- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI in Pathology Market Size, Share & Forecast | CAGR 19.1%

Global AI in Pathology Market Size, Share, Growth Analysis By Offering (Software, Services, Hardware), By Application (Oncology Diagnostics, Non-Oncology Diagnostics, Drug Discovery, Research Applications), By End-User (Hospitals, Clinical Laboratories, Pharma & Biotech Companies, Academic Institutes), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

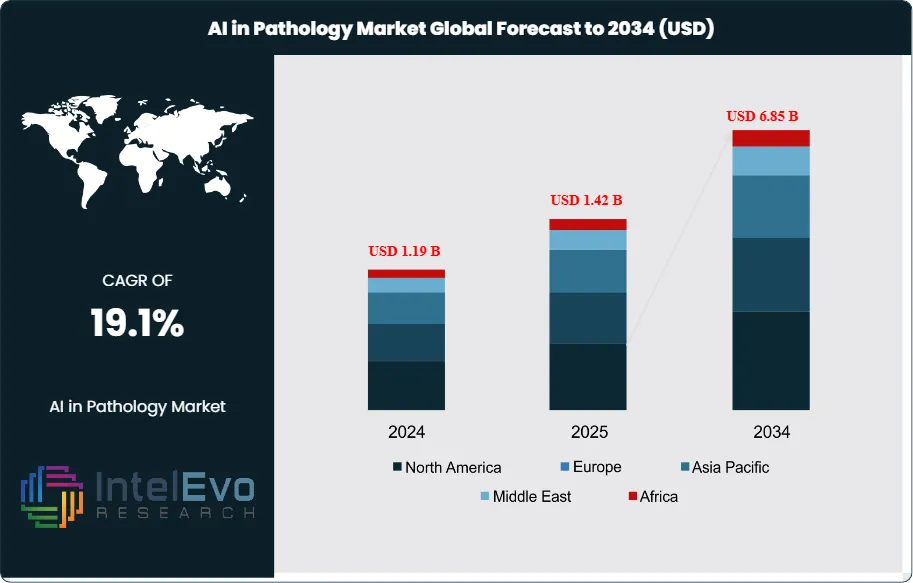

| USD 1.42 Billion | USD 6.85 Billion | 19.1% | North America, 42.3% |

The AI in Pathology Market was valued at approximately USD 1.19 Billion in 2024 and reached USD 1.42 Billion in 2025. The market is projected to grow to USD 6.85 Billion by 2034, expanding at a CAGR of 19.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 5.43 Billion over the analysis period, reflecting the accelerating integration of artificial intelligence across anatomic pathology workflows, digital slide analysis, and cancer diagnostics.

Get More Information about this report -

Request Free Sample ReportAI in pathology has transitioned from experimental research tools to clinically validated diagnostic platforms adopted in tertiary care hospitals, cancer centers, and reference laboratories. Computational pathology algorithms trained on millions of whole-slide images now achieve sensitivity and specificity metrics rivaling or exceeding board-certified pathologists in specific indications, including prostate cancer Gleason grading, breast cancer HER2 scoring, and colorectal polyp classification. This performance validation has been the primary commercial catalyst, enabling reimbursement discussions with payers in the United States and conditional approvals under the European In Vitro Diagnostic Regulation (IVDR) and FDA’s De Novo and 510(k) pathways.

Demand drivers include a global shortage of pathologists estimated at 30,000 to 50,000 practitioners, rising cancer incidence rates projected by the World Health Organization at over 29 million new cases annually by 2040, and the adoption of companion diagnostics linked to targeted oncology therapies. Biomarker quantification for PD-L1, TMB, and HER2 using AI reduces inter-laboratory variability from approximately 25% to under 5%, a statistically significant improvement that supports better patient selection for immunotherapy regimens.

Regulatory frameworks are maturing. The FDA granted De Novo authorization for several AI-assisted image analysis systems between 2022 and 2025, while the EU’s IVDR transition deadline for Class C in vitro diagnostics has created compliance pressure that paradoxically accelerates AI vendor engagement with large diagnostic networks. The Asia Pacific region, led by China’s National Medical Products Administration reforms and Japan’s AMED-funded digital pathology consortium, is closing the adoption gap with North America.

Investment activity reinforces the market thesis. Venture capital deployment into computational pathology exceeded USD 800 Million between 2023 and 2025, while large in vitro diagnostics companies and pharmaceutical firms have executed strategic acquisitions to secure AI-enabled tissue analysis capabilities. The intersection of AI in pathology with spatial transcriptomics, proteomics, and multi-modal imaging is creating data infrastructure that will extend the forecast-period opportunity well into the next decade.

, By Application (Oncology Diagnostics, Non-Oncology Diagnostics, Drug Discovery, Research Applications), By End-User (Hospitals, Clinical Laboratories, Pharma & Biotech Companies, Academic Institutes), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global AI in pathology market was valued at USD 1.42 Billion in 2025 and is projected to reach USD 6.85 Billion by 2034, growing at a CAGR of 19.1% during the forecast period 2026–2034.

- Segment Dominance: By offering, software solutions lead with approximately 61.5% of market revenue in 2025, driven by algorithmic image analysis platforms deployed across hospital laboratory information systems.

- Segment Dominance: By application, oncology diagnostics accounts for the largest application share at approximately 54.8% in 2025, supported by FDA-cleared cancer detection and grading algorithms across breast, prostate, and colorectal indications.

- Driver: A global deficit of 30,000 to 50,000 pathologists combined with a 25% year-over-year increase in cancer biopsy volumes is compelling laboratories to adopt AI-assisted reading tools to maintain diagnostic throughput.

- Restraint: High implementation costs averaging USD 250,000 to USD 600,000 per site for whole-slide imaging infrastructure and AI software licensing, combined with limited reimbursement coverage in emerging markets, restrict adoption in community hospitals and low-resource settings.

- Opportunity: AI-driven companion diagnostics for immuno-oncology represent an addressable opportunity exceeding USD 1.8 Billion by 2034, as pharmaceutical manufacturers require standardized, auditable biomarker quantification to support IND and NDA filings.

- Trend: Foundation models trained on multi-stain, multi-organ whole-slide image datasets are replacing narrow single-task classifiers; adoption of foundation model architectures in commercial pathology AI products reached approximately 18% of new deployments in 2025 and is forecast to exceed 60% by 2030.

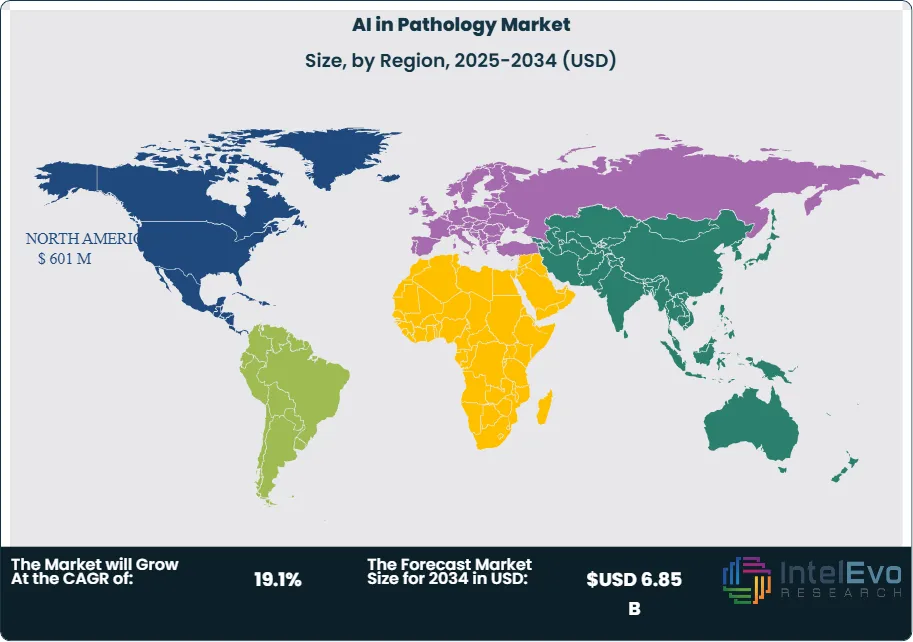

- Regional Analysis: North America holds the largest regional share at 42.3%, equivalent to approximately USD 601 Million in 2025, supported by FDA regulatory clarity, established digital pathology infrastructure, and concentrated oncology center demand.

Competitive Landscape Overview

The AI in pathology market is moderately consolidated at the top tier, with the four leading companies accounting for approximately 38% of global revenue in 2025. Competition is predominantly technology-driven, with differentiation centered on algorithm performance metrics, regulatory clearance breadth, laboratory information system integrations, and cloud-based deployment flexibility. Merger and acquisition activity intensified between 2023 and 2025 as large diagnostics corporations moved to acquire pure-play computational pathology firms. New entrants backed by foundation model capabilities are applying pressure on established vendors primarily through pricing and breadth of indication coverage.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| Paige.AI | USA | Leader | Paige Prostate | North America | Received FDA clearance expansion to breast cancer detection; partnered with Memorial Sloan Kettering for multi-organ model (2025) |

| Philips (PathAI Anatomics) | Netherlands | Leader | IntelliSite Pathology Suite | Europe / North America | Completed integration of PathAI co-developed algorithms into IntelliSite platform; expanded EU IVDR portfolio (2025) |

| Roche (navify) | Switzerland | Leader | navify Digital Pathology | Europe / Global | Launched navify Algorithm Suite update with HER2 and PD-L1 AI modules; signed pharma companion diagnostic agreements (Jan 2025) |

| Leica Biosystems (Danaher) | USA / Germany | Leader | Aperio GT 450 + AI | North America / Europe | Announced AI algorithm marketplace partnership with PathAI and Aiforia; expanded service contracts with 80+ cancer centers (2025) |

| PathAI | USA | Challenger | AISight Platform | North America | Secured Series D funding of USD 165 Million; launched multi-stain workflow for clinical trial sites (2024) |

| Aiforia Technologies | Finland | Niche Player | Aiforia Cloud | Europe | Launched GLP-compliant preclinical AI module; expanded Nordic hospital agreements (Q1 2025) |

| Ibex Medical Analytics | Israel | Niche Player | Galen Prostate & Breast | North America / Middle East | Received CE IVDR Class C certification for Galen Breast platform (Dec 2024) |

| Proscia | USA | Niche Player | Concentriq Dx | North America | Raised USD 55 Million Series C; added AI-native annotation tools for pharma R&D workflows (2025) |

By Offering

The AI in pathology market by offering is divided into software, services, and hardware segments, with software commanding the dominant position. Software platforms accounted for approximately 61.5% of total market revenue in 2025, equivalent to roughly USD 873 Million. These platforms encompass algorithm suites for whole-slide image analysis, laboratory workflow management applications, and cloud-based diagnostic support tools. Growth in the software segment is sustained by subscription and usage-based pricing models that reduce upfront capital barriers for laboratories, recurring revenue streams that attract institutional investors, and continuous performance improvement through federated learning across partner institutions. Image analysis algorithms cleared by the FDA or certified under IVDR carry premium pricing, with annual software licenses for cancer detection modules ranging from USD 80,000 to USD 300,000 per installation depending on volume throughput and indication breadth.

Services constitute approximately 23.8% of market revenue in 2025, valued at roughly USD 338 Million. This segment encompasses implementation consulting, algorithm validation and customization, training programs for pathologists and laboratory technicians, and managed digital pathology services where vendors assume operational responsibility for scanning and AI-assisted reads. The services segment benefits from the complexity of laboratory information system integration and the regulatory validation requirements that mandate site-specific performance verification before clinical deployment. Emerging pharma-focused contract research services that provide AI-assisted tissue analysis for oncology clinical trials are growing at an above-average rate within this sub-segment.

Hardware, including whole-slide scanners, servers, and workstation infrastructure, represents approximately 14.7% of market revenue in 2025 at USD 209 Million. Hardware revenue is directly correlated with digital pathology adoption rates. Laboratories transitioning from optical microscopy to fully digital workflows are first-time buyers of primary scanning systems, while established digital labs generate replacement and upgrade demand. Slide scanner throughput has risen substantially, with current generation platforms achieving 400 to 600 slides per eight-hour shift, reducing per-slide scanning costs below USD 1.50 at scale.

By Application

Oncology diagnostics represent the largest application segment at approximately 54.8% of market revenue in 2025, valued at USD 778 Million. Cancer remains the primary commercial focus for AI in pathology given the high diagnostic complexity, clinician demand for second-read tools, and direct linkage between AI-assisted biomarker quantification and targeted therapy selection. Prostate, breast, colorectal, and lung cancer represent the four highest-volume indications, collectively driving over 70% of oncology application revenue. Regulatory-cleared algorithms in these indications command pricing premiums and benefit from reimbursement category discussions initiated by the American College of Pathology and the College of American Pathologists.

Non-oncology diagnostics, including inflammatory disease, infectious pathology, and transplant evaluation, account for approximately 21.3% of market revenue in 2025 at USD 302 Million. This segment is earlier in the commercial adoption cycle relative to oncology but shows a higher organic growth rate due to the expansion of AI into routine histopathology beyond cancer. Dermatopathology AI for inflammatory skin conditions and nephropathology AI for transplant rejection scoring are the fastest-growing non-oncology sub-categories.

Drug discovery and development applications account for approximately 14.6% of market revenue in 2025, estimated at USD 207 Million. Pharmaceutical and biotechnology companies use AI-assisted pathology to accelerate preclinical safety studies, identify pharmacodynamic biomarkers in clinical trial biopsies, and develop companion diagnostics aligned with therapeutic mechanisms. Contract research organizations with dedicated digital pathology AI capabilities have seen clinical trial site agreements increase 35% between 2023 and 2025. Research and academic applications constitute the remaining approximately 9.3%, valued at USD 132 Million in 2025.

By End-User

Hospitals and health systems represent the largest end-user segment at approximately 46.2% of market revenue in 2025, valued at USD 656 Million. Academic medical centers and comprehensive cancer centers within health systems are the earliest and most intensive adopters, serving as reference sites that generate clinical evidence and train commercial AI models. Community hospital adoption is growing but constrained by budget limitations and pathologist workforce gaps that paradoxically create the demand for AI while limiting the institutional capacity to evaluate and procure it.

Clinical and reference laboratories hold approximately 28.4% of market share in 2025 at USD 403 Million. Commercial reference laboratory networks, including large-volume national operators, are aggressively evaluating AI platforms to improve quality consistency across decentralized operations and to reduce pathologist labor costs per case. Standardized AI reading reduces the inter-reader variability inherent in multi-site laboratory networks, making the technology particularly compelling for laboratory organizations managing pathologist shortage through distributed remote-read models.

Pharmaceutical and biotech companies account for approximately 16.9% at USD 240 Million in 2025, while academic and research institutions represent the remaining 8.5% at USD 121 Million. Pharma adoption is tied directly to companion diagnostic development pipelines and the increasing regulatory expectation that biomarker data submitted in drug approval packages be generated using analytically validated, reproducible digital methods.

By Deployment Mode

Cloud-based deployment has emerged as the dominant mode, representing approximately 52.4% of market revenue in 2025 at USD 744 Million. Cloud deployment eliminates the need for on-premise computing infrastructure, enables rapid algorithm updates without site-by-site installation cycles, and facilitates federated training across multi-site laboratory networks without centralizing protected health information. HIPAA-compliant cloud environments from major hyperscalers have cleared the primary security objection from hospital IT departments, accelerating the migration from legacy on-premise installations. On-premise deployment retains approximately 35.1% share at USD 498 Million, favored by institutions with strict data sovereignty requirements, existing server infrastructure investments, or regulatory mandates in certain international jurisdictions. Hybrid deployment, combining local processing for sensitive patient data with cloud-based algorithm management, accounts for the remaining 12.5% at USD 178 Million.

Regional Analysis

North America

North America holds the largest regional share in the global AI in pathology market at approximately 42.3%, equivalent to USD 601 Million in 2025. The United States accounts for the substantial majority of regional revenue, driven by the density of NCI-designated cancer centers, the FDA’s regulatory framework for software as a medical device, and strong venture capital and strategic investment flows into computational pathology. The College of American Pathologists has established digital pathology accreditation standards that incentivize laboratory investment in scanning and AI infrastructure, creating institutional demand at a policy level. Canada contributes meaningfully to regional totals through its publicly funded provincial cancer programs piloting AI-assisted cervical and colorectal cancer screening. Mexico is in early-stage digital pathology infrastructure development. The United States market benefits from direct-to-payer engagement models, where AI pathology vendors are negotiating per-case reimbursement arrangements with national commercial insurers, a development that will structurally transform revenue models over the forecast period.

Europe

Europe represents approximately 26.8% of global market revenue at USD 381 Million in 2025. The European In Vitro Diagnostic Regulation has created both regulatory burden and commercial opportunity, as laboratories required to validate and re-certify diagnostic tools under IVDR are choosing AI platforms with pre-certified status to reduce compliance risk. Germany leads European adoption through its university hospital network and the German Cancer Research Center’s investment in digital pathology standardization. The United Kingdom, through NHS England and Cancer Research UK collaborations, has deployed AI-assisted pathology pilots across more than 40 NHS trust pathology hubs. France has advanced AI in pathology through the national INCa cancer research funding program. The Netherlands has a concentrated diagnostics industry anchored by Philips that influences pan-European hospital procurement. Pan-European regulatory harmonization under IVDR and coordinated imaging data initiatives from the European Health Data Space are creating scalable market access frameworks that reduce per-country regulatory friction.

Asia Pacific

Asia Pacific accounts for approximately 22.1% of global market revenue at USD 314 Million in 2025 and is the fastest-growing regional segment, driven by high cancer incidence rates, government-led digital health investment, and a large deficit of trained pathologists relative to population. China’s National Medical Products Administration has cleared several domestically developed AI pathology platforms for cervical cytology and gastric cancer screening, and national policy mandates for hospital information system interoperability are creating a favorable infrastructure environment. Japan’s Pharmaceuticals and Medical Devices Agency has streamlined software medical device approval timelines, enabling faster market entry for AI pathology solutions, while the AMED national research funding body has supported digital pathology infrastructure across academic hospitals. India’s market, valued at approximately USD 38 Million in 2025, is growing rapidly from a low base, driven by the adoption of AI-assisted cervical cancer screening in national health programs and the expansion of hospital chains investing in laboratory automation. South Korea’s strong digital health infrastructure and active diagnostic industry position it as a leading adopter in Southeast Asia.

Latin America

Latin America represents approximately 5.6% of global market revenue at USD 79 Million in 2025. Brazil dominates the regional market through its large private hospital network, active oncology research at INCA, and digital health initiatives from the Ministry of Health targeting cancer diagnostics equity. Chile and Colombia have active digital pathology programs within university hospital networks. Mexico’s market is emerging, constrained by budget limitations in the public health system but driven by private hospital investments in clinical technology differentiation. Regulatory frameworks in Latin America are largely modeled on FDA and European guidelines but lack the uniform implementation resources, creating vendor-specific registration timelines of 12 to 24 months per market. Regional growth over the forecast period will be driven primarily by cervical cancer screening AI, which addresses a high-burden disease with established national programs amenable to algorithmic augmentation.

Middle East & Africa

The Middle East and Africa region accounts for approximately 3.2% of global market revenue at USD 45 Million in 2025. The United Arab Emirates, through Dubai Healthcare City and Abu Dhabi’s SEHA health system, represents the most advanced AI adoption environment in the region, with multiple AI pathology platforms deployed in tertiary care centers. Saudi Arabia’s Vision 2030 health transformation program has allocated capital for laboratory digitization, and the Saudi Food and Drug Authority has established a dedicated software medical device regulatory pathway. South Africa leads Sub-Saharan Africa with active digital pathology adoption in academic hospitals and national laboratories serving HIV and tuberculosis diagnostic needs. The region’s growth trajectory is constrained by scanner infrastructure costs and internet bandwidth limitations in rural Sub-Saharan African settings, though cellular connectivity improvements and cloud-native lightweight AI architectures are gradually expanding addressable geography.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software

- Services

- Hardware

By Application

- Oncology Diagnostics

- Non-Oncology Diagnostics

- Drug Discovery and Development

- Research and Academic Applications

By End-User

- Hospitals and Health Systems

- Clinical and Reference Laboratories

- Pharmaceutical and Biotechnology Companies

- Academic and Research Institutions

By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.42 B |

| Forecast Revenue (2034) | USD 6.85 B |

| CAGR (2025-2034) | 19.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software, Services, Hardware), By Application, (Oncology Diagnostics, Non-Oncology Diagnostics, Drug Discovery and Development, Research and Academic Applications), By End-User, (Hospitals and Health Systems, Clinical and Reference Laboratories, Pharmaceutical and Biotechnology Companies, Academic and Research Institutions), By Deployment Mode, (Cloud-Based, On-Premise, Hybrid) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PAIGE.AI, ROCHE (NAVIFY DIGITAL PATHOLOGY), LEICA BIOSYSTEMS (DANAHER CORPORATION), PATHAI, PHILIPS (INTELLISITE PATHOLOGY SUITE), IBEX MEDICAL ANALYTICS, AIFORIA TECHNOLOGIES, PROSCIA, GESTALT DIAGNOSTICS, VISIOPHARM, SECTRA, TRIBUN HEALTH, INVEOX, HAMAMATSU PHOTONICS, MOTIC DIGITAL PATHOLOGY, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Oncology Diagnostics, Non-Oncology Diagnostics, Drug Discovery, Research Applications), By End-User (Hospitals, Clinical Laboratories, Pharma & Biotech Companies, Academic Institutes), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

, By Application (Oncology Diagnostics, Non-Oncology Diagnostics, Drug Discovery, Research Applications), By End-User (Hospitals, Clinical Laboratories, Pharma & Biotech Companies, Academic Institutes), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

, By Application (Oncology Diagnostics, Non-Oncology Diagnostics, Drug Discovery, Research Applications), By End-User (Hospitals, Clinical Laboratories, Pharma & Biotech Companies, Academic Institutes), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the AI in Pathology Market?

The Global AI in Pathology Market was valued at USD 1.19 Billion in 2024 and is projected to reach USD 6.85 Billion by 2034, growing at a CAGR of 19.1% from 2026 to 2034, driven by increasing adoption of digital pathology, rising demand for AI-assisted cancer diagnostics, advancements in machine learning algorithms, and growing investments in precision medicine, laboratory automation, and healthcare analytics solutions.

Who are the major players in the AI in Pathology Market?

PAIGE.AI, ROCHE (NAVIFY DIGITAL PATHOLOGY), LEICA BIOSYSTEMS (DANAHER CORPORATION), PATHAI, PHILIPS (INTELLISITE PATHOLOGY SUITE), IBEX MEDICAL ANALYTICS, AIFORIA TECHNOLOGIES, PROSCIA, GESTALT DIAGNOSTICS, VISIOPHARM, SECTRA, TRIBUN HEALTH, INVEOX, HAMAMATSU PHOTONICS, MOTIC DIGITAL PATHOLOGY, Others

Which segments covered the AI in Pathology Market?

By Offering, (Software, Services, Hardware), By Application, (Oncology Diagnostics, Non-Oncology Diagnostics, Drug Discovery and Development, Research and Academic Applications), By End-User, (Hospitals and Health Systems, Clinical and Reference Laboratories, Pharmaceutical and Biotechnology Companies, Academic and Research Institutions), By Deployment Mode, (Cloud-Based, On-Premise, Hybrid)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date