- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI-Powered Video Surveillance Analytics Market Size, Share | CAGR 18.7%

Global AI-Powered Video Surveillance Analytics Market Size, Share, Analysis By Offering (Hardware, Software, Services), By Deployment (Cloud, On-Premises, Hybrid), By Use Case (Intrusion Detection, Vehicle Identification & License Plate Recognition, Facial Recognition, People Counting & Crowd Density, Behavior Analysis), By End-User (Government & Public Safety, Commercial, Transportation & Logistics, Critical Infrastructure, Residential) Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 8.25 Billion | USD 38.50 Billion | 18.7% | North America, 39.0% |

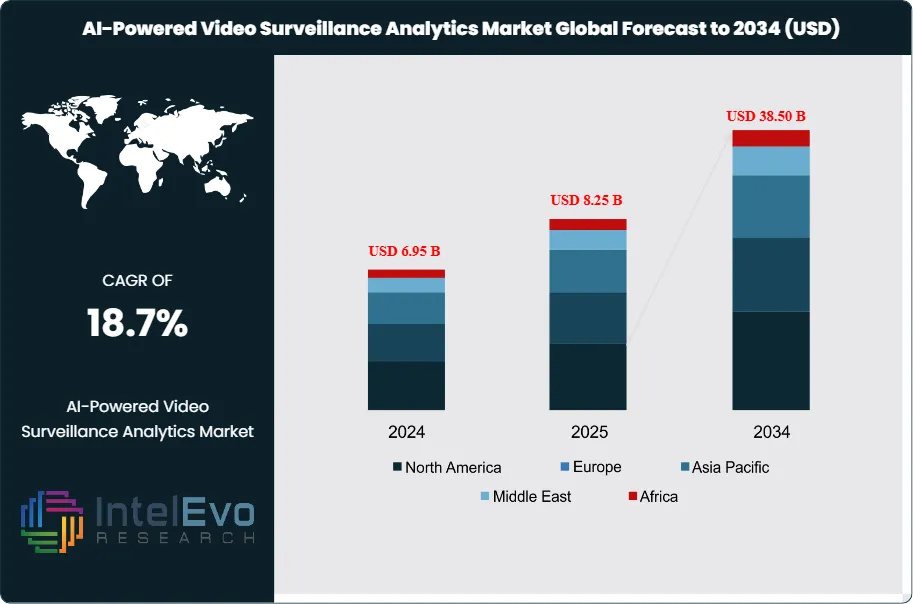

The AI-Powered Video Surveillance Analytics Market was valued at approximately USD 6.95 Billion in 2024 and reached USD 8.25 Billion in 2025. The market is projected to grow to USD 38.50 Billion by 2034, expanding at a CAGR of 18.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 30.25 Billion over the analysis period. The AI-powered video surveillance analytics market is defined as the integrated stack of cameras, edge compute devices, video management software, and deep-learning analytics that apply computer vision, object detection, facial recognition, license plate recognition, behavior analysis, and anomaly detection to live and recorded video streams for security, operational, and business intelligence purposes.

Get More Information about this report -

Request Free Sample ReportScope includes AI-enabled IP cameras with embedded neural processing units, cloud-native video management systems, edge analytics appliances running on NVIDIA Jetson and Metropolis platforms, and algorithmic offerings spanning perimeter intrusion detection, crowd density analytics, personal protective equipment monitoring, and automated license plate reading. Traditional analog CCTV systems without any AI inference capability, consumer-grade doorbell cameras without cloud analytics, and pure-play cybersecurity video-content analysis are excluded. The market is anchored to a parent video surveillance industry estimated at USD 38.7 Billion in 2025, of which AI-powered analytics penetration reached approximately 21% and is projected to exceed 55% by 2034.

Regulatory frameworks are the decisive catalyst in 2025. The EU AI Act prohibitions under Article 5 became enforceable on February 2, 2025, restricting real-time remote biometric identification in public spaces for law enforcement with narrow exceptions, banning untargeted scraping of facial images from the internet or CCTV footage, and outlawing emotion recognition in workplaces and educational institutions. High-risk AI system obligations become enforceable on August 2, 2026. In the United States, the NDAA Section 889 continues to ban federal procurement of Hikvision and Dahua equipment, shifting US federal spend to NDAA-compliant vendors including Axis Communications, Avigilon, Hanwha Vision, and Verkada.

Technology maturation is collapsing inference costs. Edge AI accelerators such as the NVIDIA Jetson Orin and Ambarella CV3 series deliver up to 275 TOPS at sub-30 W power envelopes, enabling real-time multi-stream inference directly on cameras. Vision-language models (VLMs) and generative AI search capabilities compressed typical forensic investigation time from hours to minutes. NVIDIA Metropolis, combined with the Video Search and Summarization (VSS) blueprint announced during GTC Paris 2025, is accelerating development of visual AI agents across more than 50 NVIDIA partner companies including Avigilon, Dahua, Hanwha Vision, Hikvision, and Milestone Systems.

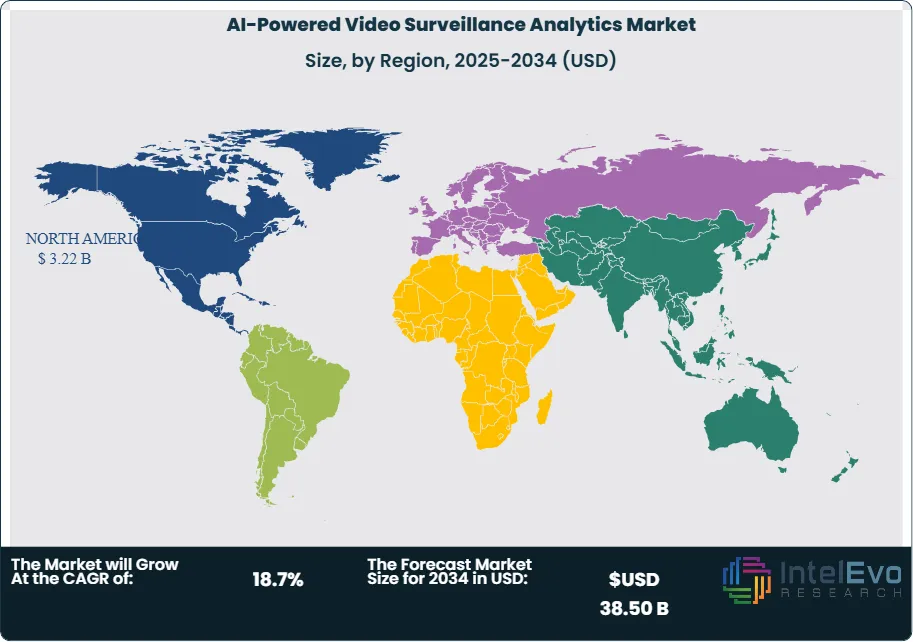

Regional concentration is pronounced. North America held 39.0% of the AI-powered video surveillance analytics market in 2025 at approximately USD 3.22 Billion, supported by smart city deployments in New York, Los Angeles, and Chicago and by Walmart, Target, and Costco retail analytics mandates. Asia Pacific held 30.0% share at USD 2.48 Billion, led by China's Skynet national surveillance program and Hikvision's domestic dominance. Europe held 21.0% share at USD 1.73 Billion, anchored by EU AI Act compliance spend and German, French, and UK public-safety deployments.

Supply-chain dynamics are consolidating around vertically integrated platform providers. Motorola Solutions expanded its Avigilon and Pelco portfolios with the March 2025 acquisition of Theatro for USD 173 Million and the August 2025 USD 4.4 Billion Silvus Technologies acquisition. Hikvision and Dahua maintain scale leadership in hardware, while Verkada, Genetec, and Milestone Systems lead cloud-native VMS adoption. NVIDIA's GPU and software ecosystem provides the horizontal compute layer for most high-end deployments, creating structural dependencies across competitor portfolios.

Forward to 2034, three forces will shape market direction. Vision-language model integration will replace keyword-based forensic search with natural-language queries across petabyte-scale video archives. Sovereign AI mandates in the EU, UAE, Saudi Arabia, and India will favor domestically trained models and NDAA-compliant or equivalent regional supply chains. Convergence between physical security, cybersecurity, and operational analytics will drive smart-camera spend beyond security use cases into manufacturing quality control, retail loss prevention, and smart-city traffic management.

, By Deployment (Cloud, On-Premises, Hybrid), By Use Case (Intrusion Detection, Vehicle Identification & License Plate Recognition, Facial Recognition, People Counting & Crowd Density, Behavior Analysis), By End-User (Government & Public Safety, Commercial, Transportation & Logistics, Critical Infrastructure, Residential) Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global AI-powered video surveillance analytics market expanded from USD 8.25 Billion in 2025 and is projected to reach USD 38.50 Billion by 2034, delivering a CAGR of 18.7% across the forecast period.

- Segment Dominance (Offering): Hardware led with 46.0% share in 2025, approximately USD 3.80 Billion, anchored by AI-enabled IP cameras, network video recorders, and edge compute appliances from Hikvision, Dahua, Axis, and Hanwha Vision.

- Segment Dominance (Deployment): Cloud deployments captured 60.2% share in 2025, equal to USD 4.97 Billion, as video surveillance as a service (VSaaS) replaced capex-heavy on-premises installations at mid-market scale.

- Driver: Smart city programs across more than 1,000 cities globally and public-safety compliance mandates under the FBI Next Generation Identification system, UK College of Policing guidance, and China's GB/T standards compelled multi-billion-dollar analytics deployments through 2025.

- Restraint: EU AI Act Article 5 prohibitions effective February 2, 2025, combined with fragmented US state biometric privacy laws in Illinois BIPA, Texas CUBI, and Washington, add compliance costs of USD 150,000-500,000 per enterprise deployment.

- Opportunity: Vision-language model and generative AI integration into forensic search, summarization, and natural-language querying addresses an estimated USD 4.8 Billion incremental opportunity by 2034 across retail, transportation, and critical infrastructure verticals.

- Trend: Edge AI inference reached 21% of global analytics workloads in 2025 and is projected to exceed 48% by 2034, shifting compute from centralized servers to NVIDIA Jetson, Ambarella, and Hailo accelerators embedded directly inside cameras.

- Regional Analysis: North America dominated with 39.0% share, generating USD 3.22 Billion in 2025, driven by NDAA Section 889 compliance spend, Motorola Solutions' Avigilon platform expansion, and retail AI analytics rollouts at Walmart, Target, and Kroger.

Key Insights Summary

- The EU AI Act prohibitions under Article 5 became enforceable on February 2, 2025, restricting real-time remote biometric identification in public spaces with narrow law-enforcement exceptions and banning untargeted CCTV facial-image scraping across all 27 member states.

- EU AI Act high-risk AI system obligations become enforceable on August 2, 2026, with fines up to EUR 15 Million or 3% of global turnover for non-compliant facial recognition and biometric categorization deployments.

- NVIDIA announced the Omniverse Blueprint for Smart City AI at GTC Paris in June 2025, combining NVIDIA Cosmos, NeMo, and Metropolis platforms with Video Search and Summarization blueprints, deployed with partners including Milestone Systems, Bentley, Linker Vision, and SNCF Gares&Connexions.

- Motorola Solutions completed the USD 4.4 Billion acquisition of Silvus Technologies in August 2025 and acquired Theatro for USD 173 Million on March 6, 2025, extending its Avigilon video surveillance portfolio with AI voice and mesh networking capabilities.

- Milestone Systems merged with Arcules in February 2025 to unify on-premises XProtect with cloud VSaaS under one brand, addressing hybrid-deployment demand across multi-site enterprise customers.

- Hikvision unveiled AIoT scenario-based solutions at Intersec Dubai in January 2025, showcasing multi-sensor fusion, thermal-visible-radar integration, and 5G connectivity across critical infrastructure use cases.

- NEC Corporation introduced in January 2025 a generative AI system that integrates video analysis with large language models to deliver personalized, automated worker guidance by identifying discrepancies between ideal and actual task movements.

Competitive Landscape Overview

The AI-powered video surveillance analytics market is moderately consolidated, with the top four players accounting for approximately 48-55% of combined global revenue in 2025. Competition centers on AI model accuracy, edge compute throughput, NDAA Section 889 compliance, and cloud-native VMS capabilities rather than hardware price alone. Hikvision, Dahua, Motorola Solutions (Avigilon), and Axis Communications each occupy distinct strategic positions: vertically integrated hardware-and-analytics scale, cost-competitive hardware with AIoT integration, NDAA-compliant enterprise platforms, and edge-AI open-camera ecosystems. Competitive evolution accelerated in 2025 with Milestone Systems and Arcules merging in February, Motorola Solutions acquiring Theatro in March and Silvus Technologies in August, and generative AI capabilities launching across Avigilon, Verkada, and Genetec platforms. Flock Safety raised USD 275 Million in March 2025 to build US manufacturing lines and lift annual recurring revenue beyond USD 300 Million.

Competitive Landscape Matrix

| Company | HQ | Position | Key Offering | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Hangzhou Hikvision Digital Technology Co., Ltd. | China | Leader | HikCentral VMS, AI cameras, AcuSense, DarkFighter | Asia Pacific, EMEA | AIoT scenario solutions at Intersec Dubai, Jan 2025 |

| Motorola Solutions, Inc. (Avigilon) | USA | Leader | Avigilon Unity, Appearance Search, Pelco VideoXpert | North America, Europe | USD 4.4B Silvus acquisition completed Aug 2025 |

| Zhejiang Dahua Technology Co., Ltd. | China | Leader | WizMind AI series, DSS Pro VMS, thermal imaging | Asia Pacific, MEA, LatAm | Ongoing AI-camera portfolio refresh in 2025 |

| Axis Communications AB (Canon Group) | Sweden | Leader | ACAP analytics platform, AXIS Object Analytics, ARTPEC-9 chip | Europe, North America | ARTPEC-9 edge AI chip rollout across 2025 camera lines |

| Milestone Systems A/S (Canon Group) | Denmark | Challenger | XProtect VMS, Project Hafnia anonymized training data | Global, Europe-led | Merged with Arcules Feb 2025 for hybrid cloud offering |

| Hanwha Vision Co., Ltd. | South Korea | Challenger | WISENET AI cameras, Wisenet WAVE VMS | North America, Asia | Expanded AI camera line with open-platform analytics, 2025 |

| Genetec Inc. | Canada | Challenger | Security Center, AutoVu LPR, Mission Control | North America, Europe | Expanded cloud-native analytics integrations through 2025 |

| Verkada Inc. | USA | Challenger | Cloud-native AI cameras, Command platform, NDAA-compliant hardware | North America | Generative AI search and natural-language queries launched 2025 |

| Honeywell International Inc. | USA | Niche Player | MAXPRO VMS, 70 Series AI cameras | Global, industrial and infrastructure | AI camera adoption in Bengaluru smart city program, 2025 |

| NEC Corporation | Japan | Niche Player | NeoFace biometric platform, generative AI video analysis | Asia Pacific, global | Generative AI worker-guidance system launched Jan 2025 |

By Offering

Hardware held the largest offering share at 46.0% in 2025, equal to USD 3.80 Billion. AI-enabled IP cameras, network video recorders, edge compute appliances, and thermal-visible-radar multi-sensor modules comprise the segment. Hikvision, Dahua, Axis Communications, and Hanwha Vision lead hardware shipments, with embedded NVIDIA Jetson, Ambarella CV3, and Hailo-8 accelerators delivering up to 275 TOPS of edge inference throughput. Multi-sensor fusion combining visible-light, thermal, and radar inside a single enclosure reached commercial scale in 2025, freeing central servers for forensic analytics. Hardware remains revenue-dominant because cameras are the physical prerequisite for any analytics workflow, yet unit economics are compressing as edge AI features transition from premium to mid-tier SKUs.

Software captured 38.0% share at USD 3.14 Billion in 2025 and is the fastest-growing offering category through 2034. Video management systems (VMS) including Milestone XProtect, Genetec Security Center, Avigilon Unity, and Verkada Command embed real-time analytics, automated event triage, and cloud connectors. Deep-learning models for intrusion detection, facial recognition, license plate recognition, and behavior analysis are increasingly licensed as subscriptions. NVIDIA DeepStream, TAO Toolkit, and Metropolis VSS blueprints provide the horizontal software foundation used by many vendors. Services contributed 16.0% share at USD 1.32 Billion, covering deployment, integration, customization, and managed video monitoring services provided by system integrators and VSaaS operators.

By Deployment

Cloud deployment dominated with 60.2% share in 2025 at USD 4.97 Billion. Video surveillance as a service (VSaaS) adoption accelerated because cloud-native architectures reduce capital expenditure, simplify multi-site management, and support rapid model updates. Verkada, Eagle Eye Networks, Rhombus, and Cloudastructure lead pure-cloud deployments, while Genetec, Milestone Systems, and Avigilon offer hybrid models through Genetec Stratocast, Milestone-Arcules, and Avigilon Alta. According to Eagle Eye Networks data, 56% of cloud-based video cameras used cloud-only recording in 2023, with the remainder employing a cloud-and-on-premises combination. On-Premises held 29.8% share at USD 2.46 Billion, preferred by government, critical infrastructure, and regulated industries that internalize data sovereignty. Hybrid deployments held 10.0% at USD 0.83 Billion and are projected as the fastest-growing sub-segment through 2034.

By Use Case

Intrusion detection led use-case segmentation with 22.0% share in 2025 at USD 1.82 Billion, anchored by perimeter protection across commercial sites, data centers, utilities, and residential gated communities. Vehicle identification and license plate recognition (LPR) held 20.0% at USD 1.65 Billion, with AutoVu, Avigilon, Flock Safety, and Motorola Solutions VaaS platforms supporting law enforcement, parking, and tolling deployments. Facial recognition held 18.0% at USD 1.49 Billion, concentrated in airports, border control, and retail loss prevention where EU AI Act high-risk compliance obligations become enforceable from August 2, 2026. People counting and crowd density analytics held 14.0% at USD 1.16 Billion, behavior analysis at 12.0% at USD 0.99 Billion, and other use cases including fire detection, PPE compliance, and wrong-way detection accounted for 14.0% at USD 1.16 Billion.

By End-User

Government and public safety was the largest vertical at 32.0% share in 2025 (USD 2.64 Billion), anchored by smart city programs in New York, Los Angeles, Chicago, London, Paris, Beijing, Shanghai, Singapore, and Dubai. FBI Next Generation Identification, UK College of Policing guidance, and China's GB/T surveillance standards drive federal and municipal procurement. Commercial enterprises held 28.0% share (USD 2.31 Billion) across retail, BFSI, and hospitality, where Walmart, Target, Kroger, and Costco deploy AI analytics for loss prevention and operations. Transportation and logistics accounted for 14.0% (USD 1.16 Billion), covering airports, seaports, railways, and logistics yards. Critical infrastructure including airports, utilities, and energy facilities contributed 11.0% (USD 0.91 Billion), residential at 9.0% (USD 0.74 Billion), and healthcare, education, and industrial manufacturing collectively at 6.0% (USD 0.49 Billion).

Regional Analysis

North America

North America held the largest share of the AI-powered video surveillance analytics market at 39.0% in 2025, generating USD 3.22 Billion. The United States anchored regional leadership through NDAA Section 889 procurement rules that bar federal agencies from acquiring Hikvision and Dahua equipment, steering public spend toward Axis Communications, Avigilon, Hanwha Vision, Verkada, and Genetec. State-level biometric privacy laws including Illinois BIPA, Texas CUBI, and Washington HB 1493 shape enterprise deployment design. Motorola Solutions completed its USD 4.4 Billion Silvus Technologies acquisition in August 2025. Canada contributed through Genetec's global Security Center platform, while Mexico advanced smart-city deployments in Mexico City, Guadalajara, and Monterrey.

Asia Pacific

Asia Pacific accounted for 30.0% of global revenue in 2025 at approximately USD 2.48 Billion, with growth led by China, Japan, India, and South Korea. China is the largest national sub-market, driven by the Skynet surveillance program, GB/T national standards, and Hikvision's domestic dominance across more than 180 countries. Japan advanced through NEC Corporation's NeoFace platform and January 2025 generative AI video analysis launch. India accelerated with Staqu Technologies' JARVIS platform installed at the Ayodhya Ram Mandir on January 22, 2025, plus Bengaluru's Honeywell-powered smart city AI surveillance network. South Korea's Hanwha Vision expanded its WISENET AI camera line, and Singapore's Safe City program led regional smart-city adoption.

Europe

Europe held 21.0% share in 2025, equal to USD 1.73 Billion. EU AI Act Article 5 prohibitions became enforceable on February 2, 2025, restricting real-time remote biometric identification in public spaces and banning untargeted CCTV facial-image scraping. High-risk AI system obligations take effect on August 2, 2026, with fines up to EUR 15 Million or 3% of turnover. Germany advanced through Dallmeier, Bosch Security, and Siemens smart-city pilots. France continues the Paris 2024 Olympics legacy video analytics deployments under the Loi JO experimental framework. The United Kingdom expanded Metropolitan Police live facial recognition trials into South London. Milestone Systems launched Project Hafnia with NVIDIA in 2025 to build anonymized, ethically sourced video data platforms for EU cities.

Middle East & Africa

Middle East & Africa represented 6.5% of the global market at USD 0.54 Billion in 2025, with the fastest regional growth rate at a projected 22.5% CAGR through 2034. The UAE Ministry of Interior, Dubai Police, and Saudi Arabia's Mawhiba smart city programs drive demand. Hikvision's Intersec Dubai January 2025 showcase featured AIoT multi-sensor fusion for Gulf infrastructure. NEOM in Saudi Arabia deployed large-scale AI video analytics under Vision 2030. Qatar extended infrastructure from the FIFA World Cup 2022 into permanent smart-city monitoring. Latin America contributed 3.5% share at USD 0.29 Billion, led by Brazil's public-safety deployments in São Paulo and Rio de Janeiro, Mexico's Guadalajara and CDMX programs, and Chile's Santiago municipal surveillance upgrades.

Country Analysis

United States:

The US AI-powered video surveillance analytics market reached USD 2.65 Billion in 2025 and is projected to grow at a CAGR of 18.2%, reaching approximately USD 12.20 Billion by 2034. Market depth is anchored by NDAA Section 889 procurement restrictions that block Hikvision and Dahua from federal contracts, steering over USD 1 Billion annually toward Avigilon, Axis, Hanwha Vision, Verkada, and Genetec. The FBI Next Generation Identification system, CBP biometric entry-exit, and TSA airport modernization programs drive federal demand. State-level biometric laws including Illinois Biometric Information Privacy Act and Texas Capture or Use of Biometric Identifier Act shape enterprise facial recognition deployment. Motorola Solutions' March 2025 Theatro acquisition and August 2025 Silvus Technologies acquisition extended its video surveillance platform, while Flock Safety raised USD 275 Million in March 2025 to scale US manufacturing.

China:

China's AI-powered video surveillance analytics market reached USD 1.45 Billion in 2025 and is projected to grow at a CAGR of 19.8% to approximately USD 7.35 Billion by 2034. The market is anchored by the Ministry of Public Security Skynet program, the GB/T 28181 national video surveillance interoperability standard, and widespread deployment across 600-plus cities. Hikvision retained domestic scale leadership with over USD 12.9 Billion in 2024 annual revenue, while Dahua Technology maintained USD 5.0 Billion. SenseTime, YITU Tech, CloudWalk Technology, and Megvii compete on facial recognition and behavior analysis algorithms. Hikvision showcased AIoT scenario-based solutions at Intersec Dubai in January 2025, and Chinese export growth into the Middle East, Africa, and Southeast Asia accelerated through 2025.

United Kingdom:

The UK AI-powered video surveillance analytics market reached USD 0.48 Billion in 2025 and is projected to grow at a CAGR of 17.5% to approximately USD 2.10 Billion by 2034. Expansion is driven by the Metropolitan Police Service live facial recognition deployments, which reportedly scanned approximately 1 million faces in 2025, and by permanent LFR camera installations planned in Croydon, South London. The College of Policing guidance, Biometrics and Forensics Ethics Group, and Surveillance Camera Commissioner shape enforcement. Post-Brexit the UK operates outside the EU AI Act but maintains adjacency through the UK GDPR and Data Protection Act. South Wales Police expanded live facial recognition trials to international sports events in 2025, and Welsh Government smart-city pilots advanced in Cardiff and Newport.

India:

India's AI-powered video surveillance analytics market reached USD 0.38 Billion in 2025 and is projected to grow at a CAGR of 22.3% to approximately USD 2.35 Billion by 2034, the fastest major-country CAGR. Demand is driven by the Smart Cities Mission covering 100 cities under the Ministry of Housing and Urban Affairs and by CCTV-based Crime & Criminal Tracking Network & Systems (CCTNS) deployments. Staqu Technologies' JARVIS AI platform was installed at the Ayodhya Ram Mandir on January 22, 2025. Bengaluru's AI-powered surveillance network deployed Honeywell 70 Series AI cameras with facial recognition, license plate recognition, and smart motion detection. AllGoVision Technologies, Videonetics, and Matrix Comsec expanded domestic AI analytics capacity, while Digital Personal Data Protection Act compliance shapes deployment design.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Hardware

- Software

- Services

By Deployment

- Cloud

- On-Premises

- Hybrid

By Use Case

- Intrusion Detection

- Vehicle Identification and License Plate Recognition

- Facial Recognition

- People Counting and Crowd Density

- Behavior Analysis

- Other Use Cases

By End-User

- Government and Public Safety

- Commercial (Retail, BFSI, Hospitality)

- Transportation and Logistics

- Critical Infrastructure

- Residential

- Other End-Users

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.25 B |

| Forecast Revenue (2034) | USD 38.50 B |

| CAGR (2025-2034) | 18.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Hardware, Software, Services), By Deployment, (Cloud, On-Premises, Hybrid), By Use Case, (Intrusion Detection, Vehicle Identification and License Plate Recognition, Facial Recognition, People Counting and Crowd Density, Behavior Analysis, Other Use Cases), By End-User, (Government and Public Safety, Commercial (Retail, BFSI, Hospitality), Transportation and Logistics, Critical Infrastructure, Residential, Other End-Users) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HANGZHOU HIKVISION DIGITAL TECHNOLOGY CO., LTD., MOTOROLA SOLUTIONS, INC. (AVIGILON), ZHEJIANG DAHUA TECHNOLOGY CO., LTD., AXIS COMMUNICATIONS AB (CANON GROUP), MILESTONE SYSTEMS A/S (CANON GROUP), HANWHA VISION CO., LTD., GENETEC INC., VERKADA INC., HONEYWELL INTERNATIONAL INC., NEC CORPORATION, BOSCH SECURITY SYSTEMS GMBH, SENSETIME GROUP INC., YITU TECHNOLOGY, CLOUDWALK TECHNOLOGY CO., LTD., I-PRO CO., LTD., FLOCK SAFETY, INC., AGENT VIDEO INTELLIGENCE LTD., EAGLE EYE NETWORKS, NVIDIA CORPORATION, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud, On-Premises, Hybrid), By Use Case (Intrusion Detection, Vehicle Identification & License Plate Recognition, Facial Recognition, People Counting & Crowd Density, Behavior Analysis), By End-User (Government & Public Safety, Commercial, Transportation & Logistics, Critical Infrastructure, Residential) Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Deployment (Cloud, On-Premises, Hybrid), By Use Case (Intrusion Detection, Vehicle Identification & License Plate Recognition, Facial Recognition, People Counting & Crowd Density, Behavior Analysis), By End-User (Government & Public Safety, Commercial, Transportation & Logistics, Critical Infrastructure, Residential) Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Deployment (Cloud, On-Premises, Hybrid), By Use Case (Intrusion Detection, Vehicle Identification & License Plate Recognition, Facial Recognition, People Counting & Crowd Density, Behavior Analysis), By End-User (Government & Public Safety, Commercial, Transportation & Logistics, Critical Infrastructure, Residential) Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the AI-Powered Video Surveillance Analytics Market?

The Global AI-Powered Video Surveillance Analytics Market was valued at USD 6.95 Billion in 2024 and is projected to reach USD 38.50 Billion by 2034, growing at a CAGR of 18.7% from 2026 to 2034. Growth is driven by increasing adoption of AI-enabled surveillance systems, real-time threat detection, facial recognition, behavior analytics, computer vision technologies, smart city initiatives, and cloud-based video analytics platforms across government, transportation, retail, healthcare, and industrial sectors worldwide.

Who are the major players in the AI-Powered Video Surveillance Analytics Market?

HANGZHOU HIKVISION DIGITAL TECHNOLOGY CO., LTD., MOTOROLA SOLUTIONS, INC. (AVIGILON), ZHEJIANG DAHUA TECHNOLOGY CO., LTD., AXIS COMMUNICATIONS AB (CANON GROUP), MILESTONE SYSTEMS A/S (CANON GROUP), HANWHA VISION CO., LTD., GENETEC INC., VERKADA INC., HONEYWELL INTERNATIONAL INC., NEC CORPORATION, BOSCH SECURITY SYSTEMS GMBH, SENSETIME GROUP INC., YITU TECHNOLOGY, CLOUDWALK TECHNOLOGY CO., LTD., I-PRO CO., LTD., FLOCK SAFETY, INC., AGENT VIDEO INTELLIGENCE LTD., EAGLE EYE NETWORKS, NVIDIA CORPORATION, Others

Which segments covered the AI-Powered Video Surveillance Analytics Market?

By Offering, (Hardware, Software, Services), By Deployment, (Cloud, On-Premises, Hybrid), By Use Case, (Intrusion Detection, Vehicle Identification and License Plate Recognition, Facial Recognition, People Counting and Crowd Density, Behavior Analysis, Other Use Cases), By End-User, (Government and Public Safety, Commercial (Retail, BFSI, Hospitality), Transportation and Logistics, Critical Infrastructure, Residential, Other End-Users)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI-Powered Video Surveillance Analytics Market

Published Date : 01 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date