- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

AI in Space Exploration Market Size 2025–2034 | CAGR 33.2%

Global AI in Space Exploration Market Size, Share & Growth Analysis By Type (Rovers, Robotic Arms, Space Probes), By Application (Robotics, Remote Sensing & Monitoring, Data Analytics, Asteroid Mining, Manned Vehicles & Reusable Launch Systems, Communications, Remote Missions), By End-User (Government, Commercial), By Region & Key Players – Industry Overview, Market Dynamics, Technology Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

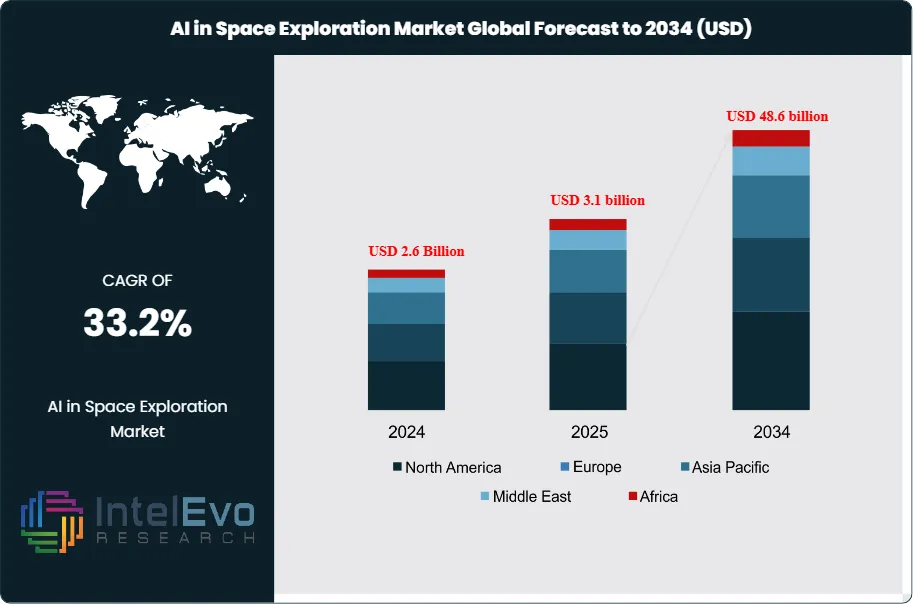

The AI in Space Exploration Market is estimated to reach approximately USD 3.1 billion in 2025 and is projected to expand to around USD 48.6 billion by 2034, registering a very strong compound annual growth rate (CAGR) of about 33.2% during the forecast period from 2026 to 2034. Market growth is fueled by rising deployment of AI-driven autonomous navigation, mission planning, and data analytics across satellite operations, deep-space missions, and planetary exploration programs. Space agencies and private players increasingly rely on AI to process massive volumes of satellite imagery, optimize spacecraft performance, and enable real-time decision-making in remote environments. Additionally, growing investments in space commercialization, defense space programs, and AI-enabled robotics are accelerating adoption, positioning AI as a critical enabler of next-generation space exploration and long-term market expansion.

Get More Information about this report -

Request Free Sample ReportThis growth reflects the rapid integration of artificial intelligence into mission planning, spacecraft operations, and data analysis, and the broader digitalization of space infrastructure. In 2023, the market stood at USD 2.0 Billion, with North America accounting for over 40% of global revenue, supported by strong space agency budgets and early adoption of autonomous mission technologies.

AI-enabled autonomy has become a core response to rising mission complexity and the limitations of real-time human control. As of 2022, approximately 5,500 operational satellites were in orbit, and projections indicate that about 58,000 additional satellites could launch by 2030, intensifying demand for AI-driven traffic management, health monitoring, and payload optimization. AI systems already improve asteroid detection accuracy by around 10%, map roughly 90% of the Martian surface, and can classify maritime vessels in satellite imagery with over 95% accuracy, underscoring their role in data-intensive use cases.

On the supply side, advances in on-board processing, edge AI chips, and resilient software stacks enable higher autonomy at lower power and weight. Analysts estimate that AI adoption in the space industry has grown 29,300% over the past five years, while the broader AI segment within space technology is expected to reach around USD 342 Billion by 2025. These trends support new business models in automated Earth observation, in-orbit servicing, and predictive maintenance, while also driving ecosystem consolidation around key platform and analytics providers.

Regulatory and risk considerations remain material. Space agencies and regulators focus on spectrum management, orbital debris mitigation, and safety assurance for autonomous decision-making, especially as deep space missions depend on AI to operate beyond practical communication windows. Cybersecurity, algorithm transparency, and liability for AI-led decisions present growing concerns for investors. Regionally, North America and Europe lead deployment, reinforced by NASA and the European Space Agency, while Asia Pacific, led by China, India, and Japan, is emerging as a key investment hotspot. Across stakeholders, an estimated 70% of industry professionals expect AI to exert significant impact on space missions over the next decade, supporting a strong long-term outlook for this market.

, By Application (Robotics, Remote Sensing & Monitoring, Data Analytics, Asteroid Mining, Manned Vehicles & Reusable Launch Systems, Communications, Remote Missions), By End-User (Government, Commercial), By Region & Key Players – Industry Overview, Market Dynamics, Technology Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Global AI in Space Exploration Market stood at USD 3.1 billion and is projected to reach USD 48.6 billion by 2034, implying a compound annual growth rate of 33.2% over 2026-2034. This growth trajectory reflects accelerating integration of AI across mission planning, operations, and data analysis over 2024-2034.

- Segment Dominance: The Rovers segment led the market with over 35.0% share, 2023, supported by intensive use of AI for navigation, hazard avoidance, and scientific data collection. This segment continues to anchor AI deployments as agencies prioritize autonomous surface exploration missions through 2024-2034.

- Segment Dominance: The Robotics segment accounted for more than 30.0% share, 2023, as AI-enabled manipulators and robotic platforms supported in-orbit servicing, assembly, and maintenance. Vendors expand AI-driven robotic capabilities to raise operational uptime and efficiency across missions over 2024-2034.

- Driver: Government customers represented over 73.0% share, 2023, providing stable funding for AI-driven exploration, defense, and scientific programs. Long-term public space budgets and mission roadmaps underpin demand visibility for AI solutions over 2024-2034.

- Restraint: High mission development, testing, and AI-integration costs, estimated: 0.8 billion USD, 2024, limit participation by smaller commercial operators. Complex qualification and reliability requirements for AI algorithms in harsh space environments further slow deployment over 2024-2034.

- Opportunity: Expanding use of AI for autonomous operations, data analytics, and on-board decision-making in commercial constellations creates new revenue pools, estimated: 5.0 billion USD, 2030. Vendors that deliver modular, space-qualified AI platforms can address both government and private missions across 2024-2034.

- Trend: Mission planners increasingly deploy AI-driven rovers and robotics, which together controlled over 65.0% combined share, 2023, across key mission hardware categories. This shift signals a steady move toward higher autonomy levels in both planetary and orbital operations over 2024-2034.

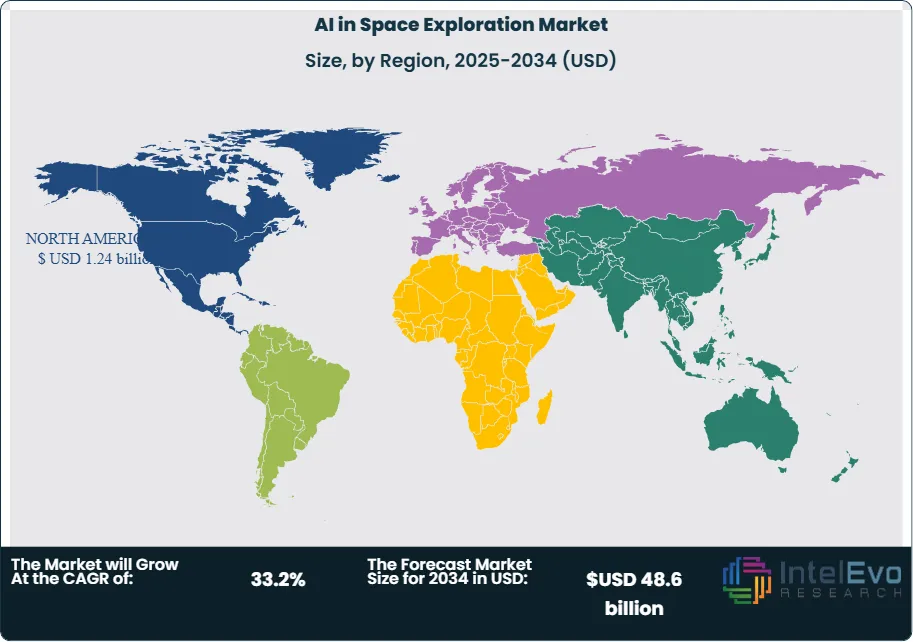

- Regional Analysis: North America held more than 40.0% share, 2023, reflecting strong investment by leading space agencies and prime contractors in AI-enabled missions. Other regions, led by Europe and Asia, are expected to narrow the gap with rising AI-in-space budgets, estimated: 3.0 billion USD, 2030, over 2024-2034.

By Type

The market for AI-enabled systems in space exploration continues to shift toward hardware platforms that can operate with minimal human control. Rovers account for the largest share of deployments. They represented more than 35 percent of global installations in 2023 and continue to expand in missions planned for 2025 and beyond. Agencies rely on rovers for surface mobility, subsurface analysis, and atmospheric monitoring on the Moon and Mars. Their role grows as mission planners prioritize long-duration operations and higher data output.

AI integration strengthens rover performance. Modern rovers process sensor data in real time, classify terrain features, avoid hazards, and adjust travel paths without assistance from Earth. These capabilities reduce downtime caused by communication delays. They also raise mission productivity by enabling continuous sampling and autonomous field decisions. Several programs under NASA, ESA, and ISRO now require onboard AI packages as a baseline specification for future rover fleets.

Space probes and robotic arms form the next largest categories. Probes equipped with onboard analytics handle deep-space observations and data filtering, which reduces downlink loads. Robotic arms support repair, docking, and cargo handling. Both segments gain importance as governments prepare for lunar infrastructure projects and early commercial activity in cislunar space. As missions scale in complexity, demand grows for AI-supported systems that maintain accuracy and operational continuity.

By Application

Robotics remains the leading application area for AI in space exploration, maintaining more than 30 percent of total market share in 2023. Robots equipped with AI conduct maintenance, assembly, inspection, and sampling across orbits and planetary surfaces. Their use reduces the exposure of astronauts to hazardous conditions and limits the cost of sending crewed missions for tasks that can be completed autonomously.

Remote sensing and monitoring continue to expand as satellite constellations grow. AI filters raw imagery, detects anomalies, and prioritizes datasets for scientific analysis. Missions targeting climate research, planetary geology, and near-Earth object tracking depend on machine-learning models to raise accuracy and shorten processing cycles. Data analytics also accelerates. Operators deploy AI tools to manage high-volume sensor streams, run predictive diagnostics, and support mission planning.

Asteroid mining and reusable launch operations represent emerging fields. Early feasibility studies indicate that autonomous excavation and material sorting will require high-precision AI systems. Reusable launch vehicles also integrate AI for health monitoring and rapid turnaround. As commercial space companies scale their operations through 2030, these applications are expected to shift from experimental to operational status.

By End-Use

Government agencies remain the dominant end-users of AI in space exploration. They accounted for more than 73 percent of total spending in 2023. Public programs supply long-term funding cycles and large-scale missions, which creates steady demand for AI-based navigation, data processing, and mission-control systems. Agencies use AI to extend satellite lifetimes, manage large constellations, and support deep-space exploration.

The public sector also drives early research. Programs under NASA, ESA, JAXA, and CNSA invest in autonomous spacecraft operations and onboard analytics. These initiatives form the foundation for upcoming missions to Mars, Jupiter’s moons, and cislunar infrastructure. Governments increasingly collaborate with commercial suppliers to accelerate development timelines and reduce operational risk.

Commercial adoption is rising as private firms scale constellations for communications and Earth observation. AI improves image classification, reduces operational costs, and supports predictive maintenance. As launch costs decline and new business models emerge, commercial operators are expected to take a larger share of AI deployments between 2025 and 2035.

By Region

North America maintains the largest regional share, exceeding 40 percent in 2023. The region benefits from strong investment by NASA, the U.S. Department of Defense, and commercial firms such as SpaceX, Blue Origin, Lockheed Martin, and Northrop Grumman. These organizations embed AI in mission-critical systems, from capsule guidance to satellite analytics. The regional market exceeded 0.8 billion USD in 2023 and is projected to expand steadily as new lunar and planetary missions move into development.

Europe holds the second-largest share. ESA programs adopt AI to improve orbital management, robotic landers, and Earth observation workflows. The region also emphasizes AI for sustainability applications, including climate monitoring and debris tracking. Asia Pacific advances quickly. China, India, and Japan invest in lunar probes, reusable launch platforms, and autonomous spacecraft systems, creating strong demand for AI-enabled operations.

Latin America and the Middle East & Africa remain smaller but grow as governments increase participation in satellite programs. Several countries explore public-private partnerships to build local space capabilities using AI-driven monitoring, telecommunications, and climate research solutions. These regions are expected to move from early adoption to structured investment through 2030.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Rovers

- Robotic Arms

- Space Probes

- Other Types

By Application

- Robotics

- Remote Sensing and Monitoring

- Data Analytics

- Asteroid Mining

- Manned Vehicles and Reusable Launch

- Communications

- Remote Missions

By End-user

- Government

- Commercial

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.1 billion |

| Forecast Revenue (2034) | USD 48.6 billion |

| CAGR (2025-2034) | 33.2% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Rovers, Robotic Arms, Space Probes, Other Types), By Application (Robotics, Remote Sensing and Monitoring, Data Analytics, Asteroid Mining, Manned Vehicles and Reusable Launch, Communications, Remote Missions), By End-user (Government, Commercial) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | D-Orbit, Iceye, Lockheed Martin, Hawkeye 360, Thales Group, Blacksky Global, Planet Labs Inc., Maxar Technologies Inc., Spire Global, Airbus, Astroscale, Capella Space, Hewlett Packard Enterprise (HPE), SpaceX, IBM, Booz Allen Hamilton, Northrop Grumman, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Robotics, Remote Sensing & Monitoring, Data Analytics, Asteroid Mining, Manned Vehicles & Reusable Launch Systems, Communications, Remote Missions), By End-User (Government, Commercial), By Region & Key Players – Industry Overview, Market Dynamics, Technology Trends, Competitive Landscape & Forecast 2026–2034")

, By Application (Robotics, Remote Sensing & Monitoring, Data Analytics, Asteroid Mining, Manned Vehicles & Reusable Launch Systems, Communications, Remote Missions), By End-User (Government, Commercial), By Region & Key Players – Industry Overview, Market Dynamics, Technology Trends, Competitive Landscape & Forecast 2026–2034")

, By Application (Robotics, Remote Sensing & Monitoring, Data Analytics, Asteroid Mining, Manned Vehicles & Reusable Launch Systems, Communications, Remote Missions), By End-User (Government, Commercial), By Region & Key Players – Industry Overview, Market Dynamics, Technology Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI in Space Exploration Market?

The AI in Space Exploration Market is projected to grow from USD 3.1 billion in 2025 to USD 48.6 billion by 2034, expanding at a CAGR of 33.2% during 2026–2034, driven by AI-powered satellite analytics, autonomous navigation, mission planning, and rising investments in commercial and defense space programs.

Who are the major players in the AI in Space Exploration Market?

D-Orbit, Iceye, Lockheed Martin, Hawkeye 360, Thales Group, Blacksky Global, Planet Labs Inc., Maxar Technologies Inc., Spire Global, Airbus, Astroscale, Capella Space, Hewlett Packard Enterprise (HPE), SpaceX, IBM, Booz Allen Hamilton, Northrop Grumman, Other Key Players

Which segments covered the AI in Space Exploration Market?

By Type (Rovers, Robotic Arms, Space Probes, Other Types), By Application (Robotics, Remote Sensing and Monitoring, Data Analytics, Asteroid Mining, Manned Vehicles and Reusable Launch, Communications, Remote Missions), By End-user (Government, Commercial)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI in Space Exploration Market

Published Date : 02 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date