- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI Code Generation Tools Market Forecast 2034 | CAGR 21.5%

Global AI-Powered Code Generation Tools Market Size, Share, Growth & Industry Analysis By Offering (IDE-Integrated Coding Assistants, Standalone AI Code Editors, API & Platform Services, Automated Testing & Code Review Tools), By End-User (Enterprise Software Engineering Teams, Individual Developers, SMEs), By Deployment (Cloud-Hosted, Hybrid, On-Premise), By Capability Level (Code Completion, Agentic Coding, Code Review & Security, Natural Language-to-Code) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

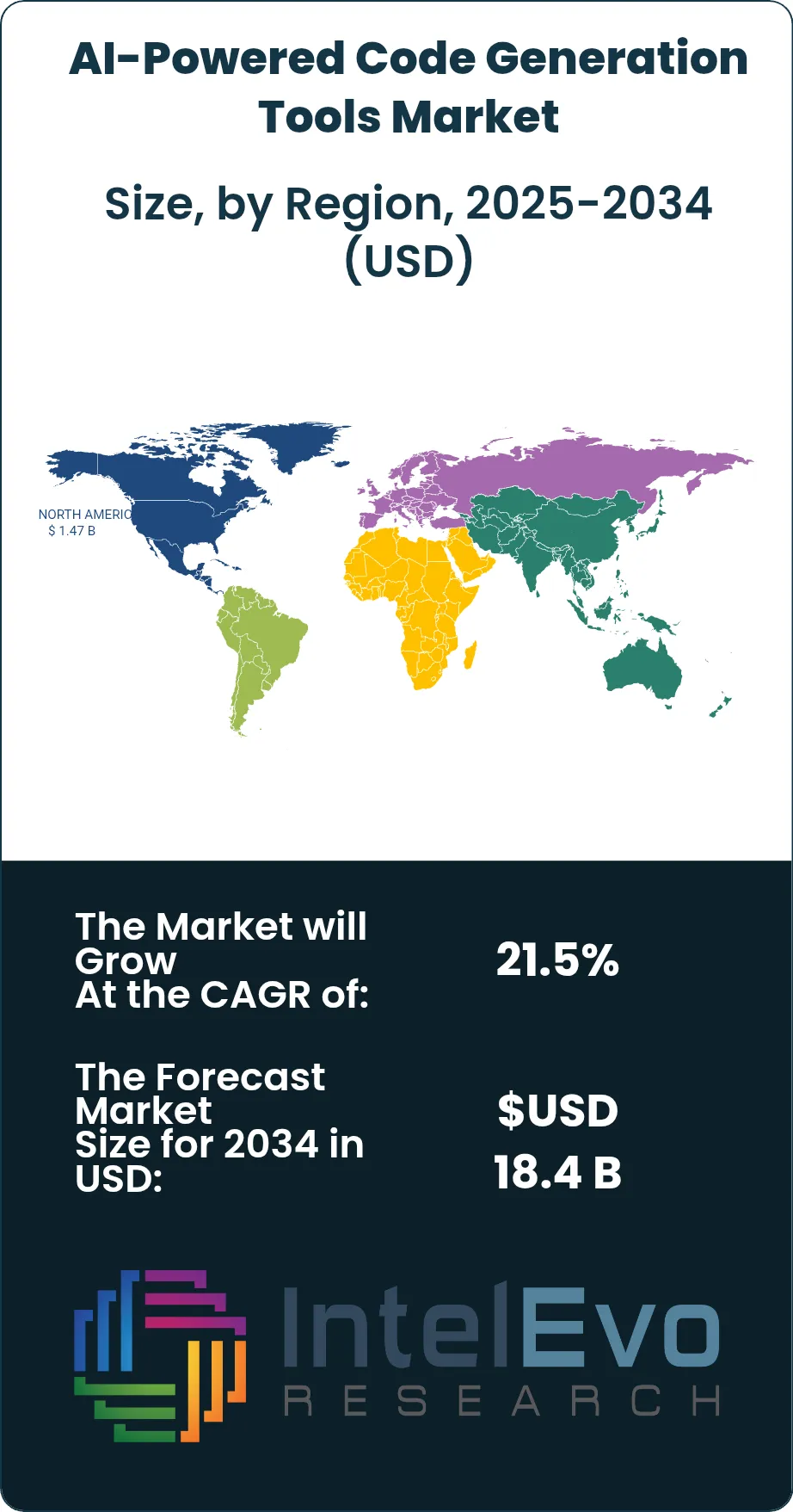

| USD 3.2 Billion | USD 18.4 Billion | 21.5% | North America, 46.0% |

The AI-Powered Code Generation Tools Market was valued at approximately USD 2.63 Billion in 2024 and reached USD 3.2 Billion in 2025. The market is projected to grow to USD 18.4 Billion by 2034, expanding at a CAGR of 21.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 15.2 billion over the analysis period. AI-powered code generation tools encompass IDE-integrated coding assistants, standalone AI code editors, automated testing generators, code review bots, natural-language-to-code translators, and full-project scaffolding platforms that use large language models to accelerate software development workflows.

Get More Information about this report -

Request Free Sample ReportDemand for AI-powered code generation tools is accelerating as software engineering organizations confront a persistent global developer shortage estimated at 4 million unfilled positions in 2025 by the US Bureau of Labor Statistics and Evans Data Corporation. GitHub Copilot, the market's most adopted product, surpassed 2.5 million paid subscribers by January 2025, with enterprise developers accepting 35% of AI-generated code suggestions and saving an estimated 90 minutes per day. The EU AI Act, entering phased enforcement from August 2025, introduced transparency requirements for AI systems generating software code used in high-risk applications, creating a compliance-driven segment for auditable code generation platforms.

Technology advances are reshaping the competitive structure. Transformer-based models fine-tuned on proprietary codebases now achieve 68% code completion accuracy on enterprise benchmarks, up from 42% in 2023. Multi-language support spanning Python, JavaScript, TypeScript, Java, Go, Rust, and C++ became standard in 2025. Agentic coding assistants capable of autonomous multi-file editing, debugging, and pull request management grew from 5% to 22% of enterprise licenses in 2025. Retrieval-augmented generation (RAG) architectures connecting code models to internal documentation and API references improved suggestion relevance by 40–50%.

Regional patterns show North America leading with 46.0% share in 2025, driven by Silicon Valley's concentration of tool developers and the world's largest enterprise software engineering workforce. Asia Pacific held 24.5%, powered by India's IT services sector and China's domestic code generation platforms. Europe accounted for 19.5%, shaped by AI Act compliance requirements and strong developer communities in Germany and the UK. Latin America contributed 5.5%, concentrated in Brazil's growing tech sector. The Middle East and Africa held 4.5%, led by UAE and Israel AI investments. Risk factors include intellectual property concerns over AI-generated code, model hallucination in complex logic, vendor lock-in, and open-source model competition eroding paid tool pricing. The AI-powered code generation tools market outlook remains strong as software development demand continues to outpace available human engineering capacity through 2034.

, By End-User (Enterprise Software Engineering Teams, Individual Developers, SMEs), By Deployment (Cloud-Hosted, Hybrid, On-Premise), By Capability Level (Code Completion, Agentic Coding, Code Review & Security, Natural Language-to-Code) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The AI-powered code generation tools market was valued at USD 3.2 billion in 2025 and is projected to reach USD 18.4 billion by 2034, registering a CAGR of 21.5% over the forecast period 2026–2034.

- Segment Dominance (By Offering): IDE-integrated coding assistants captured 54.0% of the market in 2025, valued at USD 1.73 billion, as developers adopted in-editor AI suggestions that required no workflow changes.

- Segment Dominance (By End-User): Enterprise software engineering teams accounted for 62.0% of market revenue in 2025, driven by large organizations deploying site-wide code generation licenses to address developer productivity targets.

- Driver: A global developer shortage of 4 million unfilled positions in 2025 compelled organizations to adopt AI code generation tools; enterprises using these tools reported 30–55% faster task completion across development workflows.

- Restraint: Intellectual property and code licensing concerns limited adoption; 29% of enterprises paused rollouts pending legal clarity on ownership of AI-generated code and potential open-source license contamination.

- Opportunity: Agentic coding platforms capable of autonomous multi-file editing, debugging, and deployment represent a USD 5.4 billion incremental opportunity through 2034 as organizations shift from code suggestion to full workflow automation.

- Trend: Agentic code generation grew from 5% to 22% of enterprise licenses in 2025, with tools like Cursor, Devin, and GitHub Copilot Workspace enabling autonomous project-level code modifications beyond single-line completions.

- Regional Analysis: North America led with 46.0% market share, generating USD 1.47 billion in 2025; GitHub Copilot's dominance, concentrated VC funding, and the largest enterprise developer workforce anchored regional demand.

Competitive Landscape Overview

The AI-powered code generation tools market is highly consolidated, with the top four providers collectively holding approximately 62% of global revenue in 2025. Competition is platform-driven, centering on model accuracy, IDE integration depth, enterprise security features, and multi-language support breadth. GitHub Copilot maintains a dominant installed base advantage through its integration with the world's largest developer platform. Startup challengers have gained share rapidly by offering standalone AI-native code editors with superior agentic capabilities. Venture capital investment in code generation startups exceeded USD 3.5 billion during 2024–2025, intensifying competitive pressure on incumbents.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| GitHub (Microsoft) | US | Leader | GitHub Copilot / Copilot Workspace | Global | Surpassed 2.5M paid subscribers; launched Copilot Workspace (Jan 2025) |

| Cursor (Anysphere) | US | Leader | Cursor AI Code Editor | North America | Raised USD 900M Series C at USD 9B valuation (Jan 2026) |

| Google (DeepMind) | US | Leader | Gemini Code Assist / AlphaCode | Global | Integrated Gemini Code Assist into Cloud Workstations (Mar 2025) |

| Amazon Web Services | US | Leader | Amazon Q Developer | Global | Rebranded CodeWhisperer to Q Developer with agentic features (Feb 2025) |

| Anthropic | US | Challenger | Claude Code (CLI) | North America | Launched Claude Code CLI for terminal-based agentic coding (Apr 2025) |

| Tabnine | Israel | Challenger | Tabnine Enterprise | Global | Released private-deployment model with zero data retention (Jun 2025) |

| Cognition AI | US | Challenger | Devin AI Software Engineer | North America | Raised USD 175M Series A; launched Devin autonomous agent (Dec 2024) |

| Sourcegraph | US | Challenger | Cody AI Assistant | North America | Expanded Cody enterprise with multi-repo context (Aug 2025) |

| Replit | US | Niche Player | Replit Agent / Ghostwriter | Global | Launched Replit Agent for full-app generation from prompts (Sep 2025) |

| IBM | US | Niche Player | IBM watsonx Code Assistant | North America | Deployed COBOL-to-Java migration assistant for 50+ banks (May 2025) |

By Offering:

IDE-integrated coding assistants dominated the market with a 54.0% share valued at USD 1.73 billion in 2025. These tools operate as extensions or plugins within existing development environments such as Visual Studio Code, JetBrains IntelliJ, and Neovim, providing inline code completions, function suggestions, and documentation generation without disrupting developer workflows. GitHub Copilot leads this segment with over 2.5 million paid subscribers. The low friction of IDE integration drives adoption; developers activate the tool through a single plugin installation with no workflow changes required. Standalone AI code editors held 24.0% share, generating USD 0.77 billion in 2025. This segment includes purpose-built editors like Cursor, Windsurf, and Replit that redesign the coding interface around AI-first principles. Standalone editors offer deeper agentic capabilities, including multi-file editing, terminal command execution, and autonomous debugging, that IDE plugins cannot easily replicate. Cursor's rapid growth to over 500,000 active users by mid-2025 validated this segment. API and platform services captured 14.0%, valued at USD 0.45 billion, providing enterprise developers with code generation model access through REST APIs for custom integration into internal toolchains and CI/CD pipelines. Automated testing and code review tools held 8.0%, worth USD 0.26 billion, using AI to generate unit tests, detect vulnerabilities, and review pull requests.

By End-User:

Enterprise software engineering teams commanded 62.0% of market revenue in 2025, generating USD 1.98 billion. Large organizations with over 500 developers deploy site-wide code generation licenses to address productivity targets, reduce time-to-market for software releases, and mitigate the impact of developer attrition. Enterprise buyers prioritize data security, with 78% requiring SOC 2 Type II compliance and private model deployment options. Average enterprise spending on code generation tools reached USD 420 per developer per year in 2025. Individual developers and freelancers held 22.0%, valued at USD 0.70 billion. This segment purchases individual subscriptions, typically priced at USD 10–20 per month, for personal productivity enhancement. GitHub Copilot Individual and Cursor Pro dominate this tier. SME development teams captured 16.0%, generating USD 0.51 billion. Small and mid-sized software companies adopt team-tier subscriptions that provide shared billing, usage analytics, and basic admin controls at lower per-seat costs than enterprise agreements.

By Deployment:

Cloud-hosted code generation dominated with 71.0% share, valued at USD 2.27 billion in 2025. Cloud deployment offers continuous model updates, zero infrastructure management, and elastic inference scaling. Most commercial tools, including GitHub Copilot, Cursor, and Amazon Q Developer, operate as cloud services with model inference running on provider-managed GPU clusters. Hybrid deployment held 19.0%, generating USD 0.61 billion. Enterprises in regulated industries such as finance, healthcare, and defense require hybrid architectures where code context stays on-premise while inference calls route through private endpoints. Tabnine Enterprise and IBM watsonx Code Assistant lead hybrid and private deployment options. On-premise deployment captured 10.0%, valued at USD 0.32 billion, serving defense contractors, intelligence agencies, and financial institutions operating in air-gapped environments using locally hosted open-source code models such as StarCoder, CodeLlama, and DeepSeek-Coder.

By Capability Level:

Code completion and suggestion tools led with 48.0% share, valued at USD 1.54 billion in 2025. These tools provide line-level and block-level code suggestions triggered by developer context, representing the foundational capability that drove initial market adoption. Accuracy rates on enterprise benchmarks reached 68% in 2025. Agentic coding platforms held 22.0%, generating USD 0.70 billion. Agentic tools autonomously perform multi-step development tasks: planning changes across multiple files, executing terminal commands, running tests, and iterating on errors without human intervention. Cursor Composer, GitHub Copilot Workspace, and Cognition's Devin define this segment. Code review and security analysis captured 16.0%, worth USD 0.51 billion, using AI to detect bugs, security vulnerabilities, and code quality issues in pull requests. Natural-language-to-code translation held 14.0%, valued at USD 0.45 billion, converting plain English specifications into functional code, particularly targeting non-technical users and product managers.

Regional Analysis

North America:

North America led the AI-powered code generation tools market with 46.0% share, generating USD 1.47 billion in 2025. The United States accounted for over 93% of regional revenue, driven by the headquarters concentration of all four market leaders (GitHub, Cursor, Google, AWS), the world's largest enterprise software engineering workforce at 4.4 million developers, and the highest per-developer tool spending globally. Silicon Valley venture capital invested over USD 3.5 billion in code generation startups during 2024–2025. The US federal government's Executive Order on AI Safety and NIST's Secure Software Development Framework (SSDF) encouraged the adoption of AI code review tools with vulnerability detection capabilities. Canada contributed through its AI research hubs in Toronto and Montreal, with Shopify and other tech companies deploying enterprise code generation at scale. Mexico's growing nearshore software development sector began integrating AI coding tools to improve productivity for US-facing clients.

Europe:

Europe held 19.5% of the global market, valued at USD 0.62 billion in 2025. The EU AI Act introduced transparency requirements for AI-generated code used in high-risk applications, creating a compliance-driven market segment for auditable code generation platforms. Germany led European demand through its automotive software and industrial IoT development sectors, where Siemens, Bosch, and SAP engineering teams adopted code generation tools at scale. The United Kingdom maintained strong adoption through London's fintech corridor and Cambridge's AI research cluster. France contributed through its startup community and Mistral AI's domestically developed code models. The Netherlands emerged as a testing ground for multilingual code generation serving pan-European development teams. European enterprises showed stronger preference for private-deployment options; 45% of regional buyers selected hybrid or on-premise code generation solutions compared to 22% globally, driven by GDPR data residency concerns around sending proprietary source code to US-hosted cloud inference endpoints.

Asia Pacific:

Asia Pacific captured 24.5% market share, generating USD 0.78 billion in 2025. India represented the largest country-level market in the region, with IT services giants Infosys, TCS, Wipro, and HCL deploying code generation tools across their global delivery centers to boost developer productivity by 25–35%. India's 5.8 million developer workforce makes it the second-largest developer population globally. China contributed through domestically developed code generation platforms from Baidu (Comate), Alibaba (Tongyi Lingma), and ByteDance, which serve Chinese enterprises under Cyberspace Administration regulations that restrict cross-border code model usage. Japan's NEC and Fujitsu deployed Japanese-language code assistants for enterprise software maintenance and legacy system modernization. South Korea's Samsung SDS and Kakao invested in code generation for semiconductor firmware and mobile application development. Australia allocated government funding for AI-assisted software development in public sector digital transformation projects.

Latin America:

Latin America accounted for 5.5% of the global market, generating USD 0.18 billion in 2025. Brazil dominated regional demand, with its 1.2 million developer workforce adopting code generation tools at rates approaching North American levels. Nubank, iFood, and other Brazilian tech firms deployed GitHub Copilot across their engineering organizations. Mexico contributed through its nearshore software development industry, where code generation tools improved the productivity of teams servicing US enterprise clients. Argentina's Buenos Aires tech community showed strong individual developer adoption, with Cursor and GitHub Copilot usage rates among the highest per capita in Latin America. Colombia invested in developer training programs that incorporated AI coding tools as part of government-backed tech workforce initiatives.

Middle East and Africa:

The Middle East and Africa region held 4.5% market share, valued at USD 0.14 billion in 2025. Israel contributed significantly through its AI startup sector; Tabnine, headquartered in Tel Aviv, is one of the market's leading enterprise code generation providers. Israeli defense and cybersecurity software firms adopted private-deployment code generation tools for classified development environments. The UAE invested in AI-powered software development through its national AI strategy, with government technology agencies deploying code assistants for smart city and e-government applications. Saudi Arabia's NEOM and Vision 2030 technology initiatives created demand for AI-assisted software development across construction, logistics, and public services. South Africa represented the largest sub-Saharan African market, with financial services and telecommunications developers piloting AI code generation. Limited local cloud infrastructure in parts of Africa constrains adoption, though hyperscaler data center expansions in Johannesburg and Cape Town are gradually reducing latency barriers.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- IDE-Integrated Coding Assistants

- Standalone AI Code Editors

- API and Platform Services

- Automated Testing and Code Review Tools

By End-User

- Enterprise Software Engineering Teams

- Individual Developers and Freelancers

- SME Development Teams

By Deployment

- Cloud-Hosted

- Hybrid

- On-Premise

By Capability Level

- Code Completion and Suggestion

- Agentic Coding Platforms

- Code Review and Security Analysis

- Natural-Language-to-Code Translation

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.2 B |

| Forecast Revenue (2034) | USD 18.4 B |

| CAGR (2025-2034) | 21.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (IDE-Integrated Coding Assistants, Standalone AI Code Editors, API and Platform Services, Automated Testing and Code Review Tools), By End-User, (Enterprise Software Engineering Teams, Individual Developers and Freelancers, SME Development Teams), By Deployment, Cloud-Hosted, Hybrid, On-Premise), By Capability Level, (Code Completion and Suggestion, Agentic Coding Platforms, Code Review and Security Analysis, Natural-Language-to-Code Translation), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | GITHUB (MICROSOFT), CURSOR (ANYSPHERE), GOOGLE (DEEPMIND), AMAZON WEB SERVICES (AWS), ANTHROPIC, TABNINE, COGNITION AI, SOURCEGRAPH, REPLIT, IBM (WATSONX), CODEIUM / WINDSURF, JETBRAINS, META (CODE LLAMA), HUGGING FACE (STARCODER), SNYK, DEEPSOURCE, MAGIC AI, POOLSIDE AI, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User (Enterprise Software Engineering Teams, Individual Developers, SMEs), By Deployment (Cloud-Hosted, Hybrid, On-Premise), By Capability Level (Code Completion, Agentic Coding, Code Review & Security, Natural Language-to-Code) Industry Trends & Forecast 2026–2034")

, By End-User (Enterprise Software Engineering Teams, Individual Developers, SMEs), By Deployment (Cloud-Hosted, Hybrid, On-Premise), By Capability Level (Code Completion, Agentic Coding, Code Review & Security, Natural Language-to-Code) Industry Trends & Forecast 2026–2034")

, By End-User (Enterprise Software Engineering Teams, Individual Developers, SMEs), By Deployment (Cloud-Hosted, Hybrid, On-Premise), By Capability Level (Code Completion, Agentic Coding, Code Review & Security, Natural Language-to-Code) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI-Powered Code Generation Tools Market?

Global AI code generation tools market valued at USD 2.63B in 2024, reaching USD 18.4B by 2034, growing at a CAGR of 21.5% from 2026–2034.

Who are the major players in the AI-Powered Code Generation Tools Market?

GITHUB (MICROSOFT), CURSOR (ANYSPHERE), GOOGLE (DEEPMIND), AMAZON WEB SERVICES (AWS), ANTHROPIC, TABNINE, COGNITION AI, SOURCEGRAPH, REPLIT, IBM (WATSONX), CODEIUM / WINDSURF, JETBRAINS, META (CODE LLAMA), HUGGING FACE (STARCODER), SNYK, DEEPSOURCE, MAGIC AI, POOLSIDE AI, Others

Which segments covered the AI-Powered Code Generation Tools Market?

By Offering, (IDE-Integrated Coding Assistants, Standalone AI Code Editors, API and Platform Services, Automated Testing and Code Review Tools), By End-User, (Enterprise Software Engineering Teams, Individual Developers and Freelancers, SME Development Teams), By Deployment, Cloud-Hosted, Hybrid, On-Premise), By Capability Level, (Code Completion and Suggestion, Agentic Coding Platforms, Code Review and Security Analysis, Natural-Language-to-Code Translation),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI-Powered Code Generation Tools Market

Published Date : 06 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date