AI Server Market Size, Growth, Share & Forecast | CAGR of 31.57%

Global AI Server Market Size, Share, Analysis Report By Processor Type (GPU-based Servers, ASIC-based Servers , FPGA-based Servers), Server Form Factor (Blade Servers, Rack-mounted Servers, Tower Servers), End-User Industry (Healthcare, IT & Telecommunications, Automotive, Healthcare, Financial Services, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034

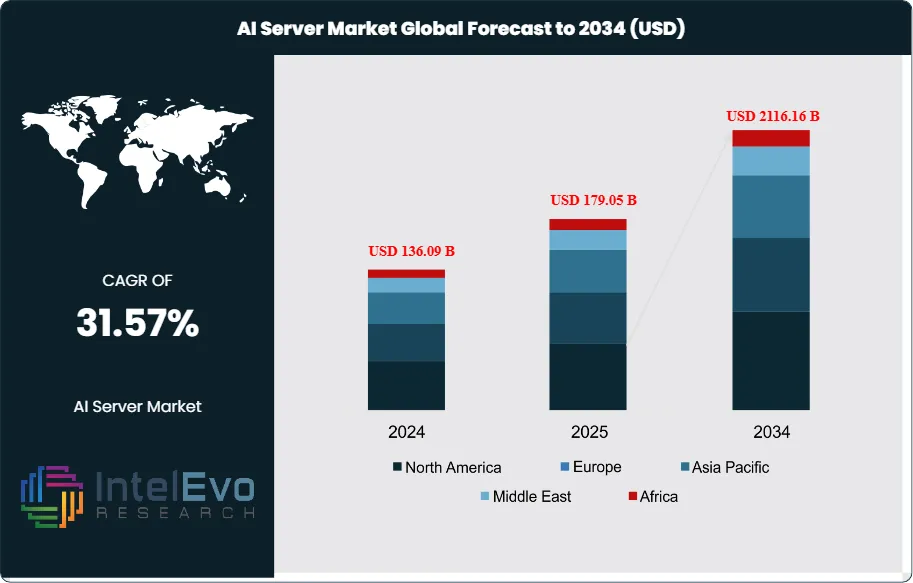

The AI Server Market size is expected to be worth around USD 2116.16 Billion by 2034, from USD 136.09 Billion in 2024, growing at a CAGR of 31.57% during the forecast period from 2024 to 2034. The AI Server Market encompasses specialized computing hardware designed to accelerate artificial intelligence workloads, including machine learning training, deep learning inference, and neural network processing. These servers integrate advanced processors such as GPUs, specialized AI chips, and high-performance computing components optimized for parallel processing and complex mathematical operations required by AI applications across various industries and deployment scenarios.

The market is experiencing unprecedented growth driven by the rapid adoption of generative AI, large language models, and enterprise AI applications. Organizations across industries are investing heavily in AI infrastructure to support digital transformation initiatives, automate business processes, and develop intelligent applications. The increasing complexity of AI models and the need for real-time processing capabilities are driving demand for specialized server hardware that can handle massive computational workloads efficiently.

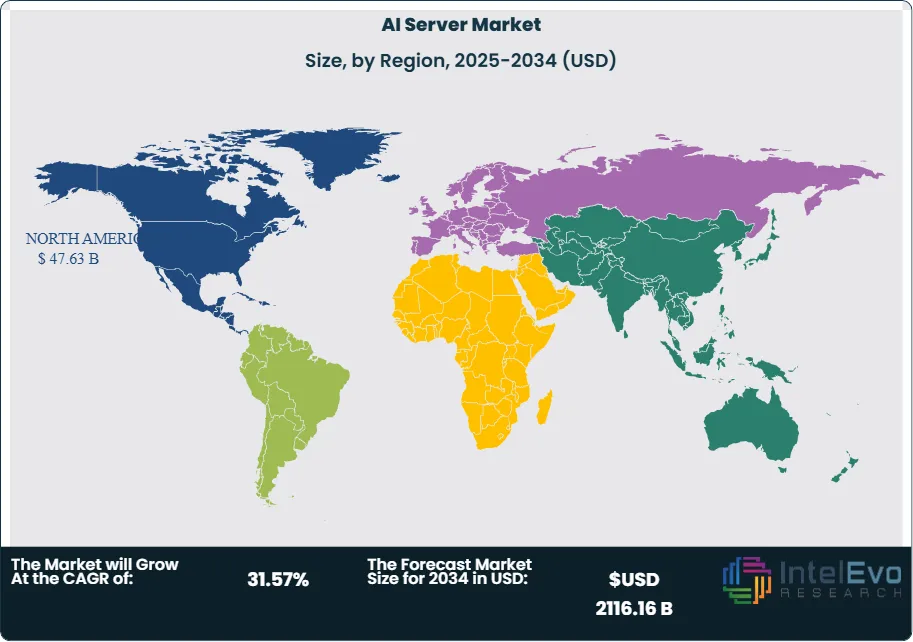

North America leads the global AI server market with dominant market share, driven by major technology companies, cloud service providers, and early AI adoption across enterprises. The region benefits from significant investments in AI research, extensive data center infrastructure, and the presence of leading AI technology companies. Asia-Pacific represents the fastest-growing market, fueled by government AI initiatives, manufacturing digitization, and expanding cloud infrastructure across emerging economies.

The pandemic accelerated digital transformation and remote work adoption, significantly boosting demand for AI servers to support cloud services, video conferencing, content delivery, and automated business processes. Organizations accelerated their AI adoption timelines to address new operational challenges, automate processes, and maintain business continuity during lockdowns. This trend established a new baseline for AI infrastructure investment that continues to drive market growth.

US export restrictions on advanced semiconductors to China and other geopolitical tensions are reshaping the AI server supply chain and market dynamics. These restrictions are driving regional localization efforts, alternative supplier development, and technology sovereignty initiatives. Companies are diversifying their supply chains and developing region-specific products to navigate trade policy complexities while maintaining market access.

Key Takeaways

Market Growth: The AI Server Market is expected to reach USD 2116.16 Billion by 2034, fueled by widespread adoption of generative AI, large language models, and enterprise AI solutions as organizations invest substantially in AI infrastructure for digital transformation and business process automation.

Processor Type Dominance: GPU-based servers lead the processor segment due to superior parallel processing capabilities and AI algorithm optimization.

Server Form Factor Dominance: Rack-mounted servers dominate the form factor segment, driven by modular scalability and data center efficiency requirements.

End-User Industry Dominance: The IT & Telecom sector dominates the AI server market due to its fundamental need for massive computing power to support cloud services, data centers, AI model training, and telecommunications infrastructure that forms the backbone of modern digital economy and AI deployment across all industries.

Drivers: Key drivers accelerating growth include generative AI adoption and enterprise digital transformation, which boost market expansion through increased computational requirements and AI infrastructure investments.

Restraints: Growth is hindered by high capital costs and supply chain constraints, which create challenges such as implementation barriers and component availability issues.

Opportunities: The market is poised for expansion due to opportunities like edge AI deployment and industry-specific AI solutions, which enable distributed computing and specialized applications.

Trends: Emerging trends including liquid cooling adoption and AI accelerator integration are reshaping the market by enabling higher performance density and specialized processing capabilities.

Regional Leader: North America leads owing to technology innovation and cloud infrastructure investments. Asia-Pacific and Europe show high promise due to government AI initiatives and industrial digitization.

Processor Type Analysis:

GPU-based Servers Leads With over 55% Market Share In AI Server Market: The processor type segment is dominated by GPU-based servers, which have emerged as the preferred choice for AI workloads due to their superior parallel processing capabilities and optimization for AI algorithms. GPU servers excel in handling the matrix operations and parallel computations that form the foundation of machine learning and deep learning applications. Their architecture enables efficient processing of large datasets and complex neural networks, making them essential for training large language models and running inference workloads. The segment's leadership reflects the fundamental alignment between GPU architecture and AI computational requirements, establishing GPUs as the industry standard for AI acceleration.

Server Form Factor Analysis:

Rack-mounted servers lead the form factor segment by providing optimal scalability, standardization, and data center efficiency that align with enterprise AI deployment requirements. These servers offer modular design flexibility, enabling organizations to scale their AI infrastructure incrementally while maintaining consistent performance and management capabilities. Rack-mounted configurations provide superior airflow management, power distribution, and space utilization compared to alternative form factors. The segment's dominance reflects the practical advantages of rack-mounted systems in data center environments where density, cooling efficiency, and operational management are critical considerations for large-scale AI deployments.

End-User Industry Analysis:

The IT & Telecom segment leads the market driven by extensive requirements for high-performance computing infrastructure supporting cloud computing platforms, AI-as-a-Service offerings, and telecommunications networks. Major cloud service providers like AWS, Microsoft Azure, and Google Cloud heavily invest in AI servers to support machine learning workloads, natural language processing, and computer vision applications. Telecom companies utilize AI servers for network optimization, predictive maintenance, and 5G infrastructure management. The sector's continuous expansion of data centers and increasing adoption of edge computing further accelerates demand for specialized AI server hardware capable of handling intensive computational workloads.

Regional Analysis:

North America Leads With more than 35% Market Share In AI Server Market: North America maintains its position as the global AI server market leader, driven by the presence of major technology companies, extensive cloud infrastructure, and early enterprise adoption of AI technologies. The region benefits from significant investments in AI research and development, with companies like NVIDIA, Google, Microsoft, and Amazon driving both technological innovation and market demand. The United States leads regional consumption through its mature data center ecosystem, advanced cloud services infrastructure, and aggressive enterprise AI adoption across various industries.

Asia-Pacific represents the fastest-growing regional market, fueled by government-led AI initiatives, manufacturing sector digitization, and rapidly expanding cloud infrastructure across emerging economies. China, Japan, and South Korea are driving regional growth through substantial AI investments, smart city projects, and industrial automation initiatives. The region's growth is supported by increasing data generation, mobile internet penetration, and the emergence of local AI technology companies that are driving domestic demand for AI infrastructure.

Europe maintains a stable market position with steady growth supported by regulatory frameworks promoting AI development, industrial digitization initiatives, and sustainability-focused technology adoption. The region's emphasis on ethical AI, data privacy, and energy-efficient computing creates unique market dynamics that favor advanced AI server technologies. Germany, France, and the United Kingdom lead regional adoption through their strong industrial bases, research institutions, and commitment to digital transformation across manufacturing and service sectors.

Processor Type: (GPU-based Servers, ASIC-based Servers , FPGA-based Servers), Server Form Factor: (Blade Servers, Rack-mounted Servers, Tower Servers), End-User Industry: (Healthcare, IT & Telecommunications, Automotive, Healthcare, Financial Services, Others)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Hewlett Packard Enterprise (HPE), NVIDIA Corporation, Dell Technologies, ZTE Corporation, Lenovo Group, Super Micro Computer, IBM Corporation, Fujitsu Limited, Huawei Technologies, Inspur Information, Atos SE

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 OBJECTIVES

1.2 MARKET DEFINITION

1.2.1 MARKET SCOPE

1.3 RESEARCH METHODOLOGY

1.3.1 SECONDARY DATA

1.3.2 PRIMARY DATA

1.3.3 MARKET SIZE ESTIMATION

1.3.4 BOTTOM-UP APPROACH

1.3.5 TOP-DOWN APPROACH

1.4 RESEARCH ASSUMPTION

1.5 STAKEHOLDERS

1.6 CURRENCY

1.7 YEARS CONSIDERED

1.8 LIMITATION

2 EXECUTIVE SUMMARY

3 MARKET OUTLOOK

3.1 INTRODUCTION

3.2 DROC MATRIX

3.3 MARKET CHALLENGES

3.4 MARKET SHARE ANALYSIS

3.5 COST STRUCTURE ANALYSIS

3.6 VALUE CHAIN ANALYSIS

3.7 COVID-19 IMPACT ANALYSES

3.8 TARIFF IMPACT ANALYSIS

4 INDUSTRY TRENDS

4.1 INTRODUCTION

4.2 PESTEL ANALYSIS

4.3 PORTER’S FIVE FORCES MODEL

4.3.1 DEGREE OF COMPETITION

4.3.2 BARGAINING POWER OF BUYERS

4.3.3 BARGAINING POWER OF SUPPLIERS

4.3.4 THREAT FROM SUBSTITUTES

4.3.5 THREAT FROM NEW ENTRANTS

5 AI SERVER PROCESSOR TYPE ANALYSIS

5.1 INTRODUCTION

5.2 HISTORICAL MARKET PROCESSOR TYPE ANALYSIS, 2019-2023

5.3 CURRENT AND FUTURE MARKET VALUE (MILLION) PROJECTIONS, 2024–2034

5.4 Y-O-Y GROWTH TREND ANALYSIS

5.5 GPU-BASED SERVERS

5.6 ASIC-BASED SERVERS

5.7 FPGA-BASED SERVERS

6 AI SERVER-SERVER FORM FACTOR ANALYSIS

6.1 INTRODUCTION

6.2 HISTORICAL MARKET SERVER FORM FACTOR ANALYSIS, 2019-2023

6.3 CURRENT AND FUTURE MARKET VALUE (MILLION) PROJECTIONS, 2024–2034

6.4 Y-O-Y GROWTH TREND ANALYSIS

6.5 BLADE SERVERS

6.6 RACK-MOUNTED SERVERS

6.7 TOWER SERVERS

7 AI SERVER MARKET END-USER INDUSTRY ANALYSIS

7.1 INTRODUCTION

7.2 HISTORICAL MARKET END-USER INDUSTRY ANALYSIS, 2019-2023

7.3 CURRENT AND FUTURE MARKET VALUE (MILLION) PROJECTIONS, 2024–2034

7.4 Y-O-Y GROWTH TREND ANALYSIS

7.5 HEALTHCARE

7.6 IT & TELECOMMUNICATIONS

7.7 AUTOMOTIVE

7.8 HEALTHCARE

7.9 FINANCIAL SERVICES

7.10 OTHERS

8 GLOBAL AI SERVER REGIONAL ANALYSIS

8.1 INTRODUCTION

8.2 NORTH AMERICA

8.2.1 NORTH AMERICA HISTORICAL MARKET COUNTRY ANALYSIS, 2019-2023

8.2.2 CURRENT AND FUTURE MARKET VALUE (MILLION) PROJECTIONS, 2024–2034

8.2.3 Y-O-Y GROWTH TREND ANALYSIS

8.2.3.1 U.S.

8.2.3.2 CANADA

8.2.3.3 MEXICO

8.3 ASIA-PACIFIC

8.3.1 APAC HISTORICAL MARKET COUNTRY ANALYSIS, 2019-2023

8.3.2 CURRENT AND FUTURE MARKET VALUE (MILLION) PROJECTIONS, 2024–2034

8.3.3 Y-O-Y GROWTH TREND ANALYSIS

8.3.3.1 CHINA

8.3.3.2 JAPAN

8.3.3.3 KOREA

8.3.3.4 INDIA

8.3.3.5 SOUTHEAST ASIA

8.4 MIDDLE EAST AND AFRICA

8.4.1 MIDDLE EAST AND AFRICA HISTORICAL MARKET COUNTRY ANALYSIS, 2019-2023

8.4.2 CURRENT AND FUTURE MARKET VALUE (MILLION) PROJECTIONS, 2024–2034

8.4.3 Y-O-Y GROWTH TREND ANALYSIS

8.4.3.1 SAUDI ARABIA

8.4.3.2 UAE

8.4.3.3 EGYPT

8.4.3.4 NIGERIA

8.4.3.5 SOUTH AFRICA

8.5 EUROPE

8.5.1 EUROPE HISTORICAL MARKET COUNTRY ANALYSIS, 2019-2023

8.5.2 CURRENT AND FUTURE MARKET VALUE (MILLION) PROJECTIONS, 2024–2034

8.5.3 Y-O-Y GROWTH TREND ANALYSIS

8.5.3.1 GERMANY

8.5.3.2 FRANCE

8.5.3.3 UK

8.5.3.4 SPAIN

8.5.3.5 ITALY

8.6 SOUTH AMERICA

8.6.1 SOUTH AMERICA HISTORICAL MARKET COUNTRY ANALYSIS, 2019-2023

8.6.2 CURRENT AND FUTURE MARKET VALUE (MILLION) PROJECTIONS, 2024–2034

8.6.3 Y-O-Y GROWTH TREND ANALYSIS

8.6.3.1 BRAZIL

8.6.3.2 ARGENTINA

8.6.3.3 COLUMBIA

9 COUNTRY LEVEL ANALYSIS

9.1 UNITED STATES

9.2 CANADA

9.3 MEXICO

9.4 CHINA

9.5 JAPAN

9.6 INDIA

9.7 KOREA

9.8 SAUDI AREBIA

9.9 UAE

9.10 EGYPT

9.11 NIGERIA

9.12 SOUTH AFRICA

9.13 GERMANY

9.14 FRANCE

9.15 UK

9.16 SPAIN

9.17 ITALY

9.18 BRAZIL

9.19 ARGENTINA

9.20 COLUMBIA

10 MARKET PLAYERS

10.1 HEWLETT PACKARD ENTERPRISE (HPE)

10.1.1 BUSINESS OVERVIEW:

10.1.2 PRODUCT PORTFOLIO

10.1.3 RECENT DEVELOPMENTS

10.1.4 SWOT ANALYSIS:

10.2 NVIDIA CORPORATION

10.3 DELL TECHNOLOGIES

10.4 ZTE CORPORATION

10.5 LENOVO GROUP

10.6 SUPER MICRO COMPUTER

10.7 IBM CORPORATION

10.8 FUJITSU LIMITED

10.9 HUAWEI TECHNOLOGIES

10.10 INSPUR INFORMATION

10.11 ATOS SE

11 ABOUT US

LIST OF TABLES

TABLE 1 AI SERVER REGIONAL HISTORICAL MARKET ANALYSIS, 2019-2023(USD MILLION)

TABLE 2 GLOBAL AI SERVER MARKET, 2024–2034, (USD MILLION)

TABLE 3 AI SERVER CURRENT AND FUTURE REGIONAL ANALYSIS, 2024–2034 (USD MILLION)

TABLE 4 GLOBAL AI SERVER HISTORICAL MARKET PROCESSOR TYPE ANALYSIS, 2019-2023, (USD MILLION)

TABLE 5 AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034 (USD MILLION)

TABLE 6 GPU-BASED SERVERS CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2019-2034 (USD MILLION)

TABLE 7 ASIC-BASED SERVERS CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2019-2034 (USD MILLION)

TABLE 8 FPGA-BASED SERVERS CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2019-2034 (USD MILLION)

TABLE 9 GLOBAL AI SERVER HISTORICAL MARKET SERVER FORM FACTOR ANALYSIS, 2019-2023, (USD MILLION)

TABLE 10 AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034 (USD MILLION)

TABLE 11 BLADE SERVERS CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2019-2034 (USD MILLION)

TABLE 12 RACK-MOUNTED SERVERS CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2019-2034 (USD MILLION)

TABLE 13 TOWER SERVERS CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2019-2034 (USD MILLION)

TABLE 14 GLOBAL AI SERVER HISTORICAL MARKET END-USER INDUSTRY ANALYSIS, 2019-2023, (USD MILLION)

TABLE 15 AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034 (USD MILLION)

TABLE 16 HEALTHCARE CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2019-2034 (USD MILLION)

TABLE 17 IT & TELECOMMUNICATIONS CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2019-2034 (USD MILLION)

TABLE 18 AUTOMOTIVE CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2019-2034 (USD MILLION)

TABLE 19 HEALTHCARE CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2019-2034 (USD MILLION)

TABLE 20 FINANCIAL SERVICES CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2019-2034 (USD MILLION)

TABLE 21 OTHERS CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2019-2034 (USD MILLION)

TABLE 22 NORTH AMERICA AI SERVER HISTORICAL MARKET ANALYSIS, 2019-2023, (USD MILLION)

TABLE 23 NORTH AMERICA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034 (USD MILLION)

TABLE 24 NORTH AMERICA AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034 (USD MILLION)

TABLE 25 NORTH AMERICA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034 (USD MILLION)

TABLE 26 U.S. AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034

TABLE 27 U.S. AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 28 CANADA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 29 CANADA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 30 MEXICO AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 31 MEXICO AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 32 APAC AI SERVER HISTORICAL MARKET ANALYSIS, 2019-2023, (USD MILLION)

TABLE 33 ASIA-PACIFIC AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034 (USD MILLION)

TABLE 34 ASIA-PACIFIC AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034 (USD MILLION)

TABLE 35 ASIA-PACIFIC AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034 (USD MILLION)

TABLE 36 CHINA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 37 CHINA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 38 JAPAN AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 39 JAPAN AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 40 KOREA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 41 KOREA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 42 INDIA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 43 INDIA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 44 SOUTHEAST ASIA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 45 SOUTHEAST ASIA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 46 MIDDLE EAST AND AFRICA AI SERVER HISTORICAL MARKET ANALYSIS, 2019-2023, (USD MILLION)

TABLE 47 MIDDLE EAST AND AFRICA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034 (USD MILLION)

TABLE 48 MIDDLE EAST AND AFRICA AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034 (USD MILLION)

TABLE 49 MIDDLE EAST AND AFRICA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034 (USD MILLION)

TABLE 50 SAUDI ARABIA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 51 SAUDI ARABIA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 52 UAE AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 53 UAE AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 54 EGYPT AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 55 EGYPT AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 56 NIGERIA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 57 NIGERIA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 58 SOUTH AFRICA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 59 SOUTH AFRICA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 60 EUROPE AI SERVER HISTORICAL MARKET ANALYSIS, 2019-2023, (USD MILLION)

TABLE 61 EUROPE AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034 (USD MILLION)

TABLE 62 EUROPE AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034 (USD MILLION)

TABLE 63 EUROPE AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034 (USD MILLION)

TABLE 64 GERMANY AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 65 GERMANY AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 66 FRANCE AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 67 FRANCE AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 68 UK AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 69 UK AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 70 SPAIN AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 71 SPAIN AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 72 ITALY AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 73 ITALY AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 74 SOUTH AMERICA AI SERVER HISTORICAL MARKET ANALYSIS, 2019-2023, (USD MILLION)

TABLE 75 SOUTH AMERICA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034 (USD MILLION)

TABLE 76 SOUTH AMERICA AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034 (USD MILLION)

TABLE 77 SOUTH AMERICA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034 (USD MILLION)

TABLE 78 BRAZIL AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 79 BRAZIL AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 80 ARGENTINA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 81 ARGENTINA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

TABLE 82 COLUMBIA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

TABLE 83 COLUMBIA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

LIST OF FIGURES

FIGURE 1 GLOBAL AI SERVER MARKET, 2024–2034, (USD MILLION)

FIGURE 2 RESEARCH METHODOLOGY

FIGURE 3 GLOBAL AI SERVER CURRENT AND FUTURE MARKET REGIONAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 4 GLOBAL AI SERVER CURRENT AND FUTURE BY PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 5 MARKET OVERVIEW

FIGURE 6 MARKET SEGMENTATION

FIGURE 7 MARKET SHARE ANALYSIS

FIGURE 8 COST STRUCTURE ANALYSIS

FIGURE 9 VALUE CHAIN ANALYSIS

FIGURE 10 PORTER’S FIVE FORCES ANALYSIS

FIGURE 11 KEY GROWTH STRATEGIES

FIGURE 12 AI SERVER PROCESSOR TYPE ANALYSIS

FIGURE 13 GLOBAL AI SERVER CURRENT AND FUTURE MARKET PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 14 AI SERVER-SERVER FORM FACTOR ANALYSIS

FIGURE 15 GLOBAL AI SERVER CURRENT AND FUTURE MARKET SERVER FORM FACTOR ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 16 AI SERVER END-USER INDUSTRY ANALYSIS

FIGURE 17 GLOBAL AI SERVER CURRENT AND FUTURE MARKET END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 18 GLOBAL AI SERVER CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 21 NORTH AMERICA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 22 NORTH AMERICA AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 23 NORTH AMERICA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 24 U.S. AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 25 U.S. AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 26 CANADA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 27 CANADA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 28 MEXICO AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 29 MEXICO AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 30 MARKET SHARE BY COUNTRY

FIGURE 31 APAC AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 32 APAC AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 33 APAC AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 34 CHINA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 35 CHINA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 36 JAPAN AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 37 JAPAN AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 38 KOREA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 39 KOREA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 40 INDIA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 41 INDIA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 42 SOUTHEAST ASIA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 43 SOUTHEAST ASIA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 44 MARKET SHARE BY COUNTRY

FIGURE 45 MIDDLE EAST AND AFRICA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 46 MIDDLE EAST AND AFRICA AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 47 MIDDLE EAST AND AFRICA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 48 SAUDI ARABIA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 49 SAUDI ARABIA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 50 UAE AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 51 UAE AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 52 EGYPT AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 53 EGYPT AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 54 NIGERIA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 55 NIGERIA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 56 SOUTH AFRICA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 57 SOUTH AFRICA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 58 MARKET SHARE BY COUNTRY

FIGURE 59 EUROPE AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 60 EUROPE AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 61 EUROPE AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 62 GERMANY AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 63 GERMANY AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 64 FRANCE AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 65 FRANCE AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 66 UK AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 67 UK AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 68 SPAIN AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 69 SPAIN AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 70 ITALY AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 71 ITALY AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 72 MARKET SHARE BY COUNTRY

FIGURE 73 SOUTH AMERICA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 74 SOUTH AMERICA AI SERVER CURRENT AND FUTURE SERVER FORM FACTOR ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 75 SOUTH AMERICA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 76 BRAZIL AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 77 BRAZIL AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 78 ARGENTINA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 79 ARGENTINA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 80 COLUMBIA AI SERVER CURRENT AND FUTURE PROCESSOR TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 81 COLUMBIA AI SERVER CURRENT AND FUTURE END-USER INDUSTRY ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 82 FINANCIAL OVERVIEW:

Key Players Analysis:

NVIDIA Corporation: NVIDIA maintains its dominant market position through continuous innovation in GPU technology, comprehensive AI software ecosystems, and strategic partnerships that establish the company as the de facto standard for AI acceleration. The company's competitive advantages include its CUDA software platform, extensive developer community, and early recognition of AI's potential that enabled sustained investment in relevant technologies. NVIDIA's market leadership stems from its ability to provide complete solutions that combine hardware, software, and development tools, making it easier for organizations to deploy AI applications. The company continues to expand its market presence through strategic acquisitions, cloud partnerships, and the development of specialized AI products for emerging applications such as autonomous vehicles and robotics.

Dell Technologies: Dell leverages its extensive enterprise relationships, global distribution network, and comprehensive technology portfolio to provide integrated AI server solutions that address complete customer requirements from infrastructure to support services. The company's competitive strength lies in its ability to combine AI servers with storage, networking, and management solutions that simplify deployment and operation for enterprise customers. Dell's market position benefits from its established relationships with major enterprises, proven service capabilities, and expertise in complex system integration projects. The company's strategic focus on hybrid cloud solutions and edge computing positions it well for the evolving AI infrastructure market where customers seek integrated solutions rather than individual components.

Super Micro Computer: Super Micro Computer has established itself as a leader in high-performance AI servers through its focus on specialized cooling solutions, application-optimized designs, and rapid product development cycles that enable quick response to evolving customer requirements. The company's competitive differentiation stems from its expertise in liquid cooling, custom server configurations, and direct customer engagement that enables tailored solutions for specific AI applications. Super Micro's market success reflects its ability to serve the most demanding AI workloads with innovative thermal management and performance optimization technologies. The company's direct sales model and engineering-focused approach enable close collaboration with customers to develop optimized solutions for emerging AI applications and deployment scenarios.

Hewlett Packard Enterprise (HPE): HPE utilizes its enterprise technology expertise, hybrid cloud solutions, and comprehensive service capabilities to provide AI infrastructure that integrates seamlessly with existing enterprise environments while enabling scalable AI deployment. The company's competitive advantages include its established enterprise relationships, extensive service organization, and expertise in complex technology integration projects that require coordination across multiple technology domains. HPE's market position benefits from its ability to provide complete AI solutions that encompass servers, storage, networking, and management software while ensuring compatibility with existing enterprise infrastructure. The company's strategic focus on edge computing and hybrid cloud solutions aligns well with enterprise requirements for flexible AI deployment options that can adapt to changing business requirements.

Market Key Players

Hewlett Packard Enterprise (HPE)

NVIDIA Corporation

Dell Technologies

ZTE Corporation

Lenovo Group

Super Micro Computer

IBM Corporation

Fujitsu Limited

Huawei Technologies

Inspur Information

Atos SE

Drivers:

Generative AI and Large Language Model Adoption:

The explosive growth of generative AI applications and large language models is driving unprecedented demand for high-performance AI servers capable of training and running increasingly complex neural networks. Organizations across industries are deploying generative AI for content creation, code generation, customer service automation, and decision support applications that require substantial computational resources. The training of large language models requires massive parallel processing capabilities, specialized memory architectures, and optimized interconnect technologies that push the boundaries of server performance. This trend extends beyond technology companies to encompass enterprises in healthcare, finance, retail, and manufacturing that are integrating generative AI into their core business processes. The computational requirements for these applications continue to grow exponentially, creating sustained demand for advanced AI server infrastructure that can handle model sizes measured in billions of parameters and datasets spanning petabytes of information.

Enterprise Digital Transformation and AI Integration:

Comprehensive digital transformation initiatives across enterprises are driving systematic adoption of AI technologies that require dedicated server infrastructure to support machine learning workflows, real-time analytics, and intelligent automation applications. Companies are investing in AI servers to modernize their operations, improve decision-making capabilities, and create competitive advantages through data-driven insights and automated processes. This transformation encompasses everything from customer experience optimization and supply chain automation to fraud detection and predictive maintenance applications that require specialized computing infrastructure. The driver's impact extends across industries as organizations recognize AI as essential for maintaining competitiveness, improving operational efficiency, and creating new revenue opportunities. Enterprise AI adoption requires reliable, scalable server infrastructure that can integrate with existing IT systems while providing the performance necessary for production AI workloads.

Restraints:

High Capital Investment and Infrastructure Costs:

The substantial capital requirements for AI server implementation create significant barriers for organizations, particularly smaller companies and those in cost-sensitive industries where budget constraints limit technology adoption opportunities. AI server costs encompass not only the hardware itself but also associated infrastructure including cooling systems, power distribution, network connectivity, and specialized software licenses that can collectively represent millions of dollars in initial investment. These costs are compounded by the rapid pace of technological advancement, which can lead to concerns about hardware obsolescence and the need for frequent upgrades to maintain competitive performance. The high-performance components required for AI workloads, including advanced GPUs, high-bandwidth memory, and specialized processors, command premium prices that can make implementation challenging for organizations with limited IT budgets. Additionally, the total cost of ownership includes ongoing operational expenses for power consumption, cooling, and specialized technical support that can significantly impact long-term financial planning.

Supply Chain Constraints and Component Availability:

Limited availability of critical AI server components, particularly advanced GPUs and specialized AI accelerators, creates supply chain bottlenecks that constrain market growth and increase lead times for system deployment. The concentration of advanced semiconductor manufacturing in specific geographic regions creates vulnerability to disruptions from geopolitical tensions, natural disasters, and capacity constraints that can significantly impact component availability. These supply chain challenges are exacerbated by the rapid growth in AI adoption, which has created demand that often exceeds manufacturing capacity for specialized components. Organizations face extended waiting periods for critical hardware, forcing them to delay AI initiatives or accept alternative solutions that may not meet their optimal performance requirements. The complexity of AI server supply chains, which involve multiple specialized component suppliers and assembly partners, creates additional coordination challenges that can impact delivery schedules and system availability.

Opportunities:

Edge AI and Distributed Computing Expansion:

The growing deployment of AI applications at the edge creates significant opportunities for specialized AI servers designed for distributed computing environments, autonomous systems, and real-time processing applications that cannot rely on centralized cloud infrastructure. Edge AI applications in autonomous vehicles, industrial automation, smart cities, and IoT devices require local processing capabilities that can operate with minimal latency while maintaining reliability in challenging environmental conditions. This opportunity extends to retail analytics, healthcare monitoring, manufacturing quality control, and security applications where real-time AI processing is essential for operational effectiveness. Edge AI deployment enables new use cases that were previously impractical due to latency, bandwidth, or connectivity constraints, creating demand for ruggedized, energy-efficient AI servers that can operate in diverse deployment environments. The edge computing trend is supported by advances in AI accelerator technology, improved power efficiency, and the development of specialized software frameworks that enable complex AI workloads to run effectively on distributed infrastructure.

Industry-Specific AI Solutions and Vertical Integration:

The development of industry-specific AI applications creates opportunities for specialized AI server configurations optimized for particular use cases, regulatory requirements, and operational environments across healthcare, financial services, manufacturing, and other vertical markets. Different industries have unique requirements for AI infrastructure, including compliance standards, security protocols, performance characteristics, and integration capabilities that create opportunities for customized server solutions. Healthcare AI applications require servers that can handle medical imaging workloads, ensure patient data privacy, and integrate with existing hospital information systems. Financial services AI applications need specialized security features, real-time processing capabilities, and regulatory compliance features that differ from general-purpose AI infrastructure. Manufacturing AI applications require ruggedized hardware, industrial communication protocols, and integration with operational technology systems. These vertical-specific requirements create opportunities for AI server manufacturers to develop specialized products and establish deep partnerships with industry leaders.

Trends:

Liquid Cooling and Thermal Management Innovation

The adoption of advanced liquid cooling technologies is transforming AI server design by enabling higher performance density, improved energy efficiency, and better thermal management for increasingly powerful AI accelerators and processors. Traditional air cooling approaches are reaching their limits as AI workloads generate more heat and require higher performance density to optimize data center space utilization. Liquid cooling enables direct heat removal from critical components, allowing for higher clock speeds, improved processor performance, and reduced fan noise that creates better data center operating environments. This trend includes immersion cooling, direct-to-chip cooling, and hybrid cooling solutions that can handle the thermal challenges of next-generation AI accelerators. The technology enables data centers to achieve higher compute density while reducing overall energy consumption and operational costs. Advanced thermal management is becoming a key differentiator for AI server manufacturers as customers seek solutions that can maximize performance while minimizing operational complexity and environmental impact.

AI Accelerator Integration and Specialized Processing

The integration of specialized AI accelerators and domain-specific processors is reshaping AI server architecture by enabling optimized performance for specific AI workloads while improving overall system efficiency and reducing total cost of ownership. This trend encompasses the development of AI-specific chips, neural processing units, and specialized accelerators designed for particular AI algorithms or application domains. AI accelerator integration enables servers to achieve better performance per watt, reduced latency, and improved cost-effectiveness for specific AI applications compared to general-purpose computing approaches. The trend includes both discrete accelerator cards and integrated solutions that combine multiple processing technologies in unified architectures. Advanced AI accelerators enable new capabilities such as real-time inference, edge AI deployment, and energy-efficient training that expand the practical applications of AI technology across various industries and use cases.

Recent Development

In August 2025: Nvidia has revealed that its RTX Pro 6000 Blackwell Server Edition GPU is now being integrated into compact 2U rack-mount servers by multiple global system partners as part of the company's Enterprise AI factory-validated design program. This development marks a significant shift from previous deployment requirements, where customers seeking to implement these graphics cards in their private cloud environments had to accommodate bulkier 4U server configurations with increased cooling and power requirements. The new 2U form factor represents one of the most widely adopted rack-mount standards in on-premises data center facilities, making the technology more accessible for enterprise deployments.

In August 2025: HPE is broadening its NVIDIA AI Computing by HPE solutions lineup through the introduction of new ProLiant Compute servers featuring NVIDIA's Blackwell architecture, alongside enhanced functionalities within HPE Private Cloud AI. These developments aim to address the increasing enterprise demand for robust infrastructure capable of supporting generative AI, agentic AI, and physical AI applications, while simultaneously opening new avenues for channel partners to provide turnkey AI technology stacks to their customers.

Frequently Asked Questions

How big is the AI Server Market?

The AI Server Market will grow from USD 136.09 Bn in 2024 to USD 2116.16 Bn by 2034 at 31.57% CAGR. Explore trends, key players, and innovations driving growth.

Who are the major players in the AI Server Market?

Hewlett Packard Enterprise (HPE), NVIDIA Corporation, Dell Technologies, ZTE Corporation, Lenovo Group, Super Micro Computer, IBM Corporation, Fujitsu Limited, Huawei Technologies, Inspur Information, Atos SE

Which segments covered the AI Server Market?

Processor Type: (GPU-based Servers, ASIC-based Servers , FPGA-based Servers), Server Form Factor: (Blade Servers, Rack-mounted Servers, Tower Servers), End-User Industry: (Healthcare, IT & Telecommunications, Automotive, Healthcare, Financial Services, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, Server Form Factor (Blade Servers, Rack-mounted Servers, Tower Servers), End-User Industry (Healthcare, IT & Telecommunications, Automotive, Healthcare, Financial Services, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

, Server Form Factor (Blade Servers, Rack-mounted Servers, Tower Servers), End-User Industry (Healthcare, IT & Telecommunications, Automotive, Healthcare, Financial Services, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

, Server Form Factor (Blade Servers, Rack-mounted Servers, Tower Servers), End-User Industry (Healthcare, IT & Telecommunications, Automotive, Healthcare, Financial Services, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

, Server Form Factor (Blade Servers, Rack-mounted Servers, Tower Servers), End-User Industry (Healthcare, IT & Telecommunications, Automotive, Healthcare, Financial Services, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")