- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI Model Fine-Tuning Services Market Forecast 2034 | CAGR 18.2%

Global AI Model Fine-Tuning Services Market Size, Share, Growth & Industry Analysis By Offering (Managed Fine-Tuning Services, Platform-Based Self-Service Fine-Tuning, Consulting & Advisory Services), By Fine-Tuning Method (PEFT/LoRA/QLoRA, Full-Parameter Supervised Fine-Tuning, RLHF, Instruction Tuning), By Vertical (BFSI, Healthcare, IT & Telecom, Retail & E-Commerce, Government & Defense, Manufacturing & Energy, Others), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2025–2034) | Largest Region (2025) |

| USD 3.8 Billion | USD 17.1 Billion | 18.2% | North America, 42.0% |

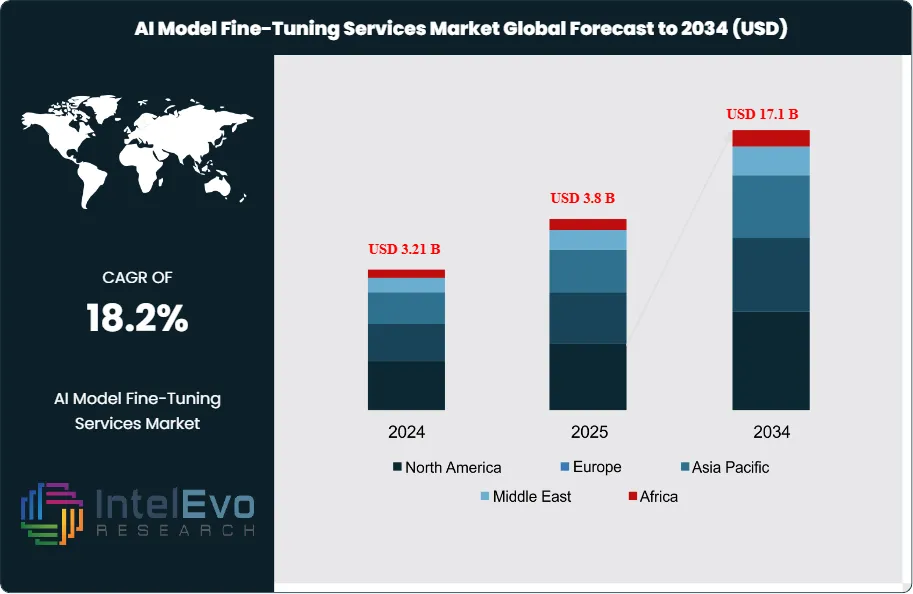

The AI Model Fine-Tuning Services Market was valued at approximately USD 3.21 Billion in 2024 and reached USD 3.8 Billion in 2025. The market is projected to grow to USD 17.1 Billion by 2034, expanding at a CAGR of 18.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 13.3 billion over the analysis period. AI model fine-tuning services encompass supervised fine-tuning, reinforcement learning from human feedback (RLHF), parameter-efficient fine-tuning (LoRA, QLoRA, adapters), domain adaptation, instruction tuning, and managed training infrastructure offered by cloud providers, specialized AI firms, and consulting organizations.

Get More Information about this report -

Request Free Sample Report

Demand for AI model fine-tuning services is accelerating as enterprises move from generic foundation model usage to customized deployments tailored to proprietary data, internal workflows, and regulated industry requirements. A 2025 survey by the NIST AI Safety Institute found that 57% of Fortune 500 companies had initiated at least one fine-tuning project, up from 28% in 2023. The EU AI Act, which entered enforcement in phases starting August 2025, has created a compliance-driven demand tier; organizations operating high-risk AI systems must demonstrate that models are tuned, evaluated, and documented against specific performance benchmarks. GDPR data residency requirements further push enterprises toward private fine-tuning environments rather than third-party API-only access.

Technology effects are pronounced. Parameter-efficient fine-tuning methods such as LoRA and QLoRA have reduced GPU compute costs by 60–80% compared to full-parameter training, dramatically lowering the barrier for mid-market enterprises. Multi-modal fine-tuning; covering text, image, audio, and code; grew from 12% of service engagements in 2023 to 29% in 2025. Retrieval-augmented generation (RAG) combined with fine-tuning is emerging as the preferred architecture for enterprise knowledge systems, with 41% of new projects adopting this hybrid approach.

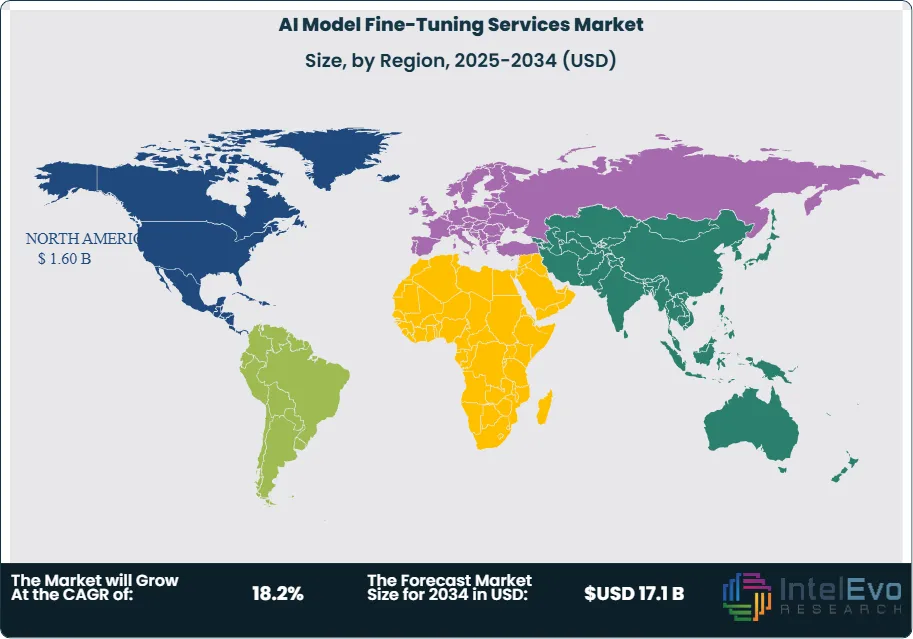

Regional investment patterns show North America leading with 42.0% share in 2025, anchored by hyperscaler infrastructure and venture capital concentration. Asia Pacific held 27.5% share, driven by China's aggressive LLM development programs and India's IT services sector pivoting toward AI training offerings. Europe accounted for 20.0%, shaped by AI Act compliance spending and sovereign model initiatives in France and Germany. Latin America contributed 5.5%, concentrated in Brazil's financial sector AI adoption. The Middle East and Africa held 5.0%, led by UAE government-backed AI programs. Risk factors include GPU supply constraints, data privacy litigation, model security vulnerabilities, and talent shortages in ML engineering. The AI model fine-tuning services market outlook remains strong as every major industry vertical accelerates custom model deployment through 2034.

, By Fine-Tuning Method (PEFT/LoRA/QLoRA, Full-Parameter Supervised Fine-Tuning, RLHF, Instruction Tuning), By Vertical (BFSI, Healthcare, IT & Telecom, Retail & E-Commerce, Government & Defense, Manufacturing & Energy, Others), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The AI model fine-tuning services market was valued at USD 3.8 billion in 2025 and is projected to reach USD 17.1 billion by 2034, registering a CAGR of 18.2% over the forecast period 2025–2034.

- Segment Dominance (By Offering): Managed fine-tuning services captured 52.6% of the market in 2025, valued at USD 2.00 billion, as enterprises outsourced model customization to specialized providers with GPU infrastructure and ML engineering talent.

- Segment Dominance (By Vertical): The BFSI vertical accounted for 24.0% of market revenue in 2025, driven by regulatory compliance demands, fraud detection fine-tuning, and customer service automation projects across banking and insurance.

- Driver: Enterprise adoption of foundation models surged to 57% among Fortune 500 firms in 2025; organizations require domain-specific fine-tuning to meet accuracy, compliance, and latency requirements that generic models cannot satisfy.

- Restraint: GPU compute scarcity and high training costs remain barriers; average fine-tuning project costs range from USD 50,000 to USD 500,000, limiting adoption among SMEs and resource-constrained organizations.

- Opportunity: Vertical-specific fine-tuning platforms for healthcare, legal, and financial services represent a USD 4.2 billion incremental opportunity through 2034, as regulated industries demand pre-validated, compliance-ready model customization.

- Trend: Parameter-efficient fine-tuning (LoRA, QLoRA, adapters) accounted for 64% of all fine-tuning engagements in 2025, up from 35% in 2023, reducing compute requirements by 60–80% and enabling rapid iteration cycles.

- Regional Analysis: North America led with 42.0% market share, generating USD 1.60 billion in 2025; hyperscaler cloud infrastructure and concentrated VC funding in the San Francisco Bay Area and New York anchored demand.

Competitive Landscape Overview

The AI model fine-tuning services market is moderately fragmented, with the top four providers collectively holding approximately 38% of global revenue in 2025. Competition is platform-driven, centering on GPU infrastructure access, proprietary fine-tuning toolchains, model evaluation frameworks, and vertical-specific expertise. Hyperscalers dominate through integrated cloud-plus-model offerings, while specialized AI firms compete on domain depth, data privacy guarantees, and faster time-to-deployment. Merger and acquisition activity intensified through 2024–2025 as enterprise software companies acquired fine-tuning startups to embed custom AI capabilities into their platforms. New entrants from India's IT services sector and open-source model communities have added pricing pressure in the mid-market tier.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Microsoft (Azure AI) | US | Leader | Azure OpenAI Fine-Tuning Service | North America | Launched GPT-4o fine-tuning API with enterprise data isolation (Feb 2025) |

| Google Cloud | US | Leader | Vertex AI Model Tuning | North America | Released Gemini fine-tuning with grounding integration (Mar 2025) |

| Amazon Web Services | US | Leader | Amazon Bedrock Custom Models | Global | Added LoRA fine-tuning for Anthropic Claude on Bedrock (Jan 2025) |

| OpenAI | US | Leader | OpenAI Fine-Tuning API | North America | Introduced supervised fine-tuning for GPT-4o and o1 series (Dec 2024) |

| Anthropic | US | Challenger | Claude Fine-Tuning (Enterprise) | North America | Expanded enterprise fine-tuning with Constitutional AI alignment (Apr 2025) |

| IBM (watsonx) | US | Challenger | watsonx.ai Tuning Studio | North America | Launched InstructLab community fine-tuning framework (Jun 2025) |

| Hugging Face | US | Challenger | AutoTrain / Training Cluster | Global | Partnered with Dell for on-premise fine-tuning appliances (Sep 2025) |

| Cohere | Canada | Challenger | Cohere Fine-Tuning for Enterprise | North America | Raised USD 500M Series D; expanded multilingual fine-tuning (May 2025) |

| Scale AI | US | Niche Player | Scale Donovan Fine-Tuning | North America | Won USD 250M US DoD contract for defense model tuning (Aug 2025) |

| Databricks (Mosaic) | US | Niche Player | Mosaic AI Fine-Tuning | North America | Acquired MosaicML training infrastructure; launched DBRX tuning (Jan 2026) |

By Offering:

Managed fine-tuning services dominated the market with a 52.6% share valued at USD 2.00 billion in 2025. Managed services include provider-led model customization engagements where the vendor handles data preparation, hyperparameter selection, training orchestration, evaluation, and deployment. Enterprises in regulated industries such as banking, healthcare, and government prefer managed services because providers carry the operational burden of GPU procurement, model versioning, and compliance documentation. Average engagement duration ranges from 6 to 16 weeks, with pricing structured as project-based fees or monthly retainers. Platform-based self-service fine-tuning held 33.4% share, generating USD 1.27 billion in 2025. This segment covers cloud-hosted APIs and no-code/low-code interfaces that allow enterprise ML teams to fine-tune models independently using their own data. Microsoft Azure OpenAI Service, Google Vertex AI, and Amazon Bedrock lead this segment. Growth is driven by ML-mature organizations that possess in-house data science teams and prefer direct control over training pipelines. Consulting and advisory services captured 14.0%, valued at USD 0.53 billion. This segment serves enterprises in early AI maturity stages, providing strategy development, use case identification, data readiness assessment, and fine-tuning roadmap creation before committing to managed or self-service engagements.

By Fine-Tuning Method:

Parameter-efficient fine-tuning (PEFT) led with 44.0% market share, valued at USD 1.67 billion in 2025. PEFT methods, including LoRA (Low-Rank Adaptation), QLoRA, and adapter layers, modify only a small subset of model parameters while freezing the base weights. This approach reduces GPU memory requirements by 60–80% and training time by 50–70% compared to full-parameter methods, making enterprise fine-tuning economically viable on mid-tier GPU clusters. Full-parameter supervised fine-tuning held 28.5% share, generating USD 1.08 billion. This method retrains all model weights on domain-specific datasets and delivers the highest accuracy gains for specialized applications such as medical coding, legal contract analysis, and scientific literature review. The cost per project is 3–5x higher than PEFT, limiting adoption to large enterprises and government agencies with dedicated GPU budgets. Reinforcement learning from human feedback (RLHF) and reward model training accounted for 17.5%, valued at USD 0.67 billion. RLHF is used to align model outputs with human preferences for safety, tone, and factual accuracy, particularly in customer-facing applications. Instruction tuning and prompt-based adaptation captured the remaining 10.0%, worth USD 0.38 billion, serving rapid-deployment use cases where organizations need quick behavioral adjustments without extensive retraining.

By Vertical:

Banking, financial services, and insurance (BFSI) led with 24.0% market share, generating USD 0.91 billion in 2025. Fine-tuning in BFSI targets fraud detection model accuracy, credit risk scoring, regulatory document processing, and customer service chatbot specialization. Basel III/IV compliance requirements and SEC disclosure rules are pushing financial institutions to tune models for auditability and explainability. Healthcare and life sciences held 18.5%, valued at USD 0.70 billion. Clinical note summarization, drug interaction prediction, medical imaging analysis, and patient communication systems require domain-adapted models trained on HIPAA-compliant data. Technology and telecommunications captured 16.0%, worth USD 0.61 billion, driven by code generation, IT helpdesk automation, and network operations intelligence. Retail and e-commerce accounted for 13.5%, generating USD 0.51 billion, with product recommendation engines, search relevance tuning, and dynamic pricing models as primary use cases. Government and defense held 11.0%, valued at USD 0.42 billion, driven by intelligence analysis, document classification, and cybersecurity threat detection. Manufacturing and energy contributed 9.0%, or USD 0.34 billion, focusing on predictive maintenance, quality inspection, and supply chain optimization. Other verticals including education, legal, and media accounted for the remaining 8.0%, valued at USD 0.30 billion.

By Enterprise Size:

Large enterprises commanded 68.0% of market revenue in 2025, valued at USD 2.58 billion. Organizations with over 5,000 employees possess the data volumes, compute budgets, and ML engineering teams required for complex fine-tuning projects. These enterprises typically engage in multi-model fine-tuning strategies, maintaining different tuned variants for customer service, internal knowledge management, and compliance functions. Fortune 500 adoption of fine-tuning services reached 57% in 2025, with average annual spending per enterprise ranging from USD 1.2 million to USD 8.5 million. Small and medium enterprises (SMEs) held 32.0%, generating USD 1.22 billion. SME adoption is accelerating due to parameter-efficient methods and platform-based self-service tools that have lowered entry costs to under USD 50,000 per project. Cloud providers offering pay-per-training-hour pricing models have been critical enablers. The SME segment grew at 23.1% year-over-year in 2025, outpacing the overall market, as vertical SaaS companies and mid-market retailers embedded fine-tuned models into their product offerings.

Regional Analysis

North America:

North America led the AI model fine-tuning services market with 42.0% share, generating USD 1.60 billion in 2025. The United States accounted for over 90% of regional revenue, driven by Silicon Valley's concentration of foundation model developers, enterprise cloud infrastructure from Microsoft Azure, Google Cloud, and AWS, and the largest pool of ML engineering talent globally. The US government's Executive Order on AI Safety (October 2023) and subsequent NIST AI Risk Management Framework updates have created compliance-driven demand for documented, auditable fine-tuning processes. Wall Street banks allocated an estimated USD 2.3 billion collectively to generative AI initiatives in 2025, with model fine-tuning consuming 30–40% of those budgets. Canada contributed through its AI research hubs in Montreal and Toronto, with Cohere and other startups driving enterprise fine-tuning innovation. Mexico's nearshoring trend is attracting AI service centers that support US-based fine-tuning operations with bilingual data annotation.

Europe:

Europe held 20.0% of the global market, valued at USD 0.76 billion in 2025. The EU AI Act, which classifies many enterprise AI deployments as high-risk systems, mandates that organizations demonstrate model customization, testing, and documentation against defined performance standards. This regulatory framework has created a distinct compliance-driven fine-tuning market segment worth an estimated USD 180 million in 2025 within Europe alone. Germany led regional demand through its automotive and manufacturing sectors, where fine-tuned models support quality control, supply chain management, and engineering documentation. The United Kingdom maintained strong momentum through its financial services sector in London; the FCA's AI governance guidelines encouraged banks to deploy fine-tuned models with explainability features. France's Mistral AI and sovereign model initiatives generated domestic fine-tuning demand. The Netherlands emerged as a hub for multilingual fine-tuning services, serving pan-European enterprises. Cloud data residency requirements under GDPR push organizations toward European-hosted fine-tuning infrastructure, benefiting regional providers.

Asia Pacific:

Asia Pacific captured 27.5% market share, generating USD 1.05 billion in 2025. China dominated regional demand with aggressive LLM development programs from Baidu, Alibaba Cloud, and ByteDance, each offering enterprise fine-tuning services for domestically developed models like ERNIE, Qwen, and Doubao. China's Cyberspace Administration regulations require that all generative AI services deployed within the country undergo government-approved safety evaluations, creating a compliance-driven fine-tuning requirement unique to the market. India held the second-largest share in the region, with IT services giants Infosys, TCS, and Wipro building dedicated AI fine-tuning practices that serve global enterprise clients. Japan contributed through industrial AI applications in manufacturing and robotics, with NEC and Fujitsu offering Japanese-language model tuning. South Korea's Samsung SDS and LG AI Research invested in semiconductor and electronics-specific model customization. Australia's government AI strategy allocated AUD 300 million for public sector AI modernization, including fine-tuning services for healthcare and defense applications.

Latin America:

Latin America accounted for 5.5% of the global market, generating USD 0.21 billion in 2025. Brazil led regional demand, driven by its financial sector; Banco do Brasil, Itau Unibanco, and Nubank each initiated fine-tuning projects for Portuguese-language customer service, credit scoring, and anti-money laundering models. Mexico contributed through its growing AI services sector, with companies establishing fine-tuning operations that serve both domestic enterprises and nearshore US clients. Argentina's technology community, centered in Buenos Aires, produced several fine-tuning startups focused on Spanish-language model adaptation for Latin American enterprises. Colombia invested in government AI modernization, including fine-tuned models for public health data analysis. Limited GPU infrastructure and cloud data center capacity remain constraints; most organizations rely on US-hosted cloud environments for training, with data residency negotiations adding 4–8 weeks to project timelines.

Middle East and Africa:

The Middle East and Africa region held 5.0% market share, valued at USD 0.19 billion in 2025. The UAE led regional investment through its national AI strategy and the establishment of the Technology Innovation Institute, which developed the Falcon LLM series and offers enterprise fine-tuning services. Saudi Arabia's Vision 2030 program allocated substantial budgets to AI adoption across government, healthcare, and energy sectors, with SDAIA (Saudi Data and AI Authority) mandating Arabic-language model customization for public services. Israel contributed through its AI startup sector, with companies such as AI21 Labs offering fine-tuning APIs for enterprise clients. South Africa represented the largest market in sub-Saharan Africa, with financial services and telecommunications firms piloting fine-tuned models for multilingual customer engagement. Government-backed AI hubs in Riyadh, Abu Dhabi, and Doha are attracting hyperscaler data center investments, which will improve local fine-tuning infrastructure availability through 2034.

Get More Information about this report -

Request Free Sample Report

Market Key Segments

By Offering

- Managed Fine-Tuning Services

- Platform-Based Self-Service Fine-Tuning

- Consulting and Advisory Services

By Fine-Tuning Method

- Parameter-Efficient Fine-Tuning (PEFT/LoRA/QLoRA)

- Full-Parameter Supervised Fine-Tuning

- Reinforcement Learning from Human Feedback (RLHF)

- Instruction Tuning and Prompt-Based Adaptation

By Vertical

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare and Life Sciences

- Technology and Telecommunications

- Retail and E-Commerce

- Government and Defense

- Manufacturing and Energy

- Others (Education, Legal, Media)

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.8 B |

| Forecast Revenue (2034) | USD 17.1 B |

| CAGR (2025-2034) | 18.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Managed Fine-Tuning Services, Platform-Based Self-Service Fine-Tuning, Consulting and Advisory Services), By Fine-Tuning Method, (Parameter-Efficient Fine-Tuning (PEFT/LoRA/QLoRA), Full-Parameter Supervised Fine-Tuning, Reinforcement Learning from Human Feedback (RLHF), Instruction Tuning and Prompt-Based Adaptation), By Vertical, (Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Technology and Telecommunications, Retail and E-Commerce, Government and Defense, Manufacturing and Energy, Others (Education, Legal, Media)), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises (SMEs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT (AZURE AI), GOOGLE CLOUD, AMAZON WEB SERVICES (AWS), OPENAI, ANTHROPIC, IBM (WATSONX), HUGGING FACE, COHERE, SCALE AI, DATABRICKS (MOSAIC AI), META PLATFORMS, NVIDIA (NEMO), MISTRAL AI, INFOSYS, TATA CONSULTANCY SERVICES (TCS), AI21 LABS, TOGETHER AI, ANYSCALE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Fine-Tuning Method (PEFT/LoRA/QLoRA, Full-Parameter Supervised Fine-Tuning, RLHF, Instruction Tuning), By Vertical (BFSI, Healthcare, IT & Telecom, Retail & E-Commerce, Government & Defense, Manufacturing & Energy, Others), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

, By Fine-Tuning Method (PEFT/LoRA/QLoRA, Full-Parameter Supervised Fine-Tuning, RLHF, Instruction Tuning), By Vertical (BFSI, Healthcare, IT & Telecom, Retail & E-Commerce, Government & Defense, Manufacturing & Energy, Others), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

, By Fine-Tuning Method (PEFT/LoRA/QLoRA, Full-Parameter Supervised Fine-Tuning, RLHF, Instruction Tuning), By Vertical (BFSI, Healthcare, IT & Telecom, Retail & E-Commerce, Government & Defense, Manufacturing & Energy, Others), By Enterprise Size (Large Enterprises, SMEs) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI Model Fine-Tuning Services Market?

Global AI model fine-tuning services market valued at USD 3.21B in 2024, reaching USD 17.1B by 2034, growing at a CAGR of 18.2% from 2026–2034.

Who are the major players in the AI Model Fine-Tuning Services Market?

MICROSOFT (AZURE AI), GOOGLE CLOUD, AMAZON WEB SERVICES (AWS), OPENAI, ANTHROPIC, IBM (WATSONX), HUGGING FACE, COHERE, SCALE AI, DATABRICKS (MOSAIC AI), META PLATFORMS, NVIDIA (NEMO), MISTRAL AI, INFOSYS, TATA CONSULTANCY SERVICES (TCS), AI21 LABS, TOGETHER AI, ANYSCALE, Others

Which segments covered the AI Model Fine-Tuning Services Market?

By Offering, (Managed Fine-Tuning Services, Platform-Based Self-Service Fine-Tuning, Consulting and Advisory Services), By Fine-Tuning Method, (Parameter-Efficient Fine-Tuning (PEFT/LoRA/QLoRA), Full-Parameter Supervised Fine-Tuning, Reinforcement Learning from Human Feedback (RLHF), Instruction Tuning and Prompt-Based Adaptation), By Vertical, (Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Technology and Telecommunications, Retail and E-Commerce, Government and Defense, Manufacturing and Energy, Others (Education, Legal, Media)), By Enterprise Size, (Large Enterprises, Small and Medium Enterprises (SMEs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI Model Fine-Tuning Services Market

Published Date : 03 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date