- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI in Radiology Market Size, Share & Forecast | CAGR 27.2%

Global AI in Radiology Market Size, Share, Growth Analysis By Modality (CT, MRI, X-Ray, Mammography, Ultrasound, Nuclear Imaging), By Application (Disease Detection, Workflow Triage, Image Reconstruction, Quantitative Analysis, Reporting Automation), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By End-User, AI Diagnostic Imaging Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 2.14 Billion | USD 18.73 Billion | 27.2% | North America, 38.5% |

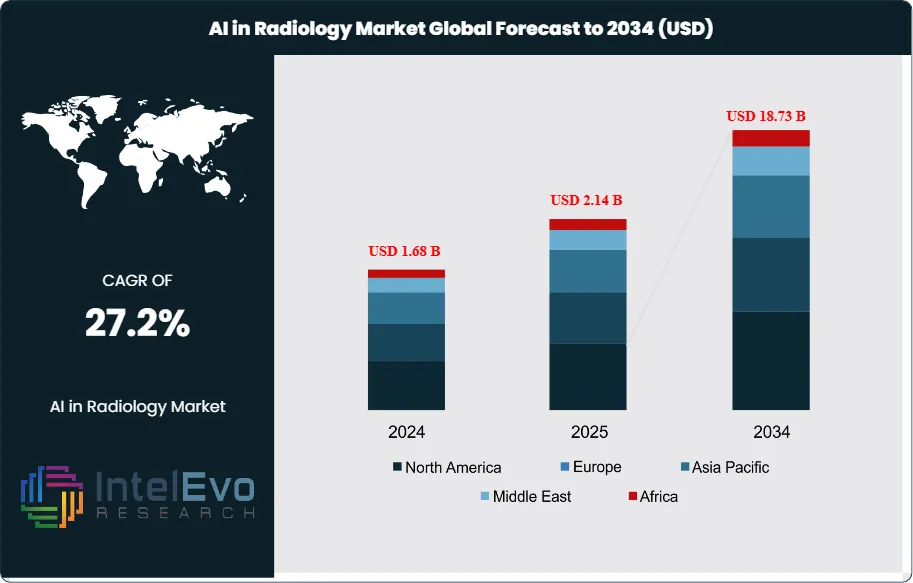

The AI in Radiology Market was valued at approximately USD 1.68 Billion in 2024 and reached USD 2.14 Billion in 2025. The market is projected to grow to USD 18.73 Billion by 2034, expanding at a CAGR of 27.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 16.59 Billion over the analysis period, reflecting the accelerating clinical integration of machine learning algorithms across diagnostic imaging workflows, the expansion of FDA-authorized AI radiology devices, and sustained reimbursement tailwinds from CMS AI-specific coding pathways.

Get More Information about this report -

Request Free Sample ReportThe AI in radiology market has evolved from pilot-stage research into mainstream clinical practice, with the FDA having authorized over 950 AI-enabled medical devices as of 2025, of which approximately 78% are specific to radiology applications including chest X-ray, mammography, CT, and MRI interpretation. The CMS introduction of the New Technology Add-on Payment for AI-based stroke detection in 2020 and the subsequent expansion of AI-specific CPT codes through 2025 have materially reduced hospital adoption friction by establishing clear reimbursement pathways. Teleradiology service providers have been among the earliest institutional adopters, integrating AI triage algorithms into reading workflows to prioritize critical findings such as intracranial hemorrhage, pulmonary embolism, and large vessel occlusion within minutes of image acquisition.

Regulatory signals shaping the AI in radiology market are intensifying. The FDA's predetermined change control plan framework, finalized in 2024, now permits AI model updates without requiring full resubmission, accelerating the deployment of continuously learning algorithms in clinical practice. The EU AI Act classifies radiology AI as high-risk under Annex III, mandating conformity assessment, post-market surveillance, and bias monitoring that is expected to create a regional compliance services sub-market of USD 0.28 Billion by 2028. Compliance with the FDA's Good Machine Learning Practice principles is becoming a standard procurement criterion among academic medical centers and integrated delivery networks.

Technology convergence is a structural feature of the AI in radiology market in 2025. Foundation model architectures are being adapted for medical imaging through vision-language pre-training on paired radiology reports and DICOM studies, enabling zero-shot performance on previously unseen pathology categories. Workflow-integrated AI deployment, embedded within PACS platforms from vendors such as GE HealthCare, Siemens Healthineers, and Philips, has replaced standalone kiosk-style AI viewers as the dominant deployment pattern. Radiologist workload pressure, with an estimated global shortage exceeding 42,000 radiologists in 2025 and reading volumes increasing by 6% annually, creates a structural productivity demand that positions AI triage and workflow prioritization as clinically necessary rather than discretionary.

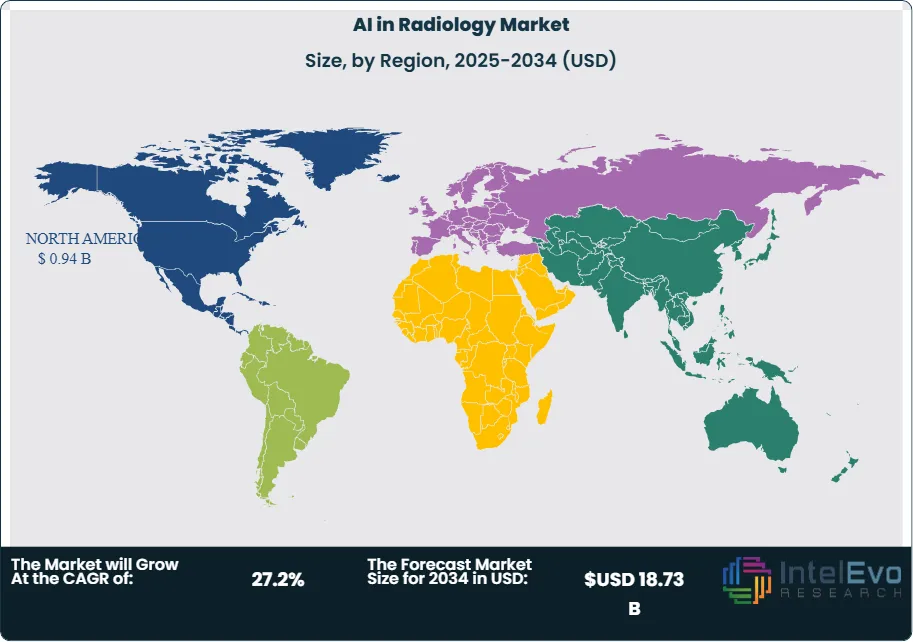

North America retains clear leadership at 43.8% share of the AI in radiology market in 2025, underpinned by FDA pathway maturity, CMS reimbursement, and concentration of imaging center operators such as RadNet and Radiology Partners that have standardized AI deployment across nationally distributed imaging networks. Asia Pacific is the fastest-growing region, driven by Chinese National Medical Products Administration approvals, Japanese PMDA pathways for AI devices, and Indian hospital chain expansion. The AI in radiology market trajectory through 2034 will be shaped by multi-organ foundation model deployment, hospital-at-home imaging workflows, and the transition of AI from assistive reading to autonomous screening in specific high-volume, well-defined indications such as diabetic retinopathy and screening mammography.

, By Application (Disease Detection, Workflow Triage, Image Reconstruction, Quantitative Analysis, Reporting Automation), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By End-User, AI Diagnostic Imaging Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global AI in radiology market was valued at USD 2.14 Billion in 2025 and is projected to reach USD 18.73 Billion by 2034, expanding at a CAGR of 27.2% during the 2026–2034 forecast period.

- Segment Dominance: By modality, the computed tomography (CT) segment leads with approximately 34.6% market share in 2025, driven by high scan volumes, time-critical indications in emergency imaging, and deep AI algorithm maturity for neurological and thoracic applications.

- Segment Dominance: By application, disease detection and diagnosis represents the largest application segment with 48.2% market share in 2025, equivalent to USD 1.03 Billion in annual revenue, anchored by FDA-cleared algorithms for stroke, pulmonary embolism, and lung nodule detection.

- Driver: A global radiologist shortage exceeding 42,000 specialists in 2025 combined with imaging volume growth of 6% annually creates structural productivity demand that is accelerating AI triage adoption across 68% of US academic medical centers.

- Restraint: Integration complexity with legacy PACS and RIS infrastructure adds USD 180,000 to USD 450,000 in implementation costs per hospital site, constraining adoption among community hospitals and smaller imaging centers with limited IT capacity.

- Opportunity: Expansion into emerging market hospital networks presents an addressable opportunity of USD 4.2 Billion within the AI in radiology market by 2034, as cloud-native deployment models lower infrastructure barriers across India, Southeast Asia, Latin America, and the Middle East.

- Trend: Foundation model-based multi-pathology algorithms have reached 28% of new FDA clearances in 2025, up from 6% in 2022, signaling a structural shift from narrow single-indication algorithms to general-purpose radiology AI platforms.

- Regional Analysis: North America leads the AI in radiology market with 43.8% share in 2025, equivalent to USD 0.94 Billion in annual revenue, driven by FDA regulatory clarity, CMS reimbursement codes, and integrated delivery network procurement standardization.

Competitive Landscape Overview

The AI in radiology market is moderately consolidated, with the top four providers, GE HealthCare, Siemens Healthineers, Philips, and Canon Medical Systems, collectively holding approximately 44% combined market share in 2025, predominantly through AI-embedded imaging equipment and PACS integration. Pure-play AI radiology specialists including Aidoc, Viz.ai, RapidAI, and Annalise.ai have established defensible positions at the clinical application layer, particularly in time-critical triage workflows. Competition is primarily clinical-evidence-driven, with FDA clearance depth, peer-reviewed validation studies, and real-world outcome data serving as primary procurement evaluation criteria. M&A activity has intensified materially since 2024, with several large imaging OEMs acquiring AI specialists to internalize algorithm development and protect platform positioning.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| GE HealthCare | USA | Leader | Edison AI / Critical Care Suite | North America, Europe | Launched Edison True PACS with integrated AI orchestration, Feb 2025 |

| Siemens Healthineers | Germany | Leader | AI-Rad Companion | Europe, Global | Expanded AI-Rad Companion to 15 organ systems; Q2 2025 |

| Koninklijke Philips | Netherlands | Leader | Radiology Smart Workflow | Europe, North America | Launched CT Smart Workflow 2.0 with AI auto-protocol, Mar 2025 |

| Canon Medical Systems | Japan | Challenger | Automation Platform AI | Asia Pacific, Europe | Introduced Altivity AI portfolio for multi-modality analysis, Jan 2025 |

| Aidoc Medical | Israel | Challenger | aiOS Clinical AI Platform | North America, Europe | Closed USD 110 Million Series E financing, May 2025 |

| Viz.ai | USA | Challenger | Viz LVO / Viz ICH | North America | Received FDA clearance for Viz Aneurysm; Sep 2025 |

| RapidAI | USA | Niche Player | Rapid Stroke Suite | North America, EMEA | Acquired Netherlands-based Icometrix radiology AI unit, Nov 2024 |

| Annalise.ai | Australia | Niche Player | Annalise Enterprise CXR/CTB | Asia Pacific, Europe | Received FDA clearance for 130+ findings chest X-ray AI, Apr 2025 |

By Modality

The AI in radiology market by modality divides into computed tomography, magnetic resonance imaging, X-ray, ultrasound, mammography, and nuclear imaging. Computed tomography leads with 34.6% share in 2025, generating USD 0.74 Billion in annual revenue, reflecting the clinical criticality and high volume of CT studies in emergency, oncology, and neurological applications. The density of FDA-cleared CT-specific algorithms, particularly for stroke detection, pulmonary embolism, and lung nodule characterization, has made CT the most AI-mature modality. Magnetic resonance imaging accounts for 22.4% share at USD 0.48 Billion, with AI applications concentrated in accelerated acquisition (reducing scan times by 30 to 50%), automated quantification of brain volumetrics, and prostate MRI lesion detection. X-ray represents 18.7% share at USD 0.40 Billion, driven by chest X-ray AI deployment in screening and emergency contexts, an application category where Annalise.ai, Lunit, and Qure.ai have established notable positions. Mammography accounts for 11.2% share at USD 0.24 Billion, with AI density assessment and lesion detection reimbursed under CMS coding updates and increasingly integrated into standard screening workflows. Ultrasound holds 8.3% share at USD 0.18 Billion, with point-of-care AI systems from Butterfly Network, GE HealthCare, and Philips extending AI assistance into non-radiologist clinician workflows. Nuclear imaging including PET and SPECT accounts for the remaining 4.8% at USD 0.10 Billion, with applications in oncology staging and cardiac perfusion quantification.

By Application

The AI in radiology market by application spans disease detection and diagnosis, workflow triage and prioritization, image acquisition and reconstruction, quantitative analysis, and reporting automation. Disease detection and diagnosis leads with 48.2% share in 2025 at USD 1.03 Billion, encompassing algorithms for stroke, pulmonary embolism, lung cancer, breast cancer, fracture detection, and cardiac pathology. Workflow triage and prioritization represents 19.4% share at USD 0.41 Billion, where time-critical algorithms redirect emergent cases to the top of radiologist reading worklists, demonstrably reducing door-to-treatment times by an average of 39 minutes in stroke care pathways. Image acquisition and reconstruction AI accounts for 14.6% share at USD 0.31 Billion, with deep learning reconstruction algorithms reducing radiation dose by 30 to 60% in CT and accelerating MRI acquisition times materially. Quantitative analysis represents 11.3% share at USD 0.24 Billion, supporting biomarker extraction for oncology, neurology, and cardiology use cases. Reporting automation and structured reporting AI accounts for 6.5% share at USD 0.14 Billion, a category growing rapidly as natural language generation models integrate into radiology information systems.

By Deployment Mode

The AI in radiology market by deployment mode divides into cloud-based, on-premise, and hybrid configurations. On-premise deployment commands 46.8% share in 2025 at USD 1.00 Billion, reflecting the hospital IT security posture favoring local data residency for Protected Health Information under HIPAA and equivalent frameworks. On-premise deployment remains the preferred configuration among large academic medical centers and integrated delivery networks with established infrastructure. Cloud-based deployment represents 33.2% share at USD 0.71 Billion and is the fastest-growing deployment mode, enabled by HIPAA-compliant cloud services from AWS HealthLake, Google Cloud Healthcare API, and Microsoft Azure Health Data Services. Cloud-based models are particularly attractive for ambulatory imaging centers, mobile imaging providers, and emerging market deployments where infrastructure investment barriers are prohibitive. Hybrid deployment accounts for 20.0% share at USD 0.43 Billion, combining on-premise inference for sensitive workflows with cloud-based training and model management. Hybrid architecture is becoming the preferred long-term infrastructure pattern among multi-site health systems seeking the performance benefits of local inference with the centralized governance advantages of cloud model lifecycle management.

By End-User

The AI in radiology market by end-user spans hospitals and health systems, diagnostic imaging centers, teleradiology service providers, academic and research institutions, and ambulatory surgical centers. Hospitals and health systems lead with 58.4% share in 2025 at USD 1.25 Billion, supported by integrated delivery network standardization of AI procurement across owned radiology practices. Diagnostic imaging centers represent 22.1% share at USD 0.47 Billion, with large US operators including RadNet, Radiology Partners, and Alliance HealthCare Services having implemented enterprise-wide AI deployment strategies. Teleradiology service providers account for 11.5% share at USD 0.25 Billion, with AI triage capabilities functioning as a core competitive differentiator in teleradiology service-level agreements. Academic and research institutions hold 5.3% share at USD 0.11 Billion, primarily consuming AI as part of research workflows and algorithmic validation programs. Ambulatory surgical centers and other settings account for the remaining 2.7% at USD 0.06 Billion, a segment poised for rapid growth as point-of-care imaging AI extends beyond traditional radiology department boundaries.

Regional Analysis

North America

North America dominates the AI in radiology market with 43.8% share in 2025, equivalent to USD 0.94 Billion in annual revenue. The United States accounts for approximately 92% of the regional total at USD 0.86 Billion, driven by the concentration of FDA-cleared AI radiology devices, CMS reimbursement pathways, and the consolidation of imaging services under national imaging operators. The FDA's Digital Health Center of Excellence has authorized over 740 radiology-specific AI devices through 2025, creating the world's deepest regulatory-validated AI radiology ecosystem. The CMS introduction of the NTAP for AI-based stroke detection established a reimbursement template that has since extended to multiple AI-specific CPT codes covering cardiac CT FFR analysis, coronary calcium scoring, and AI-assisted mammography. Canada contributes approximately USD 0.06 Billion, with activity concentrated in provincial health authority AI pilots and the Ontario Health Technology Assessment framework providing evaluation pathways. Mexico represents a smaller but growing USD 0.02 Billion market, with private hospital chains including Grupo Angeles and Hospital ABC investing in AI-enabled imaging to differentiate on service quality. Radiologist shortage pressures are acute across North America, with the American College of Radiology documenting a 3,000-radiologist gap in the US alone, sustaining structural demand for AI productivity tools. Major integrated delivery networks including Mayo Clinic, Mass General Brigham, and Cleveland Clinic have established enterprise AI governance frameworks that function as templates for broader hospital system adoption.

Europe

Europe accounts for 27.5% of the global AI in radiology market in 2025, generating USD 0.59 Billion in annual revenue. Germany leads the European market at an estimated USD 0.16 Billion, driven by university hospital adoption, the dense domestic medical device manufacturing base anchored by Siemens Healthineers, and structured reimbursement under the InnoFonds innovation fund that has supported AI radiology pilots at scale. The United Kingdom follows at USD 0.13 Billion, where NHS England's AI in Health and Care Awards have funded AI radiology deployment across NHS trusts, with particular density of deployment in chest X-ray triage and stroke imaging. France contributes approximately USD 0.09 Billion, supported by the France 2030 health technology investment plan and growing public-sector procurement through centrale d'achat mechanisms. The Netherlands accounts for approximately USD 0.06 Billion, functioning as a European AI radiology innovation hub anchored by the Radboud University Medical Center and several venture-backed AI startups. The EU AI Act's high-risk classification for radiology AI has created compliance workload that is estimated to add 18 to 22% to product deployment timelines but concurrently reinforces a preference for established, documented vendors among European hospital procurement committees. The European Federation of Radiological Societies has established an AI evaluation framework that functions as a de facto procurement standard across multiple European health systems.

Asia Pacific

Asia Pacific represents 19.6% of the AI in radiology market in 2025 at USD 0.42 Billion and is the fastest-growing region, projected at a CAGR of 31.4% through 2034. China is the largest country market in the region at an estimated USD 0.17 Billion, supported by National Medical Products Administration AI approval pathways and domestic champion AI companies including Infervision, Yitu Healthcare, and Deepwise. The Chinese government has designated AI-enabled diagnostics as a priority technology under the Healthy China 2030 initiative, with provincial reimbursement pilots underway in Zhejiang, Guangdong, and Shanghai. Japan contributes approximately USD 0.11 Billion, with PMDA regulatory pathways for AI medical devices maturing rapidly and Canon Medical Systems and Fujifilm driving domestic equipment-embedded AI adoption. India is the third-largest country market at approximately USD 0.07 Billion, growing at an estimated 34.2% CAGR as hospital chains including Apollo Hospitals, Fortis Healthcare, and Max Healthcare deploy AI to address an acute radiologist shortage of approximately 2 radiologists per 100,000 population. Qure.ai, the India-headquartered AI radiology company, has achieved global deployment distribution and represents a notable emerging market AI exporter. South Korea at approximately USD 0.04 Billion rounds out the top four, anchored by Lunit's domestic and international deployment success in mammography and chest X-ray AI. Australia and Southeast Asian markets are expanding rapidly with cloud-native AI deployment models.

Latin America

Latin America accounts for 5.3% of the global AI in radiology market in 2025 at USD 0.11 Billion, representing an emerging but rapidly accelerating adoption environment. Brazil leads the region at an estimated USD 0.06 Billion, with Diagnósticos da América (DASA), Fleury Group, and Alliar operating nationally distributed imaging networks that have standardized AI deployment for stroke triage and mammography. The Brazilian ANVISA regulatory pathway for AI medical devices has matured materially since 2023, reducing approval timelines and enabling broader vendor access. Mexico contributes approximately USD 0.03 Billion, with Grupo Angeles and Hospital ABC leading private-sector AI adoption. Argentina accounts for approximately USD 0.02 Billion with university-affiliated hospital adoption driving market activity. Currency volatility and public health system funding constraints limit penetration rates relative to developed markets, but cloud-native deployment models are progressively overcoming infrastructure barriers. The region is projected to grow at a CAGR of 28.9% through 2034 as hospital chain consolidation and digital health investment accelerate.

Middle East and Africa

The Middle East and Africa region represents 3.8% of the AI in radiology market in 2025, generating USD 0.08 Billion in annual revenue. The UAE is the dominant market at approximately USD 0.03 Billion, underpinned by government AI strategy integration with healthcare infrastructure investment, M42 (the merged Mubadala Health and G42 Healthcare entity) operating as a leading regional AI healthcare integrator, and extensive AI deployment across Sheikh Shakhbout Medical City and Cleveland Clinic Abu Dhabi. Saudi Arabia follows at approximately USD 0.02 Billion, with Vision 2030 health sector transformation driving AI procurement through the National Unified Procurement Company and flagship deployments at King Faisal Specialist Hospital and Johns Hopkins Aramco Healthcare. South Africa accounts for approximately USD 0.01 Billion, serving as the primary Sub-Saharan deployment hub with Netcare and Mediclinic private hospital groups leading adoption. The MEA region is projected to grow at a CAGR of 29.6% through 2034, among the highest across all regions, driven by sovereign wealth fund investment in healthcare infrastructure and hyperscaler cloud expansion into regional availability zones that enable cloud-native AI deployment at scale.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Modality

- Computed Tomography (CT)

- Magnetic Resonance Imaging (MRI)

- X-Ray

- Mammography

- Ultrasound

- Nuclear Imaging (PET/SPECT)

By Application

- Disease Detection and Diagnosis

- Workflow Triage and Prioritization

- Image Acquisition and Reconstruction

- Quantitative Analysis

- Reporting Automation

By Deployment Mode

- On-Premise

- Cloud-Based

- Hybrid

By End-User

- Hospitals and Health Systems

- Diagnostic Imaging Centers

- Teleradiology Service Providers

- Academic and Research Institutions

- Ambulatory Surgical Centers and Others

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.14 B |

| Forecast Revenue (2034) | USD 18.73 B |

| CAGR (2025-2034) | 27.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Modality, (Computed Tomography (CT), Magnetic Resonance Imaging (MRI), X-Ray, Mammography, Ultrasound, Nuclear Imaging (PET/SPECT)), By Application, (Disease Detection and Diagnosis, Workflow Triage and Prioritization, Image Acquisition and Reconstruction, Quantitative Analysis, Reporting Automation), By Deployment Mode, (On-Premise, Cloud-Based, Hybrid), By End-User, (Hospitals and Health Systems, Diagnostic Imaging Centers, Teleradiology Service Providers, Academic and Research Institutions, Ambulatory Surgical Centers and Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | GE HEALTHCARE TECHNOLOGIES INC., SIEMENS HEALTHINEERS AG, KONINKLIJKE PHILIPS N.V., CANON MEDICAL SYSTEMS CORPORATION, AIDOC MEDICAL LTD., VIZ.AI, INC., RAPIDAI (IRAS LABS, INC.), ANNALISE.AI PTY LTD., QURE.AI TECHNOLOGIES PVT. LTD., LUNIT INC., ENLITIC, INC., ARTERYS INC. (TEMPUS), ZEBRA MEDICAL VISION (NANOX), SUBTLE MEDICAL, INC., BUTTERFLY NETWORK, INC., HEARTFLOW, INC., BAYER AG (RADIOLOGY), FUJIFILM HOLDINGS CORPORATION, INFERVISION MEDICAL TECHNOLOGY, DEEPWISE HEALTHCARE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Disease Detection, Workflow Triage, Image Reconstruction, Quantitative Analysis, Reporting Automation), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By End-User, AI Diagnostic Imaging Trends & Forecast 2026-2034")

, By Application (Disease Detection, Workflow Triage, Image Reconstruction, Quantitative Analysis, Reporting Automation), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By End-User, AI Diagnostic Imaging Trends & Forecast 2026-2034")

, By Application (Disease Detection, Workflow Triage, Image Reconstruction, Quantitative Analysis, Reporting Automation), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By End-User, AI Diagnostic Imaging Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the AI in Radiology Market?

The Global AI in Radiology Market was valued at USD 1.68 Billion in 2024 and is projected to reach USD 18.73 Billion by 2034, growing at a CAGR of 27.2% from 2026 to 2034, driven by increasing adoption of AI-powered diagnostic imaging, rising demand for automated radiology workflows, advancements in deep learning algorithms, and growing use of AI in early disease detection and precision healthcare.

Who are the major players in the AI in Radiology Market?

GE HEALTHCARE TECHNOLOGIES INC., SIEMENS HEALTHINEERS AG, KONINKLIJKE PHILIPS N.V., CANON MEDICAL SYSTEMS CORPORATION, AIDOC MEDICAL LTD., VIZ.AI, INC., RAPIDAI (IRAS LABS, INC.), ANNALISE.AI PTY LTD., QURE.AI TECHNOLOGIES PVT. LTD., LUNIT INC., ENLITIC, INC., ARTERYS INC. (TEMPUS), ZEBRA MEDICAL VISION (NANOX), SUBTLE MEDICAL, INC., BUTTERFLY NETWORK, INC., HEARTFLOW, INC., BAYER AG (RADIOLOGY), FUJIFILM HOLDINGS CORPORATION, INFERVISION MEDICAL TECHNOLOGY, DEEPWISE HEALTHCARE, Others

Which segments covered the AI in Radiology Market?

By Modality, (Computed Tomography (CT), Magnetic Resonance Imaging (MRI), X-Ray, Mammography, Ultrasound, Nuclear Imaging (PET/SPECT)), By Application, (Disease Detection and Diagnosis, Workflow Triage and Prioritization, Image Acquisition and Reconstruction, Quantitative Analysis, Reporting Automation), By Deployment Mode, (On-Premise, Cloud-Based, Hybrid), By End-User, (Hospitals and Health Systems, Diagnostic Imaging Centers, Teleradiology Service Providers, Academic and Research Institutions, Ambulatory Surgical Centers and Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date