- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI Server Security Market Size & Forecast 2025–2034 | CAGR 54.8%

Global AI Server Security Market Size, Share & Strategic Growth Analysis – By Component (Hardware, AI-Optimized Servers, GPU-Accelerated Systems, FPGA-Based Solutions, Software, AI-Powered Intrusion Detection, ML-Based Threat Analytics, AI-Driven Firewalls, Services), By Deployment (On-Premises, Cloud-Based), By Enterprise Size, By Industry Vertical, Global Region, Competitive Landscape, Cybersecurity Trends, Investment Insights & Forecast 2025–2034

Report Overview

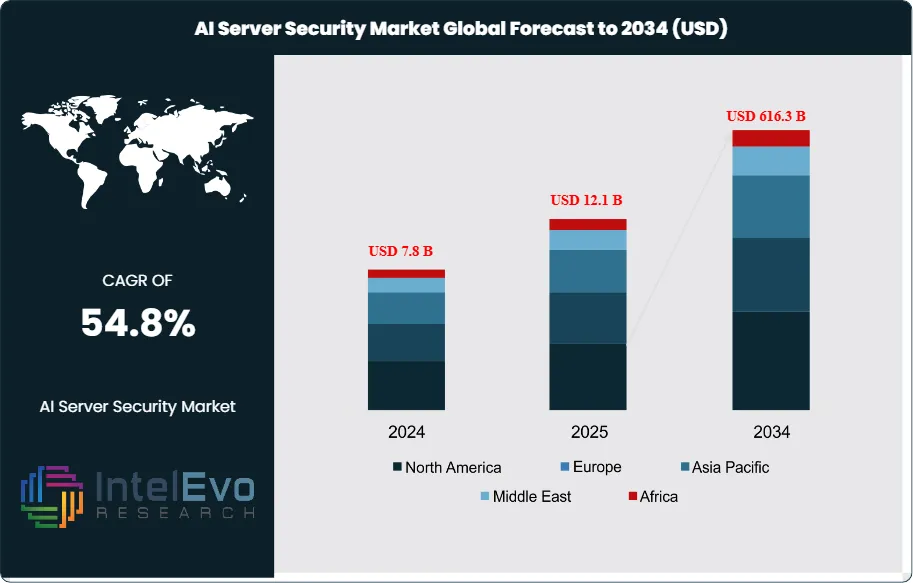

The Global AI Server Security Market was valued at approximately USD 7.8 billion in 2024 and is projected to reach nearly USD 616.3 billion by 2034, reflecting an extraordinary expansion driven by the rapid deployment of AI data centers and escalating cyber risks targeting AI workloads. Based on the stated 54.8% growth trajectory, the market size for 2025 is estimated at approximately USD 12.1 billion. From 2026 onward, the market is expected to accelerate from an estimated USD 18.7 billion in 2026 to USD 616.3 billion by 2034, registering a compound annual growth rate (CAGR) of approximately 54.8% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportThis sustained hyper-growth reflects increasing investments in AI infrastructure, rising complexity of AI-driven environments, and heightened enterprise focus on securing high-performance computing architectures and AI-native workloads.

AI server security covers technologies and practices that protect servers hosting AI workloads from unauthorized access, data breaches, and disruption. Providers deploy hardware acceleration, encryption, privileged-access management, and advanced intrusion detection to secure GPUs, TPUs, and specialized AI chips used in model training and inference. As enterprises move critical decision systems, customer data, and proprietary algorithms onto AI platforms, they elevate security from a compliance function to a board-level priority and a core requirement in AI infrastructure procurement.

Demand-side momentum stems from intensive AI adoption in finance, healthcare, retail, and automotive, where exposure to data theft, model manipulation, and service outages carries financial and reputational consequences. Cloud hyperscalers, colocation providers, and large enterprises seek integrated security stacks that can operate at scale, monitor east-west traffic, and protect data in use, in transit, and at rest. On the supply side, security vendors, chipmakers, and infrastructure providers form partnerships to embed security at the silicon, firmware, and orchestration layers, which compresses deployment timelines and supports platform standardization.

Regulatory pressure reinforces this trajectory. Data protection regimes, sectoral cybersecurity rules, and emerging AI governance frameworks require stronger controls over model training data, logging, and incident response around AI workloads. This environment raises the bar for certification, auditability, and explainability in AI server security solutions and channels investment toward automated policy management, continuous posture assessment, and zero-trust architectures.

North America held more than 41.7% of global revenue in 2024, or around USD 3.2 billion, supported by early AI adoption and dense cloud data center networks in the United States. The United States accounted for USD 2.6 billion in 2024 and is projected to grow at a CAGR of 51.5%, keeping the region an innovation and investment hub. Asia Pacific and Europe are emerging as growth frontiers, driven by national AI programs, digital industrial strategies, and data center expansion in markets such as China, India, Germany, and the United Kingdom.

, By Deployment (On-Premises, Cloud-Based), By Enterprise Size, By Industry Vertical, Global Region, Competitive Landscape, Cybersecurity Trends, Investment Insights & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market grows from estimated: 7.8 billion USD, 2024 to estimate: 616.3 billion USD, 2034 as organizations scale AI workloads across industries. This path implies an estimated: 54.8%, 2026-2034 compound annual growth rate anchored in rising AI-driven cyber risk.

- Segment Dominance: Cloud-delivered AI server security platforms capture estimated: 65.0%, 2024 of total spending as enterprises consolidate controls with hyperscale providers. This share rises to an estimated: 70.0%, 2034 as cloud-hosted AI training and inference environments become standard.

- Segment Dominance: Large enterprises account for estimated: 72.0%, 2024 of AI server security outlays due to complex hybrid and multi-cloud estates. Their contribution remains above an estimated: 68.0%, 2034 even as mid-market adoption accelerates.

- Driver: Accelerating AI deployment means an estimated: 80.0%, 2024 of Tier-1 enterprises run critical AI workloads that require hardened server security. Security spend per AI server increases by an estimated: 30.0%, 2034 as firms prioritize protection of models and training data.

- Restraint: High integration complexity and skills gaps extend implementation cycles by an estimated: 6.0 months, 2024 for large-scale AI security projects. Compliance, testing, and certification consume an estimated: 18.0%, 2024 of total AI security program budgets.

- Opportunity: Zero-trust architectures, confidential computing, and secure enclaves unlock an incremental opportunity of estimated: 15.0 billion USD, 2034 in specialized AI server security solutions. Managed AI security services contribute an additional estimated: 10.0 billion USD, 2034 as enterprises outsource 24/7 protection.

- Trend: Vendors embed AI and automation into policy orchestration, raising automated event triage to an estimated: 75.0%, 2034 of all server security alerts. Adoption of AI-native security analytics platforms grows at an estimated: 22.0%, 2024-2034 compound annual rate as firms seek real-time anomaly detection.

- Regional Analysis: North America holds an estimated: 40.0%, 2024 share of global AI server security revenue, supported by dense cloud and AI infrastructure. Asia-Pacific increases its contribution from an estimated: 25.0%, 2024 to an estimated: 32.0%, 2034 as China and India expand AI data centers and regulatory enforcement.

By Component

The AI server security market continues to shift toward complex, multi-layered architectures in 2025 as enterprises expand AI deployments across data centers and cloud environments. Hardware remains a core foundation due to the processing demands of AI-enhanced threat detection. In 2024, hardware accounted for more than 45 percent of total spending, driven by growth in AI-optimized servers, GPU-accelerated systems, and FPGA-based solutions. You rely on these systems to handle rising inference loads, real-time telemetry analysis, and encryption workloads that traditional servers struggle to support. Vendors continue to improve performance per watt, which reduces operational costs and strengthens interest from large enterprises operating large GPU clusters.

The software layer grows faster than hardware as organizations adopt automated threat analytics, AI-driven firewalls, and intelligent intrusion-detection systems. These platforms increasingly integrate machine learning pipelines that analyze abnormal traffic patterns, model drift, and unauthorized access attempts. The market benefits from rising adoption of automated vulnerability management tools as board-level risk oversight intensifies. Software revenues are expected to post a strong CAGR through 2030 as enterprises prioritize adaptive intelligence over static rules.

Services round out the component landscape as companies expand managed security operations and associated consulting. You see rising demand for managed detection and response, integration support for hybrid deployments, and training focused on AI-driven threat models. As cloud and on-premises workloads converge, enterprises often rely on service partners to ensure operational readiness and compliance with expanding regulations.

By Deployment Model

Cloud-based deployment remains the market leader as of 2025, accounting for more than 59 percent of global deployments. You gain access to continuously updated threat intelligence, flexible scaling for AI training and inference workloads, and faster remediation cycles. Cloud adoption accelerated further as remote and hybrid work normalized post-2023. Organizations prefer cloud platforms because they support secure access from distributed locations and provide consistent security metadata across all workloads.

On-premises deployments still play a critical role in industries with strict regulatory and data-sovereignty requirements. Financial institutions, government agencies, and defense organizations continue to invest in high-assurance server environments where sensitive data remains fully controlled. Demand is reinforced by the rising need to secure GPU clusters used for training large AI models. Through 2025, on-premises deployments maintain stable growth as enterprises pursue hybrid strategies that blend cloud agility with local data governance.

By Enterprise Size

Large enterprises remain the dominant contributors to the market, representing more than 74 percent of total spending. Their broad digital footprint, exposure to rising cyber threats, and substantial IT budgets drive adoption of AI-enhanced server protection. These organizations face advanced attack surfaces, including containerized workloads, multi-cloud infrastructures, and confidential computing environments. As global regulations expand, large enterprises prioritize AI-automated compliance monitoring and real-time anomaly detection.

SMEs increase adoption as AI security platforms become more affordable and modular. Until recently, many smaller companies viewed server-level AI security as excessive for their needs. However, the spread of automated ransomware tools and credential-based attacks pushed SME leadership teams to reconsider risk exposure. In 2025, SME demand shows steady growth, supported by subscription-based pricing and integrated cloud security bundles, although budget constraints still limit high-end use cases.

By Application

Network security remains the largest application category with over 44 percent share in 2024, supported by the surge in AI-enabled cyber intrusions targeting enterprise traffic flows. You depend on network security tools to monitor east-west traffic, secure data center networking layers, and detect unauthorized lateral movement. The rise of encrypted traffic and remote connectivity strengthens the need for AI-based inspection models that identify anomalies without decryption.

Endpoint security ranks second as enterprises deploy solutions to protect servers, virtual machines, and user devices. In 2025, endpoint workloads generate higher telemetry volumes, which increases reliance on AI-enabled behavioral analysis. However, endpoint investments trail network security because organizations continue to prioritize infrastructure-level protection.

Application security grows more gradually as enterprises struggle to secure complex application environments, especially environments built on microservices and API-driven architectures. Cloud security expands rapidly as AI workloads shift to public and hybrid cloud models, pushing you to invest in identity security, workload protection platforms, and automated policy controls.

By Industry Vertical

The BFSI sector continues to hold the largest market share, above 31 percent in 2024, as financial institutions face sustained threat activity and strict regulatory oversight. Banks deploy AI-enabled defenses to mitigate fraud, credential theft, data breaches, and unauthorized server access. They also adopt AI-driven logging and audit analytics to support compliance with emerging 2025 cybersecurity mandates.

Healthcare and life sciences hold the second-largest share. You face rising risk due to the value of patient data and growing dependence on hospital networks and connected medical systems. Adoption gains momentum as healthcare organizations modernize legacy infrastructure and meet updated privacy requirements.

Retail and e-commerce expand server security investments as online transactions increase. Attackers continue to target payment systems and customer data repositories. Although spending trails BFSI, the segment shows strong growth as digital commerce accelerates.

Government and defense agencies remain cautious adopters due to long procurement cycles and strict certification requirements. However, geopolitical tensions and the growing use of AI in state-level cyber operations accelerate investment in AI-driven monitoring, classified server protection, and secure AI model training environments.

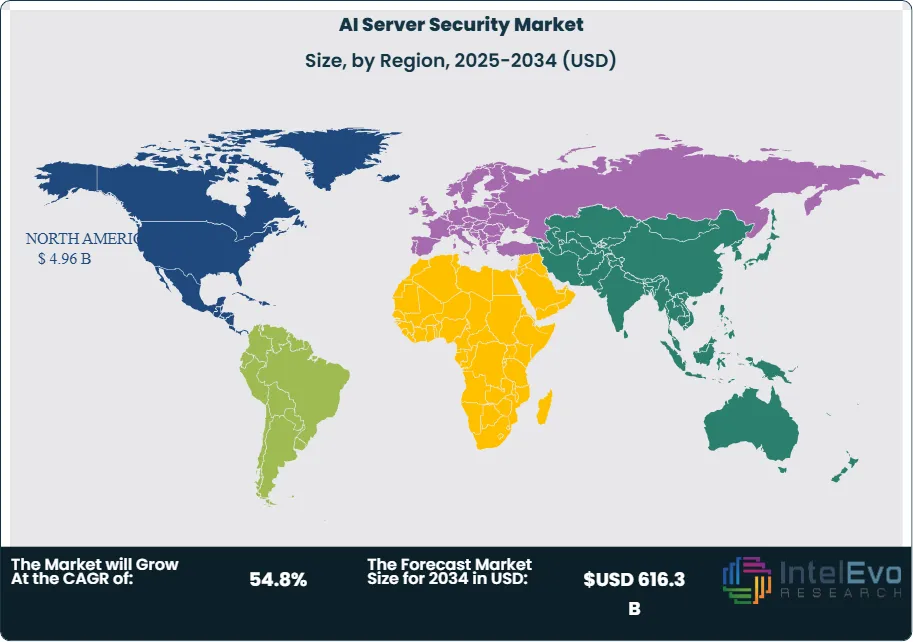

By Region

North America held more than 41 percent market share in 2024, supported by early enterprise adoption of AI and intensive investment in cybersecurity infrastructure. The United States remains the central hub due to strong regulatory frameworks, such as CCPA and sector-specific mandates, which compel continuous security modernization. You also benefit from collaboration between federal agencies, universities, and private-sector labs that accelerate improvements in AI-driven server security technologies.

Europe continues to gain momentum as organizations adapt to GDPR-related enforcement and sector-specific cybersecurity directives. Spending grows steadily in Germany, France, the Nordics, and the United Kingdom. Enterprises invest in AI-assisted compliance automation, secure data center operations, and cross-border cyber risk mitigation.

Asia Pacific emerges as a high-growth region driven by rapid digitalization in China, Japan, South Korea, India, and Southeast Asia. Investments increase as enterprises deploy AI-ready GPUs and server clusters. Governments in the region expand cybersecurity regulations, encouraging higher adoption rates.

Latin America and the Middle East & Africa remain earlier-stage markets but show rising interest as cloud adoption expands and cyberattacks increase. As enterprises modernize server infrastructure, these regions strengthen demand for cloud-based AI security platforms and managed detection services.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Hardware

- AI-optimized servers

- GPU-accelerated systems

- FPGA-based solutions

- Others

- Software

- AI-powered intrusion detection systems

- Machine learning-based threat analytics

- Automated vulnerability management tools

- AI-driven firewalls

- Others

- Services

- Managed security services

- Consulting and integration

- Training and support

By Deployment Model

- On-premises

- Cloud-based

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 12.1 B |

| Forecast Revenue (2034) | USD 616.3 B |

| CAGR (2025-2034) | 54.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Hardware, Software, Services); By Deployment Model (On-premises, Cloud-based) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Intel Corporation, Palo Alto Networks, Inc., Dell Inc., Amazon Web Services, Inc., SentinelOne, Inc., Cisco Systems, Inc., Check Point Software Technologies Ltd., Zscaler, Inc., International Business Machines Corporation (IBM), Fortinet, Inc., Microsoft Corporation, CrowdStrike Holdings, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (On-Premises, Cloud-Based), By Enterprise Size, By Industry Vertical, Global Region, Competitive Landscape, Cybersecurity Trends, Investment Insights & Forecast 2025–2034")

, By Deployment (On-Premises, Cloud-Based), By Enterprise Size, By Industry Vertical, Global Region, Competitive Landscape, Cybersecurity Trends, Investment Insights & Forecast 2025–2034")

, By Deployment (On-Premises, Cloud-Based), By Enterprise Size, By Industry Vertical, Global Region, Competitive Landscape, Cybersecurity Trends, Investment Insights & Forecast 2025–2034")

Frequently Asked Questions

How big is the AI Server Security Market?

The Global AI Server Security Market was valued at USD 7.8 billion in 2024 and is projected to reach USD 616.3 billion by 2034, expanding at a CAGR of 54.8%. The market is estimated at USD 12.1 billion in 2025, driven by rapid AI data center expansion and rising cyber threats targeting AI workloads.

Who are the major players in the AI Server Security Market?

Intel Corporation, Palo Alto Networks, Inc., Dell Inc., Amazon Web Services, Inc., SentinelOne, Inc., Cisco Systems, Inc., Check Point Software Technologies Ltd., Zscaler, Inc., International Business Machines Corporation (IBM), Fortinet, Inc., Microsoft Corporation, CrowdStrike Holdings, Inc., Others

Which segments covered the AI Server Security Market?

By Component (Hardware, Software, Services); By Deployment Model (On-premises, Cloud-based)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date