- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI-Powered Threat Intelligence Market Size, Share & Forecast | CAGR 15.6%

Global AI-Powered Threat Intelligence Market Size, Share, Growth Analysis By Offering (Solutions, Managed Threat Intelligence Services, Professional Services), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Vertical (BFSI, Government & Defense, Healthcare, IT & Telecommunications, Retail & E-Commerce, Energy & Utilities), Industry Trends, Competitive Landscape, AI Security Innovations & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 6.20 Billion | USD 22.80 Billion | 15.6% | North America, 42.8% |

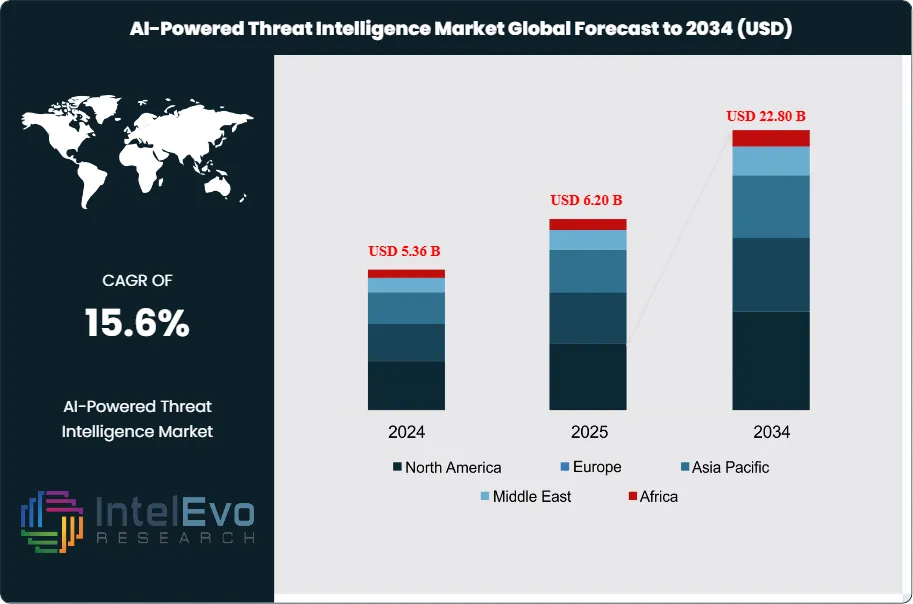

The AI-Powered Threat Intelligence Market was valued at approximately USD 5.36 Billion in 2024 and reached USD 6.20 Billion in 2025. The market is projected to grow to USD 22.80 Billion by 2034, expanding at a CAGR of 15.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 16.60 Billion over the analysis period, driven by the exponential increase in sophisticated cyberattacks, the chronic shortage of skilled cybersecurity analysts, and the accelerating adoption of artificial intelligence to process threat data at machine speed and scale.

Get More Information about this report -

Request Free Sample ReportAI-powered threat intelligence platforms ingest, correlate, and analyze indicator feeds, adversary tradecraft data, dark web intelligence, geopolitical signals, and vulnerability disclosures to produce prioritized, actionable intelligence for security operations centers, incident response teams, and executive risk management functions. The distinction from legacy threat intelligence feeds is substantive: AI-native platforms apply machine learning for automated indicator enrichment, natural language processing for dark web and open-source intelligence collection, and large language models for automated intelligence report generation — capabilities that reduce analyst processing time per threat from hours to minutes. Current market assessment shows that enterprise SOC teams using AI-powered threat intelligence platforms resolve 47% more high-priority alerts per analyst shift compared to teams relying on manual indicator feeds and static watchlists.

The AI-powered threat intelligence market operates at the intersection of regulatory pressure and operational necessity. The U.S. Securities and Exchange Commission's cyber incident disclosure rules (effective December 2023) require public companies to report material cybersecurity incidents within four business days, creating urgent demand for threat intelligence capabilities that can determine materiality rapidly. The EU's NIS2 Directive, effective October 2024, imposes mandatory threat intelligence sharing obligations on essential and important entities across 18 critical sectors, directly expanding the addressable market for structured AI-powered intelligence platforms in Europe. CISA's Known Exploited Vulnerabilities catalog and the NIST Cybersecurity Framework 2.0 both embed threat intelligence as a core program requirement, reinforcing institutional demand across U.S. federal and critical infrastructure operators.

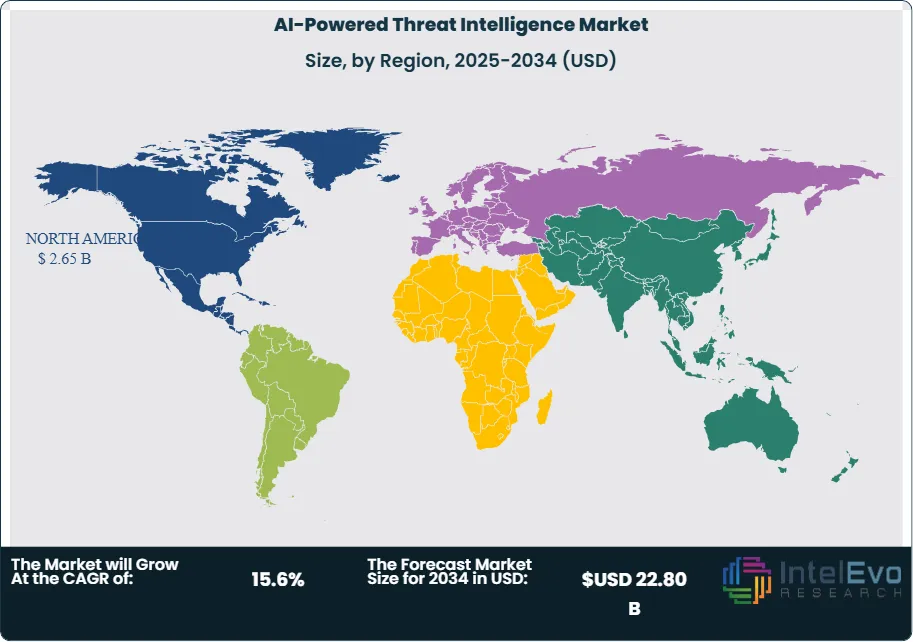

North America commands 42.8% of 2025 global market revenue, equivalent to approximately USD 2.65 Billion, anchored by the concentration of enterprise security buyers, U.S. federal procurement, and the primary vendor base. Europe holds 26.3% of 2025 share, driven by NIS2 compliance demand and the active threat environment targeting critical infrastructure across Germany, France, and the United Kingdom. Asia Pacific accounts for 20.4% of 2025 revenue and is the fastest-growing region as Singapore, Japan, and India expand national cyber defense capabilities. The AI-powered threat intelligence market is moderately consolidated, with CrowdStrike, Palo Alto Networks, Recorded Future, and Mandiant collectively holding approximately 52% of 2025 global revenue.

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Vertical (BFSI, Government & Defense, Healthcare, IT & Telecommunications, Retail & E-Commerce, Energy & Utilities), Industry Trends, Competitive Landscape, AI Security Innovations & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global AI-powered threat intelligence market was valued at USD 6.20 Billion in 2025 and is projected to reach USD 22.80 Billion by 2034, at a CAGR of 15.6% for 2026–2034.

- Segment Dominance: Solutions (software and platform licenses) account for 58.4% of 2025 market revenue, as enterprises prioritize platform-based AI threat intelligence over managed service contracts for greater control over intelligence workflows and data sovereignty.

- Segment Dominance: BFSI is the leading vertical end-user at 28.6% of 2025 market share, driven by the financial sector's high attack surface, mandatory threat sharing under financial regulators, and the direct financial impact of fraud and ransomware events on institutional risk exposure.

- Driver: The volume of ransomware and nation-state cyberattacks targeting enterprise and critical infrastructure grew 58% between 2022 and 2024, driving AI threat intelligence platform adoption; enterprise organizations using AI-powered TI report 47% higher alert resolution rates per analyst shift compared to manual feed-based approaches.

- Restraint: Skilled cybersecurity analyst shortage constrains market expansion; an estimated global deficit of 3.5 million cybersecurity professionals as of 2025 limits the human capacity needed to configure, tune, and act on AI threat intelligence outputs, particularly in mid-market and public sector organizations with constrained hiring budgets.

- Opportunity: Critical infrastructure sectors — energy, water, and transportation — represent an estimated USD 2.8 Billion incremental AI threat intelligence opportunity by 2030, as CISA directives and NIS2 mandates extend mandatory cyber threat intelligence programs to operational technology and industrial control system environments.

- Trend: Agentic AI threat hunting, where large language model-powered agents autonomously generate, validate, and prioritize threat intelligence without analyst direction, grew from 8% adoption in enterprise SOCs in 2023 to 31% in 2025, and is projected to reach 68% adoption by 2030 as Microsoft, CrowdStrike, and Palo Alto embed agentic capabilities into their dominant security platforms.

- Regional Analysis: North America leads the AI-powered threat intelligence market with 42.8% of 2025 global revenue, equivalent to approximately USD 2.65 Billion, driven by U.S. federal procurement, SEC disclosure rule compliance demand, and the headquarters concentration of leading AI cybersecurity vendors.

Competitive Landscape Overview

The AI-powered threat intelligence market is moderately consolidated, with CrowdStrike, Palo Alto Networks, Recorded Future (Mastercard), and Mandiant (Google Cloud) together accounting for approximately 52% of 2025 global revenue. Competition is platform-driven: vendors that successfully embed AI threat intelligence into broader security operations platforms — including SIEM, SOAR, EDR, and XDR — gain retention advantages over standalone threat intelligence products. M&A activity accelerated in 2023 and 2024, highlighted by Mastercard's USD 2.65 Billion acquisition of Recorded Future and Google's continued investment in Mandiant's intelligence capabilities. AI feature velocity — specifically the speed at which vendors deploy LLM-powered intelligence automation — has become the decisive competitive differentiator for enterprise contract renewals.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| CrowdStrike | USA | Leader | Falcon Intelligence (AI threat intel platform) | North America | Launched Falcon Adversary Intelligence Pro with generative AI threat actor profiling; expanded APAC SOC integrations (Feb 2025) |

| Palo Alto Networks | USA | Leader | Cortex XSOAR / AutoFocus TIM | North America | Integrated Precision AI threat intelligence layer into XSIAM 3.0; signed USD 330M DoD cybersecurity contract (Jan 2025) |

| Recorded Future (Mastercard) | USA | Challenger | Recorded Future Intelligence Cloud | Global | Mastercard completed full integration of Recorded Future; launched AI-native threat actor attribution engine (Apr 2025) |

| Mandiant (Google Cloud) | USA | Challenger | Mandiant Threat Intelligence / Advantage | North America | Integrated Mandiant TI into Google SecOps platform; released 2025 M-Trends report covering 1,800+ incident investigations (Mar 2025) |

| Microsoft (MSFT Security) | USA | Challenger | Microsoft Defender Threat Intelligence | Global | Launched Security Copilot 2.0 with agentic threat hunting and automated IOC enrichment across 78 trillion daily signals (Jun 2025) |

| IBM (X-Force) | USA | Niche Player | IBM X-Force Threat Intelligence Index | Global | Released X-Force Threat Intelligence Index 2025; expanded X-Force IR retainer services to 12 new APAC markets (Jan 2025) |

| Anomali | USA | Niche Player | Anomali ThreatStream / Lens | North America | Launched Anomali AI Copilot for automated threat hunting across MITRE ATT&CK framework; secured 6 new Fortune 500 clients (May 2025) |

| ThreatConnect | USA | Niche Player | ThreatConnect TI Operations Platform | North America | Released ThreatConnect 7.4 with LLM-powered intelligence summarization and automated playbook triggering (Sep 2025) |

| Flashpoint | USA | Niche Player | Flashpoint Ignite (deep/dark web TI) | North America | Acquired Echosec Systems to expand open-source intelligence collection; integrated geopolitical risk scoring (Oct 2025) |

| EclecticIQ | Netherlands | Niche Player | EclecticIQ Intelligence Center | Europe | Launched EclecticIQ Platform 3.5 with native MISP federation and automated TAXII 2.1 feed management (Jan 2026) |

By Offering

Solutions — encompassing software platforms, SaaS intelligence subscriptions, and API-based threat intelligence feeds — hold 58.4% of 2025 global AI-powered threat intelligence market revenue, equivalent to approximately USD 3.62 Billion. Enterprise buyers increasingly prefer platform-based intelligence solutions that integrate directly with their existing SIEM, SOAR, EDR, and XDR environments through native connectors and API integrations, enabling automated indicator enrichment and alert prioritization without manual analyst intervention. The shift from static indicator feeds to AI-enriched intelligence platforms — which apply machine learning for automatic false-positive filtering, threat actor attribution, and kill-chain mapping — has driven average contract values higher, with enterprise TI platform agreements now averaging USD 180,000 to USD 450,000 per year at large financial institutions and technology companies. Services — including managed threat intelligence, strategic intelligence briefings, incident response retainer programs, and intelligence program consulting — account for the remaining 41.6% of 2025 market revenue. Managed threat intelligence services are growing fastest within this category, as mid-market organizations that lack internal threat intelligence analyst capacity outsource the full intelligence lifecycle to specialized providers. The services segment is structurally important for vendors like Mandiant and IBM X-Force, whose intelligence programs are anchored by investigative expertise and proprietary telemetry from incident response engagements.

By Deployment Mode

Cloud-based and SaaS deployment dominates the AI-powered threat intelligence market with 52.3% of 2025 global revenue. Cloud-native deployment enables continuous model retraining on the latest threat telemetry, real-time indicator sharing across customer environments, and elastic compute scaling for high-volume intelligence processing — capabilities that on-premise architectures cannot match without substantial infrastructure investment. CrowdStrike, Recorded Future, and Anomali operate fully cloud-native intelligence platforms, and the shift toward multi-tenant intelligence clouds has compressed per-customer operating costs while enabling the sharing of anonymized threat signals across the full customer base to improve collective detection accuracy. On-premise deployment retains 31.4% of 2025 market share, concentrated among government agencies, defense contractors, and regulated financial institutions that require data residency compliance, classified network operation, or air-gapped deployment for the most sensitive intelligence workloads. The U.S. Intelligence Community's use of on-premise or private-cloud threat intelligence systems — including classified variants of commercial platforms — represents a significant and structurally sticky demand base. Hybrid deployment, which routes classified or sensitive intelligence workloads to on-premise infrastructure while processing open-source and commercial feeds on cloud platforms, accounts for 16.3% of 2025 revenue and is the fastest-growing deployment model among defense contractors, critical infrastructure operators, and multinational financial institutions.

By Vertical / End-User Industry

BFSI is the dominant vertical in the AI-powered threat intelligence market, generating 28.6% of 2025 global revenue. Financial institutions face the highest-density threat environment of any commercial sector, targeted by nation-state actors, organized cybercriminal groups, and opportunistic ransomware operators simultaneously. The Financial Services Information Sharing and Analysis Center mandates structured threat intelligence sharing among member institutions, and AI platforms that can automatically correlate FS-ISAC feeds with proprietary telemetry and dark web intelligence provide a material operational advantage. U.S. federal banking regulators, including the Office of the Comptroller of the Currency and the Federal Reserve, have strengthened expectations for threat intelligence program maturity in recent supervisory guidance cycles. Government and defense accounts for 22.4% of 2025 market share, driven by U.S. federal procurement under CISA's cybersecurity advisories, the Defense Information Systems Agency's zero-trust architecture mandates, and NATO member state cyber defense investment. Healthcare and life sciences holds 18.7% of 2025 revenue, propelled by the Health Insurance Portability and Accountability Act enforcement environment and the acute vulnerability of hospital networks to ransomware — the average cost of a healthcare data breach reached USD 10.9 Million in 2024. IT and telecommunications accounts for 14.2%, retail and e-commerce for 9.8%, and energy and utilities for 6.3% of 2025 market share.

Regional Analysis

North America

North America leads the global AI-powered threat intelligence market with 42.8% of 2025 revenue, approximately USD 2.65 Billion. The United States is the overwhelmingly dominant national market, driven by the world's highest enterprise cybersecurity spending intensity, the concentration of leading AI threat intelligence vendors, and a regulatory environment that has materially elevated demand since 2023. The SEC's cyber incident disclosure rules, which require public companies to disclose material cybersecurity incidents within four business days, have forced enterprise security teams to invest in threat intelligence capabilities that can assess breach materiality faster than human analysts working manually. CISA's Shields Up initiative and Binding Operational Directive 22-01 — which mandates federal agencies to remediate known exploited vulnerabilities within defined timelines — have embedded threat intelligence as a core operational requirement for U.S. federal civilian agency security programs. The U.S. Department of Defense's CMMC 2.0 framework, which extends cybersecurity requirements throughout the defense industrial base, is creating new mid-market demand for AI threat intelligence among defense contractors that previously relied on basic indicator feeds. Canada contributes meaningfully through the Canadian Centre for Cyber Security's threat intelligence sharing programs and the large financial institution base in Toronto that mirrors U.S. BFSI sector demand patterns. Mexico's growing financial services and manufacturing sectors are beginning to invest in structured threat intelligence as ransomware attacks on LATAM targets increased 72% between 2022 and 2024.

Europe

Europe holds 26.3% of 2025 global AI-powered threat intelligence market revenue, approximately USD 1.63 Billion. The region's regulatory environment is the most demanding globally for threat intelligence program requirements. The EU's NIS2 Directive, effective October 2024, mandates that essential and important entities across 18 critical sectors implement threat intelligence capabilities, report significant cyber incidents to national competent authorities within 24 hours, and participate in national information sharing networks — requirements that have directly stimulated investment in structured AI intelligence platforms across European critical infrastructure operators. Germany is the continent's largest single market, driven by the national cybersecurity authority BSI's active threat intelligence programs and the industrial sector's exposure to nation-state espionage targeting automotive and chemical manufacturing. The United Kingdom maintains a sophisticated threat intelligence market through the National Cyber Security Centre's threat intelligence sharing programs, GCHQ's commercial outreach, and the large financial services concentration in London. France's ANSSI has strengthened threat intelligence requirements for operators of vital importance, while the Netherlands hosts both ENISA's operations and EclecticIQ, the region's leading independent AI threat intelligence platform vendor. The European cybersecurity market benefits from coordinated investment through the European Cybersecurity Competence Centre, which has directed over EUR 2 Billion to cybersecurity capability development since 2021.

Asia Pacific

Asia Pacific accounts for 20.4% of 2025 global AI-powered threat intelligence market revenue, approximately USD 1.27 Billion, and is the fastest-growing major region with an estimated regional CAGR exceeding 18% through 2034. Japan is the most technically mature national market, with a well-established industrial cybersecurity culture and the National center of Incident readiness and Strategy for Cybersecurity operating structured threat intelligence sharing programs for critical infrastructure. The Japanese government's 2022 decision to quintuple cybersecurity spending by 2027 is directly driving enterprise and government AI threat intelligence adoption. Singapore is the regional hub for cybersecurity operations, hosting ASEAN government threat intelligence sharing programs and the regional headquarters of every major Western cybersecurity vendor; the Cyber Security Agency of Singapore's threat intelligence platforms serve as a model for ASEAN member state capability development. India is the highest-growth national market in the region, where the CERT-In mandatory incident reporting framework, the rapid expansion of domestic financial services digital infrastructure, and the IT services sector's global security responsibilities are collectively driving enterprise AI threat intelligence investment at greater than 20% annual growth. China maintains a substantial but largely domestically supplied threat intelligence market, with state-affiliated vendors serving government and critical infrastructure accounts under the Multi-Level Protection Scheme cybersecurity framework. South Korea's financial sector, telecommunications industry, and defense procurement programs sustain a sophisticated domestic demand base.

Latin America

Latin America represents 6.2% of 2025 global AI-powered threat intelligence market revenue, approximately USD 384 Million. Brazil is the dominant national market, driven by the financial services sector's aggressive ransomware targeting, the Lei Geral de Proteção de Dados data protection framework's incident reporting requirements, and the cybersecurity programs of major Brazilian banks — Itaú, Bradesco, and Banco do Brasil — which maintain some of the most sophisticated security operations in the region. Brazil's financial sector lost an estimated USD 800 Million to cybercrime in 2024, creating acute demand for threat intelligence capable of detecting fraud and intrusion patterns before financial losses materialize. Mexico's manufacturing sector — particularly automotive and electronics — has experienced significant operational technology ransomware attacks, driving investment in OT-aware threat intelligence among industrial operators. Colombia's growing financial technology sector and the cybersecurity programs of Bancolombia and Grupo Bancolombia represent the region's third-largest AI threat intelligence demand source. Regional growth is moderated by budget constraints at government and mid-market organizations, limited local AI cybersecurity expertise, and dependence on threat intelligence vendors headquartered in North America, which creates data sovereignty concerns for government buyers.

Middle East & Africa

The Middle East and Africa region accounts for 4.3% of 2025 global AI-powered threat intelligence market revenue, approximately USD 267 Million. The UAE is the most active single market, driven by the country's position as a high-profile cyber target and the government's proactive cybersecurity investment through the UAE Cybersecurity Council and the Signals Intelligence Agency. Dubai's financial free zone and the UAE's extensive digital government infrastructure create a large attack surface that has driven enterprise AI threat intelligence adoption across government, financial services, and critical infrastructure sectors. Saudi Arabia's Vision 2030 digitalization agenda has dramatically expanded the kingdom's cyber attack surface; the National Cybersecurity Authority's mandate covers both government and private sector critical infrastructure, and the authority's threat intelligence sharing programs are among the most structured in the region. South Africa operates the continent's most developed cybersecurity market, with the Financial Sector Conduct Authority's growing cyber oversight and major financial institutions including Standard Bank and FirstRand investing in AI threat intelligence to address the country's high banking fraud rates. The broader African continent represents an early-stage but high-potential market, where AU Cyber Security Expert Group programs and international development bank investments in digital infrastructure are progressively expanding the threat surface and awareness necessary to drive threat intelligence adoption.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Solutions (Software & Platform)

- Services (Managed TI, Professional Services)

By Deployment Mode

- Cloud-Based / SaaS

- On-Premise

- Hybrid

By Vertical / End-User Industry

- BFSI (Banking, Financial Services & Insurance)

- Government & Defense

- Healthcare & Life Sciences

- IT & Telecommunications

- Retail & E-Commerce

- Energy & Utilities

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.20 B |

| Forecast Revenue (2034) | USD 22.80 B |

| CAGR (2025-2034) | 15.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Solutions (Software & Platform), Services (Managed TI, Professional Services)), By Deployment Mode, (Cloud-Based / SaaS, On-Premise, Hybrid), By Vertical / End-User Industry, (BFSI (Banking, Financial Services & Insurance), Government & Defense, Healthcare & Life Sciences, IT & Telecommunications, Retail & E-Commerce, Energy & Utilities) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CROWDSTRIKE, PALO ALTO NETWORKS, RECORDED FUTURE (MASTERCARD), MANDIANT (GOOGLE CLOUD), MICROSOFT SECURITY (X-FORCE / SECURITY COPILOT), IBM (X-FORCE THREAT INTELLIGENCE), ANOMALI, THREATCONNECT, FLASHPOINT, ECLECTICIQ, SECUREWORKS (TAEGIS THREAT INTELLIGENCE), CYWARE LABS, INTEL 471, DIGITAL SHADOWS (RELIAQUEST), SILOBREAKER, TEAM CYMRU, SOLARWINDS (SECURITY EVENT MANAGER), CYBEREASON, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Vertical (BFSI, Government & Defense, Healthcare, IT & Telecommunications, Retail & E-Commerce, Energy & Utilities), Industry Trends, Competitive Landscape, AI Security Innovations & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Vertical (BFSI, Government & Defense, Healthcare, IT & Telecommunications, Retail & E-Commerce, Energy & Utilities), Industry Trends, Competitive Landscape, AI Security Innovations & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Vertical (BFSI, Government & Defense, Healthcare, IT & Telecommunications, Retail & E-Commerce, Energy & Utilities), Industry Trends, Competitive Landscape, AI Security Innovations & Forecast 2026-2034")

Frequently Asked Questions

How big is the AI-Powered Threat Intelligence Market?

The Global AI-Powered Threat Intelligence Market was valued at USD 5.36 Billion in 2024 and is projected to reach USD 22.80 Billion by 2034, growing at a CAGR of 15.6% from 2026 to 2034, driven by rising cyber threats, increasing adoption of AI-driven security analytics, and growing demand for real-time threat detection and response solutions.

Who are the major players in the AI-Powered Threat Intelligence Market?

CROWDSTRIKE, PALO ALTO NETWORKS, RECORDED FUTURE (MASTERCARD), MANDIANT (GOOGLE CLOUD), MICROSOFT SECURITY (X-FORCE / SECURITY COPILOT), IBM (X-FORCE THREAT INTELLIGENCE), ANOMALI, THREATCONNECT, FLASHPOINT, ECLECTICIQ, SECUREWORKS (TAEGIS THREAT INTELLIGENCE), CYWARE LABS, INTEL 471, DIGITAL SHADOWS (RELIAQUEST), SILOBREAKER, TEAM CYMRU, SOLARWINDS (SECURITY EVENT MANAGER), CYBEREASON, Others

Which segments covered the AI-Powered Threat Intelligence Market?

By Offering, (Solutions (Software & Platform), Services (Managed TI, Professional Services)), By Deployment Mode, (Cloud-Based / SaaS, On-Premise, Hybrid), By Vertical / End-User Industry, (BFSI (Banking, Financial Services & Insurance), Government & Defense, Healthcare & Life Sciences, IT & Telecommunications, Retail & E-Commerce, Energy & Utilities)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI-Powered Threat Intelligence Market

Published Date : 08 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date