- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI Drug Discovery Platform Market Forecast 2034 | CAGR 24.3%

Global AI-Powered Drug Discovery Platform Market Size, Share, Growth & Industry Analysis By Offering Type (SaaS-Based Platforms, Integrated Software & Proprietary Data Solutions, Professional Services & AI Model Customisation), By Therapeutic Area (Oncology, Neurology, Infectious Disease, Cardiovascular, Rare Genetic Disorders, Immunology), By Drug Modality (Small Molecule, Biologics, Peptides, Cell & Gene Therapy) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2025–2034) | Largest Region (2025) |

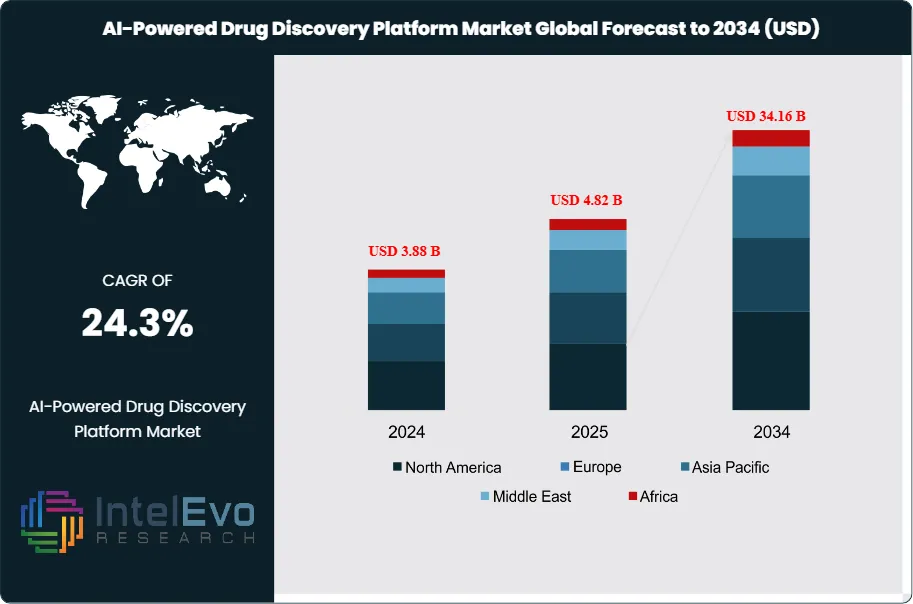

| USD 4.82 Billion | USD 34.16 Billion | 24.3% | North America, 52.3% |

The AI-Powered Drug Discovery Platform Market was valued at approximately USD 3.88 Billion in 2024 and reached USD 4.82 Billion in 2025. The market is projected to grow to USD 34.16 Billion by 2034, expanding at a CAGR of 24.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 29.34 Billion over the analysis period, reflecting the accelerating integration of artificial intelligence, machine learning, and generative chemistry into the pharmaceutical research and development value chain at every stage from target identification through preclinical candidate selection.

Get More Information about this report -

Request Free Sample ReportThe AI-powered drug discovery platform market encompasses software platforms, SaaS-deployed machine learning models, proprietary data assets, and integrated computational chemistry tools used by biopharmaceutical companies, academic research institutions, and contract research organisations to identify novel therapeutic targets, design and screen drug candidates, predict ADMET properties, and optimise lead molecules. The market operates at the intersection of computational biology, deep learning, and medicinal chemistry, with platform differentiation concentrated in three areas: the breadth and quality of proprietary biological and chemical training data, the accuracy of property prediction models across diverse chemical space, and the depth of workflow integration within pharma R&D informatics infrastructure. In 2025, AI-powered drug discovery platforms contributed to at least 18 clinical candidates entering Phase I trials, up from 3 in 2020, demonstrating measurable clinical translation of AI-generated molecules.

Regulatory influences on the AI-powered drug discovery platform market are materialising through two channels: FDA's Artificial Intelligence/Machine Learning (AI/ML)-Based Software as a Medical Device (SaMD) Action Plan and the agency's Drug Modernization Act provisions that encourage computational pre-clinical models to reduce animal testing. The FDA's Centre for Drug Evaluation and Research (CDER) engaged with 32 drug developers that used AI platforms in IND-enabling studies in 2025, signalling institutional acceptance of AI-generated molecular data in regulatory submissions. The EU's Innovative Health Initiative (IHI), committing EUR 2.4 Billion jointly with industry through 2027, includes AI drug discovery as a priority funding theme and is supporting academic-commercial platform development across seven member states.

North America dominated the AI-powered drug discovery platform market with a 52.3% share in 2025, anchored by the concentration of leading platform companies in the US, the largest pharma R&D spending base in the world at USD 108 Billion annually, and NIH funding directed at computational biology. Europe held a 21.4% share, with the UK, Switzerland, and Germany hosting the highest concentration of European AI drug discovery companies. Asia Pacific contributed 19.8%, with China investing aggressively in domestic AI drug discovery infrastructure and Insilico Medicine's clinical validation of the first AI-designed drug molecule reinforcing the region's competitive credibility. The pharma industry's median drug development cost of USD 2.3 Billion per approved drug and the 90% historical Phase II failure rate create the economic pressure that is converting AI platform adoption from optional to operationally necessary for competitive R&D productivity, sustaining the market's above-sector CAGR through 2034.

, By Therapeutic Area (Oncology, Neurology, Infectious Disease, Cardiovascular, Rare Genetic Disorders, Immunology), By Drug Modality (Small Molecule, Biologics, Peptides, Cell & Gene Therapy) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Global AI-Powered Drug Discovery Platform Market was valued at USD 4.82 Billion in 2025 and is forecast to reach USD 34.16 Billion by 2034, growing at a CAGR of 24.3% during the 2025–2034 forecast period.

- Segment Dominance: SaaS-based platform deployment held the largest offering-type share at 58.4% in 2025, generating USD 2.81 Billion, driven by pharma R&D organisations' preference for cloud-deployed AI tools that integrate with existing informatics infrastructure without capital-intensive on-premise installation.

- Segment Dominance: Oncology represented the leading therapeutic area application segment at 38.6% of platform revenue in 2025, generating USD 1.86 Billion, reflecting the highest AI platform contract density among cancer drug development programmes across Big Pharma and biotech.

- Driver: Pharma R&D productivity pressure, reflected in a 90% Phase II failure rate and an average USD 2.3 Billion cost per approved drug, is driving AI platform adoption, with 78% of top-50 global pharmaceutical companies having executed at least one AI drug discovery platform contract by 2025.

- Restraint: Data quality and availability constraints limit AI model accuracy for underrepresented target classes and rare disease indications, with an estimated 62% of AI-generated candidate failures in 2025 attributed to insufficient training data for the specific target or chemical series rather than model architecture deficiencies.

- Opportunity: Generative AI-based de novo molecular design represents an addressable market opportunity of USD 8.4 Billion by 2034, with at least 22 platforms incorporating large language model or diffusion model-based molecular generation as of 2025, covering a chemical design space estimated at 10^60 synthesisable small molecules.

- Trend: Integration of protein structure prediction tools, including AlphaFold3 and ESMFold, into commercial AI drug discovery platforms reached 74.2% of leading platform offerings in 2025, up from 18.6% in 2021, fundamentally changing the structure-based drug design workflow.

- Regional Analysis: North America led the global AI-powered drug discovery platform market with a 52.3% share in 2025, generating USD 2.52 Billion, anchored by the US pharma R&D spending base of USD 108 Billion annually and the concentration of six of the top eight AI drug discovery platform companies in the United States.

Competitive Landscape Overview

The AI-powered drug discovery platform market is moderately fragmented, with Schrödinger, Insilico Medicine, Recursion Pharmaceuticals, and BenevolentAI collectively holding approximately 46% of global platform revenue in 2025. Competition is primarily technology-driven, centred on training data depth, model validation against clinical outcomes, and platform integration breadth across the drug discovery workflow. Competitive intensity escalated sharply in 2025 and early 2026 as consolidation activity accelerated, with Recursion's USD 688 Million acquisition of Exscientia representing the largest AI drug discovery M&A transaction on record and signalling a move toward vertically integrated AI-biology-chemistry platforms over point-solution providers.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Schrödinger | USA | Leader | FEP+ / LiveDesign Platform | North America / Europe | Expanded AI-accelerated FEP+ to support RNA-targeted drug design; signed 5 new pharma partnership deals (Feb 2025) |

| Insilico Medicine | Hong Kong | Leader | Chemistry42 / Biology42 Platform | Asia Pacific / North America | INS018_055 (AI-designed IPF drug) entered Phase II in US and China; raised USD 110M Series D (Apr 2025) |

| Recursion Pharmaceuticals | USA | Leader | Recursion OS (phenomics + AI) | North America | Acquired Exscientia for USD 688M to combine phenomics with generative chemistry; Nvidia partnership expanded (Jan 2026) |

| BenevolentAI | UK | Challenger | BenevolentAI Platform (KG + ML) | Europe / North America | Pivoted to SaaS licensing model after AZ lead candidate discontinuation; signed 3 Big Pharma platform contracts (Sep 2025) |

| Atomwise | USA | Challenger | AtomNet deep learning platform | North America | Completed 1,800th virtual screen for partner pharma companies; raised USD 45M Series C extension (Jun 2025) |

| Exscientia (acquired) | UK | Challenger | Centaur Chemist generative AI | Europe | Acquisition by Recursion closed Jan 2026; Centaur Chemist platform integrated into Recursion OS pipeline. |

| XtalPi | China | Niche Player | Intelligent Digital Drug Discovery (ID4) | Asia Pacific | Secured USD 200M Series D; expanded US operations with new Cambridge MA office (Mar 2025) |

| Relay Therapeutics | USA | Niche Player | Dynamo platform (protein motion AI) | North America | Disclosed RLY-2608 Phase II data in PIK3CA-mutant breast cancer showing 54% ORR (Aug 2025) |

By Offering Type

SaaS-based platform deployment represented the largest offering-type segment of the AI-powered drug discovery platform market at 58.4% share and USD 2.81 Billion in 2025. Cloud-deployed AI drug discovery platforms provide pharmaceutical R&D teams with on-demand access to computational chemistry workflows, machine learning model libraries, and biological knowledge graph query tools without requiring in-house HPC infrastructure investment. The median annual SaaS contract value across the top 10 AI drug discovery platform providers was USD 1.4 Million per pharma client in 2025, with enterprise-tier agreements at top-20 global pharma companies averaging USD 6.2 Million annually. SaaS platform adoption is accelerating as pharma IT functions standardise on cloud-native R&D informatics, enabling AI platforms to integrate with existing ELN (Electronic Lab Notebook), LIMS, and compound management systems via API. The SaaS segment is projected to grow at 25.8% CAGR through 2034, outpacing the overall market as platform-as-a-service models expand from target identification and lead optimisation to include clinical biomarker prediction and patient stratification modules.

Integrated software and data solutions, combining proprietary biological databases with machine learning models sold through multi-year enterprise licence agreements, held a 28.6% share in 2025, generating USD 1.38 Billion. Schrödinger's LiveDesign platform and Insilico Medicine's integrated Biology42-Chemistry42 suite represent the leading examples of this model, where the platform's value is inseparable from the proprietary molecular simulation data or bioactivity datasets embedded in the product. This offering type commands higher contract values than pure SaaS tools, with average enterprise licence agreements reaching USD 8.5 Million to USD 12 Million per year at leading providers. Professional services, including AI model customisation, data curation, and computational chemistry consulting, accounted for the remaining 13.0% of market revenue at USD 0.63 Billion in 2025, a segment growing modestly as pharma organisations build in-house AI capabilities and reduce third-party services dependency.

By Therapeutic Area

Oncology accounted for 38.6% of AI-powered drug discovery platform revenue by therapeutic area in 2025, generating USD 1.86 Billion. The concentration of oncology applications reflects the therapeutic area's highest AI platform contract density, driven by the commercial incentive of the global oncology drug market exceeding USD 280 Billion annually, the availability of large genomic and proteomic training datasets from The Cancer Genome Atlas (TCGA), and the structural diversity of oncology targets including kinases, GPCRs, nuclear receptors, and protein-protein interaction surfaces that reward AI-based polypharmacology modelling. Relay Therapeutics' Dynamo platform and Schrödinger's FEP+ suite are the most frequently contracted AI platforms in oncology drug design as of 2025. Neurology and central nervous system disorders held a 18.4% share in 2025, the second-largest therapeutic area segment, driven by the historically low CNS drug approval success rate of 6.2% that creates the strongest economic incentive for AI-assisted candidate selection. Infectious disease, cardiovascular disease, and rare genetic disorders each held 12% to 14% shares, with the rare disease segment growing fastest at an estimated 28.4% CAGR through 2034 as AI platforms address the limited patient data challenge through federated learning and synthetic data augmentation approaches. Immunology and inflammation applications accounted for the remaining 9.0% of market revenue.

By Drug Modality

Small molecule drug discovery applications dominated the AI-powered drug discovery platform market by drug modality at a 61.2% share in 2025, generating USD 2.95 Billion. AI platforms for small molecule discovery cover the full workflow from target identification and virtual screening through ADMET prediction, lead optimisation, and synthetic route design, representing the most mature application of AI in pharmaceutical R&D with the longest validation history. Molecular dynamics simulation, free energy perturbation (FEP), and generative chemistry tools are standard components of small molecule AI platforms and are used by all major global pharmaceutical companies in their chemistry-driven pipeline programmes. Biologic and large molecule discovery applications held a 22.4% share in 2025, driven by antibody sequence design tools, protein engineering platforms, and ADC linker-payload optimisation models that leverage structural deep learning to design superior therapeutic biologics. Peptide and oligonucleotide drug design platforms contributed 10.8%, growing rapidly as interest in GLP-1 agonist analogues, siRNA, and antisense oligonucleotide discovery accelerates demand for AI-assisted sequence and secondary structure optimisation tools. Cell and gene therapy target identification platforms held the remaining 5.6%, a nascent segment expanding as CRISPR and CAR-T developers integrate AI-based guide RNA design, off-target prediction, and patient biomarker stratification into their discovery workflows.

Regional Analysis

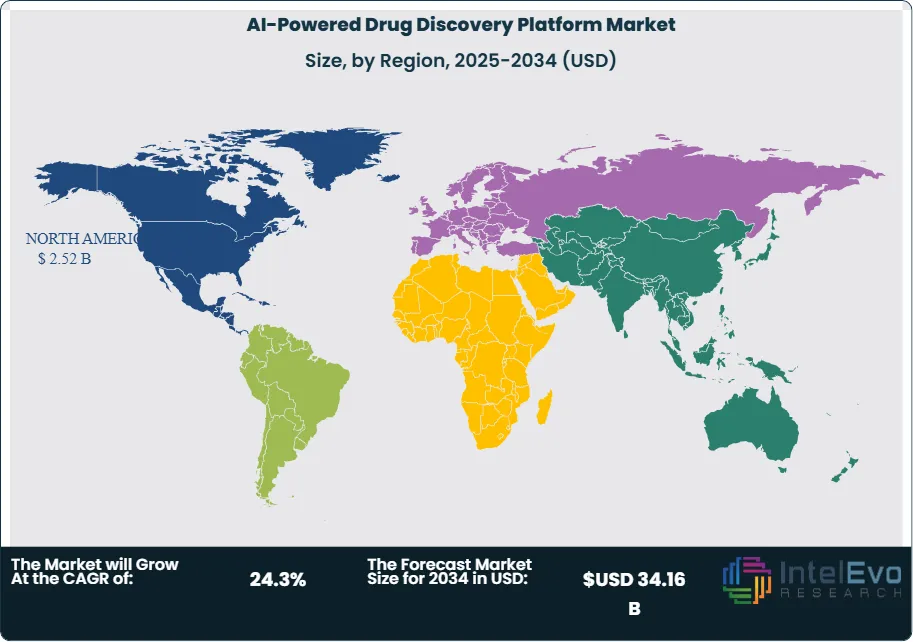

| Region | Share (2025) | Revenue (USD B) | Key Countries |

| North America | 52.3% | 2.52 | United States, Canada |

| Europe | 21.4% | 1.03 | UK, Germany, Switzerland, Sweden |

| Asia Pacific | 19.8% | 0.95 | China, Japan, South Korea, India |

| Latin America | 3.8% | 0.18 | Brazil, Mexico, Argentina |

| Middle East & Africa | 2.7% | 0.13 | Israel, UAE, South Africa |

North America

North America led the global AI-powered drug discovery platform market with a 52.3% share and USD 2.52 Billion in revenue in 2025. The United States accounts for approximately 94% of regional revenue, anchored by the world's largest pharmaceutical R&D spending base at USD 108 Billion annually, the highest concentration of AI drug discovery platform companies globally, and NIH funding that directed USD 1.8 Billion toward computational biology and AI-assisted drug development between 2022 and 2025. Six of the eight leading global AI drug discovery platform companies are headquartered in the US: Schrödinger, Recursion Pharmaceuticals, Atomwise, Relay Therapeutics, Roivant Sciences, and Insitro. Big Pharma US operations, including Pfizer's Worldwide Research and Development division, Merck's Quantitative Sciences group, and AbbVie's Genomics and Informatics Centre, each maintained USD 40 Million to USD 120 Million annual AI platform and computational drug discovery budgets in 2025. The FDA's constructive engagement with AI-generated IND data, reflected in 32 formal AI-related CDER interactions in 2025, reduces regulatory risk for US-based platform adopters and accelerates commercial uptake. Canada contributed approximately 6% of North American revenue through the University of Toronto's computational biology programmes and emerging AI drug discovery companies including Cyclica (acquired by Recursion in 2023) and Valence Labs.

Europe

Europe held a 21.4% share of the AI-powered drug discovery platform market in 2025, generating USD 1.03 Billion. The UK anchors European market activity as the headquarters of BenevolentAI, Exscientia (now Recursion), and Healx, and as the host of the Alan Turing Institute's drug discovery AI programme. AstraZeneca's Cambridge AI hub, Novo Nordisk's UK computational chemistry centre, and GlaxoSmithKline's AI/ML research group collectively represent an estimated USD 280 Million in annual AI platform procurement within the UK alone. Germany hosted Bayer AG's comprehensive AI drug discovery investment of USD 220 Million committed through 2027, focusing on cardiovascular and oncology target identification. Switzerland's Roche and Novartis both operate large-scale proprietary AI drug discovery platforms built on internal data assets complemented by third-party platform licensing. The EU's Innovative Health Initiative (IHI) provides EUR 2.4 Billion in joint public-private funding through 2027, with AI drug discovery explicitly listed as a priority investment category, directly supporting platform development at European academic-commercial consortia. Sweden, home to AstraZeneca's Discovery Sciences leadership, contributed approximately 8% of European regional revenue in 2025.

Asia Pacific

Asia Pacific held a 19.8% share of the AI-powered drug discovery platform market in 2025, generating USD 0.95 Billion, with China representing approximately 52% of regional revenue. China's domestic AI drug discovery industry is led by Insilico Medicine, XtalPi, Alchemab, and DP Technology (Hermite platform), all of which have secured USD 50 Million or more in venture capital and are advancing AI-designed clinical candidates through Chinese NMPA clinical trial applications. China's government policy explicitly supports AI pharmaceutical development through the National New Drug Major Project, which committed RMB 12 Billion (approximately USD 1.65 Billion) to biomedical AI through 2025. Insilico Medicine's INS018_055, an AI-designed anti-fibrotic drug for idiopathic pulmonary fibrosis generated entirely by the Chemistry42 generative chemistry platform, entered Phase II clinical trials in both the US and China in 2025, representing the most clinically advanced AI-originated drug molecule globally. Japan contributed approximately 24% of Asia Pacific revenue through Takeda Pharmaceutical's USD 300 Million AI drug discovery investment and Astellas Pharma's proprietary ML-based ADMET prediction platform. South Korea and India each contributed approximately 12% of regional revenue through CRO service organisations integrating AI drug discovery tools into outsourced lead optimisation services.

Latin America

Latin America held a 3.8% share of the AI-powered drug discovery platform market in 2025, generating USD 0.18 Billion. Brazil represents the largest national market within the region at approximately 54% of regional revenue, driven by FIOCRUZ's computational drug discovery capabilities, the University of Sao Paulo's large-scale cheminformatics infrastructure, and a growing number of early-stage AI drug discovery startups including Ayana Bio and BiomeHub targeting tropical infectious disease indications with limited global pharma attention. The Brazilian health technology assessment body CONITEC has begun accepting computational pre-clinical ADMET data in drug registration dossiers as of 2024, creating regulatory pull for AI platform adoption among domestic generic and specialty pharma companies. Mexico contributed approximately 24% of Latin American revenue through multinational pharma R&D satellite offices in Monterrey and the Tecnologico de Monterrey computational drug discovery programme, which trained over 400 computational chemists between 2022 and 2025. Argentina's platform market is smaller but growing at an above-regional rate, supported by the Argentine Computational Biology Network coordinating academic AI drug discovery research.

Middle East & Africa

The Middle East & Africa region held a 2.7% share of the AI-powered drug discovery platform market in 2025, generating USD 0.13 Billion. Israel dominated regional activity with approximately 46% of MEA market revenue, supported by Weizmann Institute's computational drug design programmes and Israeli AI drug discovery companies including BioStrategies and Pepticom, which applies AI to peptide therapeutics design. The UAE's investment in AI health infrastructure through the Abu Dhabi Investment Office (ADIO) attracted USD 870 Million in life sciences AI commitments between 2022 and 2025, with Insilico Medicine and XtalPi both establishing UAE operations to serve Gulf market pharma R&D. Saudi Arabia's Vision 2030 health sector digitalisation programme allocated USD 320 Million to AI in pharmaceutical research through the Saudi Commission for Health Specialties. South Africa's Council for Scientific and Industrial Research (CSIR) operates computational drug discovery infrastructure targeting endemic diseases including tuberculosis, malaria, and HIV, utilising open-source and commercially licensed AI platforms. The MEA region is projected to grow at 26.8% CAGR through 2034, the highest regional growth rate, as government AI investment and multinational platform expansion converge.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering Type

- SaaS-Based Platform Deployment

- Integrated Software & Proprietary Data Solutions

- Professional Services & AI Model Customisation

By Therapeutic Area

- Oncology

- Neurology & Central Nervous System

- Infectious Disease

- Cardiovascular Disease

- Rare Genetic Disorders

- Immunology & Inflammation

By Drug Modality

- Small Molecule Drug Discovery

- Biologic & Large Molecule Discovery

- Peptide & Oligonucleotide Drug Design

- Cell & Gene Therapy Target Identification

By End-User

- Large Pharmaceutical Companies

- Biotech & Specialty Pharma Companies

- Contract Research Organisations (CROs)

- Academic & Government Research Institutions

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.82 B |

| Forecast Revenue (2034) | USD 34.16 B |

| CAGR (2025-2034) | 24.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering Type, (SaaS-Based Platform Deployment, Integrated Software & Proprietary Data Solutions, Professional Services & AI Model Customisation), By Therapeutic Area, (Oncology, Neurology & Central Nervous System, Infectious Disease, Cardiovascular Disease, Rare Genetic Disorders, Immunology & Inflammation), By Drug Modality, (Small Molecule Drug Discovery, Biologic & Large Molecule Discovery, Peptide & Oligonucleotide Drug Design, Cell & Gene Therapy Target Identification), By End-User, (Large Pharmaceutical Companies, Biotech & Specialty Pharma Companies, Contract Research Organisations (CROs), Academic & Government Research Institutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SCHRÖDINGER, INSILICO MEDICINE, RECURSION PHARMACEUTICALS, BENEVOLENTAI, ATOMWISE, RELAY THERAPEUTICS, XTALPI, EXSCIENTIA (RECURSION), INSITRO, ABSCI CORPORATION, DEEP GENOMICS, IKTOS, ENTOS, ALCHEMAB, DP TECHNOLOGY (HERMITE), PEPTICOM, CYCLICA (RECURSION), VALO HEALTH, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Therapeutic Area (Oncology, Neurology, Infectious Disease, Cardiovascular, Rare Genetic Disorders, Immunology), By Drug Modality (Small Molecule, Biologics, Peptides, Cell & Gene Therapy) Industry Trends & Forecast 2026–2034")

, By Therapeutic Area (Oncology, Neurology, Infectious Disease, Cardiovascular, Rare Genetic Disorders, Immunology), By Drug Modality (Small Molecule, Biologics, Peptides, Cell & Gene Therapy) Industry Trends & Forecast 2026–2034")

, By Therapeutic Area (Oncology, Neurology, Infectious Disease, Cardiovascular, Rare Genetic Disorders, Immunology), By Drug Modality (Small Molecule, Biologics, Peptides, Cell & Gene Therapy) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI-Powered Drug Discovery Platform Market?

Global AI-powered drug discovery market valued at USD 3.88B in 2024, reaching USD 34.16B by 2034, growing at a CAGR of 24.3% from 2026–2034.

Who are the major players in the AI-Powered Drug Discovery Platform Market?

SCHRÖDINGER, INSILICO MEDICINE, RECURSION PHARMACEUTICALS, BENEVOLENTAI, ATOMWISE, RELAY THERAPEUTICS, XTALPI, EXSCIENTIA (RECURSION), INSITRO, ABSCI CORPORATION, DEEP GENOMICS, IKTOS, ENTOS, ALCHEMAB, DP TECHNOLOGY (HERMITE), PEPTICOM, CYCLICA (RECURSION), VALO HEALTH, OTHERS

Which segments covered the AI-Powered Drug Discovery Platform Market?

By Offering Type, (SaaS-Based Platform Deployment, Integrated Software & Proprietary Data Solutions, Professional Services & AI Model Customisation), By Therapeutic Area, (Oncology, Neurology & Central Nervous System, Infectious Disease, Cardiovascular Disease, Rare Genetic Disorders, Immunology & Inflammation), By Drug Modality, (Small Molecule Drug Discovery, Biologic & Large Molecule Discovery, Peptide & Oligonucleotide Drug Design, Cell & Gene Therapy Target Identification), By End-User, (Large Pharmaceutical Companies, Biotech & Specialty Pharma Companies, Contract Research Organisations (CROs), Academic & Government Research Institutions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI-Powered Drug Discovery Platform Market

Published Date : 15 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date