AI in Smartphone & Wearable Market Size, Share & Growth | CAGR 30.8%

Global AI in Smartphone and Wearable Market Size, Share & Analysis By Type (Smartphone & Tablet, Wearable), By Application (Logistics & Transportation, Healthcare, Automotive, BFSI, Aerospace & Defence, Others), Innovation Trends & Forecast 2025–2034

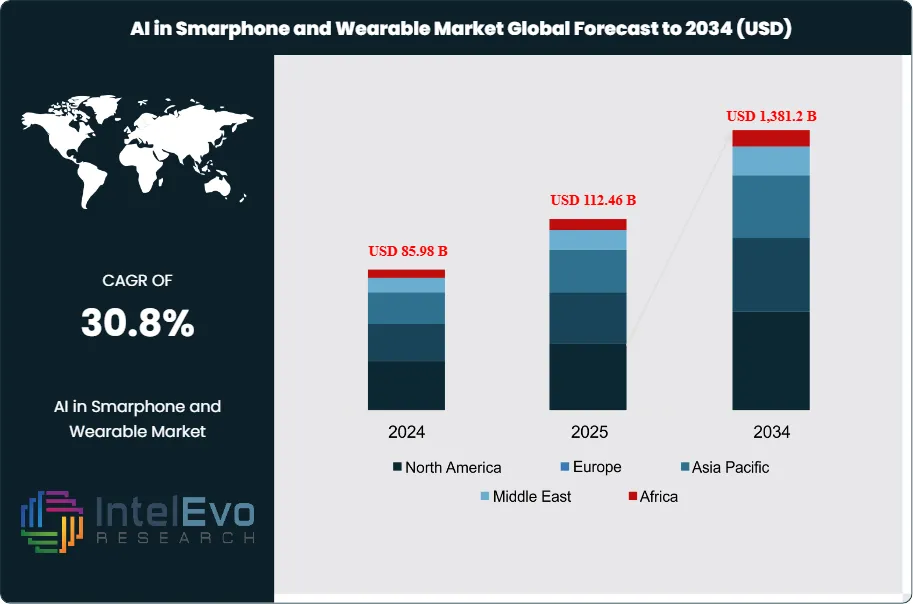

The AI in Smartphone and Wearable Market size is expected to reach around USD 85.98 Billion in 2024 and is projected to be worth approximately USD 1,381.2 Billion by 2034, growing at an estimated CAGR of around 30.8% from 2025 to 2034. This remarkable growth trajectory highlights the accelerating integration of artificial intelligence into consumer devices, reshaping the competitive landscape of the global technology sector.

The market’s expansion is underpinned by rising consumer demand for smarter, more intuitive devices that deliver personalized experiences. AI-driven features such as intelligent voice assistants, predictive text, facial and voice recognition, and advanced health monitoring have transitioned from premium add-ons to mainstream expectations. In particular, health-focused wearables have gained significant traction, offering continuous tracking of vital signs—including heart rate, sleep quality, and physical activity—making them indispensable tools for wellness-conscious individuals and patients managing chronic conditions.

At the core of this growth are rapid innovations in semiconductor technology, enabling on-device AI processing and reducing reliance on cloud-based computation. This shift not only enhances performance but also strengthens data privacy and responsiveness, which are critical factors for user adoption. According to recent industry surveys, AI-capable smartphones accounted for 16% of shipments in 2024, with this share projected to surge to 54% by 2028, reflecting a compound annual growth rate of 63% between 2024 and 2028. The adoption of AI agents, edge computing, and contextual intelligence is expected to further differentiate next-generation devices, driving strong replacement demand and competitive product launches.

Despite these opportunities, the market faces notable challenges. The high cost of AI integration—requiring advanced hardware and substantial R&D investments—raises device prices, limiting accessibility for cost-sensitive consumers and constraining smaller manufacturers. Additionally, the collection and processing of vast volumes of personal data heighten concerns around security and compliance. Stricter regulations on data protection, particularly in regions such as the European Union and North America, are pushing companies to strengthen cybersecurity frameworks, which adds to operational complexity and costs.

Regionally, North America and Asia-Pacific stand out as leading markets. North America benefits from high consumer purchasing power, strong innovation ecosystems, and early adoption of premium devices, while Asia-Pacific is emerging as the fastest-growing region, driven by its vast smartphone user base, competitive pricing strategies, and rapid digitalization. Together, these regions represent key investment hotspots for global players seeking to capture the next wave of AI-enabled device growth.

Key Takeaways

Market Growth: The Global AI in Smartphone and Wearable Market was valued at USD 85.98 Billion in 2024 and is projected to reach approximately USD 1,381.2 Billion by 2034, growing at a robust CAGR of 30.8%. Growth is fueled by rising consumer demand for intelligent devices, on-device AI processing, and health monitoring capabilities.

Product Type: Smartphones and tablets dominated the market in 2024, accounting for over 56.7% share. Their leadership is supported by mass adoption, rapid chipset advancements from players like Qualcomm and Apple, and integration of AI-driven features such as voice assistants, predictive typing, and facial recognition.

Application: Healthcare applications led with a 22.3% share in 2024, driven by increasing demand for AI-enabled wearables that provide real-time health insights, including heart rate, sleep cycle, and fitness tracking. These devices are increasingly adopted by health-conscious consumers and patients managing chronic conditions.

Driver: Advancements in semiconductor technology, including AI-optimized processors, are accelerating adoption by enabling efficient on-device computing, improving responsiveness, and reducing reliance on cloud processing.

Restraint: High costs of AI integration, encompassing advanced hardware and intensive R&D, continue to raise device prices, creating barriers to mass adoption in price-sensitive markets and limiting entry for smaller manufacturers.

Opportunity: Expanding use cases for AI-powered wearables in preventive healthcare, remote patient monitoring, and personalized wellness solutions represent a significant growth frontier, particularly as healthcare digitization accelerates.

Trend: The market is witnessing a surge in demand for AI agents and contextual intelligence, with on-device AI processing emerging as a disruptive trend that enhances privacy, responsiveness, and user personalization.

Regional Analysis: North America led the market in 2024 with a 38.35% revenue share (USD 25 billion), supported by high consumer spending power, early technology adoption, and strong innovation ecosystems. Asia-Pacific is poised to be the fastest-growing region, driven by its vast smartphone user base, competitive pricing, and rapid digital transformation initiatives.

Type Analysis

As of 2025, the smartphones and tablets segment continues to dominate the AI in Smartphone and Wearable Market, accounting for more than half of global revenue share. This leadership reflects the rapid and widespread deployment of AI-driven functionalities within mobile devices, which are now essential for enhancing usability, personalization, and overall user engagement. Features such as real-time language translation, advanced image recognition, and context-aware voice assistants are no longer niche but have become integral to consumer expectations.

The momentum is further reinforced by the strategic focus of technology leaders—such as Apple, Samsung, and Qualcomm—on embedding dedicated AI chipsets into flagship devices. These processors enable complex tasks, including natural language processing and on-device predictive analytics, without requiring cloud support. This shift not only improves performance and security but also reduces latency, a factor critical for applications like augmented reality and mobile gaming.

Looking ahead, the smartphone and tablet category is expected to remain the core revenue driver of this market, serving as the foundation for broader AI integration across connected ecosystems. Their ability to act as a hub for applications in healthcare, finance, and logistics ensures that these devices will remain at the center of digital lifestyles, sustaining their dominance over the forecast period.

Application Analysis

In 2025, the healthcare segment maintains its position as a leading application area for AI-enabled smartphones and wearables, capturing more than one-fifth of the global market.

This strength is rooted in the growing emphasis on preventive healthcare, personalized wellness management, and chronic disease monitoring. Devices equipped with AI-driven algorithms and biometric sensors are delivering critical insights—ranging from heart rhythm irregularities and oxygen saturation levels to stress detection and sleep quality analysis.

The value proposition of these devices extends beyond individual consumers to healthcare providers, who are increasingly integrating AI wearables into remote patient monitoring programs. This capability reduces the burden on clinical facilities by shifting routine tracking into everyday environments, enabling earlier interventions and reducing hospitalization rates. Industry collaborations, such as partnerships between device manufacturers and healthcare systems, are also expanding the ecosystem for AI-driven digital health solutions.

As awareness of digital wellness grows, demand for personalized health apps—capable of offering lifestyle guidance, fitness coaching, and medication reminders—is accelerating. The combination of continuous monitoring, AI-based predictive analytics, and user-friendly interfaces is redefining patient engagement models. Over the coming years, healthcare applications are expected to be one of the fastest-growing verticals, making them a strategic opportunity for both device makers and healthcare providers.

Regional Analysis

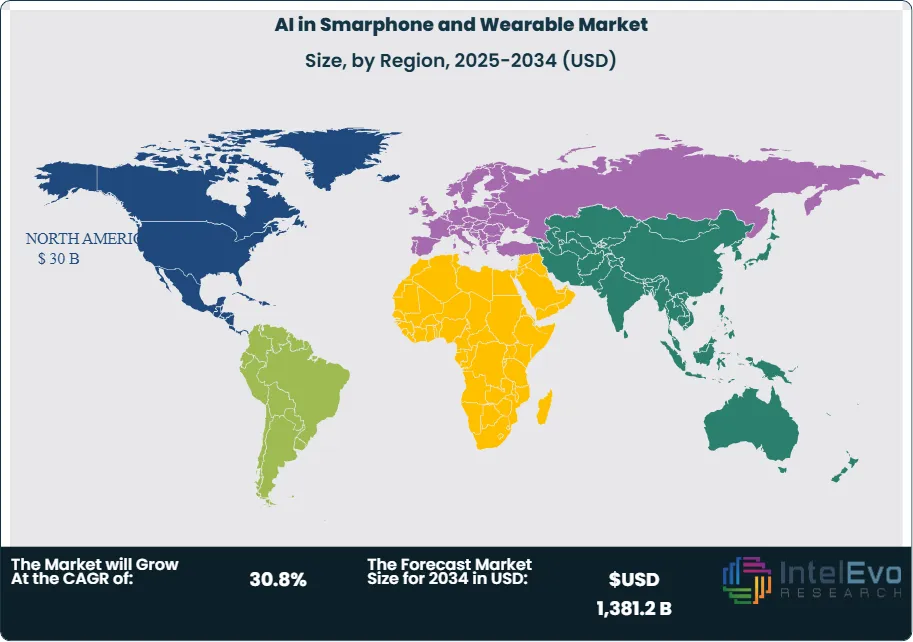

North America continues to lead the global AI in Smartphone and Wearable Market in 2025, generating revenues of more than USD 30 billion and accounting for a market share exceeding 37%. This dominance stems from the region’s mature digital infrastructure, high purchasing power, and strong ecosystem of innovators ranging from established technology giants to AI-focused startups. The U.S., in particular, plays a central role as a hub for research, investment, and commercialization of next-generation AI-enabled devices.

The region’s competitive advantage is reinforced by extensive public and private sector funding in AI research and its deployment across consumer and enterprise applications. From AI-powered health wearables adopted in remote patient care to advanced AI-driven mobile applications supporting industries such as banking and logistics, North America demonstrates a broad spectrum of use cases. Moreover, consumer readiness to embrace emerging technologies, coupled with stringent but supportive regulatory frameworks around AI ethics and data protection, strengthens long-term growth.

Going forward, North America is expected to retain its leadership, while Asia-Pacific emerges as the fastest-growing regional market. Countries such as China, India, and South Korea are witnessing rapid expansion in smartphone penetration, coupled with competitive device pricing and rising investment in domestic AI innovation. Together, these dynamics highlight a dual growth story: North America’s role as an innovation leader and Asia-Pacific’s rise as a volume-driven growth engine.

Would you like me to also add sub-sections for “Wearables” (under By Type) so the analysis feels more balanced between smartphones and wearables, rather than focused mostly on phones and tablets?

By Type (Smartphone & Tablet, Wearable), By Application (Logistics & Transportation, Healthcare, Automotive, BFSI, Aerospace & Defence, Others)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Apple Inc., Samsung Electronics Co., Ltd., Huawei Technologies Co., Ltd., Xiaomi Corporation, Fitbit (acquired by Google), Garmin Ltd., Oppo Electronics Corp., Vivo Communication Technology Co., Ltd., Sony Corporation, Realme.

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL AI IN SMARPHONE AND WEARABLE CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Player Analysis

Lenovo: Lenovo has positioned itself as a strong contender in the AI-enabled smartphone and wearable landscape, leveraging its strength in hardware design and global distribution. The company is increasingly embedding AI-driven functionalities into its premium smartphones and wearable devices, focusing on productivity, security, and immersive experiences. Its strategic emphasis lies in optimizing edge computing through AI-powered processors, allowing faster on-device decision-making without heavy reliance on cloud systems.

In 2025, Lenovo’s differentiation stems from its integration of AI into enterprise-focused wearables and smartphones, aimed at sectors such as logistics, healthcare, and education. By aligning its consumer devices with broader enterprise ecosystems—including cloud services and IoT solutions—Lenovo is carving out a niche as a versatile player bridging consumer convenience and business applications.

Apple: Apple remains a market leader in AI-driven smartphones and wearables, underpinned by its proprietary ecosystem and vertically integrated hardware-software model. With the Apple Neural Engine (ANE) embedded in its A-series and M-series processors, the company continues to push advancements in on-device machine learning. Its flagship devices—iPhone and Apple Watch—serve as benchmarks for AI-enabled personalization, predictive analytics, and health monitoring solutions.

In 2025, Apple’s strategic edge lies in its health ecosystem. The Apple Watch, equipped with advanced AI algorithms, now delivers comprehensive insights into cardiovascular health, sleep quality, and mental well-being. Moreover, Apple’s focus on privacy-centric AI, using federated learning and encrypted on-device data processing, has strengthened consumer trust—a key differentiator in an era of growing regulatory scrutiny. The company’s expanding integration of AI across iOS and health applications reinforces its role as a front-runner in shaping user-centric, intelligent digital experiences.

Huawei: Despite geopolitical challenges, Huawei continues to be a major innovator in the AI-enabled smartphone and wearable market. The company’s Kirin AI chipsets and HarmonyOS ecosystem have been central to its strategy, enabling seamless integration of AI-driven applications across smartphones, wearables, and connected devices. In 2025, Huawei has doubled down on AI-enhanced imaging, multilingual virtual assistants, and health-focused wearables, catering to both domestic and international markets where demand for advanced yet competitively priced devices remains high.

Huawei differentiates itself through its investment in 5G-AI convergence, using its telecommunications expertise to create ultra-low-latency AI applications for mobile users. Its growing presence in Asia-Pacific and parts of Europe highlights its resilience, as the company leverages AI capabilities to maintain competitiveness in both premium and mid-tier segments.

Xiaomi: Xiaomi has emerged as a disruptor by democratizing access to AI-enabled smartphones and wearables at highly competitive price points. The company’s aggressive strategy focuses on integrating AI-driven health monitoring, voice assistance, and camera enhancements into mid-range and budget-friendly devices, thereby expanding the market reach of AI technologies.

In 2025, Xiaomi is building differentiation through its MIUI AI interface and strong IoT ecosystem, where smartphones and wearables act as central hubs for connected devices. This ecosystem-driven approach has positioned Xiaomi not only as a consumer electronics leader but also as a critical enabler of smart home integration. By coupling affordability with AI-powered features, the company has successfully captured a significant share in emerging markets such as India, Southeast Asia, and Latin America.

Samsung: Samsung remains one of the most influential global players in the AI in Smartphone and Wearable Market, leveraging its scale, innovation capacity, and broad product portfolio. Its Exynos AI processors and integration of AI into the Galaxy ecosystem have enabled advanced functionalities such as real-time language translation, AI-optimized photography, and predictive device management.

In 2025, Samsung’s competitive strength lies in multi-device intelligence—linking smartphones, smartwatches, and connected appliances into a unified ecosystem through SmartThings AI. Its Galaxy Watch series has expanded into advanced healthcare applications, offering ECG, stress monitoring, and sleep analytics enhanced by AI algorithms. Additionally, Samsung’s leadership in display technology and semiconductor innovation reinforces its ability to integrate cutting-edge AI features across devices, sustaining its leadership in both premium and mass-market categories.

Key Market Players

Apple Inc.

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

Xiaomi Corporation

Fitbit (acquired by Google)

Garmin Ltd.

Oppo Electronics Corp.

Vivo Communication Technology Co., Ltd.

Sony Corporation

Realme

Driver

Key Market Drivers Accelerating AI Adoption in Smartphones & Wearables

As of 2025, a primary growth driver for the AI in Smartphone and Wearable Market is the accelerated integration of edge AI capabilities into consumer devices. By enabling real-time processing directly on smartphones and wearables, manufacturers are reducing dependence on cloud computing, thereby improving speed, privacy, and user control. This has expanded the adoption of applications such as intelligent health monitoring, voice-based virtual assistants, and AI-powered imaging.

Global technology leaders—including Apple, Samsung, and Huawei—are investing heavily in specialized AI processors that support complex tasks such as natural language processing and computer vision. These advancements are enhancing user personalization, improving device efficiency, and creating new value propositions across healthcare, lifestyle, and entertainment segments, making AI a core differentiator in next-generation devices.

Restraint

Major Restraints Hindering AI Integration in Consumer Devices

Despite strong momentum, the market faces constraints due to the high cost of AI integration in mobile hardware. Designing and manufacturing neural processing units (NPUs) and other AI-optimized chipsets requires significant R&D spending and advanced fabrication processes, driving up production costs. As a result, AI-enabled smartphones and wearables often carry premium price tags, creating adoption barriers in price-sensitive markets.

In addition, frequent upgrades in both hardware and software ecosystems require consumers and enterprises to adapt continuously, which can slow adoption among segments resistant to rapid technological change. For smaller device manufacturers, these high entry costs limit competitiveness, reinforcing the dominance of large players with the financial capacity to sustain long-term innovation.

Opportunity

Growing Opportunities in AI-Powered Health and Wellness Ecosystems

The most compelling opportunity for 2025 lies in the expanding role of AI-powered health and wellness applications. Rising global awareness around preventive healthcare, coupled with the shift toward remote monitoring, has positioned AI-enabled wearables as essential tools for consumers and healthcare providers alike. Devices are increasingly capable of tracking cardiac activity, sleep cycles, blood oxygen levels, and stress indicators, delivering actionable insights for improved health outcomes.

Moreover, partnerships between technology companies and healthcare providers are opening pathways for integrating wearables into formal care delivery models, such as chronic disease management and telehealth. As regulatory frameworks in regions like North America and Asia-Pacific begin to support digital health innovation, the adoption of AI-based health solutions is expected to surge, creating a long-term revenue stream for device makers and service providers.

Trend

Emerging Trends Shaping the Future of AI-Enabled Smart Devices

A defining trend in 2025 is the rise of multi-modal AI ecosystems in smartphones and wearables. Devices are evolving beyond single-purpose applications to act as hubs that seamlessly integrate with smart homes, connected vehicles, and enterprise workflows. AI-driven assistants are becoming context-aware, capable of predicting user needs and coordinating across devices in real time.

Simultaneously, the shift toward edge AI and federated learning is strengthening data privacy and reducing latency, addressing a critical consumer concern. This is complemented by innovations in biometric authentication, AI-enhanced imaging, and adaptive power management, which are transforming user experiences. Collectively, these trends are establishing smartphones and wearables not just as communication tools but as intelligent companions central to modern digital lifestyles.

Recent Developments

December 2024 – Samsung: Rolled out One UI 7 Beta, designed as an AI-first mobile platform that emphasizes dynamic, personalized user experiences. This early software push reinforces Samsung’s strategy to elevate AI integration across future device interactions.

January–February 2025 – Samsung: Debuted a new AI-centric device portfolio including foldable phones and smartwatches, emphasizing enhanced, context-aware interfaces tied into a connected ecosystem of wearables, XR devices, and appliances. A strategic collaboration with Google’s Gemini and Qualcomm supports hybrid on-device/cloud AI experiences.

March 2025 – Honor: Announced a landmark $10 billion investment over five years to advance AI across its product portfolio—spanning smartphones, PCs, tablets, and wearables—backed by strong governmental R&D support. This positions Honor for a broad ecosystem expansion and fortifies its AI innovation ambitions amid plans for a public offering.

December 2024 – Samsung: Rolled out One UI 7 Beta, designed as an AI-first mobile platform that emphasizes dynamic, personalized user experiences. This early software push reinforces Samsung’s strategy to elevate AI integration across future device interactions.

Frequently Asked Questions

How big is the AI in Smarphone and Wearable Market?

The AI in Smartphone & Wearable Market will surge from USD 85.98 Bn in 2024 to USD 1,381.2 Bn by 2034, driven by rapid AI integration and next-gen device innovation.

Who are the major players in the AI in Smarphone and Wearable Market?

Apple Inc., Samsung Electronics Co., Ltd., Huawei Technologies Co., Ltd., Xiaomi Corporation, Fitbit (acquired by Google), Garmin Ltd., Oppo Electronics Corp., Vivo Communication Technology Co., Ltd., Sony Corporation, Realme.

Which segments covered the AI in Smarphone and Wearable Market?

By Type (Smartphone & Tablet, Wearable), By Application (Logistics & Transportation, Healthcare, Automotive, BFSI, Aerospace & Defence, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, By Application (Logistics & Transportation, Healthcare, Automotive, BFSI, Aerospace & Defence, Others), Innovation Trends & Forecast 2025–2034")

, By Application (Logistics & Transportation, Healthcare, Automotive, BFSI, Aerospace & Defence, Others), Innovation Trends & Forecast 2025–2034")

, By Application (Logistics & Transportation, Healthcare, Automotive, BFSI, Aerospace & Defence, Others), Innovation Trends & Forecast 2025–2034")

, By Application (Logistics & Transportation, Healthcare, Automotive, BFSI, Aerospace & Defence, Others), Innovation Trends & Forecast 2025–2034")