- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI Agricultural Spraying Drone Market Size & Forecast | CAGR 18.5%

Global AI Agricultural Spraying Drone Market Size, Share, Growth & Industry Analysis By Spray Tank Capacity (Small Under 10L, Medium 10–30L, Large 30–60L, Ultra-Large Over 60L), By Crop Application (Paddy & Cereals, Fruits & Vegetables, Oilseeds & Pulses, Plantation Crops, Turf), By AI Technology Feature (Autonomous Flight, AI Mapping, Computer Vision, Terrain Following, Swarm Coordination) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 2.14 Billion | USD 9.86 Billion | 18.5% | Asia Pacific, 52.3% |

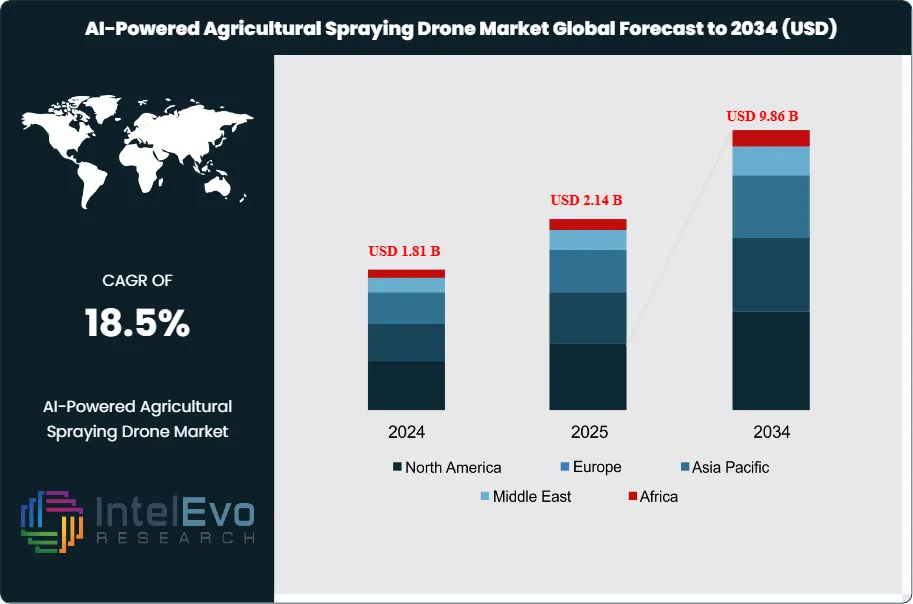

The AI-Powered Agricultural Spraying Drone Market was valued at approximately USD 1.81 Billion in 2024 and reached USD 2.14 Billion in 2025. The market is projected to grow to USD 9.86 Billion by 2034, expanding at a CAGR of 18.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 7.72 Billion over the analysis period, driven by rapid AI model integration into drone spray systems, surging demand for precision pesticide application to meet global sustainability mandates, labor scarcity in agricultural markets across Asia Pacific and North America, and progressive regulatory liberalization of commercial agricultural drone operations across major farming jurisdictions.

Get More Information about this report -

Request Free Sample ReportAI-powered agricultural spraying drones differ from conventional agricultural drones through the integration of machine learning vision systems, real-time terrain modeling, variable-rate spray prescription mapping, and autonomous obstacle avoidance. These capabilities enable AI agricultural spray drones to identify crop stress zones, weed infestations, and pest activity from onboard multispectral or RGB camera systems; calculate precise spray volumes for individual field zones; and adjust nozzle pressure, boom height, and flight speed dynamically to maximize spray deposition efficiency while minimizing chemical drift. The result is measurable reduction in pesticide and fungicide usage of 20-40% compared to conventional ground or aerial application, combined with labor savings equivalent to 10-15 human agricultural workers per drone unit per day in paddy rice and vegetable production systems.

Regulatory frameworks are progressively enabling commercial expansion. China's Civil Aviation Administration (CAAC) established the world's first comprehensive agricultural UAS operation framework, enabling large-scale commercial agricultural drone services across more than 100 million hectares of farmland. Japan's MLIT and Ministry of Agriculture amended unmanned aircraft regulations in 2022-2024 to permit BVLOS (Beyond Visual Line of Sight) agricultural drone operations, accelerating commercial service expansion. The US FAA's 2024 final rule on commercial UAS operations broadened waiver pathways for agricultural BVLOS operations, reducing regulatory barriers that previously confined US adoption to visual line-of-sight applications. India's DGCA Type Certification framework for agricultural drones, established through the Drone Rules 2021, has enabled a domestic agricultural drone manufacturing sector that grew to over 200 registered manufacturers by 2025.

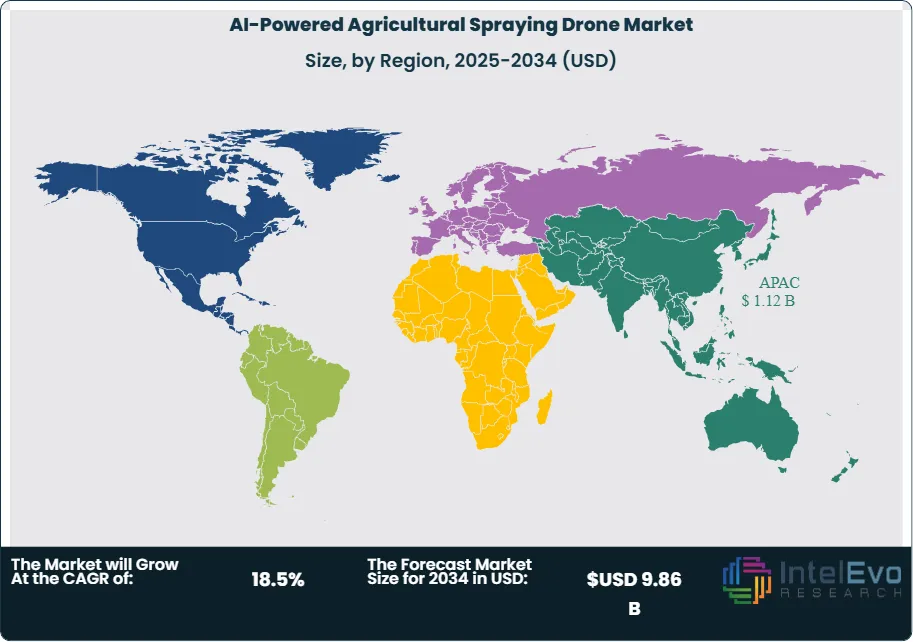

Asia Pacific dominated the AI-powered agricultural spraying drone market with a 52.3% share in 2025, equivalent to USD 1.12 Billion, driven by China and Japan's established large-scale commercial agricultural drone service industries and India's rapidly expanding domestic market. North America is the second-largest regional market and fastest-growing outside Asia Pacific, advancing at a projected CAGR of 21.4% through 2034. AI performance improvements, including real-time object detection accuracy exceeding 94% in commercial field conditions and battery systems achieving 30+ minutes of spray flight time per charge, are making AI agricultural spray drones technically competitive with conventional manned aircraft and ground-based spray equipment across a growing range of crop and terrain configurations.

, By Crop Application (Paddy & Cereals, Fruits & Vegetables, Oilseeds & Pulses, Plantation Crops, Turf), By AI Technology Feature (Autonomous Flight, AI Mapping, Computer Vision, Terrain Following, Swarm Coordination) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global AI-powered agricultural spraying drone market was valued at USD 2.14 Billion in 2025 and is forecast to reach USD 9.86 Billion by 2034, registering a CAGR of 18.5% during the 2026-2034 forecast period.

- Segment Dominance: By spray capacity, medium-capacity AI spraying drones (10-30L tank capacity) held the largest share at 48.4% of the market in 2025, balancing flight duration, payload capacity, and operational flexibility across paddy rice, wheat, corn, and vegetable crop applications.

- Segment Dominance: By crop application, paddy rice and cereal crops accounted for 42.6% of the AI-powered agricultural spraying drone market in 2025, driven by China and Japan's large-scale commercial rice drone service operations and the high labor intensity of traditional paddy rice pesticide application methods.

- Driver: Agricultural labor scarcity across Asia Pacific and North America, where the agricultural workforce declined by an estimated 12-18% between 2018 and 2025 in key farming regions, is the primary structural driver compelling farm operators to adopt AI spraying drones as a cost-effective labor substitution technology.

- Restraint: Regulatory limitations on BVLOS agricultural drone operations in Europe and Latin America, where aviation authority UAS frameworks continue to impose visual line-of-sight restrictions on most commercial agricultural drone spraying operations, constrain market penetration in regions with favorable agricultural production conditions.

- Opportunity: India's PM-KISAN drone adoption program and PLI incentive scheme for agricultural drone manufacturing, which allocated approximately USD 3.4 Billion equivalent in subsidies and incentives for agricultural mechanization including drones through 2025, represents a rapidly scaling addressable market estimated at USD 920 Million by 2034 in the world's second-largest agricultural economy.

- Trend: Integration of AI-based prescription spray maps generated from satellite or drone multispectral imagery into agricultural spraying drone flight planning systems grew at approximately 32.8% annually in 2025, enabling variable-rate application of pesticides and fertilizers that reduce chemical input costs by 20-40% versus uniform broadcast application.

- Regional Analysis: Asia Pacific led the AI-powered agricultural spraying drone market with a 52.3% share, equivalent to USD 1.12 Billion in 2025, driven by China's 130+ Million hectares of drone-serviceable farmland, Japan's established commercial rice spraying drone service sector, and India's rapidly scaling domestic drone manufacturing base.

Competitive Landscape Overview

The AI-powered agricultural spraying drone market is highly consolidated at the hardware platform level, with DJI, XAG, Yamaha Motor, and Hylio collectively accounting for approximately 62% of global market revenues in 2025. DJI alone holds an estimated 34% global share through its Agras product line. Competition centers on AI sensing capability, spray system precision, battery endurance per flight cycle, and software platform integration depth. Hardware-level competition is being increasingly supplemented by competition on AI fleet management platforms, prescription map integration quality, and drone-as-a-service commercial models. New entrants from India and Southeast Asia are intensifying mid-market competition on price, with locally manufactured drone platforms achieving price points 40-60% below premium Chinese competitors.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| DJI (SZ DJI Technology) | China | Leader | Agras T60 AI Spraying Drone | Asia Pacific & Global | Launched Agras T60 with dual-atomization AI spraying system; expanded global agricultural drone network; Q1 2025. |

| XAG Co. Ltd. | China | Leader | XAG P100 AI-Guided Agricultural Drone | Asia Pacific | Signed government partnership for AI drone-based pesticide reduction program in 5 Chinese provinces; 2025. |

| Yamaha Motor Co. | Japan | Leader | FAZER R G2 Precision Agriculture Drone | Asia Pacific | Launched FAZER R G2 with upgraded AI terrain-following and spray optimization; targeted Japanese rice market; Q2 2025. |

| Hylio Inc. | USA | Leader | AG-230 AI Agricultural Spraying Drone | North America | Expanded US dealer network to 42 states; received FAA waiver for BVLOS agricultural drone operations; March 2025. |

| Rantizo | USA | Challenger | AI-Guided Drone Application Platform | North America | Partnered with a major US ag retailer chain to offer drone-as-a-service spray programs; Q3 2025. |

| ideaForge Technology | India | Challenger | SWITCH 2.0 Agricultural Spray Drone | Asia Pacific | Secured USD 15M Series C to expand agricultural drone manufacturing capacity in India; 2025. |

| Kray Technologies | India | Niche Player | Kray X6 AI Spraying Drone | Asia Pacific | Received DGCA type certification for commercial agricultural drone spraying; expanded to 8 Indian states; 2025. |

| Aviant | Norway | Niche Player | AI Drone Delivery & Spraying Platform | Europe | Secured European drone spraying regulatory approval under EASA UAS category for Nordic precision farming; 2025. |

| AeroVironment | USA | Niche Player | Quantix Recon with Spray Integration | North America | Integrated AI variable-rate spray prescription maps with Quantix platform for US specialty crop markets; Q3 2025. |

| EFT (Shenzhen EFT Intelligent) | China | Niche Player | E616P Heavy-Lift AI Spraying Drone | Asia Pacific & Emerging Markets | Expanded distribution of E616P AI spray drone to Southeast Asian and South American agricultural markets; Jan 2026. |

By Spray Tank Capacity

The AI-powered agricultural spraying drone market by spray tank capacity spans small capacity (under 10L), medium capacity (10-30L), large capacity (30-60L), and ultra-large capacity (over 60L) platforms. Medium-capacity AI spraying drones held the dominant segment share at 48.4% of the market in 2025, equivalent to approximately USD 1.04 Billion. This capacity class, exemplified by DJI's Agras T30 and T40 series and XAG's P40 and P100, balances spray payload with flight duration and maneuverability across the widest range of agricultural terrain and crop types. Medium-capacity drones achieve operational coverage rates of 40-80 hectares per day in flat terrain paddy rice or wheat production systems, providing labor productivity ratios that justify ROI for commercial drone service providers operating at scale. The 10-30L tank class is also the most technically developed, with the broadest range of AI spray prescription and variable-rate application integrations across competing platforms.

Large-capacity AI spraying drones with 30-60 liter tanks represented 28.6% of the market in 2025, with demand concentrated in large-scale row crop agriculture in China, Brazil, and the United States where field sizes support extended flight paths without refilling. DJI's Agras T60, launched in Q1 2025 with a 60-liter dual-tank capacity and AI dual-atomization spray system, represents the current large-capacity benchmark. Small-capacity drones under 10 liters held 14.2% of the market in 2025, serving orchard, vineyard, specialty crop, and smallholder farm applications where field size and canopy structure limit operation of larger platforms. Ultra-large capacity platforms exceeding 60 liters represented the remaining 8.8% of the AI-powered agricultural spraying drone market by capacity in 2025, targeting large-area aerial application operations where maximum payload reduces refill frequency.

By Crop Application

The AI-powered agricultural spraying drone market by crop application covers paddy rice and cereal crops, fruits and vegetables, oilseeds and pulses, plantation crops, and turf and specialty applications. Paddy rice and cereal crops held the dominant application share at 42.6% of the market in 2025, equivalent to approximately USD 912 Million. China's paddy rice production system, encompassing approximately 30 million hectares of irrigated rice paddy, constitutes the world's largest single application market for agricultural spray drones, where drone spraying is estimated to cover over 20% of total rice pesticide application area as of 2025. Japan's commercial rice drone spraying sector, developed since the 1990s through Yamaha's RMAX manned helicopter platform and now migrating to AI-enabled multirotor systems, provides a mature commercial model that demonstrates the scale of adoption achievable in paddy rice production. Wheat and corn spraying in China, India, and the United States are growing rapidly as AI variable-rate spray systems prove efficacy in large-scale row crop environments.

Fruits and vegetables represented 28.4% of the AI-powered agricultural spraying drone market in 2025. Orchard spraying for apple, pear, citrus, and grape production requires AI obstacle avoidance and canopy penetration optimization that is technically more demanding than open-field crop applications, driving premium pricing in this segment. Oilseeds and pulses accounted for 14.8% of the market in 2025, driven by soybean, canola, and sunflower spray applications in Brazil, Canada, and Argentina. Plantation crops including palm oil, rubber, coffee, and cocoa represented 8.6% of the AI agricultural spray drone market in 2025, with Southeast Asian palm oil plantations representing the highest-volume individual plantation crop application. Turf, ornamentals, and specialty applications collectively held the remaining 5.6%.

By AI Technology Feature

The AI-powered agricultural spraying drone market by AI technology feature segments into autonomous flight and obstacle avoidance, AI variable-rate spray prescription mapping, computer vision-based crop health assessment, AI terrain-following and tilt compensation, and multi-drone swarm coordination. Autonomous flight and obstacle avoidance held the largest AI feature segment share at 36.4% of the market in 2025. This capability, enabled by forward and downward-facing lidar or ultrasonic obstacle detection systems combined with real-time path replanning algorithms, is the foundational AI feature that distinguishes AI-powered agricultural spray drones from conventional remotely piloted agricultural aircraft. DJI's Agras series incorporates multi-directional radar obstacle sensing that enables safe autonomous flight at 5-7 meters above crop canopy across complex terrain including hillside orchards and irregular-shaped field boundaries.

AI variable-rate spray prescription mapping represented 28.8% of the AI technology feature segment in 2025 and is the fastest-growing individual feature category at an estimated CAGR of 26.4%, as integration of drone multispectral imagery, NDVI analysis, and AI pest detection models enables precise spatial targeting of chemical applications. Computer vision-based crop health assessment held 18.6% of the segment, enabling real-time identification of disease symptoms, insect pest populations, and nutrient deficiency patterns during spray operations. AI terrain-following and tilt compensation systems, which maintain consistent spray height and adjust nozzle angle on sloped terrain, accounted for 10.4% of the AI feature segment in 2025. Multi-drone swarm coordination, where AI fleet management systems orchestrate simultaneous operation of 2-10 drones across a single field without interference, held the remaining 5.8% and is growing rapidly in large-scale commercial service operations.

By Business Model

The AI-powered agricultural spraying drone market by business model covers direct hardware sales, drone-as-a-service (DaaS) subscription and contract services, hardware-plus-software subscription bundling, and government-sponsored agricultural mechanization programs. Direct hardware sales held the largest business model share at 44.8% of the AI-powered agricultural spraying drone market in 2025. This model dominates in China and Japan, where commercial agricultural drone service companies and larger farming operations purchase fleets of AI spray drones for in-house operation, supported by manufacturer dealer networks offering training, maintenance, and parts supply. Drone-as-a-service models, where service providers charge per-hectare or seasonal contract fees for spray services delivered using their own AI drone fleets, accounted for 32.6% of the market in 2025 and are the fastest-growing commercial model in North America, India, and Southeast Asia. Hardware-plus-software subscription models, which bundle drone hardware with AI prescription mapping, fleet management, and data analytics software on annual subscription terms, held 16.2% of the market in 2025. Government-sponsored agricultural mechanization programs, which subsidize drone hardware purchase or usage for smallholder farmers, represented 6.4% of the market.

Regional Analysis

Asia Pacific

Asia Pacific AI-powered agricultural spraying drone market held a 52.3% share in 2025, generating approximately USD 1.12 Billion in revenue, and represents the world's most commercially mature agricultural drone application market. China accounts for the largest national market globally, where the CAAC's progressive agricultural UAS regulatory framework, combined with government subsidy programs for agricultural mechanization under the Ministry of Agriculture and Rural Affairs, has enabled large-scale commercial drone spraying services across rice, wheat, corn, and vegetable production. By 2025, an estimated 50,000+ commercial agricultural drone operators were registered in China, with the total agricultural drone spraying area exceeding 1 Billion spray applications, making it the world's largest single national agricultural drone spraying market. Japan's commercial agricultural drone spraying sector, centered on paddy rice production, uses AI multirotor systems from Yamaha Motor and DJI through a network of licensed commercial spraying service operators supported by the Japan Agricultural Aviation Association. India is the fastest-growing national market within Asia Pacific, where the DGCA Drone Rules 2021 and the government's PLI scheme for drone manufacturing have generated over 200 registered agricultural drone manufacturers, with the PM-KISAN drone adoption program directing subsidies toward farmer purchases of AI spraying drones. Australia contributes through large-scale broadacre cropping AI drone spray operations in wheat, canola, and sugarcane, where the CASA's UAS operational rules permit commercial agricultural applications with appropriate operator certification.

North America

North America held approximately 22.4% of the global AI-powered agricultural spraying drone market in 2025, generating approximately USD 480 Million. The United States is the dominant national market, where FAA's 2024 amendments to commercial UAS operational rules significantly broadened the BVLOS waiver pathway for agricultural operations, enabling commercial drone service providers to operate AI spray drones across larger field areas without human visual observers stationed along the flight path. The US commercial agricultural spray drone service sector is experiencing rapid consolidation, with larger drone service companies aggregating regional operators and expanding into multi-state service networks supported by AI fleet management platforms. Key crops driving US AI drone spray adoption include specialty crops including almonds, pistachios, blueberries, and wine grapes in California and the Pacific Northwest, where premium product pricing justifies precision spray technology investment. Corn, soybean, and wheat spray applications in the Midwest are growing as AI prescription spray map integration improves chemical use efficiency in large-scale row crop systems. Canada contributes through canola and wheat spraying in Alberta and Saskatchewan, where BVLOS exemptions from Transport Canada enable commercial drone services across large prairie field units. Mexico is an emerging market where horticultural export crop production drives premium drone spray service adoption.

Europe

Europe held approximately 12.6% of the global AI-powered agricultural spraying drone market in 2025, generating approximately USD 270 Million. The European Union's UAS regulatory framework under EASA Commission Delegated Regulation (EU) 2019/945 and Implementing Regulation (EU) 2021/664 establishes the commercial UAS operational framework, with most agricultural spray drone operations requiring specific category authorization that involves operational risk assessment submission to national aviation authorities. This regulatory process creates a compliance overhead that constrains market penetration compared to Asia Pacific, where simpler agricultural drone licensing frameworks exist. However, the EU's Farm to Fork Strategy target to reduce chemical pesticide use by 50% by 2030 creates strong demand-side incentive for precision spray technology that AI agricultural drones uniquely satisfy. Germany and France are the largest European AI spray drone markets, driven by large-scale wine grape and cereal crop production. Spain's intensive fruit and vegetable export sector and Netherlands' greenhouse and high-value outdoor specialty crop production represent growing applications. The UK's Civil Aviation Authority has established favorable conditions for commercial agricultural drone spraying under BVLOS exemptions in sparsely populated farming areas, supporting growth in the English and Scottish arable farming markets.

Latin America

Latin America held approximately 8.4% of the global AI-powered agricultural spraying drone market in 2025, generating approximately USD 180 Million. Brazil is the largest and strategically most significant national market, where the world's largest soybean production system encompassing approximately 43 million hectares of cultivated area represents a massive potential AI spray drone application zone. Brazil's ANAC (National Civil Aviation Agency) has established agricultural drone operation regulations that permit commercial spraying operations under specific conditions, but BVLOS restrictions continue to limit the operational efficiency of commercial service providers in very large field environments. The practical minimum field size for economically viable AI drone spray services in Brazilian soybean and corn production is estimated at approximately 50-100 hectares, which covers the majority of the country's commercial farming operations. Argentina is the second-largest Latin American market, with soybean and wheat production driving AI spray drone service demand in the Pampas agricultural region. Colombia and Ecuador represent growing specialty crop markets where coffee, banana, and cut flower export production drives precision spray technology adoption. Chile's wine grape and premium fruit export sectors create demand for AI precision spray capability in sloped vineyard terrain where autonomous obstacle avoidance delivers the most significant efficiency advantages over conventional application methods.

Middle East & Africa

The Middle East and Africa region held approximately 4.3% of the global AI-powered agricultural spraying drone market in 2025, generating approximately USD 92 Million. The UAE is the most active regional market, where the General Civil Aviation Authority's progressive UAS regulatory framework and government investment in agricultural technology through initiatives including the UAE Food Security Strategy 2051 have created a receptive environment for AI precision agriculture drone adoption. Saudi Arabia's Vision 2030 agricultural modernization program includes precision agriculture technology as a strategic investment area, and government funding for smart farming demonstrations has introduced AI agricultural spraying drones into date palm, wheat, and vegetable production systems. South Africa is the leading African market, where the South African Civil Aviation Authority's UAS regulations permit commercial agricultural drone operations under Part 101 of the Civil Aviation Regulations, supporting growing adoption in wine grape, deciduous fruit, and large-scale grain production regions. Kenya and Ethiopia represent emerging Sub-Saharan African markets where development program funding from organizations including the UN Food and Agriculture Organization and USAID is introducing AI agricultural spray drone technology to smallholder farming systems as a means of reducing pesticide application labor costs and improving crop protection effectiveness.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Spray Tank Capacity

- Small Capacity (Under 10L)

- Medium Capacity (10-30L)

- Large Capacity (30-60L)

- Ultra-Large Capacity (Over 60L)

By Crop Application

- Paddy Rice & Cereal Crops

- Fruits & Vegetables

- Oilseeds & Pulses

- Plantation Crops

- Turf & Specialty Applications

By AI Technology Feature

- Autonomous Flight & Obstacle Avoidance

- AI Variable-Rate Spray Prescription Mapping

- Computer Vision-Based Crop Health Assessment

- AI Terrain-Following & Tilt Compensation

- Multi-Drone Swarm Coordination

By Business Model

- Direct Hardware Sales

- Drone-as-a-Service (DaaS)

- Hardware Plus Software Subscription

- Government-Sponsored Agricultural Mechanization Programs

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.14 B |

| Forecast Revenue (2034) | USD 9.86 B |

| CAGR (2025-2034) | 18.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Spray Tank Capacity, (Small Capacity (Under 10L), Medium Capacity (10-30L), Large Capacity (30-60L), Ultra-Large Capacity (Over 60L)), By Crop Application, (Paddy Rice & Cereal Crops, Fruits & Vegetables, Oilseeds & Pulses, Plantation Crops, Turf & Specialty Applications), By AI Technology Feature, (Autonomous Flight & Obstacle Avoidance, AI Variable-Rate Spray Prescription Mapping, Computer Vision-Based Crop Health Assessment, AI Terrain-Following & Tilt Compensation, Multi-Drone Swarm Coordination), By Business Model, (Direct Hardware Sales, Drone-as-a-Service (DaaS), Hardware Plus Software Subscription, Government-Sponsored Agricultural Mechanization Programs) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | DJI (SZ DJI TECHNOLOGY), XAG CO. LTD., YAMAHA MOTOR CO., HYLIO INC., RANTIZO, IDEAFORGE TECHNOLOGY, KRAY TECHNOLOGIES, EFT (SHENZHEN EFT INTELLIGENT), AEROVIRONMENT, AVIANT, PYKA INC., DRONE DEPLOY (SOFTWARE PLATFORM), PRECISION HAWK, AGCO CORPORATION (FENDT AUTONOMY), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Crop Application (Paddy & Cereals, Fruits & Vegetables, Oilseeds & Pulses, Plantation Crops, Turf), By AI Technology Feature (Autonomous Flight, AI Mapping, Computer Vision, Terrain Following, Swarm Coordination) Industry Trends & Forecast 2026–2034")

, By Crop Application (Paddy & Cereals, Fruits & Vegetables, Oilseeds & Pulses, Plantation Crops, Turf), By AI Technology Feature (Autonomous Flight, AI Mapping, Computer Vision, Terrain Following, Swarm Coordination) Industry Trends & Forecast 2026–2034")

, By Crop Application (Paddy & Cereals, Fruits & Vegetables, Oilseeds & Pulses, Plantation Crops, Turf), By AI Technology Feature (Autonomous Flight, AI Mapping, Computer Vision, Terrain Following, Swarm Coordination) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI-Powered Agricultural Spraying Drone Market?

Global AI agricultural spraying drone market valued at USD 1.81B in 2024, reaching USD 9.86B by 2034, growing at a CAGR of 18.5% from 2026–2034.

Who are the major players in the AI-Powered Agricultural Spraying Drone Market?

DJI (SZ DJI TECHNOLOGY), XAG CO. LTD., YAMAHA MOTOR CO., HYLIO INC., RANTIZO, IDEAFORGE TECHNOLOGY, KRAY TECHNOLOGIES, EFT (SHENZHEN EFT INTELLIGENT), AEROVIRONMENT, AVIANT, PYKA INC., DRONE DEPLOY (SOFTWARE PLATFORM), PRECISION HAWK, AGCO CORPORATION (FENDT AUTONOMY), OTHERS

Which segments covered the AI-Powered Agricultural Spraying Drone Market?

By Spray Tank Capacity, (Small Capacity (Under 10L), Medium Capacity (10-30L), Large Capacity (30-60L), Ultra-Large Capacity (Over 60L)), By Crop Application, (Paddy Rice & Cereal Crops, Fruits & Vegetables, Oilseeds & Pulses, Plantation Crops, Turf & Specialty Applications), By AI Technology Feature, (Autonomous Flight & Obstacle Avoidance, AI Variable-Rate Spray Prescription Mapping, Computer Vision-Based Crop Health Assessment, AI Terrain-Following & Tilt Compensation, Multi-Drone Swarm Coordination), By Business Model, (Direct Hardware Sales, Drone-as-a-Service (DaaS), Hardware Plus Software Subscription, Government-Sponsored Agricultural Mechanization Programs)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI-Powered Agricultural Spraying Drone Market

Published Date : 20 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date