- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

AI in RPA Market Forecast Size, Growth & Automation Trends | 14.9% CAGR

Global AI in RPA Market Size, Share & Analysis By Type (Software, Service), By Deployment Mode (Cloud-based, On-premise), By Organization Size (Large Enterprises, Small & Medium Enterprises), By Application (BFSI, Pharma & Healthcare, Retail & Consumer Goods, Information Technology & Telecom, Communication and Media & Education, Other Applications) Industry Regions & Key Players – Market Architecture, Automation Trends, Competitive Strategies & Forecast 2025–2034

Report Overview

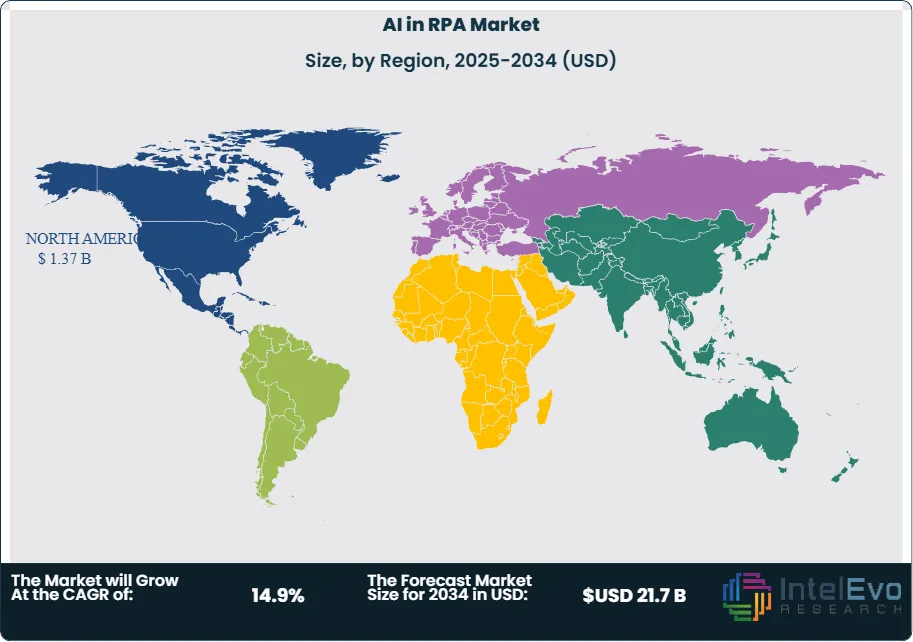

The AI in Robotic Process Automation (RPA) Market is valued at approximately USD 4.9 Billion in 2024 and is projected to reach nearly USD 21.7 Billion by 2034, expanding at a CAGR of around 14.9% during 2025–2034. AI-enabled automation is moving beyond rule-based workflows into intelligent decisioning, autonomous document processing, and predictive operations. As enterprises digitize back-office, finance, HR, and supply-chain functions, AI-driven RPA is becoming a core engine for cost optimization and workforce augmentation. This decade will mark the shift from “bots” to cognitive automation ecosystems, reshaping enterprise productivity worldwide.

Get More Information about this report -

Request Free Sample ReportThis rapid expansion underscores the accelerating convergence of automation and intelligence, as organizations increasingly seek solutions that streamline operations, reduce costs, and unlock new efficiencies. Historically, RPA adoption surged as enterprises sought to automate repetitive, rule-based tasks such as data entry, claims processing, and invoice management. More recently, the integration of artificial intelligence—particularly machine learning, natural language processing (NLP), and computer vision—has transformed RPA from a rules-based tool into a cognitive enabler capable of addressing unstructured data and complex decision-making processes.

The market’s evolution is fueled by several drivers. Demand-side factors include enterprises’ urgent need to boost productivity while containing labor costs, with surveys indicating that over 90% of executives now utilize intelligent automation in some form. Supply-side momentum comes from vendors embedding AI into RPA platforms, enabling capabilities like predictive analytics and sentiment analysis that broaden the scope of automation beyond back-office tasks. Yet challenges remain: the shortage of AI-skilled talent and the complexity of aligning AI algorithms with existing business processes often delay implementation, while integration hurdles and governance risks add layers of uncertainty for adopters.

Technological innovation is at the heart of growth. Deloitte reports that 27% of organizations deploying RPA are simultaneously adopting cognitive automation, highlighting the shift toward intelligent RPA ecosystems. Emerging solutions leverage AI to orchestrate workflows across functions, while advances in digitalization, low-code platforms, and cloud-native architectures make adoption more accessible. AI-powered RPA is particularly transforming customer service, fraud detection, and supply chain optimization, creating measurable ROI for early adopters.

Geographically, North America leads the market, buoyed by robust enterprise digitalization initiatives and heavy investments by major technology players. Europe follows closely, driven by regulatory pressures to enhance compliance and efficiency. Meanwhile, Asia-Pacific is emerging as the fastest-growing region, propelled by digital transformation programs in countries like India and China and a burgeoning ecosystem of startups. For investors, high-growth hotspots lie in sectors such as banking, healthcare, and retail, where automation demand intersects with vast data volumes and the imperative for operational resilience. Together, these dynamics position AI-driven RPA as a transformative force reshaping enterprise productivity worldwide.

, By Deployment Mode (Cloud-based, On-premise), By Organization Size (Large Enterprises, Small & Medium Enterprises), By Application (BFSI, Pharma & Healthcare, Retail & Consumer Goods, Information Technology & Telecom, Communication and Media & Education, Other Applications) Industry Regions & Key Players – Market Architecture, Automation Trends, Competitive Strategies & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global AI in RPA market was valued at USD 4.9 Billion (2024) and is projected to reach USD 21.7 Billion by 2034, registering a 14.9% CAGR (2025–2034), propelled by efficiency mandates, cost takeout, and the shift from rules-based bots to cognitive automation; >90% of executives report using intelligent automation in some capacity.

- Segment Dominance – Component: Software led with >68% revenue share in 2023, reflecting spend on orchestration platforms, model-serving, and bot lifecycle management; services (~32%) remain essential for integration, data engineering, and governance in complex estates.

- Segment Dominance – Deployment Model: On-premise accounted for >78% share in 2023, supported by data-residency and model-risk controls in regulated industries; however, cloud-native AI+RPA is the fastest-rising delivery model, expected to grow at >15% CAGR as vendors expand SaaS offerings and elastic inference.

- Driver: Enterprise scaling is accelerating adoption—large enterprises captured ~66% of 2023 spend, while 27% of RPA adopters are layering in cognitive tools (NLP, computer vision, ML), expanding automation from structured to unstructured workflows and lifting throughput and straight-through processing.

- Restraint: Integration complexity and the AI-skills gap slow rollouts; aligning models with legacy processes and controls can extend initial deployments by 4–6 months in highly regulated settings, raising near-term implementation costs and delaying time-to-value.

- Opportunity: BFSI is the largest and steadiest demand pool with ~29% share (2023); driven by KYC/AML, fraud, and claims automation, the segment is poised to exceed ~USD 3.5 billion by 2033 at an estimated ~14–15% CAGR, aided by document-intensive use cases.

- Trend: GenAI-infused RPA is moving mainstream as vendors such as UiPath, Microsoft, Automation Anywhere, and SS&C Blue Prism embed LLMs, retrieval-augmented generation, and vision to enable natural-language task creation, autonomous exception handling, and analytics-driven orchestration.

- Regional Analysis: North America led with ~28% share (USD 0.9 billion) in 2023, supported by mature digital cores and stringent governance; Asia-Pacific is the fastest-growing region (expected ~15–18% CAGR) on the back of cloud adoption in India, China, and Southeast Asia, while Europe expands steadily under compliance-driven automation.

By Type

As of 2025, software continues to anchor spend in AI-enabled RPA, accounting for roughly two-thirds of global revenue (down modestly from ~68% in 2023 as services expand). Growth is propelled by platform consolidation and native AI features—LLM-based copilots, embedded NLP/computer vision, and policy-aware orchestration—that enable automation of unstructured, judgment-intensive work. Leading suites (e.g., UiPath, Microsoft Power Automate, Automation Anywhere, SS&C Blue Prism) now ship with prompt-to-flow design, integrated model hubs, and analytics, compressing time-to-value and lifting bot reliability.

Services (consulting, integration, managed operations) are rising faster than the overall market as enterprises scale from pilot to production. Complexities—data governance, model risk management, API/legacy connectivity, and change management—drive demand for systems integrators and MSPs. From 2025 onward, managed services tied to outcome SLAs (e.g., straight-through processing rates, first-contact resolution) and continuous model monitoring are expected to capture a growing share, particularly in regulated sectors.

By Deployment Mode

In 2025, on-premise remains prevalent in highly regulated environments (banking, insurance, public sector, healthcare), sustained by data-residency mandates, deterministic latency, and tighter control over model/version governance. Many large RPA estates continue to run on self-managed infrastructure where security tooling and audit workflows are already standardized.

That said, cloud-based deployments are the fastest-growing model and are expected to outpace overall market CAGR through 2030+. Elastic inference for AI services, lower upfront cost, and continuous delivery of features (e.g., new connectors, foundation-model upfits) are shifting new workloads to SaaS and VPC-managed options. Hybrid patterns—bots near systems of record with AI services in cloud—are becoming the default in multinational rollouts to balance sovereignty and agility.

By Organization Size

Large enterprises still command the majority of spending (historically ~66% in 2023; similar mix in 2025) because they operate the scale and process diversity that benefit most from cognitive automation. These organizations prioritize end-to-end automation (order-to-cash, claims, KYC/AML, HR case management) and fund platform standardization, CoEs, and governance programs that enable multi-country deployments and stringent compliance.

SMEs are closing the gap thanks to simplified pricing, prebuilt templates, and genAI assistants that reduce design and maintenance overhead. Cloud delivery and partner-led packages (industry playbooks with curated models and connectors) are unlocking adoption in midmarket finance, healthcare providers, logistics, and professional services, where rapid payback and minimal IT lift are decisive.

By Application

BFSI remains the largest vertical—about ~28–30% of 2025 spend—driven by document-heavy workflows and regulatory reporting. Banks and insurers are expanding from back-office automation to front-office augmentation (collections, underwriting triage, claims FNOL), with measurable improvements in cycle time and auditability. Information Technology & Telecom follows, leveraging bots for service desk, billing reconciliation, and network ops, often pairing genAI with event automation for autonomous remediation.

Momentum is accelerating in Pharma & Healthcare (prior authorization, revenue cycle, pharmacovigilance) and Retail & Consumer Goods (catalog enrichment, personalization ops, invoice matching), both expected to outgrow the market average as unstructured text/vision tasks become automatable. Communication & Media & Education deploy AI-RPA for content ops, rights management, and student services, while Other applications span manufacturing quality, logistics paperwork, and energy trading confirmations—areas where exception-handling and traceability are critical.

By Region

North America retains market leadership in 2025 (historically ~28% share; ~USD 0.9B in 2023), underpinned by mature digital cores, AI talent depth, and early adoption of model governance. Europe scales steadily, guided by compliance-first rollouts and strong uptake in financial services and public administration, with growth shaped by data-protection and AI-risk frameworks.

Asia Pacific is the fastest-growing region through the late 2020s, propelled by cloud adoption, Greenfield digital programs, and cost-to-serve pressure in India, Southeast Asia, and China. Latin America and Middle East & Africa are emerging investment corridors where shared-services modernization and government digitalization are catalyzing demand; partnerships with regional SIs and hyperscalers are pivotal to navigate data localization and talent constraints. Overall, APAC’s trajectory positions it to narrow the share gap with North America by 2030 while Europe maintains a high-compliance, multi-industry expansion path.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Type

- Software

- Service

By Deployment Mode

- Cloud-based

- On-premise

By Organization Size

- Large Enterprises

- Small & Medium Enterprises

By Application

- BFSI

- Pharma & Healthcare

- Retail & Consumer Goods

- Information Technology & Telecom

- Communication and Media & Education

- Other Applications

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 4.9 B |

| Forecast Revenue (2034) | USD 21.7 B |

| CAGR (2024-2034) | 14.9% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Software, Service), By Deployment Mode (Cloud-based, On-premise), By Organization Size (Large Enterprises, Small & Medium Enterprises), By Application (BFSI, Pharma & Healthcare, Retail & Consumer Goods, Information Technology & Telecom, Communication and Media & Education, Other Applications) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | UiPath, FPT Software, Pegasystems, NICE, EdgeVerve Systems Ltd., Automation Anywhere, OnviSource, Inc., Blue Prism, NTT Advanced Technology Corp., KOFAX, Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-based, On-premise), By Organization Size (Large Enterprises, Small & Medium Enterprises), By Application (BFSI, Pharma & Healthcare, Retail & Consumer Goods, Information Technology & Telecom, Communication and Media & Education, Other Applications) Industry Regions & Key Players – Market Architecture, Automation Trends, Competitive Strategies & Forecast 2025–2034")

, By Deployment Mode (Cloud-based, On-premise), By Organization Size (Large Enterprises, Small & Medium Enterprises), By Application (BFSI, Pharma & Healthcare, Retail & Consumer Goods, Information Technology & Telecom, Communication and Media & Education, Other Applications) Industry Regions & Key Players – Market Architecture, Automation Trends, Competitive Strategies & Forecast 2025–2034")

, By Deployment Mode (Cloud-based, On-premise), By Organization Size (Large Enterprises, Small & Medium Enterprises), By Application (BFSI, Pharma & Healthcare, Retail & Consumer Goods, Information Technology & Telecom, Communication and Media & Education, Other Applications) Industry Regions & Key Players – Market Architecture, Automation Trends, Competitive Strategies & Forecast 2025–2034")

Frequently Asked Questions

How big is the AI in RPA Market?

The AI in RPA Market will rise from USD 4.9B in 2024 to USD 21.7B by 2034, driven by intelligent automation, cognitive workflows, and enterprise demand for scalable digital operations.

Who are the major players in the AI in RPA Market?

UiPath, FPT Software, Pegasystems, NICE, EdgeVerve Systems Ltd., Automation Anywhere, OnviSource, Inc., Blue Prism, NTT Advanced Technology Corp., KOFAX, Inc., Other Key Players

Which segments covered the AI in RPA Market?

By Type (Software, Service), By Deployment Mode (Cloud-based, On-premise), By Organization Size (Large Enterprises, Small & Medium Enterprises), By Application (BFSI, Pharma & Healthcare, Retail & Consumer Goods, Information Technology & Telecom, Communication and Media & Education, Other Applications)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date