- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

AI in Smart Cities Market Size, Trends & Forecast | 29.1% CAGR

Global AI in Smart Cities Market Size, Share & Analysis By Component (Hardware, Software, Services), By Application (Smart Mobility, Energy Management, Healthcare, Public Safety and Security, Waste Management, Environmental Monitoring, Water Management), By Deployment Mode (Cloud-based, On-premises), By End User (Utilities, Transportation Companies, Healthcare Providers, Real Estate Developers) Industry Regions & Key Players – Urban Digitalization Trends & Forecast 2025–2034

Report Overview

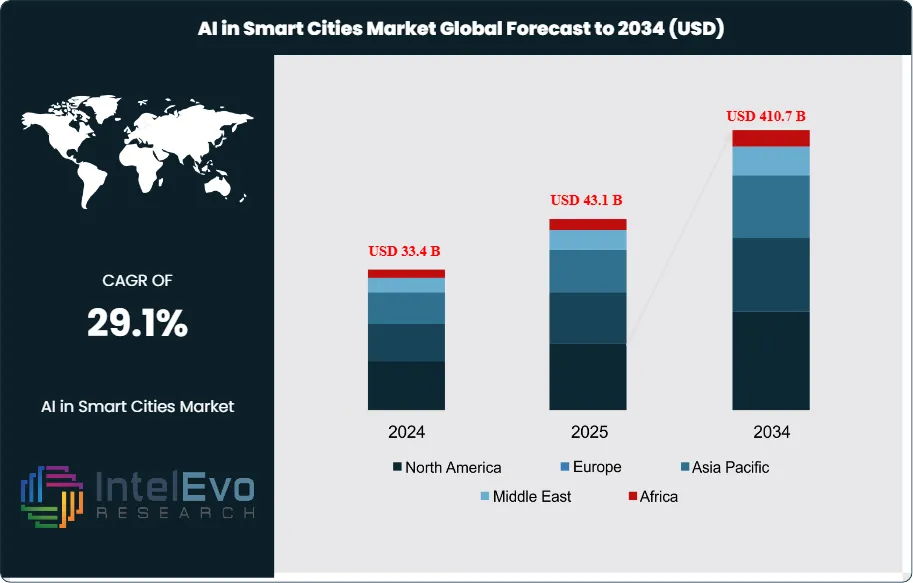

The AI in Smart Cities Market is projected to grow from USD 33.4 Billion in 2024 to approximately USD 410.7 Billion by 2034, expanding at a CAGR of around 29.1% during 2025–2034. Smart city initiatives are accelerating globally as governments and enterprises adopt AI to enhance traffic management, energy efficiency, and public safety systems. Advancements in IoT sensors, digital twins, and connected urban infrastructure are creating data-driven, automated city environments. With increasing investments in sustainable urban development, AI is becoming the backbone of next-generation city planning and real-time civic operations.

Get More Information about this report -

Request Free Sample ReportArtificial intelligence (AI) has emerged as a critical enabler of smart city development, transforming how urban areas manage infrastructure, resources, and citizen services. By integrating AI with Internet of Things (IoT) networks, cloud platforms, and advanced connectivity, cities are leveraging real-time data to optimize transportation, energy distribution, healthcare, waste management, and governance. This convergence is driving a rapid shift toward more efficient, resilient, and sustainable urban ecosystems, ultimately enhancing the quality of life for residents.

The market’s momentum is reinforced by surging urbanization, rising demand for sustainable city solutions, and the growing emphasis on digital-first public infrastructure. AI is increasingly deployed in traffic control systems to reduce congestion, predictive analytics for energy conservation, and intelligent surveillance for enhanced safety. For municipalities, these solutions not only improve operational efficiency but also support long-term urban planning by enabling data-driven decision-making. At the same time, citizens benefit from improved mobility, faster access to public services, and more transparent governance models.

Technological advancements are playing a pivotal role in shaping market growth. Machine learning, natural language processing, and predictive modeling are revolutionizing smart city operations, while cloud-based deployment ensures scalability and cost efficiency. In addition, AI-powered environmental monitoring solutions are supporting sustainability initiatives by reducing pollution levels and enabling more efficient resource allocation. Ambitious government-led programs, such as Dubai’s AI Roadmap, illustrate the forward momentum of this sector, with objectives ranging from autonomous mobility to fully digitized service delivery.

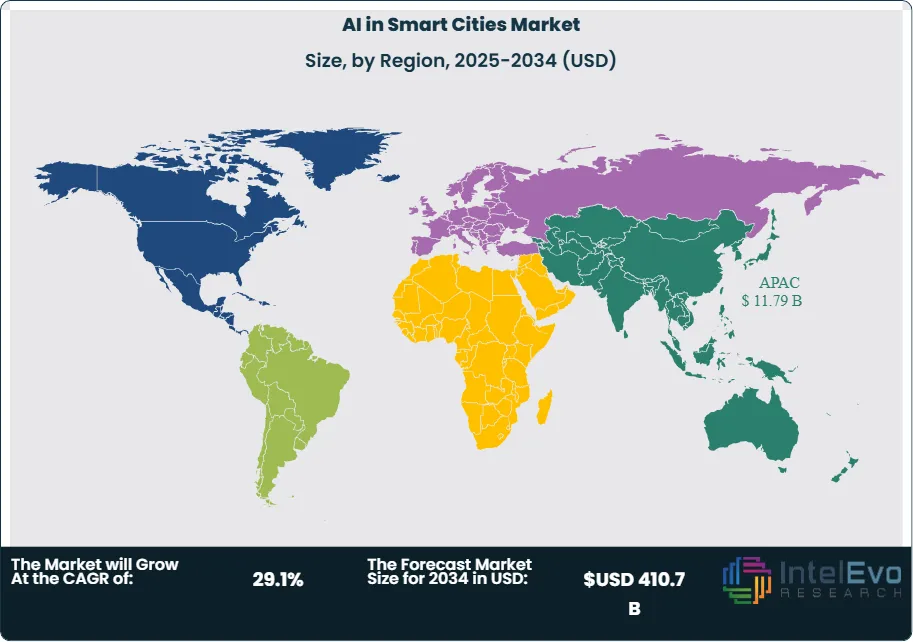

Regionally, Asia-Pacific leads the market, accounting for over 35% of global revenue in 2023, supported by large-scale government investments, robust 5G rollouts, and widespread adoption of IoT-enabled infrastructure in countries such as China, Japan, and South Korea. North America and Europe are also critical investment hotspots, driven by public-private partnerships and the integration of AI into advanced mobility and sustainability programs. Emerging economies in Latin America and the Middle East are beginning to accelerate adoption through targeted smart city initiatives, offering strong potential for growth.

Overall, the adoption of AI in smart cities is advancing beyond experimentation to become a cornerstone of urban transformation. With rising demand for intelligent, connected, and sustainable environments, the market is expected to experience robust expansion over the next decade, attracting significant investments from technology providers, governments, and infrastructure developers worldwide.

, By Application (Smart Mobility, Energy Management, Healthcare, Public Safety and Security, Waste Management, Environmental Monitoring, Water Management), By Deployment Mode (Cloud-based, On-premises), By End User (Utilities, Transportation Companies, Healthcare Providers, Real Estate Developers) Industry Regions & Key Players – Urban Digitalization Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global AI in Smart Cities Market is projected to expand from USD 33.4 Billion in 2024 to USD 410.7 billion by 2034, advancing at a CAGR of 29.1% during 2024–2033. Growth is being fueled by rapid urbanization, rising demand for sustainable urban solutions, and the integration of AI with IoT and cloud platforms.

- Offering (Software): Software solutions accounted for more than 59.3% of market share in 2023, driven by demand for AI-powered analytics, predictive modeling, and citizen service platforms. The scalability and adaptability of software are making it the backbone of smart city initiatives.

- Application (Transportation): Transportation emerged as the largest application area, holding over 38.7% share, as AI is increasingly applied to traffic management, smart mobility platforms, and autonomous vehicle infrastructure to reduce congestion and improve safety.

- Deployment (Cloud): Cloud-based AI solutions captured more than 53.5% of the market in 2023, reflecting the preference of municipalities for scalable, cost-effective deployment models that support real-time data processing and multi-stakeholder collaboration.

- Driver: The growing focus on improving citizen engagement and operational efficiency is accelerating adoption. AI-enabled tools are being used to optimize energy grids, enhance public safety, and streamline access to government services, thereby strengthening urban resilience.

- Restraint: The lack of interoperability and standardization across AI platforms and smart city systems continues to hinder seamless integration, raising costs and slowing deployment, particularly in developing economies.

- Opportunity: Rising demand for sustainability-driven solutions—such as AI-powered energy management, water conservation, and environmental monitoring—presents high-growth potential, especially as governments align with net-zero and climate-resilient city goals.

- Trend: The convergence of AI with emerging technologies such as digital twins, edge computing, and 5G is reshaping smart city operations, enabling predictive urban planning, real-time resource allocation, and autonomous mobility services.

- Regional Analysis: Asia-Pacific led the market in 2023 with over 35.3% share (USD 10.9 billion), supported by large-scale government programs in China, Japan, and South Korea. North America and Europe remain strong innovation hubs, while the Middle East is rapidly investing in AI-driven mega city projects like NEOM in Saudi Arabia.

Application Analysis

In 2025, transportation and smart mobility continue to dominate AI adoption in smart cities, building on their substantial share of nearly 39% in recent years. AI-driven platforms are being deployed to optimize traffic flow, manage congestion, and reduce carbon emissions through intelligent routing and predictive maintenance. The integration of IoT-enabled traffic signals, smart parking systems, and autonomous fleet management solutions is transforming urban mobility, with leading cities in Asia and Europe already reporting measurable reductions in travel delays and pollution levels.

Beyond mobility, applications such as public safety, healthcare, and energy management are gaining momentum. Cities are increasingly using AI for predictive policing, environmental monitoring, and smart grids that balance energy demand with renewable supply. For example, municipalities are adopting AI-driven environmental sensors to reduce air pollution and enhance disaster preparedness. These developments reflect the expanding scope of AI beyond transport, positioning it as a multi-sectoral enabler of urban resilience and sustainability.

Deployment Mode Analysis

Cloud-based AI platforms have emerged as the preferred deployment model for smart city projects in 2025, maintaining a dominant share above 50%. Their scalability and flexibility make them particularly valuable for municipalities managing vast data volumes from sensors, utilities, and connected infrastructure. Cloud deployment also reduces upfront capital investment, enabling smaller cities to implement AI solutions through subscription-based or pay-as-you-go models. This shift toward operating expenditure models is accelerating adoption across regions with budget constraints.

On-premises solutions, while more limited, remain relevant for applications requiring heightened security, such as law enforcement databases and sensitive citizen records. However, advancements in hybrid cloud and edge computing are narrowing this gap, allowing cities to balance data sovereignty with the scalability of cloud systems. This evolution underscores how deployment models are adapting to the complex realities of urban governance.

End User Analysis

In 2025, real estate developers represent one of the most influential end-user groups within the AI in smart cities market. Their adoption of AI spans smart building design, predictive maintenance, and energy-efficient infrastructure planning. Developers are leveraging AI-enhanced building management systems to optimize HVAC performance, reduce energy costs, and meet tightening sustainability regulations. These solutions not only improve operational efficiency but also align with growing investor and resident demand for greener, digitally connected living environments.

Utilities and transportation companies are also critical adopters, using AI to modernize grid management and mobility systems. For instance, AI-powered demand forecasting enables utilities to integrate renewable energy sources more effectively, while transportation firms deploy intelligent analytics to support multimodal transport hubs. Collectively, these end-user segments are driving AI’s transition from experimental projects to core operational systems in urban development.

By Regional Analysis

The Asia-Pacific region continues to lead the global AI in smart cities market in 2025, sustaining its share of more than one-third of total revenues. China, India, and Japan are at the forefront, propelled by large-scale government programs such as India’s Smart Cities Mission and China’s urban modernization initiatives. These programs emphasize AI adoption in traffic control, surveillance, and energy distribution, reinforcing APAC’s status as the global hub for smart city innovation.

North America and Europe remain highly competitive markets, with North America focusing on AI-powered citizen engagement platforms and sustainability-oriented energy management, while Europe emphasizes digital twins and green urban planning aligned with the EU’s climate goals. Meanwhile, the Middle East is accelerating investments in mega-projects such as Saudi Arabia’s NEOM, embedding AI into infrastructure from inception. Latin America and Africa, though at earlier stages of adoption, are beginning to roll out AI-enabled public safety and water management projects, highlighting significant untapped potential in emerging economies.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Component

- Hardware

- Software

- Services (Consulting, Maintenance, Training)

By Application

- Smart Mobility

- Energy Management

- Healthcare

- Public Safety and Security

- Waste Management

- Environmental Monitoring

- Water Management

- Others

By Deployment Mode

- Cloud-based

- On-premises

By End User

- Utilities

- Transportation Companies

- Healthcare Providers

- Real Estate Developers

- Others (Education, Retail)

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 33.4 B |

| Forecast Revenue (2034) | USD 410.7 B |

| CAGR (2025-2034) | 29.1% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Hardware, Software, Services (Consulting, Maintenance, Training)), By Application (Smart Mobility, Energy Management, Healthcare, Public Safety and Security, Waste Management, Environmental Monitoring, Water Management, Others), By Deployment Mode (Cloud-based, On-premises), By End User (Utilities, Transportation Companies, Healthcare Providers, Real Estate Developers, Others (Education, Retail)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ABB Ltd, Alibaba Group Holding Ltd., Cisco Systems, Inc., Gorilla Technology, Hayden AI, Hitachi, Ltd., Honeywell International Inc., Huawei Technologies Co., Ltd., IBM Corporation, Intel Corporation, Metropolis Technologies, Microsoft Corporation, NEC Corporation, Nodeflux, omniQ, Oracle Corporation, Paradox Engineering SA, Samsara Inc., SAP SE, Schneider Electric, Siemens AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Smart Mobility, Energy Management, Healthcare, Public Safety and Security, Waste Management, Environmental Monitoring, Water Management), By Deployment Mode (Cloud-based, On-premises), By End User (Utilities, Transportation Companies, Healthcare Providers, Real Estate Developers) Industry Regions & Key Players – Urban Digitalization Trends & Forecast 2025–2034")

, By Application (Smart Mobility, Energy Management, Healthcare, Public Safety and Security, Waste Management, Environmental Monitoring, Water Management), By Deployment Mode (Cloud-based, On-premises), By End User (Utilities, Transportation Companies, Healthcare Providers, Real Estate Developers) Industry Regions & Key Players – Urban Digitalization Trends & Forecast 2025–2034")

, By Application (Smart Mobility, Energy Management, Healthcare, Public Safety and Security, Waste Management, Environmental Monitoring, Water Management), By Deployment Mode (Cloud-based, On-premises), By End User (Utilities, Transportation Companies, Healthcare Providers, Real Estate Developers) Industry Regions & Key Players – Urban Digitalization Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the AI in Smart Cities Market?

The AI in Smart Cities Market is projected to grow from USD 33.4 Billion in 2024 to USD 410.7 Billion by 2034, at a CAGR of 29.1%. Smart infrastructure, IoT integration, and data-driven urban planning are accelerating global adoption of AI-powered city solutions.

Who are the major players in the AI in Smart Cities Market?

ABB Ltd, Alibaba Group Holding Ltd., Cisco Systems, Inc., Gorilla Technology, Hayden AI, Hitachi, Ltd., Honeywell International Inc., Huawei Technologies Co., Ltd., IBM Corporation, Intel Corporation, Metropolis Technologies, Microsoft Corporation, NEC Corporation, Nodeflux, omniQ, Oracle Corporation, Paradox Engineering SA, Samsara Inc., SAP SE, Schneider Electric, Siemens AG

Which segments covered the AI in Smart Cities Market?

By Component (Hardware, Software, Services (Consulting, Maintenance, Training)), By Application (Smart Mobility, Energy Management, Healthcare, Public Safety and Security, Waste Management, Environmental Monitoring, Water Management, Others), By Deployment Mode (Cloud-based, On-premises), By End User (Utilities, Transportation Companies, Healthcare Providers, Real Estate Developers, Others (Education, Retail))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date