- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

AI in Predictive Policing Market Size 2025–2034 | CAGR 47.2%

Global AI in Predictive Policing Market Size, Share & Growth Analysis By Offering (Predictive Analytics Solutions, Risk & Crime Analytics, Real-Time Monitoring Platforms, Professional & Managed Services), By Deployment Mode (Cloud-Based, On-Premises), By Organization Size (Large Enterprises, SMEs), By Technology (Machine Learning, Deep Learning, NLP, Computer Vision), By Vertical & Region – Industry Overview, Market Dynamics, Ethical & Regulatory Landscape, Competitive Strategies, Emerging Trends & Forecast 2026–2034

Report Overview

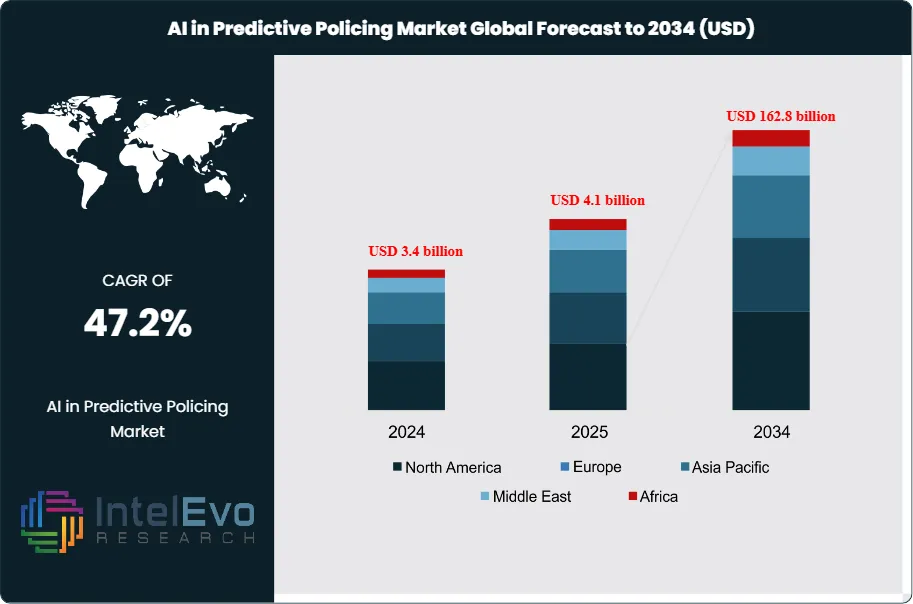

The AI in Predictive Policing Market is estimated to reach approximately USD 4.1 billion in 2025 and is projected to surge to around USD 162.8 billion by 2034, registering a very strong compound annual growth rate (CAGR) of about 47.2% during the forecast period from 2026 to 2034. This rapid expansion is driven by increasing adoption of AI-powered crime forecasting, real-time risk assessment, and data-driven patrol optimization across law enforcement agencies worldwide. Governments and public safety organizations are leveraging predictive analytics to reduce response times, allocate resources more efficiently, and improve crime prevention outcomes. Additionally, the integration of predictive policing platforms with smart city infrastructure, surveillance networks, and cloud-based analytics is accelerating deployment, positioning AI as a core pillar of next-generation public safety and security strategies.

Get More Information about this report -

Request Free Sample ReportAI in predictive policing uses machine learning and advanced analytics to forecast crime patterns and guide deployment decisions. Law enforcement agencies ingest structured and unstructured data, including incident reports, sensor feeds, and open-source intelligence, to detect spatial and temporal hotspots. This data-driven approach supports faster response, targeted patrols, and more efficient use of constrained public safety budgets, which strengthens the business case for investment.

Market expansion reflects a sharp rise in digital evidence volumes, maturing big data infrastructure, and accelerated adoption of cloud-based analytics platforms. Demand is strongest in dense urban environments where crime patterns are complex and traditional methods strain capacity. On the supply side, global technology providers, niche AI specialists, and system integrators compete on model accuracy, interpretability, integration with existing command-and-control systems, and lifecycle support. Vendors embed automation across workflows, from incident triage to real-time alerting, which lifts operational productivity for agencies facing staffing pressures.

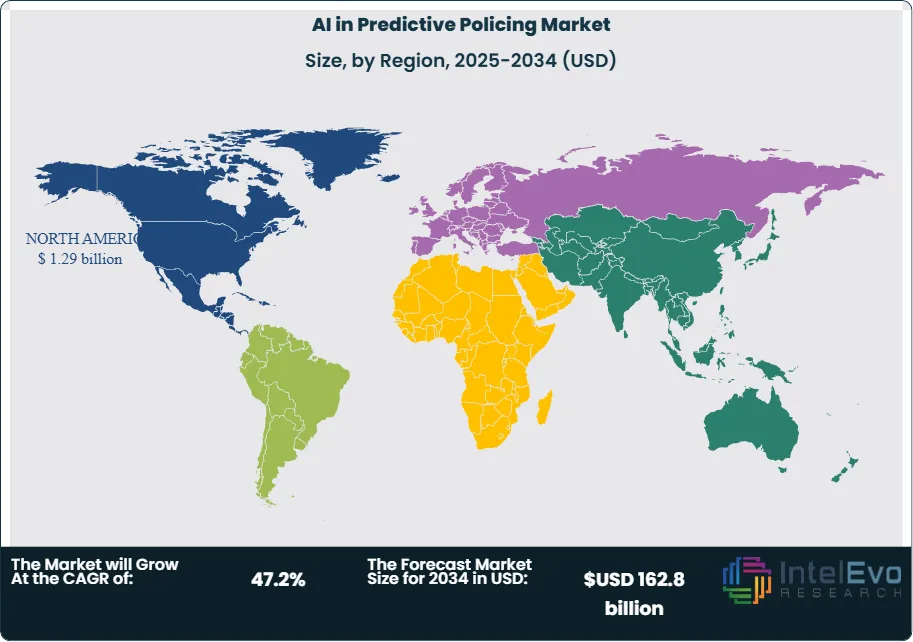

North America accounted for about 46.7% of global revenue in 2024, or roughly USD 1.6 billion, supported by early pilots, federal funding streams, and strong cloud and data-center ecosystems. Europe represents an important second pillar, with an estimated quarter of global spend as governments align public safety modernization programs with tightening algorithmic accountability and data protection rules. Asia Pacific is emerging as the fastest-growing region, driven by smart city initiatives in large metropolitan areas and investments in video analytics, IoT sensors, and edge computing. Investment activity is also rising in the Middle East and Latin America as governments scale national security and safe-city programs.

Regulation and risk management shape the trajectory of this market. Data protection frameworks, civil liberties oversight, and evolving guidelines on the use of biometrics and automated decision support impose strict governance requirements. Agencies and vendors must demonstrate that systems minimize bias, preserve due process, and keep humans in the loop for sensitive decisions. This imperative creates opportunity for transparent, auditable, and privacy-enhancing AI architectures that can deliver accurate predictions while sustaining public trust and meeting investor expectations for responsible growth.

, By Deployment Mode (Cloud-Based, On-Premises), By Organization Size (Large Enterprises, SMEs), By Technology (Machine Learning, Deep Learning, NLP, Computer Vision), By Vertical & Region – Industry Overview, Market Dynamics, Ethical & Regulatory Landscape, Competitive Strategies, Emerging Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global market for AI in predictive policing grows from USD 4.1 billion in 2025 to USD 162.8 billion by 2034, reflecting a 47.2% CAGR, 2026-2034. This expansion signals rapid scaling of algorithmic tools across public safety and adjacent risk domains.

- Segment Dominance: Solution offerings dominate with 78.5% share, 2024 and generate an estimated: 2.7 billion USD, 2024 in revenue as agencies prioritize integrated platforms over point tools. This dominance underscores preference for end-to-end analytics suites that unify ingestion, modeling, and operational deployment.

- Segment Dominance: On-premises deployments account for 66.7% of spending, 2024, while large enterprises hold 70.7% share, 2024 as they scale AI-enabled risk management and investigative analytics. This structure indicates that data sovereignty, control, and established IT capacity still favor in-house environments.

- Driver: Demand from Banking, Financial Services, and Insurance, which captures 34.6% share, 2024, and adoption of NLP technologies with 36.8% share, 2024 drive sustained investment in AI-based surveillance, fraud detection, and investigative workflows. These sectors require high-volume, real-time decisioning and thus anchor early large-scale deployments.

- Restraint: High implementation and governance costs, including model validation and compliance, act as a brake on broader diffusion with investments in oversight and risk functions at estimated: 0.8 billion USD, 2024. Concerns about data privacy and ethical use further slow uptake among resource-constrained agencies.

- Opportunity: Expanding adoption among mid-sized agencies, regulated industries, and cross-border intelligence-sharing programs offers incremental revenue potential of estimated: 25.0 billion USD, 2030. Vendors that package modular, lower-cost offerings around core analytics engines can unlock new addressable segments beyond current 3.4 billion USD, 2024 spend.

- Trend: Vendors intensify focus on explainable NLP and multimodal models, with estimated: 55.0% of new deployments, 2030 incorporating advanced transparency and auditability features compared with a baseline of 36.8%, 2024 NLP share. This evolution aligns AI in policing with tightening governance expectations.

- Regional Analysis: North America leads with 46.7% share, 2024 and 1.6 billion USD, 2024 in revenue, while the US alone contributes 1.29 billion USD, 2024 and is set to expand at 45.8% CAGR, 2024-2034. Other regions collectively contribute an estimated: 1.8 billion USD, 2024 as adoption broadens across Europe, Asia Pacific, and emerging markets.

By Type

High performance concrete continues to gain attention in 2025 as construction firms look for durable materials that support long service life and reduced maintenance. Demand rises in large infrastructure programs where strength and resistance to harsh environments influence procurement decisions. Countries investing in transportation, energy grids, and public facilities report a steady shift toward mixes engineered for higher compressive strength and better load distribution. Market estimates show high performance concrete accounting for a growing share of material specifications as budgets tighten and asset owners seek predictable lifecycle costs.

Self-consolidating concrete also expands its role across projects where improved flowability and uniform placement help reduce labor. Contractors in Asia Pacific and Europe report adoption rates rising above 20 percent in large urban builds, supported by productivity gains and fewer structural defects. Automated batching systems and quality-controlled admixtures improve consistency, which encourages wider use in high-density reinforcement applications.

Other concrete types remain relevant for specialized needs such as lightweight elements, architectural finishes, and rapid-setting works. These categories grow steadily as manufacturers broaden product portfolios to meet performance codes across residential, commercial, and industrial environments. Consistent investment in additives and material science indicates further diversification of this segment through 2030.

By Application

Pavers continue to drive significant demand as cities invest in streetscape upgrades and climate-resilient surfaces. Municipal budgets in North America and Europe allocate increasing shares to materials that support permeability targets and pedestrian-friendly designs. The market benefits from rising urban redevelopment projects, where engineered concrete pavers deliver durability and aesthetic uniformity.

Retaining walls maintain a strong position due to expanding hillside development and soil stabilization requirements. Adoption grows in transportation corridors where slope failures pose operational risks. Many governments prioritize resilient construction after recent flood events, and this shifts attention toward reinforced and modular wall systems that reduce long-term maintenance.

Other applications such as barriers, precast components, and utility structures also gain traction as contractors standardize on materials with predictable performance. The shift toward mechanized installation and digital design tools further pushes adoption across public and private projects.

By End-Use

Residential building activity remains a major contributor to concrete demand as urban expansion accelerates. Developers focus on multi-family units and mixed-use complexes that require consistent quality and shorter project timelines. Prefabricated concrete elements gain interest in 2025 as builders target cost control and reliable turnaround.

Commercial construction shows steady growth, supported by logistics hubs, office redevelopment, and data center expansion. These projects rely heavily on high-strength mixes and self-consolidating concrete for structural cores and large-span floors. Analysts expect sustained spending across retail, warehousing, and institutional assets through 2030.

Industrial facilities such as manufacturing plants and energy installations add another layer of demand. Many require specialized floors, containment areas, and high-load foundations. As global supply chains reposition, new industrial zones across Asia and parts of the Middle East continue to drive concrete consumption.

By Region

North America maintains a leading position in 2025 due to consistent infrastructure spending and strong regulatory compliance standards. The United States accelerates upgrades to highways, ports, and public buildings, reinforcing demand for advanced concrete mixes with higher strength and reliability. Canada follows similar investment patterns across transportation and utilities.

Europe posts stable growth as countries implement energy-efficiency targets and resilience mandates for buildings. Germany, France, and the Nordics invest heavily in retrofit programs and transit modernization, which increases procurement of specialized concrete materials.

Asia Pacific remains the fastest-expanding market, driven by urban population growth and large-scale industrialization. China, India, and Southeast Asian economies allocate significant budgets to transportation corridors, renewable energy facilities, and residential developments. This region is expected to capture the largest volume gains through 2030.

Latin America and the Middle East Africa display selective but rising demand. Infrastructure concessions, mining projects, and industrial expansion drive concrete requirements, while government programs focus on long-term structural resilience and improved construction standards.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Solutions

- Financial Analytics

- Risk Analytics

- Marketing Analytics

- Sales Analytics

- Customer Analytics

- Web and Social Media Analytics

- Supply chain Analytics

- Network Analytics

- Services

- Professional Services

- Consulting

- Deployment and Integration

- Support and Maintenance

- Managed Services

By Deployment Mode

- Cloud

- On-premises

By Organization Size

- Large enterprises

- Small and medium-sized enterprises (SMEs)

By Technology

- Natural Language Processing (NLP)

- Computer Vision

- Machine Learning

- Deep Learning

- Others (Reinforcement Learning, Neural Networks, etc.)

By Vertical

- BFSI

- Manufacturing

- Retail and eCommerce

- Government and Defense

- Healthcare and Life Sciences

- Energy and Utilities

- Telecommunications and IT

- Transportation and Logistics

- Media and Entertainment

- Travel and Hospitality

- Other Verticals

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.1 Billion |

| Forecast Revenue (2034) | USD 162.8 billion |

| CAGR (2025-2034) | 47.2% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering (Solutions, Services, Managed Services), By Deployment Mode (Cloud, On-premises), By Organization Size (Large enterprises, Small and medium-sized enterprises (SMEs)), By Technology (Natural Language Processing (NLP), Computer Vision, Machine Learning, Deep Learning, Others (Reinforcement Learning, Neural Networks, etc.)), By Vertical (BFSI, Manufacturing, Retail and eCommerce, Government and Defense, Healthcare and Life Sciences, Energy and Utilities, Telecommunications and IT, Transportation and Logistics, Media and Entertainment, Travel and Hospitality, Other Verticals) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Dataminr, ThirdEye Labs (acquired by Standard AI), SoundThinking Inc. (formerly ShotSpotter Inc.), Palantir Technologies Inc., Kaseware Inc., Microsoft Corporation, MIM.ai, International Business Machines Corporation (IBM), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-Based, On-Premises), By Organization Size (Large Enterprises, SMEs), By Technology (Machine Learning, Deep Learning, NLP, Computer Vision), By Vertical & Region – Industry Overview, Market Dynamics, Ethical & Regulatory Landscape, Competitive Strategies, Emerging Trends & Forecast 2026–2034")

, By Deployment Mode (Cloud-Based, On-Premises), By Organization Size (Large Enterprises, SMEs), By Technology (Machine Learning, Deep Learning, NLP, Computer Vision), By Vertical & Region – Industry Overview, Market Dynamics, Ethical & Regulatory Landscape, Competitive Strategies, Emerging Trends & Forecast 2026–2034")

, By Deployment Mode (Cloud-Based, On-Premises), By Organization Size (Large Enterprises, SMEs), By Technology (Machine Learning, Deep Learning, NLP, Computer Vision), By Vertical & Region – Industry Overview, Market Dynamics, Ethical & Regulatory Landscape, Competitive Strategies, Emerging Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI in Predictive Policing Market?

The AI in Predictive Policing Market is projected to grow from USD 4.1 billion in 2025 to USD 162.8 billion by 2034, expanding at a CAGR of 47.2% during 2026–2034, driven by AI-powered crime forecasting, real-time risk assessment, smart city integration, and data-driven law enforcement strategies.

Who are the major players in the AI in Predictive Policing Market?

Dataminr, ThirdEye Labs (acquired by Standard AI), SoundThinking Inc. (formerly ShotSpotter Inc.), Palantir Technologies Inc., Kaseware Inc., Microsoft Corporation, MIM.ai, International Business Machines Corporation (IBM), Others

Which segments covered the AI in Predictive Policing Market?

By Offering (Solutions, Services, Managed Services), By Deployment Mode (Cloud, On-premises), By Organization Size (Large enterprises, Small and medium-sized enterprises (SMEs)), By Technology (Natural Language Processing (NLP), Computer Vision, Machine Learning, Deep Learning, Others (Reinforcement Learning, Neural Networks, etc.)), By Vertical (BFSI, Manufacturing, Retail and eCommerce, Government and Defense, Healthcare and Life Sciences, Energy and Utilities, Telecommunications and IT, Transportation and Logistics, Media and Entertainment, Travel and Hospitality, Other Verticals)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI in Predictive Policing Market

Published Date : 02 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date