- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI-Powered Medical Coding Market Size, Share | CAGR 20.5%

Global AI-Powered Medical Coding Market Size, Share, Growth Analysis By Offering (Software Solutions, Services, Platform Infrastructure), By Coding Type (Inpatient Coding, Outpatient Coding, Professional Services Coding, Risk Adjustment/HCC Coding), By End-User (Hospitals, Physician Practices, Billing Organizations, Payers), By Deployment Mode (Cloud, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

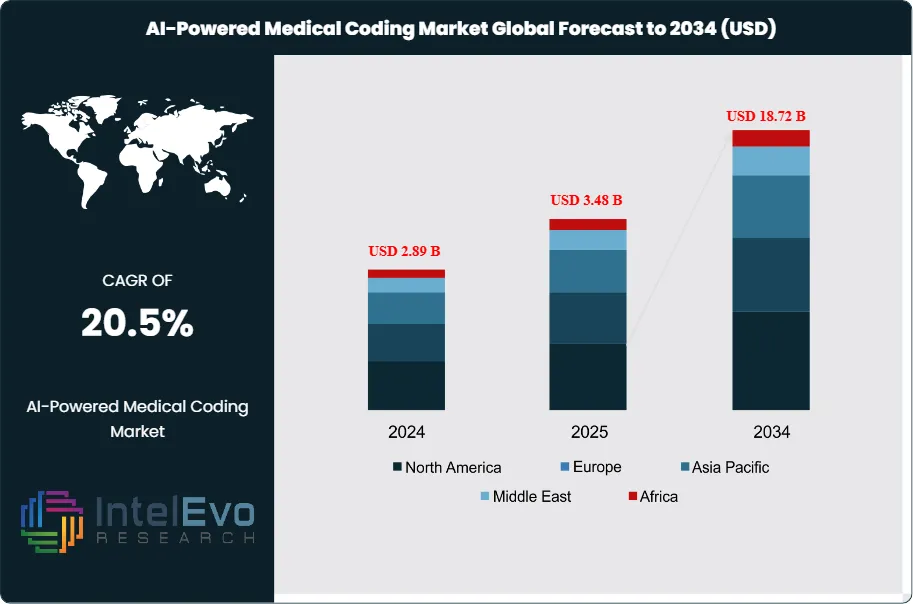

| USD 3.48 Billion | USD 18.72 Billion | 20.5% | North America, 48.6% |

The AI-Powered Medical Coding Market was valued at approximately USD 2.89 Billion in 2024 and reached USD 3.48 Billion in 2025. The market is projected to grow to USD 18.72 Billion by 2034, expanding at a CAGR of 20.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 15.24 Billion over the analysis period, driven by systemic pressure on revenue cycle operations, widening coder shortages, and the commercial maturation of large language models capable of parsing unstructured clinical documentation at production-grade accuracy.

Get More Information about this report -

Request Free Sample ReportAI-powered medical coding applies natural language processing, machine learning, and increasingly large language model architectures to convert physician notes, discharge summaries, operative reports, and ancillary clinical documentation into standardized code sets including ICD-10-CM, ICD-10-PCS, CPT, HCPCS Level II, and DRG classifications. The technology operates across a spectrum from computer-assisted coding that augments human coders to fully autonomous coding that processes specific encounter types without human intervention. Autonomous coding currently concentrates in well-structured specialties including radiology, pathology, emergency department, and ambulatory surgery, where documentation patterns are repetitive and coding logic is rules-convertible.

Demand drivers are structurally compelling. The American Health Information Management Association estimates a shortage of over 30,000 trained medical coders in the United States alone, while coder training timelines of 12 to 24 months cannot match the accelerating volume of clinical encounters. Health systems face documentation volume growth of 8% to 12% annually tied to value-based care reporting, hierarchical condition category capture, and risk adjustment requirements under Medicare Advantage and Accountable Care Organization contracts. AI coding addresses this supply-demand imbalance while simultaneously reducing days-in-accounts-receivable, denial rates, and per-chart coding costs that typically range from USD 3 to USD 12 depending on complexity.

Regulatory tailwinds reinforce the commercial case. The Centers for Medicare and Medicaid Services has clarified that AI-generated code submissions are acceptable provided the submitting organization retains responsibility for accuracy, a framework that validates enterprise deployment. The Office of Inspector General has increased audit scrutiny on coding accuracy in risk-adjusted payment programs, creating compliance-driven demand for auditable AI systems that generate evidence trails behind each code assignment. Europe has seen parallel adoption under digital health strategies in Germany, France, and the United Kingdom, while Asia Pacific markets led by India and the Philippines are emerging as both technology development hubs and high-volume deployment markets.

Investment activity underscores the thesis. Venture capital deployment into revenue cycle AI exceeded USD 1.5 Billion between 2023 and 2025, with multiple pure-play coding automation companies raising rounds at valuations above USD 1 Billion. Large revenue cycle management vendors have executed strategic acquisitions to secure AI coding capabilities, while electronic health record vendors are embedding autonomous coding natively into their platforms. The convergence of generative AI capability, health system financial pressure, and regulatory clarity positions the AI-powered medical coding market as one of the highest-growth healthcare IT categories through 2034.

, By Coding Type (Inpatient Coding, Outpatient Coding, Professional Services Coding, Risk Adjustment/HCC Coding), By End-User (Hospitals, Physician Practices, Billing Organizations, Payers), By Deployment Mode (Cloud, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global AI-powered medical coding market was valued at USD 3.48 Billion in 2025 and is projected to reach USD 18.72 Billion by 2034, growing at a CAGR of 20.5% during the forecast period 2026–2034.

- Segment Dominance: By offering, software solutions hold the dominant share at approximately 64.2% of market revenue in 2025, driven by enterprise subscription licensing of NLP and large language model coding platforms across hospital and physician group accounts.

- Segment Dominance: By application, inpatient coding represents the largest application share at approximately 44.8% of market revenue in 2025, reflecting the high coding complexity, MS-DRG revenue sensitivity, and audit exposure inherent in hospital inpatient encounters.

- Driver: A structural shortage of over 30,000 certified medical coders in the United States combined with annual clinical documentation volume growth of 8% to 12% is compelling health systems to adopt AI coding automation to maintain revenue cycle throughput and compliance accuracy.

- Restraint: Coding accuracy and audit defensibility concerns, particularly for complex inpatient and risk-adjustment encounters, limit full autonomous coding adoption to approximately 18% of enterprise deployments in 2025, with most implementations operating in computer-assisted coding mode under human coder oversight.

- Opportunity: Risk adjustment coding for Medicare Advantage and ACA marketplace plans represents an addressable opportunity exceeding USD 2.6 Billion by 2034, as payers and provider organizations adopt AI-driven HCC capture to optimize risk-adjusted revenue under value-based care contracts.

- Trend: Large language model architectures have replaced legacy rules-based and narrow NLP systems in approximately 42% of new enterprise deployments in 2025, up from near-zero penetration in 2022, fundamentally reshaping vendor competition toward model quality and fine-tuning capability.

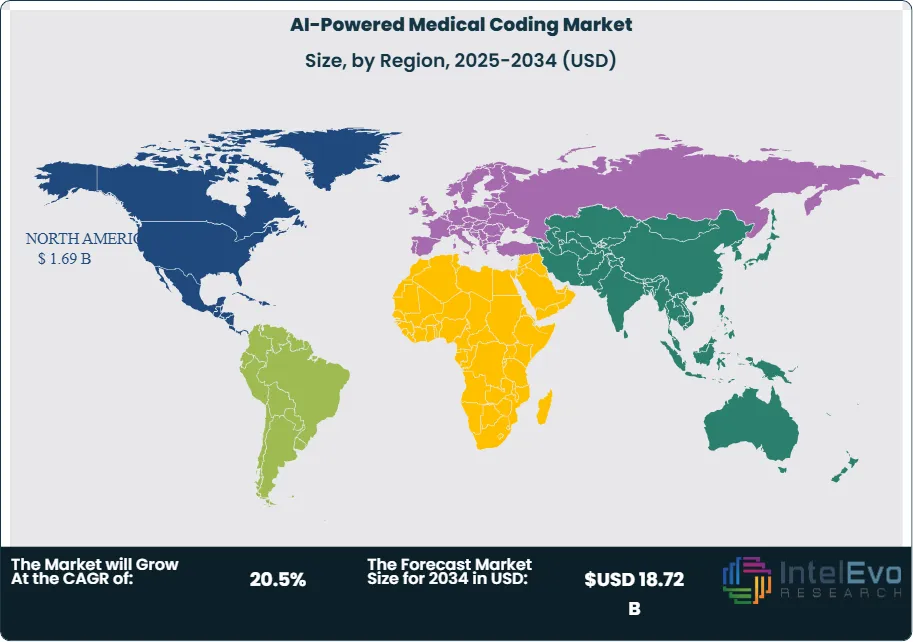

- Regional Analysis: North America holds the largest regional share at 48.6%, equivalent to approximately USD 1.69 Billion in 2025, supported by the complexity of US reimbursement coding, concentrated health system buyers, and the regulatory clarity enabling enterprise AI deployment.

Competitive Landscape Overview

The global AI-powered medical coding market is moderately fragmented, with the top four companies collectively accounting for approximately 41% of revenue in 2025. Competition is technology-driven, centered on model accuracy, specialty coverage breadth, EHR integration depth, and compliance audit capabilities. The market has witnessed significant acquisition activity between 2023 and 2025 as large revenue cycle management vendors and EHR platforms moved to secure AI coding capabilities. Well-funded pure-play autonomous coding vendors have entered the market aggressively, applying pricing and model performance pressure on incumbents. Partnership activity between AI coding firms and large health system customers is creating reference accounts that shape buyer evaluation criteria across the category.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| 3M Health Information Systems (Solventum) | USA | Leader | 3M 360 Encompass / CodeFinder | North America | Solventum spun off from 3M completed integration of generative AI coding assistant into 360 Encompass; expanded autonomous coding to emergency department encounters (2025) |

| Optum (UnitedHealth Group) | USA | Leader | Optum CAC / Optum Autonomous Coding | North America | Launched LLM-based autonomous coding platform covering radiology and pathology specialties; signed enterprise agreements with four top-20 US health systems (Mar 2025) |

| Nuance (Microsoft) | USA | Leader | DAX Copilot with Coding Intelligence | North America / Europe | Integrated autonomous coding module into DAX Copilot clinical documentation platform; launched joint Microsoft Cloud for Healthcare offering (Jan 2025) |

| Oracle Health (Cerner) | USA | Leader | Oracle Health Clinical AI Agent | North America / Global | Announced native embedding of AI coding capabilities into Oracle Health EHR; launched at customers on Oracle Cloud Infrastructure (2025) |

| Fathom | USA | Challenger | Fathom Autonomous Coding Platform | North America | Raised USD 80 Million Series E; expanded specialty coverage to include inpatient and primary care risk adjustment (2025) |

| CodaMetrix | USA | Challenger | CMX Automate | North America | Secured USD 55 Million Series B; signed multi-year autonomous coding agreement with Mass General Brigham expansion (Q2 2025) |

| AGS Health | India / USA | Niche Player | AGS AI-Powered Medical Coding | North America / Asia Pacific | Launched generative AI coding copilot for offshore coding operations; expanded Philippines delivery center by 40% (2025) |

| Maverick Medical AI | Israel / USA | Niche Player | Maverick Autonomous Coding | North America | Secured FDA-cleared clinical intelligence platform integration; expanded radiology autonomous coding deployments (Dec 2024) |

By Offering

The AI-powered medical coding market by offering is segmented into software solutions, services, and platform infrastructure. Software solutions held the dominant share at approximately 64.2% of market revenue in 2025, equivalent to roughly USD 2.23 Billion. This segment includes computer-assisted coding applications, autonomous coding engines, natural language processing platforms, and large language model fine-tuned coding copilots delivered as enterprise software subscriptions. Revenue is driven by per-chart, per-encounter, or enterprise-license pricing models that scale with health system coding volume. Leading software platforms have embedded ICD-10-CM, ICD-10-PCS, CPT, HCPCS, and DRG logic alongside clinical documentation improvement modules that prompt physicians for specificity needed to support appropriate code assignment. Subscription and consumption-based pricing models have supplanted perpetual licenses, creating the recurring revenue characteristics that attract strategic and financial buyers to the category.

Services constitute approximately 28.1% of market revenue in 2025, valued at roughly USD 978 Million. This segment includes implementation consulting, AI model customization, compliance audit support, coder training, and managed coding services delivered by AI-augmented offshore operations. Managed coding services represent the largest services sub-segment, as health systems increasingly contract with external vendors that combine AI coding automation with human coder review in a hybrid delivery model that reduces per-chart costs by 35% to 55% compared to in-house coding operations. India and Philippines-based operators have been particularly aggressive in layering generative AI capability into their services delivery to preserve margin as autonomous coding reduces human coder time per chart.

Platform infrastructure, including the underlying NLP engines, healthcare-specific foundation models, and cloud deployment environments, represents approximately 7.7% of market revenue in 2025 at USD 268 Million. This segment is emerging as an enterprise build-vs-buy question where large health systems and health plans license foundational coding AI infrastructure to develop custom internal applications rather than consuming packaged software. Foundation model infrastructure pricing is tied to API consumption, inference volumes, and fine-tuning compute costs, creating a volumetric revenue model that scales non-linearly with user activity. The platform segment is growing at a rate above the overall market as large enterprise accounts move from vendor-packaged applications to build-with-partner development models.

By Coding Type

Inpatient coding represents the largest application segment at approximately 44.8% of market revenue in 2025, valued at USD 1.56 Billion. Inpatient encounters command the highest per-chart AI coding revenue due to clinical complexity, MS-DRG revenue sensitivity, and the concentration of highest-risk audit exposure in hospital admissions. A single coding error on an inpatient chart can shift DRG assignment by thousands of dollars in reimbursement, making accuracy critical and justifying premium AI software pricing. Risk adjustment capture embedded within inpatient coding, particularly for Medicare Advantage enrollees, adds incremental revenue per chart as HCC identification drives risk-adjusted payment updates.

Outpatient coding accounts for approximately 29.5% of market revenue in 2025 at USD 1.03 Billion. The outpatient category covers ambulatory surgery, hospital outpatient visits, and observation stays, where CPT and HCPCS coding predominate. Outpatient coding volumes are 8x to 12x higher than inpatient volumes in most health systems, making per-chart coding cost pressure acute. AI automation in this segment delivers high-volume operational leverage, even though per-chart revenue is lower than inpatient. Autonomous coding penetration is highest in structured outpatient specialties including radiology, laboratory, and ambulatory surgery.

Professional services coding, which covers physician billing in all encounter settings, represents approximately 16.7% of market revenue in 2025 at USD 581 Million. Pro-fee coding is the highest-volume and lowest per-chart margin segment, making it particularly amenable to high-throughput AI automation. Risk adjustment and HCC-specific coding represent the remaining approximately 9.0% of market revenue at USD 313 Million in 2025, though this sub-segment is the fastest-growing within the coding type taxonomy as Medicare Advantage enrollment and ACA marketplace risk adjustment payments drive payer and provider demand for specialized HCC capture AI.

By End-User

Hospitals and health systems represent the largest end-user segment at approximately 52.6% of market revenue in 2025, valued at USD 1.83 Billion. Large integrated health systems are the most sophisticated buyers, typically deploying AI coding across inpatient, outpatient, and professional fee operations simultaneously under enterprise contracts that can exceed USD 5 Million annually for the largest customers. Adoption is deepening as systems move from computer-assisted coding in a minority of specialties to autonomous coding across progressively more encounter types, driving revenue expansion within existing accounts rather than purely new logo acquisition.

Physician practices and ambulatory groups account for approximately 22.3% of market revenue in 2025 at USD 776 Million. Independent physician groups, multi-specialty practices, and private equity-backed physician platforms represent a growing buyer segment, particularly as consolidation creates larger groups with sufficient coding volume to justify enterprise AI investment. Revenue cycle management outsourcing partners often deliver AI coding capability to smaller practices as part of managed services contracts, extending AI access to the long tail of smaller groups that lack internal technology evaluation capability.

Billing and revenue cycle service organizations represent approximately 16.8% of market revenue at USD 585 Million in 2025. These buyers use AI coding as a productivity and margin enhancement tool within outsourced revenue cycle operations, passing a portion of automation savings to their health system clients while retaining a majority as margin expansion. Payers and health insurance organizations account for the remaining approximately 8.3% of market revenue at USD 289 Million, primarily using AI coding for claims validation, payment integrity audits, and risk adjustment review across Medicare Advantage and commercial risk-adjusted populations.

By Deployment Mode

Cloud-based deployment dominates the market at approximately 68.4% of revenue in 2025, valued at USD 2.38 Billion. Cloud deployment has become the default as HIPAA-compliant hyperscaler environments have been validated for protected health information processing, enabling rapid model updates, federated learning improvements, and elastic compute capacity to handle coding volume seasonality. Large language model inference workloads in particular favor cloud deployment due to GPU compute economics that are inefficient in on-premise infrastructure for most enterprises. On-premise deployment retains approximately 24.6% of revenue at USD 856 Million, concentrated in government and military health systems, specific academic medical centers with data sovereignty policies, and international markets with stricter health data localization requirements. Hybrid deployment, typically combining on-premise data ingestion with cloud-based model inference, represents the remaining approximately 7.0% of market revenue at USD 244 Million.

Regional Analysis

North America

North America holds the largest share of the global AI-powered medical coding market at approximately 48.6%, equivalent to USD 1.69 Billion in 2025. The United States accounts for the substantial majority of regional revenue, driven by the complexity of US reimbursement coding across Medicare, Medicaid, commercial, Medicare Advantage, and ACA marketplace payer contracts, a concentration of large integrated health systems capable of making enterprise AI investments, and a regulatory framework that explicitly permits AI-generated code submissions under provider accountability. The American Health Information Management Association and the American Academy of Professional Coders have adapted certification curricula to reflect AI-augmented coding workflows, signaling workforce alignment with the technology trajectory. Canada contributes through provincial health authority adoption in Ontario, British Columbia, and Quebec, where health information management has been modernized with AI coding pilots in academic hospital networks. The US market benefits from active audit enforcement by the Office of Inspector General and CMS contractor organizations, which drives compliance-grade AI coding system demand where audit trail defensibility commands price premiums over lower-tier alternatives. Mexico contributes modestly through private hospital network adoption in major urban centers.

Europe

Europe represents approximately 23.1% of global market revenue at USD 804 Million in 2025. The United Kingdom leads European adoption through NHS England’s digital transformation programs that include AI coding deployment across integrated care systems, alongside private hospital adoption in the Nuffield Health and HCA Healthcare UK networks. Germany has advanced AI coding through investments by major university hospital networks and hospital consortium purchasing groups, where coding accuracy directly affects DRG-based reimbursement under the G-DRG system. France, Netherlands, and the Nordic countries have steady adoption supported by national digital health strategies and strong health IT infrastructure. The European adoption pattern differs from North America in that coding volumes per hospital are lower and DRG revenue sensitivity is modulated by national tariff systems rather than commercial payer contract complexity, translating to lower per-chart pricing but larger public hospital enterprise deployments. European Medical Device Regulation and GDPR compliance requirements add implementation timelines of 6 to 12 months compared to US deployments, creating a structural headwind to near-term growth rates even as absolute market size expands steadily.

Asia Pacific

Asia Pacific accounts for approximately 18.7% of global market revenue at USD 651 Million in 2025 and is the fastest-growing regional segment, driven by the concentration of offshore medical coding services operations, large hospital chain adoption, and government digital health investment. India holds the leading Asia Pacific share through its dominant offshore revenue cycle services industry, where AI coding automation is being embedded into service delivery for US and UK clients. The Indian services industry has evolved from labor arbitrage to AI-augmented high-value delivery, with leading operators integrating generative AI coding copilots across coder workstations. Australia’s adoption is driven by public hospital network modernization and Medicare Benefits Schedule coding automation. Japan has steady adoption in major university and private hospital groups as the country’s DPC inpatient reimbursement system shares structural similarities with DRG systems that make AI coding automation economically attractive. The Philippines represents a secondary offshore coding delivery hub with rapid AI augmentation. China’s market remains comparatively limited due to the different structure of its hospital coding and payment systems but is expected to accelerate through the forecast period as hospital information systems modernize.

Latin America

Latin America represents approximately 5.8% of global market revenue at USD 202 Million in 2025. Brazil dominates the regional market through its large private hospital chain industry, which operates under diagnosis-related payment systems that reward coding accuracy, and the Brazilian national health information exchange programs that have funded digital infrastructure enabling AI coding deployment. Mexico and Colombia represent secondary markets where private hospital networks have adopted AI coding ahead of public sector investment. Argentina and Chile have smaller but growing adoption. The region’s growth over the forecast period will be supported by the expansion of private health insurance coverage, hospital chain consolidation that creates scaled buyers capable of enterprise AI investment, and offshore coding services companies that deliver AI-augmented operations from Brazilian and Argentine delivery centers to North American customers. Currency volatility and public health sector budget constraints limit public hospital adoption, making the region’s near-term growth concentrated in private sector buyers.

Middle East & Africa

The Middle East and Africa region accounts for approximately 3.8% of global market revenue at USD 132 Million in 2025. The United Arab Emirates leads the region through Dubai Health Authority and Abu Dhabi Department of Health initiatives that have established mandatory ICD-10-CM coding across the emirate’s hospital networks, creating structural demand for AI coding productivity tools. Saudi Arabia’s Vision 2030 health transformation agenda includes health information modernization investments that encompass AI coding platforms across the Ministry of Health network and major private hospital groups. Qatar and Kuwait have parallel programs in smaller markets. South Africa leads Sub-Saharan African adoption through major private hospital groups that operate under diagnosis-related payment frameworks for medical scheme reimbursement. The wider African continent faces significant health IT infrastructure gaps that limit near-term AI coding adoption beyond leading academic and private hospital networks, though telemedicine and cloud-delivered AI services are beginning to bridge infrastructure gaps for specific use cases.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software Solutions

- Services

- Platform Infrastructure

By Coding Type

- Inpatient Coding

- Outpatient Coding

- Professional Services Coding

- Risk Adjustment / HCC Coding

By End-User

- Hospitals and Health Systems

- Physician Practices and Ambulatory Groups

- Billing and Revenue Cycle Service Organizations

- Payers and Health Insurance Organizations

By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.48 B |

| Forecast Revenue (2034) | USD 18.72 B |

| CAGR (2025-2034) | 20.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software Solutions, Services, Platform Infrastructure), By Coding Type, (Inpatient Coding, Outpatient Coding, Professional Services Coding, Risk Adjustment / HCC Coding), By End-User, (Hospitals and Health Systems, Physician Practices and Ambulatory Groups, Billing and Revenue Cycle Service Organizations, Payers and Health Insurance Organizations), By Deployment Mode, (Cloud-Based, On-Premise, Hybrid) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | 3M HEALTH INFORMATION SYSTEMS (SOLVENTUM), OPTUM (UNITEDHEALTH GROUP), NUANCE COMMUNICATIONS (MICROSOFT), ORACLE HEALTH (CERNER), FATHOM, CODAMETRIX, AGS HEALTH, MAVERICK MEDICAL AI, EPIC SYSTEMS, R1 RCM, WIPRO (HEALTHPLAN SERVICES), COGNIZANT (TRIZETTO PROVIDER SOLUTIONS), NTHRIVE, WATERS TECHNOLOGIES, IODINE SOFTWARE, ENTER.HEALTH, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Coding Type (Inpatient Coding, Outpatient Coding, Professional Services Coding, Risk Adjustment/HCC Coding), By End-User (Hospitals, Physician Practices, Billing Organizations, Payers), By Deployment Mode (Cloud, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

, By Coding Type (Inpatient Coding, Outpatient Coding, Professional Services Coding, Risk Adjustment/HCC Coding), By End-User (Hospitals, Physician Practices, Billing Organizations, Payers), By Deployment Mode (Cloud, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

, By Coding Type (Inpatient Coding, Outpatient Coding, Professional Services Coding, Risk Adjustment/HCC Coding), By End-User (Hospitals, Physician Practices, Billing Organizations, Payers), By Deployment Mode (Cloud, On-Premise, Hybrid), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the AI-Powered Medical Coding Market?

The Global AI-Powered Medical Coding Market was valued at USD 2.89 Billion in 2024 and is projected to reach USD 18.72 Billion by 2034, growing at a CAGR of 20.5% from 2026 to 2034, driven by rising adoption of AI-based healthcare automation, increasing demand for accurate medical billing and coding, advancements in NLP and machine learning technologies, and growing focus on revenue cycle management, clinical documentation improvement, and healthcare digitalization worldwide.

Who are the major players in the AI-Powered Medical Coding Market?

3M HEALTH INFORMATION SYSTEMS (SOLVENTUM), OPTUM (UNITEDHEALTH GROUP), NUANCE COMMUNICATIONS (MICROSOFT), ORACLE HEALTH (CERNER), FATHOM, CODAMETRIX, AGS HEALTH, MAVERICK MEDICAL AI, EPIC SYSTEMS, R1 RCM, WIPRO (HEALTHPLAN SERVICES), COGNIZANT (TRIZETTO PROVIDER SOLUTIONS), NTHRIVE, WATERS TECHNOLOGIES, IODINE SOFTWARE, ENTER.HEALTH, Others

Which segments covered the AI-Powered Medical Coding Market?

By Offering, (Software Solutions, Services, Platform Infrastructure), By Coding Type, (Inpatient Coding, Outpatient Coding, Professional Services Coding, Risk Adjustment / HCC Coding), By End-User, (Hospitals and Health Systems, Physician Practices and Ambulatory Groups, Billing and Revenue Cycle Service Organizations, Payers and Health Insurance Organizations), By Deployment Mode, (Cloud-Based, On-Premise, Hybrid)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI-Powered Medical Coding Market

Published Date : 20 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date