characterization and modeling accounts for 24.3% of application revenue in 2025 at USD 923 Million. AI models integrate petrophysical well log data, core measurements, and production history to generate high-resolution reservoir property grids that inform drilling and development decisions. Probabilistic AI frameworks are replacing deterministic workflows in subsurface uncertainty quantification, enabling operators to model hundreds of geological scenarios simultaneously. The application is particularly critical in unconventional resource development where lateral heterogeneity requires high-density data interpretation across dense well networks.

Drilling optimization applications hold 18.4% of market revenue in 2025 at USD 699 Million. AI systems for drilling optimization analyze real-time downhole measurement-while-drilling data to recommend weight-on-bit, rotary speed, and mud weight parameters that maximize rate of penetration while minimizing formation damage and wellbore stability risks. Autonomous drilling systems capable of self-adjusting parameters without human intervention are deployed in approximately 12% of active drilling programs globally in 2025. Production forecasting applications contribute 11.6% at USD 441 Million, while other applications including environmental compliance monitoring and supply chain optimization account for 7.0% of the market in 2025.

By Deployment Mode

Cloud-based deployment is the leading mode in the AI in oil and gas exploration market, capturing 58.9% of revenue in 2025 at USD 2.24 Billion. Cloud platforms provide elastic computing resources required for training large-scale geological AI models, enable multi-team collaboration on shared subsurface datasets, and reduce capital expenditure on dedicated computing infrastructure. Major public cloud providers including Amazon Web Services, Microsoft Azure, and Google Cloud have developed oil and gas industry-specific cloud environments with pre-configured seismic processing pipelines and geoscience software integrations. The cloud segment is experiencing the fastest growth within the deployment dimension as operators migrate legacy on-premise workstations to cloud-native AI environments.

On-premise deployment retains a 27.6% share in 2025 at USD 1.05 Billion, supported by data sovereignty requirements, high-bandwidth seismic data transfer constraints, and cybersecurity policies that prohibit uploading sensitive reservoir data to public cloud environments. National oil companies and operators in regions with underdeveloped cloud infrastructure continue to prefer on-premise AI systems deployed on dedicated high-performance computing clusters. Edge deployment represents the fastest-growing mode within the deployment segment at 13.5% share in 2025 and USD 513 Million in revenue, reflecting rising demand for real-time AI analytics at remote wellsite, offshore platform, and downhole sensor environments where cloud connectivity is unreliable or prohibited.

By End-User

International oil companies constitute the largest end-user segment of the AI in oil and gas exploration market, accounting for 39.4% of revenue in 2025 at USD 1.50 Billion. Entities including ExxonMobil, Shell, BP, TotalEnergies, and Chevron have established dedicated digital and AI centers of excellence with multi-year investment programs targeting AI integration across exploration, drilling, and production workflows. These operators drive technology benchmarking and vendor selection decisions that cascade across the broader industry. National oil companies represent 31.2% of market revenue in 2025 at USD 1.19 Billion, with Saudi Aramco, ADNOC, Petrobras, and PetroChina committing multi-billion-dollar digital transformation budgets that include significant AI in exploration components.

Independent oil companies account for 22.1% of the market in 2025 at USD 840 Million. Independent operators are increasingly adopting AI-as-a-service platforms that lower upfront investment requirements and provide access to pre-trained geological models without requiring large internal data science teams. Oilfield service companies represent the remaining 7.3% of end-user revenue at USD 277 Million in 2025, with firms like Halliburton and Baker Hughes embedding AI capabilities into their proprietary drilling and completion service offerings to differentiate technical service delivery.

Regional Analysis

Market in North America

North America leads the global AI in oil and gas exploration market with a 38.2% share in 2025, equivalent to USD 1.45 Billion in revenue. The region's dominance is anchored by the United States, which accounts for approximately 82% of North American market revenue, driven by the extraordinary density of drilling activity in unconventional shale basins including the Permian Basin, Eagle Ford, Bakken, and Marcellus. The U.S. shale industry's data-intensive operational model, characterized by multi-well pad drilling programs generating continuous streams of downhole and production data, has created ideal conditions for AI platform adoption. The presence of the world's largest concentration of oilfield technology startups, particularly in Houston and Denver, supports rapid commercialization of AI tools specifically designed for U.S. geological conditions.

Canada contributes approximately 14% of North American market revenue in 2025, with AI adoption concentrated in Alberta's oil sands operations where complex bitumen extraction workflows benefit from AI-driven thermal recovery optimization and environmental monitoring automation. Mexico represents a smaller but growing market as Pemex accelerates digital transformation initiatives in its deepwater Gulf of Mexico portfolio. The U.S. Department of Energy's digital oilfield investment programs and the National Energy Technology Laboratory's AI research partnerships provide institutional support for the market. North America is projected to maintain market leadership through 2034, growing at a CAGR of approximately 11.8%, supported by continued shale basin expansion and deepwater Gulf development.

Market in Europe

Europe accounts for 24.6% of the global AI in oil and gas exploration market in 2025, generating USD 935 Million in revenue. The United Kingdom leads the European segment, driven by North Sea upstream activity where mature field management and enhanced oil recovery optimization represent the primary AI application areas. Operators including Shell, BP, and Equinor are deploying AI reservoir surveillance systems across aging North Sea assets to extend field life and maximize recovery from existing wells without the capital expense of new exploration programs. The UK's Oil and Gas Authority digital strategy explicitly targets AI adoption as a mechanism for improving economic recovery from the continental shelf.

Norway is the second-largest European market, with Equinor's Integrated Operations concept incorporating AI-driven production optimization across its Johan Sverdrup and Troll fields. Germany contributes through its strong AI software development ecosystem, with Munich-based and Berlin-based technology firms developing geoscience AI platforms targeting European operators. The Netherlands remains relevant through Shell's global technology center in The Hague, which coordinates AI exploration research programs. European market growth is shaped by the EU's Carbon Border Adjustment Mechanism, which is incentivizing operators to use AI for emissions intensity reduction in extraction operations. Europe is expected to grow at a CAGR of 11.2% through 2034.

Market in Asia Pacific

Asia Pacific represents the fastest-growing regional segment in the AI in oil and gas exploration market, holding a 22.4% share in 2025 at USD 851 Million and projected to grow at a CAGR of 14.8% through 2034. China is the dominant country market, with PetroChina and SINOPEC deploying AI exploration platforms across onshore Sichuan Basin gas operations and offshore South China Sea developments. China's government-backed AI development strategy explicitly identifies oilfield AI as a strategic industrial application, channeling state funding toward national champion technology providers. The China National Offshore Oil Corporation has invested over USD 400 Million in digital exploration programs since 2022, with AI seismic interpretation and reservoir modeling forming core components.

India is the second-largest Asia Pacific market, with Oil and Natural Gas Corporation and Reliance Industries deploying AI tools in Krishna-Godavari Basin deepwater operations and Rajasthan onshore developments. Australia's market is driven by LNG sector digitalization, with Woodside Energy and Santos deploying AI for subsurface surveillance and production optimization in their Carnarvon Basin assets. Indonesia represents an emerging opportunity as Pertamina pursues digital transformation to improve recovery rates from its aging Sumatran fields. The Asia Pacific market benefits from government mandates for domestic energy self-sufficiency that are accelerating AI adoption to maximize recovery from existing acreage.

Market in Latin America

Latin America holds an 8.4% share of the global AI in oil and gas exploration market in 2025, valued at USD 319 Million. Brazil dominates the regional market, accounting for approximately 61% of Latin American revenue, with Petrobras deploying AI seismic interpretation and reservoir management platforms across its massive pre-salt carbonate fields in the Santos and Campos Basins. The pre-salt geology presents extreme interpretive complexity that makes AI-assisted subsurface analysis particularly valuable. Petrobras has established a dedicated technology innovation center in Rio de Janeiro with a specific mandate to develop AI applications for carbonate reservoir characterization and deepwater well optimization.

Mexico contributes approximately 22% of regional market revenue, with Pemex accelerating digital adoption across its Cantarell and Ku-Maloob-Zaap fields under government pressure to reverse production decline. Colombia's national oil company Ecopetrol is deploying AI tools to extend the productive life of Llanos Basin assets, with particular emphasis on enhanced oil recovery optimization. Argentina represents an emerging opportunity, driven by Vaca Muerta shale development where unconventional resource complexity creates demand for AI-driven geological modeling tools similar to those deployed in U.S. shale plays. Latin America is projected to grow at a CAGR of 13.1% through 2034 as energy security imperatives drive digitalization investment.

Market in Middle East & Africa

The Middle East and Africa segment accounts for 6.4% of global AI in oil and gas exploration market revenue in 2025, totaling USD 243 Million. The United Arab Emirates is the regional leader, with ADNOC's AI ambitions among the most publicly stated of any national oil company globally. ADNOC has committed to deploy AI across 100% of its operations by 2025, with exploration and reservoir management representing the largest investment areas. The company's partnership with Microsoft and IBM for AI platform development has positioned Abu Dhabi as a regional AI-in-energy hub. Saudi Arabia is the second-largest Middle East market, with Saudi Aramco's Expec Advanced Research Center conducting frontier AI research in seismic imaging, carbonate reservoir modeling, and autonomous drilling systems.

South Africa's market is primarily driven by PetroSA's offshore exploration programs and private sector natural gas developments. The broader African market presents a long-term growth opportunity as frontier basin exploration in East Africa, West Africa, and North Africa requires sophisticated subsurface imaging AI to de-risk exploration programs in geologically complex environments with limited well data. Government-sponsored exploration programs in Tanzania, Mozambique, and Kenya are beginning to incorporate AI screening tools to prioritize drilling targets. The Middle East and Africa region is expected to grow at a CAGR of 14.2% through 2034 as national oil companies intensify AI adoption programs.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software

- Services

- Hardware

By Technology

- Machine Learning

- Deep Learning and Neural Networks

- Natural Language Processing

- Computer Vision

- Other Technologies (Reinforcement Learning, Federated Learning)

By Application

- Seismic Data Interpretation

- Reservoir Characterization and Modeling

- Drilling Optimization

- Production Forecasting

- Other Applications (Environmental Compliance, Supply Chain)

By Deployment Mode

- Cloud-Based

- On-Premise

- Edge Deployment

By End-User

- International Oil Companies

- National Oil Companies

- Independent Oil Companies

- Oilfield Service Companies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.8 B |

| Forecast Revenue (2034) | USD 11.2 B |

| CAGR (2025-2034) | 12.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering (Software, Services, Hardware), By Technology (Machine Learning, Deep Learning and Neural Networks, Natural Language Processing, Computer Vision, Other Technologies (Reinforcement Learning, Federated Learning)), By Application (Seismic Data Interpretation, Reservoir Characterization and Modeling, Drilling Optimization, Production Forecasting, Other Applications (Environmental Compliance, Supply Chain)), By Deployment Mode (Cloud-Based, On-Premise, Edge Deployment), By End-User (International Oil Companies, National Oil Companies, Independent Oil Companies, Oilfield Service Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HALLIBURTON COMPANY, SLB (SCHLUMBERGER LIMITED), IBM CORPORATION, MICROSOFT CORPORATION, BAKER HUGHES COMPANY, TOTALENERGIES SE, LANDMARK GRAPHICS CORPORATION (HALLIBURTON SUBSIDIARY), ASPENTECH, PALANTIR TECHNOLOGIES INC., NVIDIA CORPORATION, AMAZON WEB SERVICES INC., GOOGLE LLC (ALPHABET INC.), IKON SCIENCE LTD., EMERSON ELECTRIC CO., WEATHERFORD INTERNATIONAL PLC, PETREL (DASSAULT SYSTEMES), KATALYST DATA MANAGEMENT, ROCK FLOW DYNAMICS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Machine Learning, Deep Learning and Neural Networks, Natural Language Processing, Computer Vision, Other Technologies including Reinforcement Learning and Federated Learning), By Application (Seismic Data Interpretation, Reservoir Characterization & Modeling, Drilling Optimization, Production Forecasting, Environmental & Supply Chain Analytics), By Deployment Mode (Cloud-Based, On-Premise, Edge Deployment), By End-User (International Oil Companies, National Oil Companies, Independent Operators, Oilfield Service Companies) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Technology (Machine Learning, Deep Learning and Neural Networks, Natural Language Processing, Computer Vision, Other Technologies including Reinforcement Learning and Federated Learning), By Application (Seismic Data Interpretation, Reservoir Characterization & Modeling, Drilling Optimization, Production Forecasting, Environmental & Supply Chain Analytics), By Deployment Mode (Cloud-Based, On-Premise, Edge Deployment), By End-User (International Oil Companies, National Oil Companies, Independent Operators, Oilfield Service Companies) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Technology (Machine Learning, Deep Learning and Neural Networks, Natural Language Processing, Computer Vision, Other Technologies including Reinforcement Learning and Federated Learning), By Application (Seismic Data Interpretation, Reservoir Characterization & Modeling, Drilling Optimization, Production Forecasting, Environmental & Supply Chain Analytics), By Deployment Mode (Cloud-Based, On-Premise, Edge Deployment), By End-User (International Oil Companies, National Oil Companies, Independent Operators, Oilfield Service Companies) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI in Oil and Gas Exploration Market?

The Global AI in Oil and Gas Exploration Market was valued at USD 3.4 Billion in 2024 and USD 3.8 Billion in 2025, projected to reach USD 11.2 Billion by 2034 at a CAGR of 12.6% from 2026–2034. Growth is driven by AI-based seismic interpretation, reservoir modeling, predictive analytics, and rising digital oilfield investments worldwide.

Who are the major players in the AI in Oil and Gas Exploration Market?

HALLIBURTON COMPANY, SLB (SCHLUMBERGER LIMITED), IBM CORPORATION, MICROSOFT CORPORATION, BAKER HUGHES COMPANY, TOTALENERGIES SE, LANDMARK GRAPHICS CORPORATION (HALLIBURTON SUBSIDIARY), ASPENTECH, PALANTIR TECHNOLOGIES INC., NVIDIA CORPORATION, AMAZON WEB SERVICES INC., GOOGLE LLC (ALPHABET INC.), IKON SCIENCE LTD., EMERSON ELECTRIC CO., WEATHERFORD INTERNATIONAL PLC, PETREL (DASSAULT SYSTEMES), KATALYST DATA MANAGEMENT, ROCK FLOW DYNAMICS, Others

Which segments covered the AI in Oil and Gas Exploration Market?

By Offering (Software, Services, Hardware), By Technology (Machine Learning, Deep Learning and Neural Networks, Natural Language Processing, Computer Vision, Other Technologies (Reinforcement Learning, Federated Learning)), By Application (Seismic Data Interpretation, Reservoir Characterization and Modeling, Drilling Optimization, Production Forecasting, Other Applications (Environmental Compliance, Supply Chain)), By Deployment Mode (Cloud-Based, On-Premise, Edge Deployment), By End-User (International Oil Companies, National Oil Companies, Independent Oil Companies, Oilfield Service Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI in Oil and Gas Exploration Market

Published Date : 12 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date