- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI-Powered Nutrition App Market Size, Share | CAGR 20.8%

Global AI-Powered Nutrition App Market Size, Share, Analysis By AI Technology (Machine Learning-Based Recommendation Engines, Natural Language Processing Nutrition Assistants, Computer Vision & Food Recognition, Generative AI & Conversational Nutrition Coaching, Predictive Analytics & Personalized Health Insights), By Application (Weight Management & Diet Planning, Fitness & Sports Nutrition, Chronic Disease Management, Personalized Nutrition & Wellness, Meal Planning & Calorie Tracking, Corporate Wellness Programs), By End-User, Revenue Model and Platform Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 4.35 Billion | USD 23.90 Billion | 20.8% | North America, 38.5% |

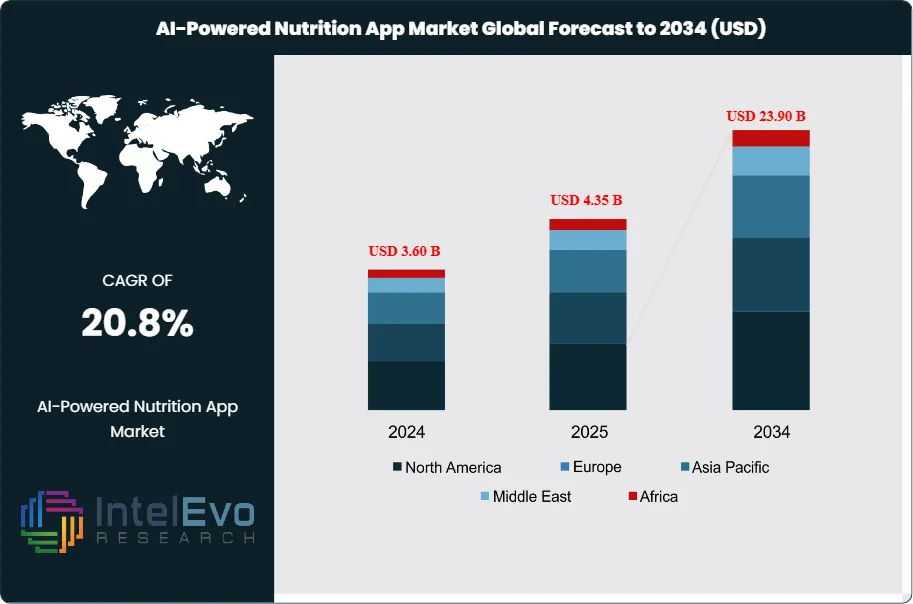

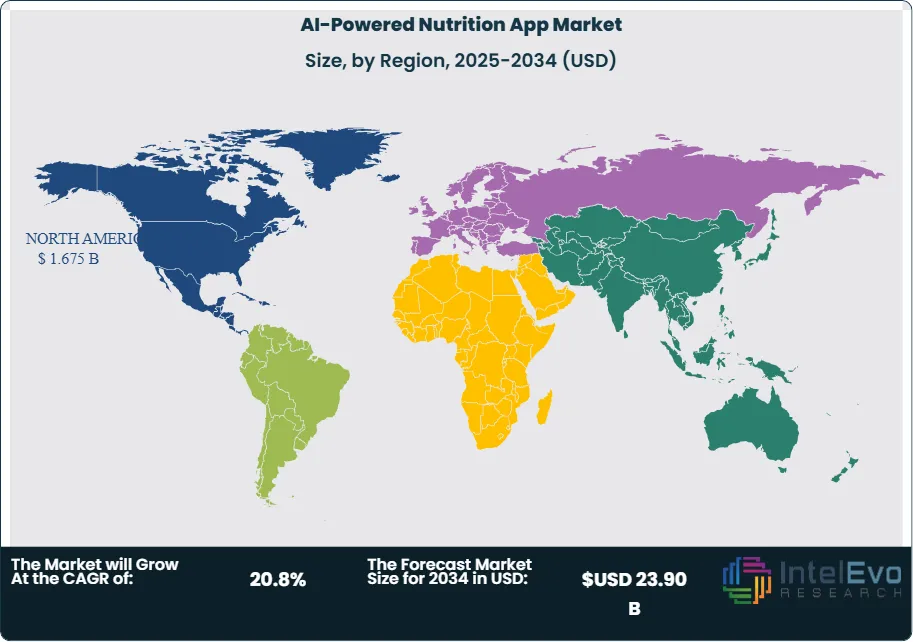

The AI-Powered Nutrition App Market was valued at approximately USD 3.60 Billion in 2024 and reached USD 4.35 Billion in 2025. The market is projected to grow to USD 23.90 Billion by 2034, expanding at a CAGR of 20.8% during the forecast period from 2026 to 2034. The market growth is driven by increasing consumer focus on personalized nutrition, preventive healthcare, weight management, and digital wellness solutions. The integration of artificial intelligence, machine learning, computer vision-based food recognition, and real-time dietary tracking capabilities is enabling highly customized nutrition recommendations and improving user engagement across mobile health platforms. This represents an absolute dollar opportunity of USD 19.55 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportGrowth in the AI-powered nutrition app market is anchored in three structural shifts. First, photo-based logging and computer vision collapsed the friction cost of calorie tracking, evidenced by Cal AI reaching 15 million downloads and over USD 40 Million in trailing 12-month revenue within two years before its March 2, 2026 acquisition by MyFitnessPal. Second, GLP-1 medication demand restructured the nutrition-app revenue model, with Noom reporting a USD 100 Million run-rate for its GLP-1 Rx and pill-based generic programs within four months of launching in September 2024, alongside its November 2025 Diabetes Lifestyle Program. Third, scientific validation became a competitive moat, with ZOE presenting its photologging accuracy study at the American Society for Nutrition conference in Orlando based on 10,000 meals from 2,124 PREDICT 1 and PREDICT 2 participants.

The regulatory environment for AI-powered nutrition apps is consolidating around three frameworks. The US Food and Drug Administration regulates select digital nutrition programs as digital therapeutics and oversees prescribing pathways for GLP-1s such as Ozempic, Wegovy, Zepbound, and Mounjaro used within app-based programs. The EU AI Act's general-purpose AI provisions entered force on August 2, 2025, requiring transparency obligations for AI-coached nutrition apps marketed into the 27-member EU. Data-privacy rules under the US Health Insurance Portability and Accountability Act typically cover only apps working with clinicians, shifting consumer-grade AI-powered nutrition app compliance to California's CCPA, Illinois' BIPA, and the EU GDPR.

Demand is structurally broadening. MyFitnessPal reported approximately 900,000 monthly downloads and USD 13 Million monthly revenue per Sensor Tower 2025 data, against 200 million cumulative registered users and a 20 million-food database. Noom served more than 1.5 million paying subscribers at USD 17 to USD 70 per month by late 2023 and welcomed over 8 million women aged 40 to 60 into its program by February 2025. HealthifyMe reached 16 million users across India and Southeast Asia, with approximately 25% of revenue from outside India. ZOE, Lumen, Viome, and InsideTracker anchor the premium-tier personalized nutrition segment with blood-testing, microbiome, and metabolic breath-analyzer integrations.

North America held the largest AI-powered nutrition app market share at 38.5% in 2025, anchored by MyFitnessPal, Noom, WW International, Viome, Lumen's US operations, and InsideTracker. Asia Pacific recorded the fastest regional growth through HealthifyMe, domestic Chinese health apps, and Japan's expanding digital-health reimbursement. The technology roadmap through 2034 tilts toward multimodal AI that combines meal images, continuous glucose data from Dexcom and Abbott FreeStyle Libre, and large language model coaching integrated with platforms such as ChatGPT Health.

Market Definition & Scope

The AI-powered nutrition app market is defined as the global commercial activity in mobile and web applications that use machine learning, deep learning, computer vision, or natural language processing to deliver dietary tracking, meal planning, nutrient analysis, behaviour coaching, or personalized nutrition recommendations. The market encompasses AI food-recognition apps including MyFitnessPal, Cal AI, and Foodvisor, behaviour-change platforms including Noom and WeightWatchers, biomarker-driven personalized nutrition including ZOE and InsideTracker, and culturally-tailored AI coaching including HealthifyMe's Ria nutritionist.

Included in the scope are subscription revenues, in-app purchases, enterprise B2B licensing, API consumption fees, and ancillary clinician-telehealth fees tied to AI-powered nutrition apps. Explicitly excluded are rule-based calorie counters without AI, generic meal delivery platforms, pure telehealth without app-based coaching, and non-nutrition fitness apps. The AI-powered nutrition app market is a subset of the broader USD 15.79 Billion personalized nutrition market and the USD 5.76 Billion diet and nutrition apps market, accounting for approximately 58% of digital-first personalized nutrition spend in 2025.

, By Application (Weight Management & Diet Planning, Fitness & Sports Nutrition, Chronic Disease Management, Personalized Nutrition & Wellness, Meal Planning & Calorie Tracking, Corporate Wellness Programs), By End-User, Revenue Model and Platform Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The AI-powered nutrition app market expands from USD 4.35 Billion in 2025 to USD 23.90 Billion by 2034, a CAGR of 20.8% over the forecast period.

- Segment Dominance by Technology: The machine learning and deep learning segment led in 2025 with 45.0% share, driven by recommendation engines at MyFitnessPal, Noom, HealthifyMe, and ZOE.

- Segment Dominance by Application: Personalized meal planning and recommendations accounted for 36.8% of 2025 revenue, reflecting subscription demand across MyFitnessPal Premium, Noom, and HealthifyMe.

- Driver: GLP-1 integration pathways drove step-change revenue for digital nutrition apps, evidenced by Noom's USD 100 Million GLP-1 run-rate within four months of September 2024 launch.

- Restraint: Employer GLP-1 coverage remained constrained at 19% of large US employers in 2025, limiting enterprise reimbursement for app-bundled weight-loss programs.

- Opportunity: Photo-based AI calorie tracking represents a USD 2.1 Billion incremental 2034 opportunity, evidenced by Cal AI's USD 40 Million trailing 12-month revenue at acquisition.

- Trend: Computer vision meal-scanning adoption expanded meaningfully in 2025, with MyFitnessPal, ZOE, Foodvisor, Cal AI, and SnapCalorie all shipping production photologging features.

- Regional: North America led the AI-powered nutrition app market with 38.5% share and USD 1.675 Billion in revenue in 2025, followed by Asia Pacific at 29.8%.

Key Insights Summary

- MyFitnessPal announced the acquisition of Cal AI on March 2, 2026, retaining the seven-person Cal AI team under founder and CEO Zach Yadegari, after Cal AI reached 15 million downloads and over USD 40 Million in trailing 12-month revenue within two years, reported by TechCrunch, Inc., GlobeNewswire, and The Next Web.

- Noom launched a Diabetes Lifestyle Program for employers and health plans in November 2025, with a three-month pilot delivering an average A1C reduction of 1.0% and a mean blood glucose reduction of 29 mg/dL, and nearly three-fourths of participants achieving clinically significant A1C reduction.

- Noom introduced Glucose Forecasting in November 2025, predicting meal glucose impact without continuous glucose monitor hardware, available initially to enterprise and select consumer members, extending the AI-powered nutrition app value proposition for prediabetic and Type 2 populations.

- Global health app revenue reached approximately USD 3.5 Billion in 2025, up 23.5% year-over-year per Business of Apps data, with WeightWatchers generating USD 368 Million and MyFitnessPal second, providing a top-line benchmark for AI-powered nutrition app category pricing power.

- HealthifyMe reached 16 million users across India and Southeast Asia by 2024 and raised approximately USD 45 Million in October 2024 led by Khosla Ventures and LeapFrog Investments to accelerate US expansion and AI integration, reported by Inc42 and Business Today.

- MyFitnessPal completed an integration with ChatGPT Health in January 2026 and expanded its ABC Fitness partnership in September 2025, positioning its 20 million-food database and 68,500-brand catalogue as the reference dataset for AI-powered nutrition app food recognition in 2026.

- ZOE validated its photologging AI in a study of 10,000 meals from 2,124 PREDICT 1 and PREDICT 2 participants and presented the findings at the American Society for Nutrition conference in Orlando in 2025, establishing a scientific benchmark for AI-powered nutrition app accuracy claims.

Competitive Landscape Overview

The AI-powered nutrition app market is fragmented at the consumer tier and moderately consolidated at the weight-loss and personalized-nutrition tiers. The top four companies, MyFitnessPal, Noom, HealthifyMe, and Zoe Limited, accounted for an estimated 34.6% of combined 2025 revenue based on public disclosures. Competition is increasingly AI-depth led rather than price-led, because computer vision accuracy, nutrition database depth, and integrated clinical pathways determine retention economics more than sticker price.

Competitive dynamics shifted materially in late 2025 and early 2026 as consolidation accelerated and clinical integrations expanded. MyFitnessPal's Cal AI acquisition on March 2, 2026, followed its Intent meal-planning acquisition in 2024 and its January 2026 ChatGPT Health integration, repositioning MyFitnessPal around an AI-native portfolio rather than a single flagship app. Noom's November 2025 Diabetes Lifestyle Program and Glucose Forecasting features push the category toward clinical outcomes benchmarking. Category entrants, including Alma backed by Menlo Ventures in February 2025 and Seed's microbiome-linked nutrition products, are compressing differentiation time on AI-powered nutrition app procurement checklists.

Competitive Landscape Matrix:

| Company | Headquarters | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| MyFitnessPal, Inc. (Francisco Partners) | United States | Leader | MyFitnessPal Premium; Meal Scan; Cal AI | North America, Europe | Acquired Cal AI on March 2, 2026; launched MyFitnessPal Ads media network on March 17, 2026 |

| Noom, Inc. | United States | Leader | Noom app; Noom Med; GLP-1 Companion | North America, Europe | Launched Diabetes Lifestyle Program and Glucose Forecasting in November 2025 |

| HealthifyMe Private Limited | India | Leader | HealthifySmart; HealthifyCoach; Ria AI nutritionist | India, Southeast Asia, Middle East | Raised approximately USD 45 Million in October 2024 for US expansion and AI integration |

| Zoe Limited | United Kingdom | Leader | ZOE Health AI Meal Tracker; Processed Food Risk Scale | United Kingdom, United States | Launched free AI photologging app in August 2025 validated against PREDICT 1 and PREDICT 2 cohorts |

| Lumen (Metaflow Ltd.) | Israel | Challenger | Lumen metabolic breath analyzer and app | North America, Europe | Expanded AI-powered metabolic coaching into corporate wellness channels |

| Viome Life Sciences, Inc. | United States | Challenger | Viome Full Body Intelligence; gut microbiome kits | North America | Launched transformative consumer health product in April 2025 integrating microbiome insights |

| Foodvisor (Bite SAS) | France | Challenger | Foodvisor AI Calorie Counter | Europe, North America | Updated AI Calorie Counter app version 6.3 in August 2025 with Apple Health integration |

| WW International, Inc. | United States | Niche Player | WeightWatchers app; Wegovy bundled program | North America, Europe | Scaled WeightWatchers Wegovy program at USD 299 through 2025 and added GLP-1 integrations |

| Lifesum AB | Sweden | Niche Player | Lifesum app | Europe, North America | Added AI habit-coaching and recipe personalization through 2025 updates |

| InsideTracker (Segterra, Inc.) | United States | Niche Player | InsideTracker blood biomarker platform | North America | Partnered with Ultrahuman on January 2025 Blood Vision preventive blood-testing platform |

Segmentation Analysis

The AI-powered nutrition app market segments by AI technology, application, end-user, revenue model, and platform. Each segmentation type maps to a distinct buying intent and AI-powered nutrition app procurement checklist, with AI technology depth driving pricing benchmarks and end-user composition driving enterprise-versus-consumer distribution.

By AI Technology

Machine learning and deep learning held the largest AI-powered nutrition app market share at 45.0% in 2025, approximately USD 1.96 Billion, underpinning recommendation engines at MyFitnessPal, Noom, HealthifyMe, and WeightWatchers. Transformer-based models now support natural-language chat coaches, such as Noom's AI and HealthifyMe's Ria AI nutritionist, and MyFitnessPal's January 2026 ChatGPT Health integration. Computer vision held 28.0% and is the fastest-growing sub-segment at an estimated 25.6% CAGR through 2034, with photo meal-recognition deployed across MyFitnessPal Meal Scan, Cal AI, Foodvisor, SnapCalorie, Bitesnap, and ZOE.

Natural language processing held 16.0%, covering conversational coaching, meal-description parsing, and recipe generation. Hybrid and other AI techniques held 11.0%, including reinforcement learning for dynamic meal plans at Suggestic and EatLove, and graph-based nutrigenomic reasoning at Viome Life Sciences, GenoPalate, and Nutrigenomix. The AI-powered nutrition app compliance requirements for health-claim substantiation, covered under the US Federal Trade Commission's Health Products Compliance Guidance updated in December 2022, increase the technical bar for each added AI layer.

By Application

Personalized meal planning and recommendations led the AI-powered nutrition app market at 36.8% in 2025, approximately USD 1.60 Billion, anchored by MyFitnessPal Premium, Noom, HealthifyMe, Lifesum, EatLove, and Suggestic. Calorie and macro tracking held 28.4%, approximately USD 1.24 Billion, with MyFitnessPal, Cal AI, Foodvisor, Lose It!, Cronometer, and Yazio as principal providers. Weight management with GLP-1 integration held 14.5%, approximately USD 631 Million, driven by Noom Med, WeightWatchers' Wegovy bundled program at USD 299, Hims & Hers, Ro, and LifeMD.

Personalized supplementation held 10.5%, covering Viome, Baze Labs, Nutrafol, and Habit's Nestlé Health Science-owned platform. Allergen and sensitivity detection held 5.4%, including Fig, Sifter, and dedicated features inside broader apps. Clinical nutrition management held 4.4%, including DayTwo for glycemic response and Virta Health's diabetes reversal program. The AI-powered nutrition app ROI calculation for health plans and employers typically centres on reduced A1C, measurable weight loss, and medication cost offsets, with Noom's November 2025 Diabetes Lifestyle Program reporting a 1.0% average A1C reduction across a three-month pilot.

By End-User

Individual consumers represented the largest AI-powered nutrition app end-user share at 65.4% in 2025, reflecting direct-to-consumer distribution across the iOS App Store, Google Play, and HarmonyOS. Healthcare providers held 14.8%, covering hospital and clinic integrations for remote patient monitoring and medical nutrition therapy delivered through platforms such as DayTwo, InsideTracker, and Virta Health. Employers and enterprises held 10.6%, driven by corporate wellness contracts at Noom Unite, HealthifyMe enterprise, and HealthifyCorporates, and by the 2026 WeightWatchers Institutional business.

Insurers held 5.3%, including DiGA-reimbursed apps in Germany and Medicare-adjacent pilots in the US. Sports and athletic end-users held 2.5%, including performance-oriented Cal AI and HealthifyCoach deployments. Academic and research users held 1.4%, anchored in Zoe Limited's PREDICT studies and Stanford Medicine-adjacent protocols. The employers and enterprises segment is the fastest-growing end-user sub-segment through 2034, expanding at an estimated 24.6% CAGR as payer coverage expands.

By Revenue Model

Subscription pricing led the AI-powered nutrition app market with 44.9% revenue share in 2025, approximately USD 1.953 Billion, including MyFitnessPal Premium at USD 79.99 annually, Noom at USD 70 monthly, WeightWatchers Clinic Wegovy at USD 299, Cal AI on a consumer subscription, and ZOE at an annual membership. Freemium and in-app purchases held 31.3%, targeting user acquisition before conversion to paid tiers.

Enterprise B2B licensing held 15.6% and is the fastest-growing sub-segment at an estimated 25.2% CAGR through 2034, as Noom Unite, HealthifyCorporates, MyFitnessPal partnerships including the ABC Fitness integration expanded on September 15, 2025, and Virta Health employer contracts scale. Advertising revenue held 8.2%, a category that expanded after MyFitnessPal launched the MyFitnessPal Ads media network on March 17, 2026, opening a new monetization layer for high-intent health-conscious consumers.

By Platform

The iOS platform held the largest AI-powered nutrition app revenue share at 53.2% in 2025, because Apple App Store users exhibit higher willingness-to-pay for digital health subscriptions across the US, UK, Japan, and Germany. Android held 43.6% of 2025 revenue and the largest share of total AI-powered nutrition app downloads, led by HealthifyMe in India, Lifesum in Europe, and mass-market deployments of MyFitnessPal, Noom, and Foodvisor. HarmonyOS and other platforms held the remaining 3.2%, with HarmonyOS the fastest-growing platform in China driven by Huawei's ecosystem expansion across 2024 and 2025.

Regional Analysis

The AI-powered nutrition app market is geographically led by North America, Asia Pacific, and Europe, together accounting for 90.1% of 2025 revenue. Regional competitive dynamics differ, with North America leading on subscription revenue per user, Asia Pacific leading on download volume and India-anchored localization, and Europe leading on DiGA reimbursement and scientific validation depth.

North America

North America held 38.5% of the AI-powered nutrition app market in 2025, approximately USD 1.675 Billion. The United States dominates with MyFitnessPal headquartered in San Francisco under Francisco Partners ownership since the October 2020 USD 345 Million acquisition from Under Armour, Noom in Princeton, WeightWatchers as WW International on NASDAQ, Cal AI now a MyFitnessPal unit, Viome Life Sciences, and InsideTracker. Canada contributes through Nutrigenomix and expanding WeightWatchers Clinic partnerships, while Mexico is an emerging buyer through HealthifyMe and Lifesum. US Food and Drug Administration guidance through 2024 and 2025 on GLP-1 telehealth prescribing and the FTC's updated Health Products Compliance Guidance define North American AI-powered nutrition app compliance requirements.

Europe

Europe accounted for 21.8% of the AI-powered nutrition app market in 2025, approximately USD 948.3 Million. The United Kingdom leads through Zoe Limited's scientific validation and PREDICT studies, Germany through the Digital Healthcare Act (DVG) which created the DiGA reimbursement pathway, France through Foodvisor (Bite SAS), and Sweden through Lifesum AB. The EU AI Act's August 2, 2025 general-purpose AI enforcement applies to nutrition apps with AI coaching, and the EU Digital Services Act and GDPR jointly define AI-powered nutrition app data-handling compliance requirements across the 27 member states. The European Medicines Agency regulates pharmaceutical components of app-bundled GLP-1 programs separately.

Asia Pacific

Asia Pacific held 29.8% of the AI-powered nutrition app market in 2025, approximately USD 1.296 Billion, and recorded the fastest regional growth. India dominates through HealthifyMe's 16 million users and USD 20.5 Million FY24 revenue, with Bangalore-headquartered HealthifyMe expanding into Singapore, Malaysia, and US Indian-diaspora markets. China's Tencent Holdings, Ant Group, and domestic Keep.ai platform integrate AI nutrition features, with Keep backed by SoftBank Vision Fund's USD 360 Million round. Japan represents the fastest-growing country-level market through 2030 per Grand View Research, with MyFitnessPal, Noom, and Asken expanding localized offerings. Chinese and Korean regulators drafted streamlined digital-therapeutics pathways in 2024 and 2025, shortening AI-powered nutrition app implementation timelines.

Latin America

Latin America held 6.5% of the AI-powered nutrition app market in 2025, approximately USD 282.8 Million. Brazil leads with strong adoption of MyFitnessPal, Lifesum, and Yazio and growing HealthifyMe penetration; Mexico follows with corporate wellness pilots; and Argentina and Colombia contribute smaller but growing consumer segments. Regional subscription pricing typically runs 30% to 40% below North American comparables because of currency dynamics and purchasing-power parity. Brazil's Agência Nacional de Vigilância Sanitária (ANVISA) regulates digital therapeutic claims, while Mexico's COFEPRIS oversees medical nutrition therapy apps.

Middle East & Africa

Middle East & Africa accounted for 3.4% of the AI-powered nutrition app market in 2025, approximately USD 147.9 Million. The United Arab Emirates and Saudi Arabia lead regional adoption, supported by Saudi Arabia's Vision 2030 healthy lifestyle goals and the UAE's Ministry of Health and Prevention's digital health strategy. South Africa leads sub-Saharan adoption through corporate wellness and private-insurer programs with Discovery Vitality. Arabic-language AI coaching remains a structural gap that HealthifyMe, MyFitnessPal, and Noom are progressively filling. Saudi Food and Drug Authority and UAE regulatory frameworks align AI-powered nutrition app clinical-claim handling with FDA and EMA benchmarks.

Country Analysis

Four national AI-powered nutrition app markets, the United States, India, the United Kingdom, and Japan, collectively accounted for approximately 60.7% of 2025 revenue. These countries concentrate vendor headquarters, regulatory frameworks, and the payer-reimbursement pilots that set AI-powered nutrition app pricing benchmarks.

United States

The United States represented approximately USD 1.52 Billion in 2025 AI-powered nutrition app revenue, with a country CAGR estimated at 21.4% through 2034. Federal activity concentrated around the US Food and Drug Administration's Digital Health Advisory Committee, which guided 2025 policy on digital therapeutics and app-bundled GLP-1 prescribing. The Federal Trade Commission's updated Health Products Compliance Guidance issued in December 2022 and reinforced through 2025 enforcement actions defined the substantiation bar for AI-powered nutrition claims. US employer GLP-1 coverage reached 19% of large employers in 2025, limiting enterprise GLP-1 reimbursement but leaving ample runway for behaviour-based apps. State-level BIPA in Illinois and CCPA in California define biometric-data handling for apps ingesting photos of meals or wearable data.

India

India represented approximately USD 657 Million in 2025 AI-powered nutrition app revenue, with a country CAGR estimated at 24.8% through 2034. HealthifyMe's 16 million users, 75+ corporate wellness clients, and USD 20.5 Million FY24 revenue anchor the domestic market, complemented by Healthify's October 2024 Rs 378 Crore (approximately USD 45 Million) Series D round led by Khosla Ventures and LeapFrog Investments. The Indian Council of Medical Research publishes dietary guidelines that HealthifyMe's Ria AI nutritionist is calibrated against. The Ministry of Ayush governs traditional-medicine integration, and the Digital Personal Data Protection Act, 2023, which came into force through 2024 and 2025, governs AI-powered nutrition app data handling.

United Kingdom

The United Kingdom represented approximately USD 258 Million in 2025 AI-powered nutrition app revenue, with a country CAGR estimated at 20.2% through 2034. Zoe Limited's London headquarters, ZOE Health AI Meal Tracker, and PREDICT 1 and PREDICT 2 studies underpin UK scientific leadership. The UK Medicines and Healthcare products Regulatory Agency (MHRA) regulates AI-powered nutrition app clinical claims, and the National Institute for Health and Care Excellence's digital health technologies evidence standards framework sets the UK AI-powered nutrition app compliance benchmark. Public-sector pilots under NHS England through 2024 and 2025 evaluated digital nutrition coaching for Type 2 diabetes prevention, creating a structural AI-powered nutrition app procurement channel.

Japan

Japan represented approximately USD 205 Million in 2025 AI-powered nutrition app revenue, with a country CAGR estimated at 22.6% through 2034, the fastest among the four profiled countries per Grand View Research. Domestic apps Asken and Calomeal lead the local market, with MyFitnessPal, Noom, and HealthifyMe expanding Japanese-language offerings through 2025. Japan's Pharmaceuticals and Medical Devices Agency (PMDA) approved selected medical nutrition therapy digital products through 2024 and 2025, and Japanese national insurance reimbursement for digital nutrition interventions is expanding under the Ministry of Health, Labour and Welfare's Society 5.0 digital health framework. Japan's ageing demographic, with more than 29% of the population over 65, underwrites structural demand for chronic-disease-oriented AI-powered nutrition apps.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By AI Technology

- Machine Learning-Based Recommendation Engines

- Natural Language Processing (NLP) Nutrition Assistants

- Computer Vision & Food Recognition

- Generative AI & Conversational Nutrition Coaching

- Predictive Analytics & Personalized Health Insights

By Application

- Weight Management & Diet Planning

- Fitness & Sports Nutrition

- Chronic Disease Management (Diabetes, Cardiovascular Health, Obesity)

- Personalized Nutrition & Wellness

- Meal Planning & Calorie Tracking

- Corporate Wellness Programs

By End-User

- Individual Consumers

- Fitness Enthusiasts & Athletes

- Healthcare Providers & Dietitians

- Corporate Wellness Organizations

- Insurance & Digital Health Companies

By Revenue Model

- Subscription-Based

- Freemium with In-App Purchases

- Advertising-Supported

- Enterprise & B2B Licensing

- Nutrition Coaching & Premium Services

By Platform

- iOS Applications

- Android Applications

- Web-Based Platforms

- Wearable-Integrated Applications

- Cross-Platform Solutions

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.35 B |

| Forecast Revenue (2034) | USD 23.90 B |

| CAGR (2025-2034) | 20.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By AI Technology, (Machine Learning-Based Recommendation Engines, Natural Language Processing (NLP) Nutrition Assistants, Computer Vision & Food Recognition, Generative AI & Conversational Nutrition Coaching, Predictive Analytics & Personalized Health Insights), By Application, (Weight Management & Diet Planning, Fitness & Sports Nutrition, Chronic Disease Management (Diabetes, Cardiovascular Health, Obesity), Personalized Nutrition & Wellness, Meal Planning & Calorie Tracking, Corporate Wellness Programs), By End-User, (Individual Consumers, Fitness Enthusiasts & Athletes, Healthcare Providers & Dietitians, Corporate Wellness Organizations, Insurance & Digital Health Companies), By Revenue Model, (Subscription-Based, Freemium with In-App Purchases, Advertising-Supported, Enterprise & B2B Licensing, Nutrition Coaching & Premium Services), By Platform, (iOS Applications, Android Applications, Web-Based Platforms, Wearable-Integrated Applications, Cross-Platform Solutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MYFITNESSPAL, INC. (FRANCISCO PARTNERS), NOOM, INC., HEALTHIFYME PRIVATE LIMITED, ZOE LIMITED, LUMEN (METAFLOW LTD.), VIOME LIFE SCIENCES, INC., FOODVISOR (BITE SAS), WW INTERNATIONAL, INC., LIFESUM AB, INSIDETRACKER (SEGTERRA, INC.), CAL AI (MYFITNESSPAL UNIT), HABIT (NESTLE HEALTH SCIENCE), DAYTWO LTD., GENOPALATE, INC., NUTRIGENOMIX INC., CRONOMETER SOFTWARE INC., YAZIO GMBH, LOSE IT! (FITNOW, INC.), SUGGESTIC, INC., EATLOVE, INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Weight Management & Diet Planning, Fitness & Sports Nutrition, Chronic Disease Management, Personalized Nutrition & Wellness, Meal Planning & Calorie Tracking, Corporate Wellness Programs), By End-User, Revenue Model and Platform Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Application (Weight Management & Diet Planning, Fitness & Sports Nutrition, Chronic Disease Management, Personalized Nutrition & Wellness, Meal Planning & Calorie Tracking, Corporate Wellness Programs), By End-User, Revenue Model and Platform Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Application (Weight Management & Diet Planning, Fitness & Sports Nutrition, Chronic Disease Management, Personalized Nutrition & Wellness, Meal Planning & Calorie Tracking, Corporate Wellness Programs), By End-User, Revenue Model and Platform Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the AI-Powered Nutrition App Market?

The Global AI-Powered Nutrition App Market was valued at USD 3.60 Billion in 2024 and is projected to reach USD 23.90 Billion by 2034, growing at a CAGR of 20.8% from 2026 to 2034. Growth is driven by rising demand for personalized nutrition, AI-powered diet planning, food recognition technology, calorie tracking, preventive healthcare, wearable device integration, telehealth adoption, chronic disease management, fitness optimization, and digital wellness solutions worldwide.

Who are the major players in the AI-Powered Nutrition App Market?

MYFITNESSPAL, INC. (FRANCISCO PARTNERS), NOOM, INC., HEALTHIFYME PRIVATE LIMITED, ZOE LIMITED, LUMEN (METAFLOW LTD.), VIOME LIFE SCIENCES, INC., FOODVISOR (BITE SAS), WW INTERNATIONAL, INC., LIFESUM AB, INSIDETRACKER (SEGTERRA, INC.), CAL AI (MYFITNESSPAL UNIT), HABIT (NESTLE HEALTH SCIENCE), DAYTWO LTD., GENOPALATE, INC., NUTRIGENOMIX INC., CRONOMETER SOFTWARE INC., YAZIO GMBH, LOSE IT! (FITNOW, INC.), SUGGESTIC, INC., EATLOVE, INC., Others

Which segments covered the AI-Powered Nutrition App Market?

By AI Technology, (Machine Learning-Based Recommendation Engines, Natural Language Processing (NLP) Nutrition Assistants, Computer Vision & Food Recognition, Generative AI & Conversational Nutrition Coaching, Predictive Analytics & Personalized Health Insights), By Application, (Weight Management & Diet Planning, Fitness & Sports Nutrition, Chronic Disease Management (Diabetes, Cardiovascular Health, Obesity), Personalized Nutrition & Wellness, Meal Planning & Calorie Tracking, Corporate Wellness Programs), By End-User, (Individual Consumers, Fitness Enthusiasts & Athletes, Healthcare Providers & Dietitians, Corporate Wellness Organizations, Insurance & Digital Health Companies), By Revenue Model, (Subscription-Based, Freemium with In-App Purchases, Advertising-Supported, Enterprise & B2B Licensing, Nutrition Coaching & Premium Services), By Platform, (iOS Applications, Android Applications, Web-Based Platforms, Wearable-Integrated Applications, Cross-Platform Solutions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI-Powered Nutrition App Market

Published Date : 02 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date