- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI-Powered Robotic Process Automation Market Size, Share | CAGR 21.5%

Global AI-Powered Robotic Process Automation Market Size, Share, Analysis By Component (Software & Platforms, Implementation Services, Managed Automation Services, Consulting & Training), By Technology (Machine Learning & NLP, Computer Vision, Intelligent Document Processing, Generative AI & LLM Agents, Process Mining & Task Mining), By Deployment Mode (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By Vertical (BFSI, Healthcare, Manufacturing, Retail, IT & Telecom, Government) Industry Trends & Forecast 2026-2034

Report Overview

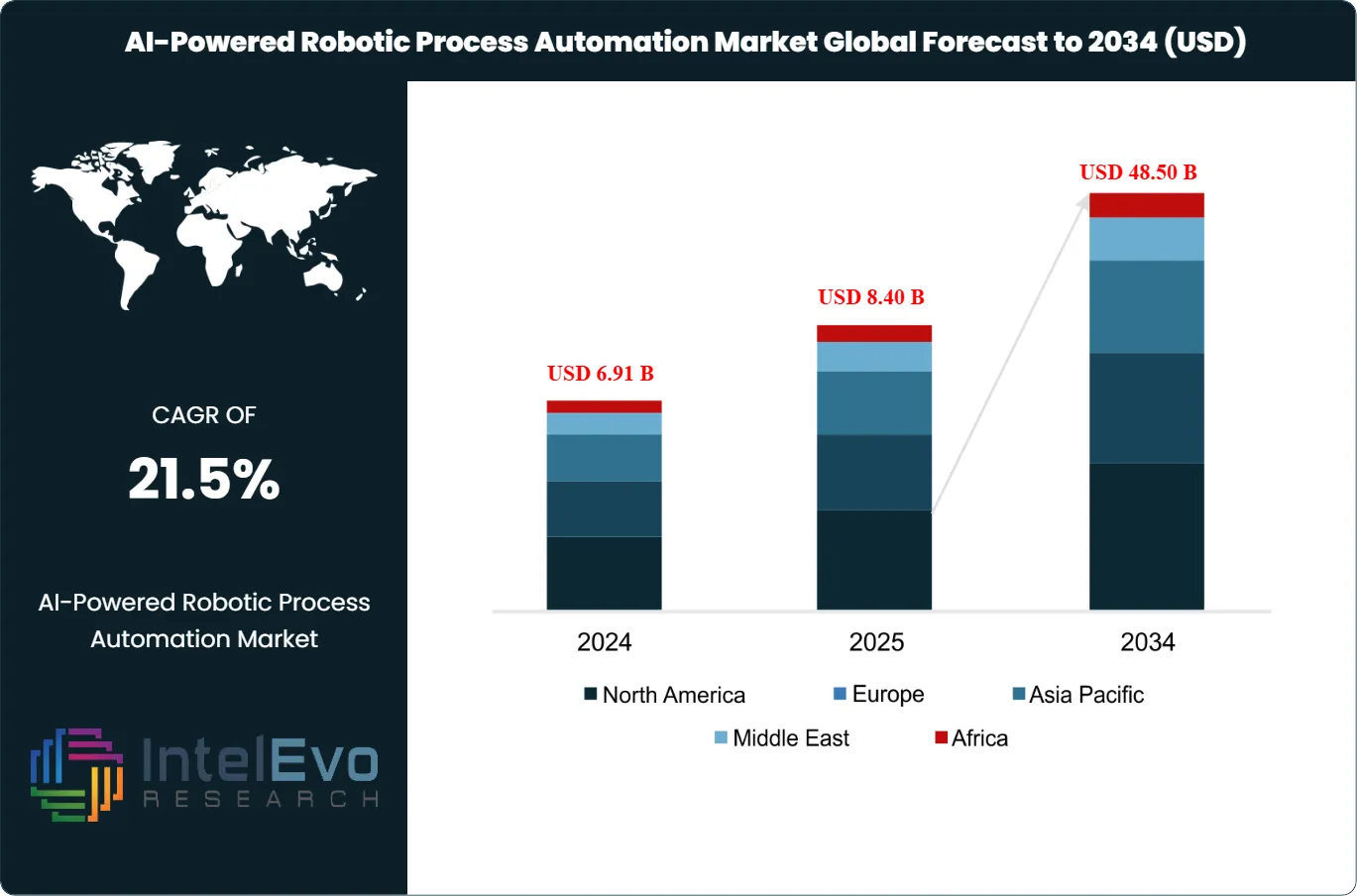

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 8.4 Billion | USD 48.5 Billion | 21.5% | North America, 41.6% |

The AI-Powered Robotic Process Automation Market was valued at approximately USD 6.91 Billion in 2024 and reached USD 8.40 Billion in 2025. The market is projected to grow to USD 48.50 Billion by 2034, expanding at a CAGR of 21.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 40.1 Billion over the analysis period. The AI-powered robotic process automation market marks the convergence of traditional RPA, which automates rule-based screen-level tasks, with machine learning, natural language processing, computer vision, and generative AI, which together extend automation into judgment-heavy, unstructured, and exception-driven processes that rule-based bots could not address.

Get More Information about this report -

Request Free Sample ReportEnterprise adoption of AI-powered RPA has crossed the inflection point between departmental pilots and enterprise-wide orchestration. Procurement data indicates that the average Fortune 500 company now operates between 800 and 2,500 attended and unattended bots, up from approximately 120-300 in 2021. The expansion is driven by measurable ROI. Industry benchmarks show that AI-augmented bots reduce process cycle time by 55-72% compared with manual execution and 25-38% compared with rule-based RPA alone, while extending automation eligibility from an estimated 30% of enterprise tasks under traditional RPA to roughly 65% when AI capabilities are layered in. Intelligent document processing powered by transformer models, conversational AI for customer-facing automation, and process mining that identifies automation candidates from event logs have become standard capabilities within leading platforms.

The competitive structure of the AI-powered robotic process automation market shifted materially in 2024-2025 with the arrival of agentic automation. Large language model-driven agents that can interpret natural-language instructions, decompose tasks across applications, handle exceptions through reasoning, and self-correct failures represent a generational advance beyond scripted bot flows. UiPath, Automation Anywhere, Microsoft, and Pegasystems all launched agent-native features in this period, and enterprise early-adopter programs report 30-45% reductions in bot development time and 18-26% increases in straight-through processing rates when agentic capabilities are deployed.

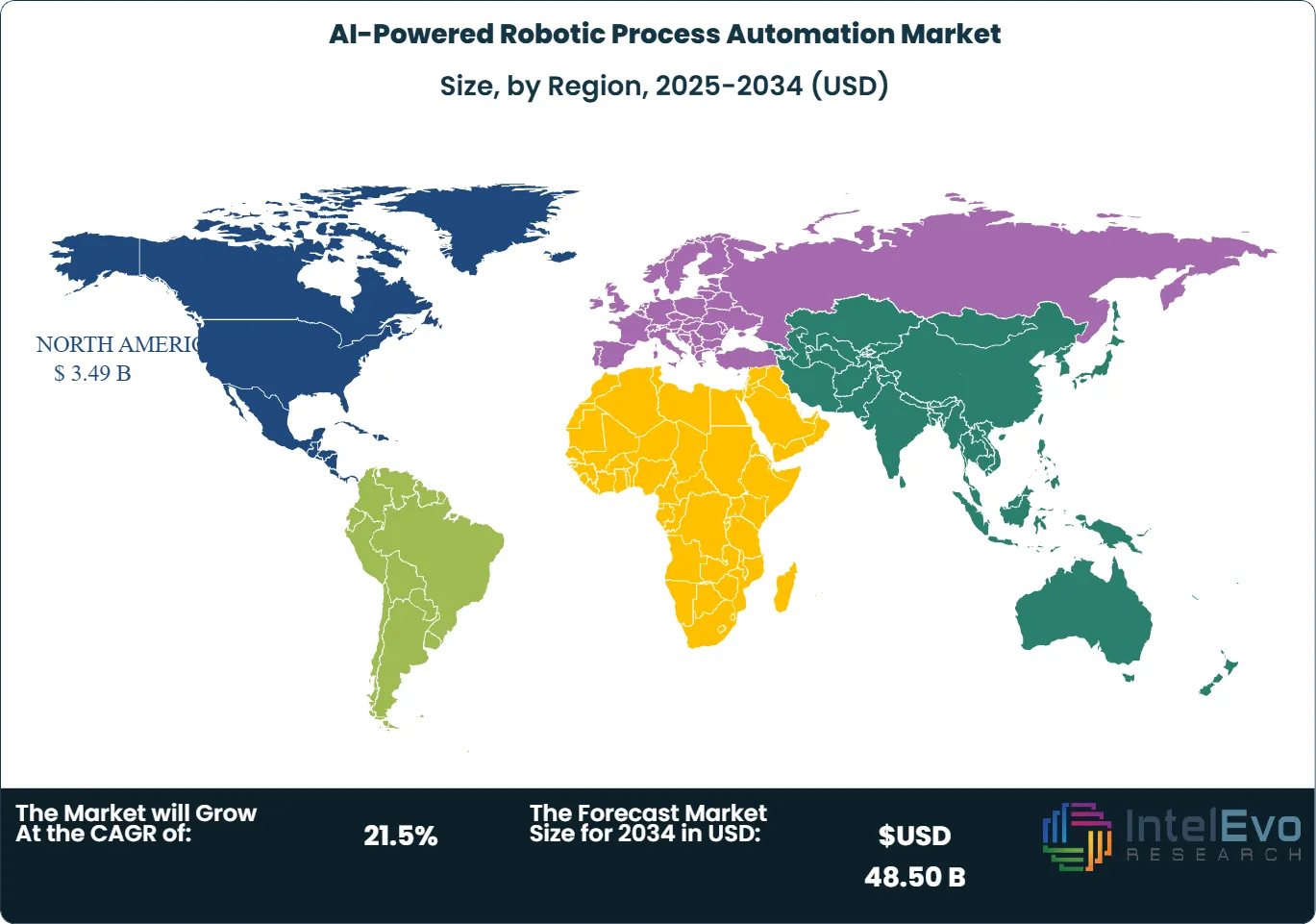

Regulatory and compliance automation is expanding the total addressable market. Financial services firms deploying AI-powered RPA for KYC remediation, sanctions screening, and regulatory reporting report 40-60% reductions in manual review volume. Healthcare organizations are using intelligent automation for claims adjudication, prior authorization, and clinical documentation improvement. Government agencies are deploying digital workers for benefits processing, tax administration, and procurement workflows. North America leads with 41.6% of market value at USD 3.49 Billion in 2025, followed by Europe at 27.4% and Asia Pacific at 22.8%, the fastest-growing region driven by Japan, India, and South Korea enterprise digitalization programs.

, By Technology (Machine Learning & NLP, Computer Vision, Intelligent Document Processing, Generative AI & LLM Agents, Process Mining & Task Mining), By Deployment Mode (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By Vertical (BFSI, Healthcare, Manufacturing, Retail, IT & Telecom, Government) Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The AI-powered robotic process automation market was valued at USD 8.4 Billion in 2025 and is projected to reach USD 48.5 Billion by 2034, expanding at a CAGR of 21.5% across the 2026-2034 forecast period.

- Segment Dominance: Software and platforms held 62.4% of market value in 2025, reflecting enterprise consolidation onto integrated automation platforms that combine RPA, AI, process mining, and orchestration.

- Segment Dominance: BFSI led vertical demand at 26.4% share in 2025, driven by KYC remediation, sanctions screening, claims processing, and regulatory reporting automation.

- Driver: AI augmentation extends automation eligibility from roughly 30% of enterprise tasks under rule-based RPA to approximately 65% when machine learning, NLP, IDP, and agentic capabilities are integrated, expanding the addressable process universe.

- Restraint: Integration complexity with legacy enterprise systems remains the primary barrier. An estimated 42% of AI-powered RPA projects exceed initial implementation timelines by 3-6 months due to API limitations, mainframe screen scraping fragility, and data governance constraints.

- Opportunity: Agentic automation, where LLM-driven agents decompose and execute multi-step processes with exception handling, represents an incremental opportunity estimated at USD 8.2 Billion between 2025 and 2030 as enterprise early-adopter programs scale to production.

- Trend: Process mining integration reached 58% penetration among enterprise AI-powered RPA deployments in 2025, enabling continuous discovery and prioritization of automation candidates from system event logs.

- Regional Analysis: North America led the AI-powered robotic process automation market in 2025 with 41.6% share and USD 3.49 Billion in revenue, supported by Fortune 500 enterprise-wide rollouts and federal digital modernization programs.

Competitive Landscape Overview

The AI-powered robotic process automation market is moderately consolidated at the platform layer and fragmented among services and niche solution providers. The four largest platform vendors accounted for an estimated 52.6% of software license and subscription revenue in 2025. Competition is technology-driven, with differentiation built on AI model breadth, agentic orchestration maturity, process mining integration, and the depth of pre-built connectors to enterprise systems including SAP, Salesforce, ServiceNow, Oracle, and mainframe environments. Microsoft's entry through Power Automate with Copilot integration has shifted competitive dynamics by bundling automation into the Microsoft 365 enterprise agreement, creating pricing pressure on pure-play vendors and forcing differentiation on depth, governance, and complex orchestration. Acquisitions have accelerated since 2024, with platform vendors absorbing process mining, intelligent document processing, and communications mining capabilities to deliver full-stack automation platforms.

Competitive Landscape Matrix

| Company | Headquarters | Market Position | Key Platform / Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| UiPath | United States | Leader | UiPath Business Automation Platform (Autopilot, AI Center, Agentic Automation) | North America, Europe, Asia Pacific | Launched Agentic Automation with autonomous multi-step AI agents in 2025 |

| Automation Anywhere | United States | Leader | Automation Success Platform (AI Agent Studio, IQ Bot, Process Discovery) | North America, Europe, Asia Pacific | Released AI Agent Studio for enterprise-grade autonomous agent creation in 2025 |

| Microsoft | United States | Leader | Power Automate (Copilot, AI Builder, Process Mining, Desktop Flows) | North America, Europe, Asia Pacific | Integrated Copilot-driven autonomous workflow generation into Power Automate in 2025 |

| SS&C Blue Prism | United Kingdom / United States | Leader | Blue Prism Intelligent Automation Platform (Decision, Decipher IDP) | Europe, North America | Deepened SS&C AI integration with Decipher IDP and advanced process orchestration in 2025 |

| SAP | Germany | Challenger | SAP Build Process Automation (Signavio, SAP AI Core integration) | Europe, North America, Asia Pacific | Embedded Joule AI copilot into SAP Build Process Automation workflows in 2025 |

| NICE Ltd. | Israel / United States | Challenger | NICE Robotic Automation (Attended, Unattended, NEVA) | North America, Europe | Extended NEVA Autopilot with generative AI-driven task orchestration in 2025 |

| Pegasystems | United States | Challenger | Pega Platform (Pega GenAI, Process Fabric, Auto ML) | North America, Europe | Integrated Pega GenAI Blueprint with autonomous process generation in 2025 |

| Celonis | Germany / United States | Challenger | Celonis Process Intelligence (Process Mining, Action Engine, PQL) | Europe, North America | Combined Process Intelligence with automated execution via Action Engine in 2025 |

| WorkFusion | United States | Niche Player | WorkFusion Intelligent Automation (Digital Workers for compliance) | North America, Europe | Launched pre-trained AML and sanctions screening digital workers for banking in 2025 |

| Appian | United States | Niche Player | Appian Platform (Process Mining, AI Copilot, Low-Code Automation) | North America, Europe | Released AI Process Designer for autonomous workflow mapping and creation in 2025 |

By Component

Software and platforms dominated the AI-powered robotic process automation market at 62.4% share in 2025, equivalent to USD 5.24 Billion. Enterprise buyers are consolidating onto integrated platforms that combine attended and unattended bot execution, intelligent document processing, conversational AI, process mining, test automation, and orchestration under a single license and governance framework. Platform pricing has shifted from per-bot licensing toward consumption-based models measuring automation value delivered, a transition led by UiPath and Automation Anywhere in 2024-2025. AI capabilities are embedded at every layer: machine learning classifiers for document extraction, NLP for email and chat automation, computer vision for screen interpretation, and generative AI for bot development acceleration and exception handling. Platform governance features including centralized credential management, audit logging, and role-based access control are critical procurement criteria for regulated industry buyers.

Services contributed 37.6% at approximately USD 3.16 Billion in 2025. This category covers implementation and integration consulting, managed automation services, Center of Excellence design, bot lifecycle management, and training. Services demand is being reshaped by two dynamics. First, the shift from departmental pilots to enterprise-wide automation programs requires organizational change management, operating model redesign, and governance framework implementation that pure technology deployment cannot address. Second, managed automation services operated by global system integrators and specialist providers are growing at 28% annually as enterprises seek to outsource bot operations, exception handling, and continuous improvement cycles. The top five global system integrators now operate dedicated AI-powered RPA practices with combined headcounts exceeding 40,000 consultants.

By Technology

Machine learning and natural language processing held the largest technology share at 38.2% in 2025, equivalent to approximately USD 3.21 Billion. ML classifiers and NLP models power the intelligence layer that extends RPA beyond rule-based execution into unstructured data processing, intent recognition, sentiment analysis, and predictive decision support. Enterprises use NLP-enabled bots for email triage, customer inquiry routing, contract clause extraction, and regulatory filing interpretation. ML-powered anomaly detection is deployed within bot orchestration to flag process exceptions and trigger human-in-the-loop escalation, increasing straight-through processing rates by 18-26% relative to static rule-based exception handling.

Computer vision and intelligent document processing captured 24.6% at USD 2.07 Billion. IDP platforms combine optical character recognition, layout analysis, and transformer-based extraction models to process invoices, purchase orders, claims forms, medical records, and identity documents at accuracy rates exceeding 94% on structured templates and 85-90% on semi-structured and unstructured inputs. Generative AI and LLM agents held 21.8% at USD 1.83 Billion, reflecting the rapid scaling of agentic automation where large language models interpret natural-language instructions, decompose multi-step processes, interact with enterprise applications through APIs and UIs, and handle exceptions via reasoning chains. Process mining and task mining contributed 15.4% at USD 1.29 Billion, providing the analytical backbone that identifies, prioritizes, and continuously monitors automation candidates from system event logs and desktop activity recordings.

By Deployment Mode

Cloud deployment led the AI-powered robotic process automation market at 68.2% share in 2025, equivalent to USD 5.73 Billion. Multi-tenant SaaS platforms align with enterprise cloud-first strategies, enable continuous AI model updates without customer-side deployment cycles, and support elastic scaling for variable automation workloads. All four leading platform vendors have transitioned to cloud-first architectures with native SaaS delivery. On-premise deployment held 19.4% at USD 1.63 Billion, concentrated in banking, defense, government, and healthcare organizations with strict data residency requirements, air-gapped network policies, or legacy mainframe environments that require local bot execution. Hybrid deployment captured 12.4% at USD 1.04 Billion, serving enterprises that operate cloud-based orchestration and AI services alongside on-premise bot runners executing against locally hosted ERP, core banking, or HIS systems.

By Vertical

BFSI led vertical demand at 26.4% share in 2025, equivalent to USD 2.22 Billion. Banks, insurers, and capital markets firms deploy AI-powered RPA for KYC and AML remediation, loan origination document processing, claims adjudication, regulatory reporting, trade settlement, and customer onboarding. ROI data from Tier 1 banks indicates 40-60% reductions in manual review volume for compliance workflows when AI-augmented bots handle document extraction, entity matching, and exception triage. Healthcare followed at 14.8% or USD 1.24 Billion, covering claims processing, prior authorization, clinical documentation improvement, patient scheduling, and revenue cycle management. Manufacturing held 13.6% at USD 1.14 Billion, driven by supply chain document processing, quality control automation, and ERP transaction management.

Retail and e-commerce captured 12.2% at USD 1.02 Billion, with deployment concentrated in order management, returns processing, catalog enrichment, and customer service automation. IT and telecommunications held 11.8% at USD 0.99 Billion, covering service desk automation, network provisioning, billing operations, and SLA management. Government accounted for 9.4% at USD 0.79 Billion, driven by benefits processing, tax administration, procurement, and citizen service automation. Remaining verticals including energy, education, and logistics contributed 11.8%. BFSI and healthcare are expected to maintain vertical leadership through 2034, while government is the fastest-growing vertical as federal and state digital modernization programs accelerate.

Regional Analysis

North America

North America led the AI-powered robotic process automation market in 2025 with 41.6% share and USD 3.49 Billion in revenue. The United States dominates, with Fortune 500 enterprises operating enterprise-wide automation programs that average 800-2,500 bots per organization. Banking, insurance, and healthcare verticals are the largest consumers, followed by federal civilian and defense agencies deploying automation under OMB modernization directives and the Federal RPA Community of Practice. GSA's Centers of Excellence have facilitated RPA deployment across more than 30 federal agencies since 2020, and the transition to AI-powered capabilities accelerated in 2024-2025 with the integration of IDP and generative AI into agency workflows. Canada contributes through banking sector automation under OSFI operational resilience guidance and provincial government digital services programs. Mexico participates through multinational shared service center operations, with financial services and manufacturing the dominant verticals. The vendor base is concentrated in North America, with UiPath, Automation Anywhere, Microsoft, and the majority of pure-play AI-powered RPA challengers headquartered in the region.

Europe

Europe held 27.4% share at USD 2.30 Billion in 2025. Germany leads European demand, driven by manufacturing sector ERP automation, automotive supply chain digitalization, and DORA-aligned financial services operational resilience programs. The United Kingdom ranks second, anchored by the City of London financial services complex, NHS operational efficiency programs, and HMRC digital tax administration initiatives. France follows through CAC 40 enterprise automation programs, Banque de France regulatory compliance automation, and public sector digital transformation under the France 2030 initiative. The Netherlands completes the top four, serving as the European shared services hub with concentrated automation deployment across BFSI, logistics, and professional services. GDPR, DORA, and CSRD compliance workflows are structural demand drivers unique to Europe, with enterprises deploying AI-powered bots for data subject access request processing, incident reporting, and ESG data collection. SS&C Blue Prism and SAP hold stronger relative positions in Europe compared with their North American share, reflecting UK heritage and SAP ERP integration advantages respectively.

Asia Pacific

Asia Pacific captured 22.8% share at USD 1.92 Billion in 2025 and is the fastest-growing regional market. Japan leads regional demand, driven by severe labor shortages in financial services and government administration, with automation deployed as a structural workforce augmentation strategy. The Japanese government's Digital Transformation initiative and the Financial Services Agency's operational efficiency guidance have accelerated adoption across banking, insurance, and public administration. India holds the second position, anchored by IT services and BPO providers embedding AI-powered RPA into client delivery models, a large domestic banking sector undergoing digital transformation under RBI guidelines, and growing government automation through programs such as the Digital India initiative. South Korea follows through KFSC-aligned financial services automation and manufacturing sector deployment across semiconductor, automotive, and electronics supply chains. China contributes through domestic platform vendors including Laiye and UiBot alongside deployments by multinationals operating shared services in Shanghai and Shenzhen. Australia advances through APRA-regulated financial services automation and APS federal government digital modernization.

Latin America

Latin America accounted for 4.4% share at USD 0.37 Billion in 2025. Brazil is the primary market, driven by Banco Central digital modernization, BFSI automation in Sao Paulo's banking cluster, and growing shared services center deployment by multinationals. Mexico follows through nearshore BPO operations, manufacturing sector ERP automation, and BFSI compliance deployment under CNBV guidance. Colombia holds the third position, with the Superintendencia Financiera encouraging operational efficiency in banking and insurance. Regional adoption patterns favor cloud-delivered platforms with pre-built connectors to SAP, Oracle, and Salesforce, which are the dominant ERP environments across Latin American enterprises. Channel development through Deloitte, Accenture, and regional system integrators is the primary route to market, with direct vendor sales concentrated among the top 200 enterprises in each country. Language model availability in Portuguese and Spanish has improved materially since 2024, reducing a prior barrier to NLP-powered automation in the region.

Middle East & Africa

The Middle East & Africa region held 3.8% share at USD 0.32 Billion in 2025. The UAE leads regional activity, with government automation programs under the UAE Strategy for Artificial Intelligence 2031 and Abu Dhabi's ADGM financial services digitalization driving enterprise-grade RPA deployment. DEWA, Emirates NBD, and federal ministries are among the most referenced public deployments. Saudi Arabia follows through Vision 2030 digital government programs, SAMA-guided financial services automation, and Aramco's enterprise operations digitalization. South Africa anchors sub-Saharan activity through JSE-listed banking and insurance groups deploying AI-powered RPA for operational efficiency under SARB and FSCA guidance. Israel contributes through a concentrated fintech and enterprise software sector that both produces and consumes automation technology. Adoption across the broader region is at an earlier stage than other geographies, with demand concentrated in government, BFSI, and oil and gas operations. GCC sovereign investment programs and African Development Bank-backed digital government initiatives are expected to sustain double-digit growth through 2030.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software & Platforms

- Services (Implementation, Managed Automation, Consulting, Training)

By Technology

- Machine Learning & Natural Language Processing

- Computer Vision & Intelligent Document Processing

- Generative AI & LLM Agents (Agentic Automation)

- Process Mining & Task Mining

By Deployment Mode

- Cloud

- On-Premise

- Hybrid

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Vertical

- BFSI

- Healthcare

- Manufacturing

- Retail & E-commerce

- IT & Telecommunications

- Government

- Others (Energy, Education, Logistics)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.40 B |

| Forecast Revenue (2034) | USD 48.50 B |

| CAGR (2025-2034) | 21.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Software & Platforms, Services (Implementation, Managed Automation, Consulting, Training)), By Technology, (Machine Learning & Natural Language Processing, Computer Vision & Intelligent Document Processing, Generative AI & LLM Agents (Agentic Automation), Process Mining & Task Mining), By Deployment Mode, (Cloud, On-Premise, Hybrid), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By Vertical, (BFSI, Healthcare, Manufacturing, Retail & E-commerce, IT & Telecommunications, Government, Others (Energy, Education, Logistics)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | UIPATH, INC., AUTOMATION ANYWHERE, INC., MICROSOFT CORPORATION, SS&C BLUE PRISM, SAP SE, NICE LTD., PEGASYSTEMS INC., CELONIS SE, WORKFUSION, INC., APPIAN CORPORATION, SALESFORCE (MULESOFT), IBM CORPORATION (WATSONX ORCHESTRATE), KOFAX (TUNGSTEN AUTOMATION), HYLAND SOFTWARE, EDGEVERVE SYSTEMS (INFOSYS), LAIYE, ELECTRONEEK, SERVICENOW, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Machine Learning & NLP, Computer Vision, Intelligent Document Processing, Generative AI & LLM Agents, Process Mining & Task Mining), By Deployment Mode (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By Vertical (BFSI, Healthcare, Manufacturing, Retail, IT & Telecom, Government) Industry Trends & Forecast 2026-2034")

, By Technology (Machine Learning & NLP, Computer Vision, Intelligent Document Processing, Generative AI & LLM Agents, Process Mining & Task Mining), By Deployment Mode (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By Vertical (BFSI, Healthcare, Manufacturing, Retail, IT & Telecom, Government) Industry Trends & Forecast 2026-2034")

, By Technology (Machine Learning & NLP, Computer Vision, Intelligent Document Processing, Generative AI & LLM Agents, Process Mining & Task Mining), By Deployment Mode (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By Vertical (BFSI, Healthcare, Manufacturing, Retail, IT & Telecom, Government) Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the AI-Powered Robotic Process Automation Market?

The Global AI-Powered Robotic Process Automation Market was valued at USD 6.91 Billion in 2024 and is projected to reach USD 48.50 Billion by 2034, growing at a CAGR of 21.5% from 2026 to 2034. Growth is driven by increasing adoption of intelligent automation, hyperautomation initiatives, AI-enhanced workflow optimization, machine learning, natural language processing (NLP), generative AI, and intelligent document processing across banking, healthcare, manufacturing, retail, and other industries worldwide.

Who are the major players in the AI-Powered Robotic Process Automation Market?

UIPATH, INC., AUTOMATION ANYWHERE, INC., MICROSOFT CORPORATION, SS&C BLUE PRISM, SAP SE, NICE LTD., PEGASYSTEMS INC., CELONIS SE, WORKFUSION, INC., APPIAN CORPORATION, SALESFORCE (MULESOFT), IBM CORPORATION (WATSONX ORCHESTRATE), KOFAX (TUNGSTEN AUTOMATION), HYLAND SOFTWARE, EDGEVERVE SYSTEMS (INFOSYS), LAIYE, ELECTRONEEK, SERVICENOW, OTHERS

Which segments covered the AI-Powered Robotic Process Automation Market?

By Component, (Software & Platforms, Services (Implementation, Managed Automation, Consulting, Training)), By Technology, (Machine Learning & Natural Language Processing, Computer Vision & Intelligent Document Processing, Generative AI & LLM Agents (Agentic Automation), Process Mining & Task Mining), By Deployment Mode, (Cloud, On-Premise, Hybrid), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By Vertical, (BFSI, Healthcare, Manufacturing, Retail & E-commerce, IT & Telecommunications, Government, Others (Energy, Education, Logistics))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI-Powered Robotic Process Automation Market

Published Date : 29 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date