- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

AI in Ultrasound Imaging Market Size & Forecast 2024–2034 | 8.8% CAGR

Global AI in Ultrasound Imaging Market Size, Share & Industry Analysis By Solution (Hardware, Software, Services), By Technology (Machine Learning, Natural Language Processing, Computer Vision, Context-Aware Computing), By Application (Radiology, Cardiovascular, Obstetrics, Gastroenterology, Breast Screening, Gynecology), By End User (Hospitals, Clinics), Regional Insights, Competitive Landscape, Innovation Trends & Forecast 2025–2034

Report Overview

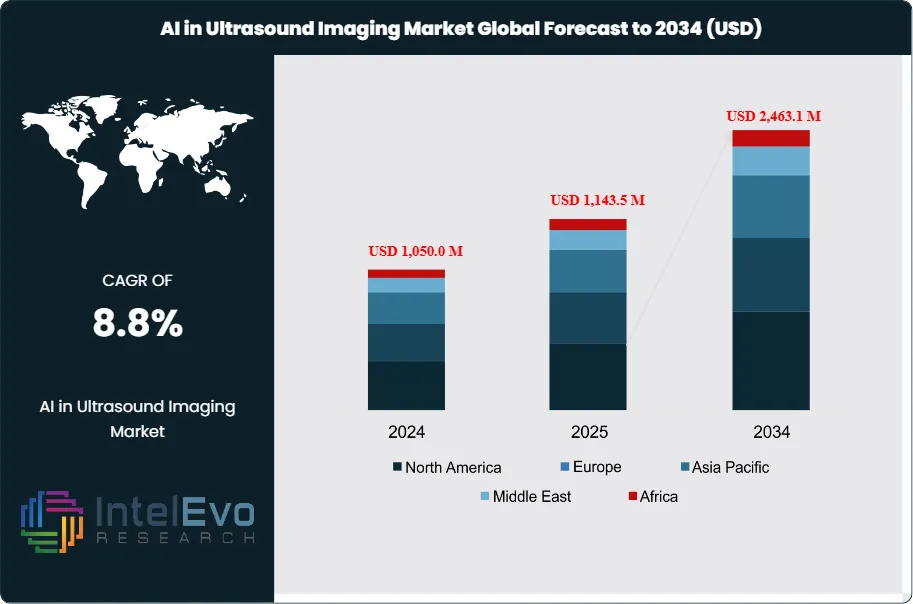

The AI in Ultrasound Imaging Market was valued at USD 1,050.0 Million in 2024 and is projected to reach approximately USD 2,463.1 Million by 2034. The market is estimated to grow to around USD 1,143.5 Million in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 8.8% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportDemand rises as disease burden lifts imaging volumes and forces providers to do more with limited specialist capacity. Ultrasound remains a front-line tool across obstetrics, cardiology, abdominal imaging, and point-of-care triage, and AI adoption accelerates where it shortens exam time and tightens diagnostic consistency. Cancer screening and follow-up also support utilization; the American Cancer Society estimated 238,810 new lung and bronchus cancer cases in the United States in 2023, which reinforces sustained demand for earlier detection pathways that include imaging. Hospitals and imaging centers should represent about 55% of 2024 revenue, while portable and point-of-care systems post the fastest unit growth as ultrasound use expands into emergency, critical care, and community settings.

On the supply side, vendors prioritize software layers that integrate with existing scanners and deliver real-time guidance, automated measurements, segmentation, and structured reporting. Integrated automation reduces operator dependence and improves repeatability, which increases the economic case for deployment at scale. Software and services are projected to rise from roughly 32% of revenue in 2024 to about 40% by 2034 as subscriptions, model updates, and workflow analytics gain share. Cloud-based interoperability also shapes purchasing decisions, and initiatives such as Google Cloud’s Medical Imaging Suite introduced in October 2022 highlight the push to make imaging data easier to exchange across PACS, EHRs, and analytics environments.

Regulatory and reimbursement dynamics set constraints and create differentiation. U.S. FDA pathways and CE marking remain essential gates, and procurement teams demand stronger evidence for clinical benefit, dataset representativeness, and post-market monitoring. Data privacy requirements under HIPAA and GDPR add compliance cost and elevate cybersecurity as a selection factor. Key risks include algorithm drift, medico-legal exposure from missed findings, workflow friction during integration, and uneven reimbursement coverage for AI-enabled functions.

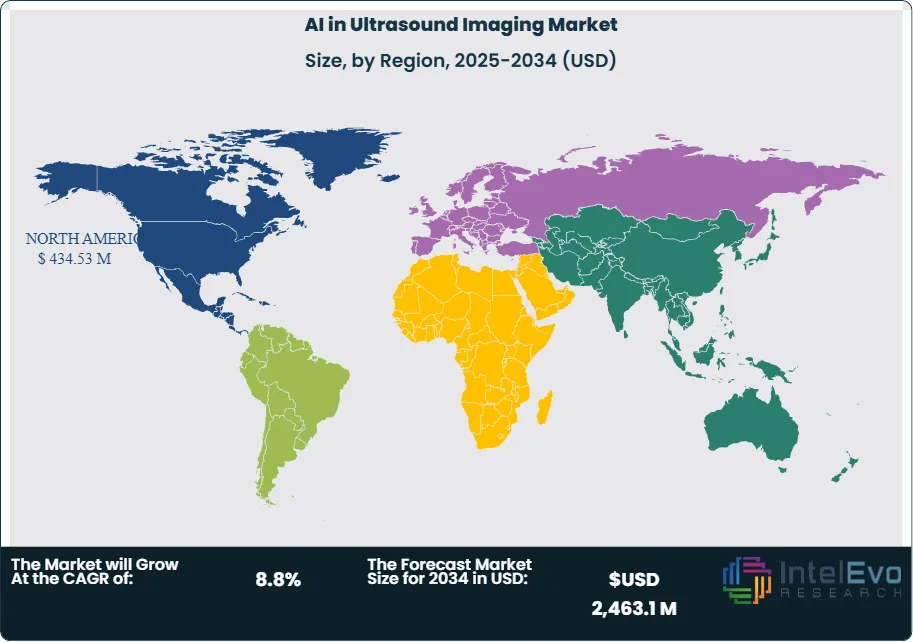

Regionally, North America is expected to hold about 38% of 2034 revenue due to established digital imaging infrastructure and faster enterprise rollout. Asia-Pacific should deliver the highest growth, near 10–11%, with investment hotspots in China, India, Japan, and Southeast Asia as systems scale maternal care, cardiometabolic screening, and mobile diagnostics. Europe remains a steady adopter, led by Germany, the U.K., and France, where providers focus on standardization and workforce productivity.

, By Technology (Machine Learning, Natural Language Processing, Computer Vision, Context-Aware Computing), By Application (Radiology, Cardiovascular, Obstetrics, Gastroenterology, Breast Screening, Gynecology), By End User (Hospitals, Clinics), Regional Insights, Competitive Landscape, Innovation Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expanded strongly, reaching estimated: 1.0 billion USD, 2024, supported by rising clinical throughput needs. It sustains estimated: 8.9% CAGR, 2024-2034.

- Segment Dominance : Solution software led adoption with a 61.3% share, 2023, reflecting rapid deployment across imaging workflows. This position implies estimated: 0.7 billion USD, 2024.

- Segment Dominance: Deep learning captured the largest model share, estimated: 58.0% share, 2023, driven by performance in complex image interpretation. It represents estimated: 0.6 billion USD, 2024.

- Driver: Neurology use cases accelerated demand as providers applied AI to neurological disorder workflows, estimated: 28.0% share, 2024. This driver supports higher utilization across 2024-2034 at estimated: 9.2% CAGR, 2024-2034.

- Restraint: Clinical validation and regulatory clearance cycles slow scale-up, extending time-to-market to estimated: 18.0 months, 2024. Compliance and data-governance costs pressure margins at estimated: 12.0% of revenue, 2024.

- Opportunity: Hospitals accelerate procurement for early detection and triage, representing estimated: 55.0% share, 2024. Enterprise rollouts can lift software attach rates to estimated: 40.0% share, 2034.

- Trend: Ultrasound workflow automation increases adoption via real-time guidance and automatic measurements, reducing scan time by estimated: 20.0%, 2024. Digital deployment expands via device-integrated and cloud-enabled delivery at estimated: 35.0% penetration, 2024.

- Regional Analysis: North America led performance in 2023 with estimated: 38.0% share, 2023, supported by higher digital imaging maturity. Regional investment sustains growth at estimated: 8.5% CAGR, 2024-2034.

By Solution

Software remains the primary revenue contributor within AI-enabled ultrasound systems as the market moves deeper into 2025. Software platforms accounted for about 61.3% of global revenue in 2023 and continue to dominate due to recurring license models and subscription-based upgrades. You see strong adoption where software integrates directly with existing ultrasound equipment, reducing capital expenditure while improving diagnostic consistency. Cloud deployment and wider broadband access across healthcare systems support faster implementation, particularly in multi-site hospital networks.

Hardware demand grows at a steadier pace, driven by AI-ready scanners and edge-computing devices deployed in emergency and point-of-care settings. Growth remains moderate because many providers prefer software retrofits over full system replacement. Services, however, show the fastest expansion outlook through 2034. Workforce shortages in AI system training, validation, and maintenance push providers to rely on third-party implementation and managed services. Service revenue is projected to grow at over 10% CAGR as hospitals prioritize operational continuity and compliance.

By Application

Neurology leads application-level revenue, holding roughly 39.5% share in 2023. AI-assisted ultrasound supports stroke triage, neuro-oncology monitoring, vascular assessment, and traumatic brain injury screening. You benefit from faster interpretation and reduced dependence on specialist availability, which remains limited in many regions. Radiology follows closely as AI improves lesion detection, image segmentation, and workflow throughput across high-volume imaging departments.

Breast screening records the strongest growth trajectory beyond 2025, supported by rising breast cancer incidence and public screening programs. Early-stage detection tools using AI-assisted ultrasound gain traction in regions with limited access to mammography. Government-backed initiatives such as India’s state-level screening programs accelerate adoption by expanding access and lowering diagnostic delays. Obstetrics and gynecology also post steady growth as maternal risk monitoring becomes more data-driven.

By End-User

Hospitals represent the largest end-user group, accounting for an estimated 55% of market revenue in 2024. You see higher uptake in tertiary and teaching hospitals where imaging volumes justify AI investment. Hospitals prioritize AI tools that shorten scan times, improve diagnostic accuracy, and support multidisciplinary care pathways.

Clinics show faster percentage growth, particularly diagnostic and specialty centers focused on women’s health and neurology. Lower-cost software solutions and portable ultrasound systems make AI adoption viable outside large hospital settings. This shift expands market reach and supports decentralized care models.

By Region

North America remains the leading regional market with about 32.1% share in 2023. High healthcare spending, rapid technology adoption, and a growing elderly population drive sustained demand. In the United States, adults aged over 65 are projected to exceed 80 million by 2040, increasing chronic disease imaging needs.

Asia Pacific records the fastest growth through 2034, supported by cost-sensitive healthcare expansion and rising demand for accurate prenatal and neurological diagnostics. You see strong momentum in China, India, and Southeast Asia as providers adopt AI to manage volume pressure at lower cost. Europe shows stable growth with emphasis on regulatory compliance, while Latin America and the Middle East and Africa remain emerging markets with improving infrastructure and targeted public health investments.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Solution

- Hardware

- Software

- Services

By Technology

- Machine Learning

- Natural Language Processing

- Context Aware Computing

- Computer Vision

By Applications

- Radiology

- Cardiovascular

- Gastroenterology

- Obstetrics

- Breast screening

- Gynecology

By End User

- Hospitals

- Clinics

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1,143.5 M |

| Forecast Revenue (2034) | USD 2,463.1 M |

| CAGR (2025-2034) | 8.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Solution (Hardware, Software, Services), By Technology (Machine Learning, Natural Language Processing, Context Aware Computing, Computer Vision), By Applications (Radiology, Cardiovascular, Gastroenterology, Obstetrics, Breast screening, Gynecology), By End User (Hospitals, Clinics) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Butterfly Network, Inc., Micron Technology, Inc., Imagia Cybernetics, Inc., Intel Corporation, Samsung, CloudMedX, Inc., GENERAL ELECTRIC COMPANY, EchoNous, Inc., Microsoft, General Vision, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Machine Learning, Natural Language Processing, Computer Vision, Context-Aware Computing), By Application (Radiology, Cardiovascular, Obstetrics, Gastroenterology, Breast Screening, Gynecology), By End User (Hospitals, Clinics), Regional Insights, Competitive Landscape, Innovation Trends & Forecast 2025–2034")

, By Technology (Machine Learning, Natural Language Processing, Computer Vision, Context-Aware Computing), By Application (Radiology, Cardiovascular, Obstetrics, Gastroenterology, Breast Screening, Gynecology), By End User (Hospitals, Clinics), Regional Insights, Competitive Landscape, Innovation Trends & Forecast 2025–2034")

, By Technology (Machine Learning, Natural Language Processing, Computer Vision, Context-Aware Computing), By Application (Radiology, Cardiovascular, Obstetrics, Gastroenterology, Breast Screening, Gynecology), By End User (Hospitals, Clinics), Regional Insights, Competitive Landscape, Innovation Trends & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

AI in Ultrasound Imaging Market

Published Date : 02 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date