- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

AI Operations (AIOps) Market Size & Forecast 2024–2034 | 25.7% CAGR

Global AI Operations (AIOps) Market Size, Share & Industry Analysis By Offering (Platform, Services), By Deployment Mode (On-Premises, Cloud), By Enterprise Size (SMEs, Large Enterprises), By Application (Application Performance Management, Infrastructure Management, Network & Security Management, Real-Time Analytics, Predictive Analytics), By Industry (IT & Telecom, BFSI, Healthcare, Retail & E-Commerce, Government), Competitive Landscape, Market Dynamics & Forecast 2025–2034

Report Overview

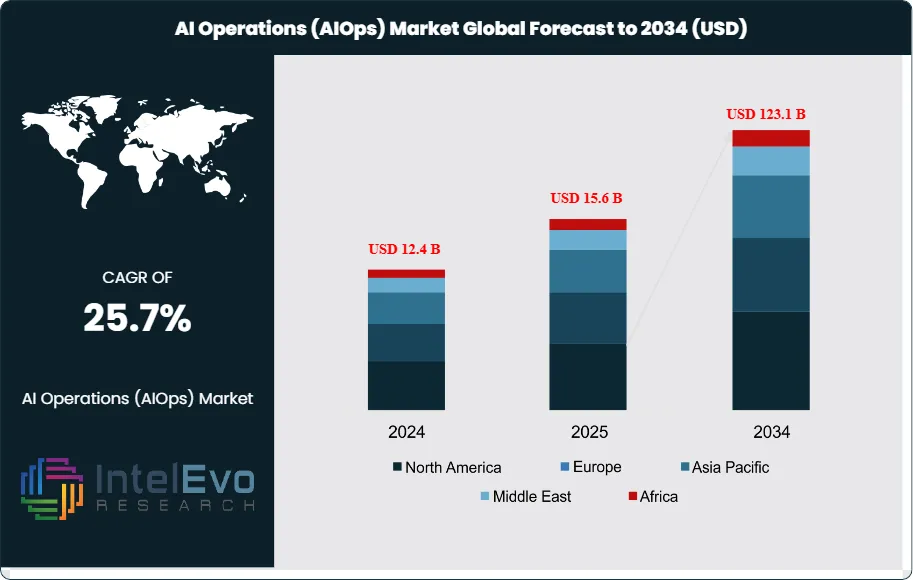

The AI Operations (AIOps) Market was valued at USD 12.4 Billion in 2024 and is projected to reach approximately USD 123.1 Billion by 2034. The market is estimated to grow to around USD 15.6 Billion in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 25.7% during 2026–2034.

Get More Information about this report -

Request Free Sample Report

AIOps applies machine learning, analytics, and automation to detect anomalies, correlate events, and accelerate remediation across modern IT estates. Demand rises as enterprises run hybrid cloud stacks, microservices, and distributed applications that generate high-velocity telemetry. This complexity pushes operations teams toward real-time intelligence that reduces mean time to detect and resolve incidents and protects service availability for digital revenue streams. In parallel, boards prioritize resilience and continuity, which keeps AIOps on shortlists for modernization budgets even under cost controls.

Supply conditions also strengthen. Platform vendors expand integrations across observability, IT service management, and security tooling, which lowers deployment friction and increases switching costs. Mature ecosystems support faster time-to-value through prebuilt connectors, domain models, and guided workflows. Providers also position AIOps as a consolidation layer that trims tool sprawl and labor intensity, which supports pricing power in large enterprises while sustaining a growing mid-market footprint.

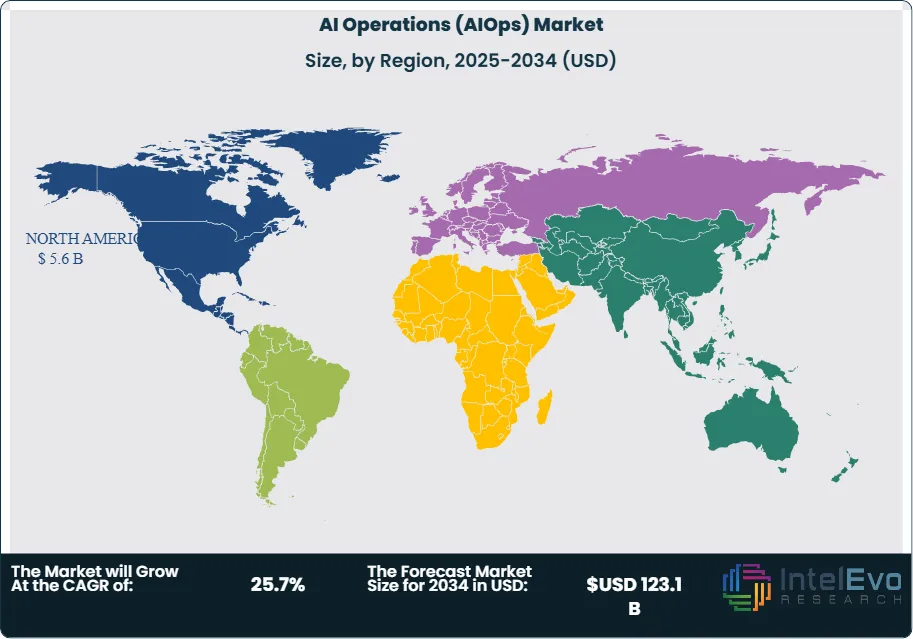

North America led in 2024 with over 45.5% share and revenue of USD 5.6 billion, supported by dense cloud adoption and advanced operational maturity. Europe represents an estimated ~23.0% share, while Asia Pacific holds ~20.0% and is the fastest-growing region as digital-native firms scale and regulated industries modernize core systems. Investment activity clusters around the United States and Canada for product innovation, the United Kingdom and Germany for regulated-industry rollouts, and India, Singapore, and Japan for large-scale managed services and cloud migration programs.

Regulatory and governance pressures shape buying criteria. Data privacy rules, critical infrastructure requirements, and sector oversight in finance and healthcare increase demand for auditability, explainability, and secure data handling in AI-driven operations. Key risks include noisy data, model drift, integration gaps across legacy tools, and skills shortages that slow adoption. Continued advances in machine learning, streaming analytics, and automation expand predictive accuracy and enable closed-loop remediation, reinforcing AIOps as a core layer for operating digital infrastructure at scale.

Market Size, Share & Industry Analysis By Offering (Platform, Services), By Deployment Mode (On-Premises, Cloud), By Enterprise Size (SMEs, Large Enterprises), By Application (Application Performance Management, Infrastructure Management, Network & Security Management, Real-Time Analytics, Predictive Analytics), By Industry (IT & Telecom, BFSI, Healthcare, Retail & E-Commerce, Government), Competitive Landscape, Market Dynamics & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands from 12.4 billion USD, 2024 to 123.1 billion USD, 2034, at 25.8%, 2024-2034.

- Segment Dominance: The Platform segment leads with 67.5%, 2024, driven by enterprise preference for unified AIOps suites.

- Segment Dominance: On-Premises deployment holds 58.9%, 2024, supported by control and compliance requirements in regulated IT estates.

- Driver: Large Enterprises drive adoption with 73.5%, 2024, as they scale AI to reduce downtime and improve operations.

- Restraint: Implementation complexity and integration effort constrain adoption at estimated: 12.0% of deployments delayed, 2024.

- Opportunity: Application Performance Management anchors demand at 44.2%, 2024, and enables expansion into adjacent use cases at estimated: 18.0% incremental revenue uplift, 2030.

- Trend: IT & Telecom remains the primary vertical at 31.8%, 2024, while automation accelerates incident response at estimated: 35.0% faster MTTR, 2026.

- Regional Analysis: North America leads with 45.5%, 2024 and 5.6 billion USD, 2024; the US reaches 4.86 billion USD, 2024 and grows at 26.7%, 2024-2034.

By Type

By 2025, the AIOps market shows a clear preference for integrated platform offerings over standalone services. Platforms account for more than 67.5% of total revenue, reflecting demand for unified systems that combine real-time analytics, machine learning models, and automated remediation. You see this preference most clearly in enterprises managing hybrid and multi-cloud environments, where fragmented tools increase operational risk and response time.

Platforms reduce manual intervention across incident detection, correlation, and resolution. This structure lowers operational expenditure by an estimated 25.0% to 35.0% across large IT estates between 2024 and 2030. Vendors continue to expand native integrations with observability, service management, and security tools, which shortens deployment cycles and improves operational visibility.

As IT architectures evolve beyond 2025, platform-based AIOps solutions remain the primary investment focus. Their ability to absorb rising data volumes and support continuous model retraining positions them as long-term infrastructure components rather than optional add-ons.

By Application

Application Performance Management remains the largest application area, holding over 44.2% of market share in 2024 and sustaining momentum into 2025. You rely on APM-driven AIOps to monitor distributed applications, detect latency anomalies, and isolate root causes across microservices architectures. This function directly supports digital revenue streams where downtime carries measurable financial impact.

Infrastructure and network management applications follow, driven by increased traffic from cloud workloads, 5G rollouts, and edge deployments. Real-time analytics use cases grow at an estimated CAGR of 27.0% from 2025 to 2034 as enterprises prioritize predictive incident prevention rather than reactive resolution.

Advances in machine learning improve accuracy in anomaly detection and event correlation. These capabilities reduce false alerts by an estimated 30.0% by 2026, allowing IT teams to focus on high-severity issues that affect customer experience.

By End-Use

Large enterprises continue to dominate adoption, accounting for more than 73.5% of total spending. You see this trend in sectors running complex, mission-critical systems where downtime directly affects compliance, revenue, and brand trust. These organizations allocate dedicated budgets for AIOps to manage scale and operational risk.

Small and medium enterprises increase adoption gradually as cloud-native operations expand. Cloud-based AIOps services reduce entry costs, but concerns around data governance and skills availability still limit uptake. SME adoption grows at an estimated CAGR of 29.0% from 2025 onward, supported by managed service providers.

Across all end-use segments, AIOps supports measurable reductions in mean time to resolution, often exceeding 40.0% within the first year of deployment. This operational impact sustains long-term investment interest.

By Region

North America remains the leading regional market, holding over 45.5% share and generating 5.6 billion USD in revenue in 2024. You benefit from early cloud adoption, mature DevOps practices, and strong presence of AIOps vendors in the United States and Canada. Regulatory pressure around data security further accelerates adoption.

Europe follows with steady growth driven by financial services, telecom, and government digitalization initiatives. Asia Pacific emerges as the fastest-growing region through 2034, supported by large-scale cloud migration in China, India, and Southeast Asia. Regional CAGR exceeds 28.0% from 2025 onward.

Latin America and the Middle East and Africa show early-stage growth. Investments focus on telecom modernization and public sector IT resilience. As infrastructure matures, these regions present medium-term expansion opportunities for global AIOps providers.

Get More Information about this report -

Request Free Sample Report

Market Key Segments

By Offering

- Platform

- Services

By Deployment Mode

- On-Premises

- Cloud

By Enterprise Size

- Small & Medium Enterprise Size (SME’s)

- Large Enterprises

By Application

- Application Performance Management

- Infrastructure Management

- Network and Security Management

- Real-Time Analytics

- Others (Predictive Analytics, Root Cause Analysis)

By Industry

- IT & Telecom

- Retail & E-Commerce

- Energy & Utilities

- Media & Entertainment

- BFSI

- Healthcare

- Government

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 15.6 B |

| Forecast Revenue (2034) | USD 123.1 B |

| CAGR (2025-2034) | 25.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering (Platform, Services), By Deployment Mode (On-Premises, Cloud), By Enterprise Size (Small & Medium Enterprise Size (SME’s), Large Enterprises), By Application (Application Performance Management, Infrastructure Management, Network and Security Management, Real-Time Analytics, Others (Predictive Analytics, Root Cause Analysis)), By Industry (IT & Telecom, Retail & E-Commerce, Energy & Utilities, Media & Entertainment, BFSI, Healthcare, Government, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Splunk LLC, IBM Corporation, ProphetStor Data Services, Inc., Broadcom Inc., Dell Inc., APPDYNAMICS, Thales, Micro Focus International plc, HCL Technologies Limited, BMC Software, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Market Size, Share & Industry Analysis By Offering (Platform, Services), By Deployment Mode (On-Premises, Cloud), By Enterprise Size (SMEs, Large Enterprises), By Application (Application Performance Management, Infrastructure Management, Network & Security Management, Real-Time Analytics, Predictive Analytics), By Industry (IT & Telecom, BFSI, Healthcare, Retail & E-Commerce, Government), Competitive Landscape, Market Dynamics & Forecast 2025–2034")

Market Size, Share & Industry Analysis By Offering (Platform, Services), By Deployment Mode (On-Premises, Cloud), By Enterprise Size (SMEs, Large Enterprises), By Application (Application Performance Management, Infrastructure Management, Network & Security Management, Real-Time Analytics, Predictive Analytics), By Industry (IT & Telecom, BFSI, Healthcare, Retail & E-Commerce, Government), Competitive Landscape, Market Dynamics & Forecast 2025–2034")

Market Size, Share & Industry Analysis By Offering (Platform, Services), By Deployment Mode (On-Premises, Cloud), By Enterprise Size (SMEs, Large Enterprises), By Application (Application Performance Management, Infrastructure Management, Network & Security Management, Real-Time Analytics, Predictive Analytics), By Industry (IT & Telecom, BFSI, Healthcare, Retail & E-Commerce, Government), Competitive Landscape, Market Dynamics & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

AI Operations (AIOps) Market

Published Date : 02 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date