- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Vapor Recovery Unit Market Size & Forecast 2034 | CAGR 6.6%

Global AI Trust, Risk and Security Management (AI TRiSM) Market Size, Share, Growth & Industry Analysis By Offering (Solutions, Services), By Deployment (Cloud, On-Premise), By Type (AI Application Security, Data Protection, Data Anomaly Detection, Others), By Application (Governance & Compliance, Security & Anomaly Detection, Privacy Management, Bias Detection & Mitigation), By End-Use (BFSI, Government, IT & Telecom, Healthcare, Manufacturing, Retail & E-Commerce, Media & Entertainment) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

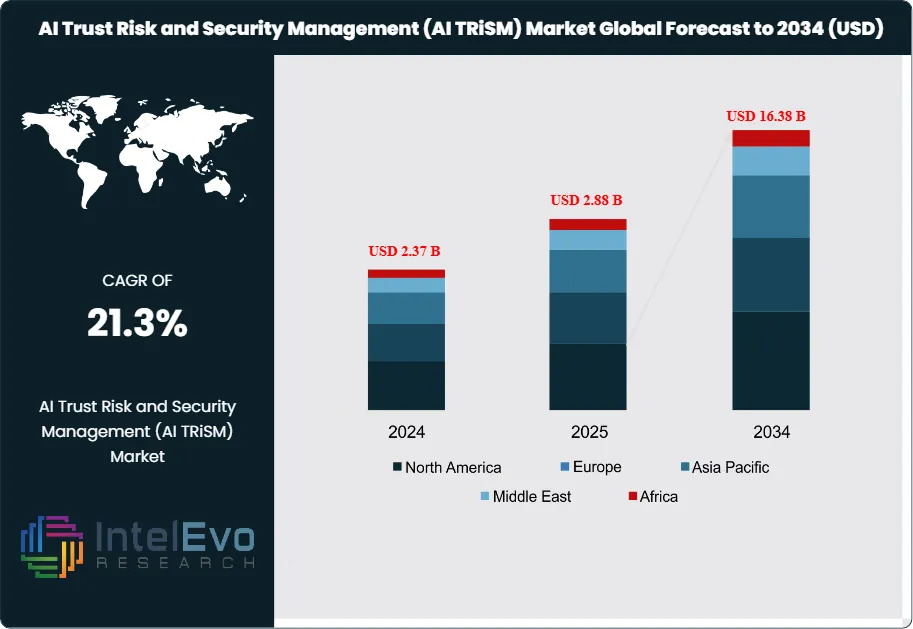

| USD 2.88 Billion | USD 16.38 Billion | 21.3% | North America, 38.2% |

The AI Trust, Risk and Security Management (AI TRiSM) Market was valued at approximately USD 2.37 Billion in 2024 and reached USD 2.88 Billion in 2025. The market is projected to grow to USD 16.38 Billion by 2034, expanding at a CAGR of 21.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 13.50 Billion over the analysis period. AI trust risk and security management market growth now tracks enterprise AI adoption rather than experimental AI spend. Gartner defines AI TRiSM as the discipline that covers governance, trustworthiness, fairness, reliability, efficacy, and data protection for AI systems. That definition has become commercially relevant because AI moved from sandbox use into customer service, software engineering, underwriting, security operations, and regulated decision flows. McKinsey reported that 78% of organizations now use AI in at least one business function and 71% regularly use generative AI in at least one business function, which sharply expands the control surface that buyers must monitor, test, and document.

Get More Information about this report -

Request Free Sample ReportAI trust risk and security management market demand is rising because regulation, cyber risk, and board scrutiny now hit the same AI program at the same time. The EU AI Act entered into force on 1 August 2024, prohibited-practice and AI-literacy rules started applying on 2 February 2025, and GPAI governance obligations became applicable on 2 August 2025. In parallel, NIST’s AI RMF and its generative AI profile give procurement teams and internal audit groups a practical control map, while ISO/IEC 42001 created the first formal AI management system standard. Those three anchors are shifting budgets away from ad hoc model reviews and toward recurring spend on inventory, runtime monitoring, red teaming, access control, policy enforcement, and audit evidence.

Supply conditions also favor rapid expansion. The vendor base now spans hyperscalers, data security platforms, AI governance specialists, and application security firms. Google Cloud launched AI Protection in March 2025. Microsoft added new protections for AI and Security Copilot agents in March 2025. Palo Alto Networks launched Prisma AIRS in April 2025. ServiceNow launched AI Control Tower in May 2025. Salesforce followed with Agentforce 3 and Command Center in June 2025. AWS pushed Bedrock Guardrails forward with Automated Reasoning checks in August 2025 and code-domain support in November 2025. This product cadence is shortening buying cycles because enterprises can now buy AI governance, security posture, and runtime control from existing software estates.

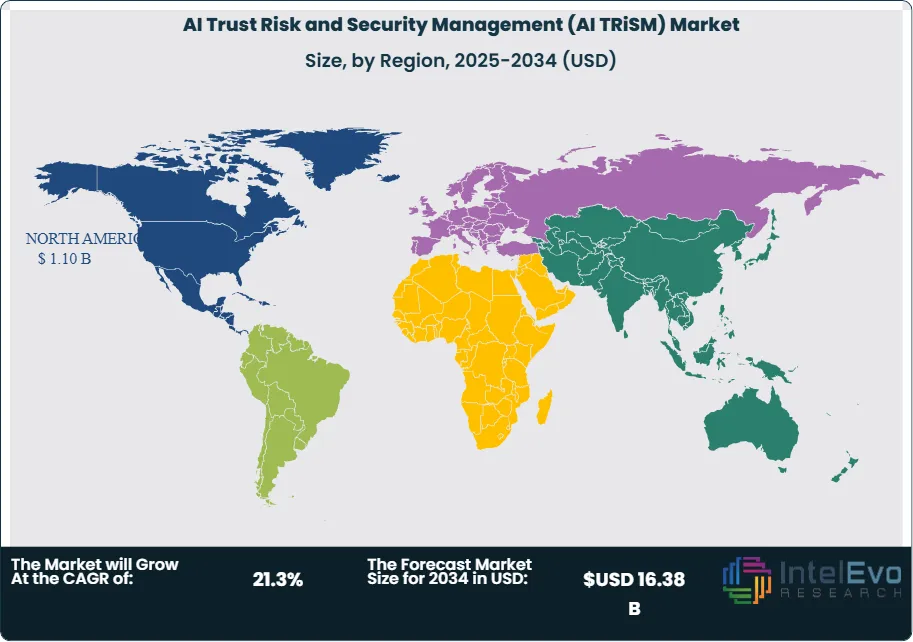

Regional demand remains uneven. North America leads in 2025 with an estimated 38.2% share, or USD 1.10 Billion, because the US combines the deepest installed base of enterprise AI, the strongest concentration of platform vendors, and the widest use of AI in IT and software functions. Europe ranks second as compliance spending accelerates around the AI Act. Asia Pacific follows closely as India, Singapore, Japan, and South Korea build national AI programs and assurance frameworks. Latin America and the Middle East and Africa remain smaller in absolute revenue, but both regions are moving from pilot spending toward policy-backed enterprise deployments.

Market Size, Share, Growth & Industry Analysis By Offering (Solutions, Services), By Deployment (Cloud, On-Premise), By Type (AI Application Security, Data Protection, Data Anomaly Detection, Others), By Application (Governance & Compliance, Security & Anomaly Detection, Privacy Management, Bias Detection & Mitigation), By End-Use (BFSI, Government, IT & Telecom, Healthcare, Manufacturing, Retail & E-Commerce, Media & Entertainment) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: AI trust risk and security management market revenue stands at USD 2.88 Billion in 2025 and is projected to reach USD 16.38 Billion by 2034, reflecting a 21.3% CAGR across 2025–2034 and an absolute gain of USD 13.50 Billion.

- Segment Dominance: Solutions lead the market with an estimated 67.5% share in 2025, equal to about USD 1.94 Billion, because enterprises first buy software for inventory, runtime guardrails, audit evidence, and policy enforcement before adding outside services.

- Segment Dominance: Governance and compliance holds the largest application share at an estimated 31.4% in 2025, or about USD 0.90 Billion, supported by AI Act enforcement milestones, NIST AI RMF adoption, and ISO/IEC 42001 alignment.

- Driver: Enterprise AI use has reached broad operational depth, with 78% of organizations using AI in at least one function and 71% regularly using generative AI in at least one function, which directly expands spending on monitoring, testing, and governance controls.

- Restraint: Regulation and risk became the top barrier to development and deployment in Deloitte’s 2025 research, rising 10 percentage points from Q1 to Q4, while over two-thirds of firms said 30% or fewer of experiments would fully scale in the next three to six months.

- Opportunity: Agent governance is the largest white-space opportunity. IBM found 61% of CEOs are already adopting AI agents and Deloitte found 26% of leaders are exploring agentic AI to a large or very large extent, opening a new control market for identity, runtime inspection, and audit trails.

- Trend: Runtime assurance is replacing static policy review. AWS reports up to 99% verification accuracy for Automated Reasoning checks, and Salesforce, ServiceNow, and Fiddler all moved toward command-center or control-plane models during 2025–2026.

- Regional Analysis: North America leads with an estimated 38.2% share in 2025, equal to about USD 1.10 Billion, helped by the region’s vendor concentration, enterprise AI penetration, and early security tooling rollouts.

Competitive Landscape Overview

AI trust risk and security management market competition remains moderately fragmented in 2025. The top four vendors account for an estimated 34.7% of global revenue. Competition is technology-led and platform-led rather than price-led, because buyers want integrated controls across data, models, agents, and audit workflows. Competitive intensity increased through 2025 as hyperscalers added native guardrails, security firms moved into AI runtime defense, and workflow vendors launched agent command centers. The March 2026 close of Google’s USD 32 Billion Wiz acquisition raises pressure on the rest of the field to unify cloud, data, and AI controls.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

|---|---|---|---|---|---|

| Microsoft | US | Leader | Microsoft Purview DSPM for AI | North America | Unveiled Security Copilot agents and new protections for AI in Mar 2025 |

| IBM | US | Leader | watsonx.governance with Guardium AI Security | North America | Added tighter Guardium AI Security and watsonx.governance integration in Jun 2025 |

| Google Cloud | US | Leader | AI Protection | North America | Completed Wiz acquisition in Mar 2026 after signing the USD 32 Billion deal in Mar 2025 |

| Palo Alto Networks | US | Leader | Prisma AIRS | North America | Launched Prisma AIRS unified AI security platform in Apr 2025 |

| ServiceNow | US | Challenger | AI Control Tower | North America | Launched AI Control Tower in May 2025 |

| Salesforce | US | Challenger | Agentforce Command Center with Einstein Trust Layer | North America | Launched Agentforce 3 with Command Center in Jun 2025 |

| Amazon Web Services | US | Challenger | Amazon Bedrock Guardrails | North America | Made Automated Reasoning checks generally available in Aug 2025 |

| DataRobot | US | Challenger | DataRobot AI Governance | North America | Rolled out its new agentic AI Platform in Jul 2025 |

| Credo AI | US | Niche Player | Credo AI Governance Platform | North America | Launched Global Partner Program in Jul 2025 |

| Fiddler AI | US | Niche Player | Fiddler AI Control Plane | North America | Raised USD 30 Million Series C in Jan 2026 to expand compound AI controls |

By Offering

AI trust risk and security management market spending by offering shows clear software concentration. Solutions account for an estimated 67.5% of 2025 revenue, or USD 1.94 Billion, while services contribute 32.5%, or USD 0.94 Billion. This mix reflects how enterprises buy AI inventory, model monitoring, guardrails, logging, policy engines, and audit evidence as recurring software first, then add advisory, integration, and red-team support later. IBM, Microsoft, Google Cloud, and Palo Alto all sell core platform controls that fit this pattern. Services remain essential in regulated sectors because policy mapping, control design, and evidence preparation still require outside support, especially for first-time AI Act readiness and ISO/IEC 42001 programs. Services demand should stay strong through 2034, but software will keep the revenue lead because runtime monitoring and agent supervision generate annual subscription spend rather than one-time project fees.

By Deployment

AI trust risk and security management market spending by deployment favors cloud, which represents an estimated 61.8% of 2025 revenue, or USD 1.78 Billion, versus 38.2% for on-premise, or USD 1.10 Billion. Cloud leads because Bedrock Guardrails, Google AI Protection, Microsoft Purview DSPM for AI, and ServiceNow AI Control Tower all assume multi-model, multi-cloud, or SaaS-heavy AI estates. Buyers want rapid onboarding, centralized policy changes, and shared telemetry across copilots, agents, and developer tools. On-premise demand remains meaningful in BFSI, defense, public sector, and healthcare where data residency, latency control, or internal model hosting still shape architecture decisions. Over the forecast period, hybrid deployment will remain common in practice, but revenue will shift further toward cloud-delivered control planes because agentic AI and third-party model use increase the need for central logging and cross-platform visibility.

By Type

AI trust risk and security management market spending by type is led by AI application security at an estimated 34.8% share in 2025, or USD 1.00 Billion. Data protection follows at 28.7%, or USD 0.83 Billion. Data anomaly detection holds 22.9%, or USD 0.66 Billion. Other controls, including bias analytics, model documentation, and policy orchestration, hold 13.6%, or USD 0.39 Billion. Application security leads because prompt injection, insecure output handling, training data poisoning, supply-chain exposure, and model denial-of-service risks have moved from theory into security roadmaps. Data protection stays close behind because AI programs cannot pass internal review without access control, data classification, lineage, and secrets hygiene. Anomaly detection remains important, but many buyers still purchase it as a module inside wider security suites.

By Application

AI trust risk and security management market demand by application is led by governance and compliance with an estimated 31.4% share in 2025, or USD 0.90 Billion. Security and anomaly detection follows at 27.6%, or USD 0.79 Billion. Privacy management represents 22.1%, or USD 0.64 Billion. Bias detection and mitigation contributes 18.9%, or USD 0.54 Billion. Governance and compliance leads because board committees and risk teams need policy inventories, approval workflows, control evidence, and model registers before they approve scaled AI use. That demand strengthened after the EU AI Act milestone dates moved from policy discussion into live obligations. Security and anomaly detection is rising quickly as enterprises move from chatbots to agents with tool use and data access. Privacy management remains central where copilots touch internal knowledge bases. Bias mitigation is still important, but it receives smaller direct budgets outside HR, lending, healthcare, and public decision systems.

By End Use

AI trust risk and security management market demand by end use is led by BFSI at an estimated 22.8% share in 2025, or USD 0.66 Billion. Government follows at 17.5%, or USD 0.50 Billion. IT and telecommunication accounts for 16.9%, or USD 0.49 Billion. Healthcare contributes 14.6%, or USD 0.42 Billion. Manufacturing represents 10.8%, retail and e-commerce 8.7%, media and entertainment 4.1%, and other sectors 4.6%. BFSI leads because explainability, fraud controls, customer-data protection, and model governance all sit close to revenue and supervisory risk. Government demand is rising through procurement rules, sovereign AI programs, and public service automation. IT and telecom keeps high share because enterprise AI adoption is deepest in IT functions, while healthcare growth remains strong due to patient-data sensitivity and clinical review requirements. Sectors with lower current share still matter because code assistants, customer agents, and enterprise search are spreading into every large organization.

Regional Analysis

North America

AI trust risk and security management market revenue in North America is estimated at 38.2% of the global total in 2025, equal to USD 1.10 Billion. The United States drives the region through the densest concentration of enterprise AI spend, cloud AI deployments, and vendor headquarters. NIST AI RMF and the generative AI profile give US enterprises a reference structure that procurement, security, and model risk teams can use immediately. Microsoft, IBM, Google Cloud, Palo Alto Networks, AWS, Salesforce, and ServiceNow all launched material AI governance or AI security capabilities during 2025–2026, which keeps buying friction low for existing customers. Canada adds demand through financial services, public sector modernization, and cross-border data governance needs. Mexico remains smaller in absolute value but benefits from nearshore software delivery, manufacturing digitalization, and growing use of copilots in shared-service environments. North America should remain the largest AI trust risk and security management market through 2034 because software engineering, security operations, and enterprise knowledge workflows are moving first in this region.

Europe

AI trust risk and security management market revenue in Europe is estimated at 26.4% in 2025, or USD 0.76 Billion. Europe ranks second because regulation converts governance from a best-practice discussion into a spending requirement. The AI Act’s phased timetable matters directly to this market. Prohibited-practice and AI-literacy provisions started applying in February 2025, and GPAI obligations became applicable in August 2025. That timetable increases demand for use-case inventory, conformity evidence, vendor due diligence, and runtime monitoring. Germany leads regional spending because of its industrial software base, automotive AI programs, and strong enterprise compliance budgets. The United Kingdom remains large through financial services and cyber tooling. France benefits from public sector digital policy and large-model activity. The Netherlands is strategically relevant because multicloud, data infrastructure, and international corporate headquarters concentrate there. ISO/IEC 42001 is gaining attention across Europe as firms seek a certifiable governance structure that sits beside privacy and information-security management programs.

Asia Pacific

AI trust risk and security management market revenue in Asia Pacific is estimated at 23.1% in 2025, or USD 0.67 Billion. Asia Pacific is the fastest-closing gap to Europe because governments are building both AI growth policy and assurance structures at the same time. India is a major demand center after the IndiaAI Mission, which carries an outlay of more than INR 10,300 crore and aims to widen compute access and AI deployment. Singapore is influential well beyond its size because IMDA and the AI Verify Foundation launched the Global AI Assurance Pilot in February 2025 and followed with new trusted-data and assurance tools in July 2025. Japan is moving with risk-management guidance in public procurement and a pro-adoption AI Promotion Act. South Korea’s AI Basic Act, effective from January 2026, adds a formal trust and safety frame. China remains commercially important because enterprise AI deployment is broad, but vendor selection and governance controls vary by sector and local regulatory context.

Latin America

AI trust risk and security management market revenue in Latin America is estimated at 6.2% in 2025, or USD 0.18 Billion. Brazil leads the region as domestic AI investment, data center policy, and digital regulation move upward together. Brazil launched proposals in September 2025 to attract data-center investment and regulate digital competition, while earlier national plans had already committed roughly USD 4 Billion equivalent for AI development between 2024 and 2028. Mexico ranks second, supported by BFSI digitization, shared-services growth, and broader private-sector AI uptake, even though it still lacks a dedicated AI law. Chile is the most visible policy mover after launching an updated national AI policy and AI bill aligned with responsible-development principles. The regional market is still smaller than North America, Europe, or Asia Pacific because enterprise AI estates are narrower and local AI governance budgets remain newer. Even so, demand for privacy management, bias testing, and public-sector assurance is moving from pilot status to structured procurement.

Middle East and Africa

AI trust risk and security management market revenue in the Middle East and Africa is estimated at 6.1% in 2025, or USD 0.18 Billion. The region remains smaller in absolute revenue, but policy support is unusually strong in Gulf markets. The UAE continues to anchor regional demand through the UAE Strategy for Artificial Intelligence and the UAE Charter for the Development and Use of AI, which centers on human oversight, privacy, transparency, and responsible deployment. Saudi Arabia is building a parallel path through SDAIA guidance and government-facing generative AI guidelines, which pull spending into data governance, assurance, and model oversight. South Africa remains the largest sub-Saharan commercial buyer because financial services and telecom groups are moving AI into fraud, service, and internal productivity workflows. Israel also matters for specialized cyber and AI security technology. Across the region, public-sector programs and regulated industries will remain the first large buyers, while commercial demand widens as copilots and agents move into customer operations.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Solutions

- Services

By Deployment

- Cloud

- On-premise

By Type

- AI Application Security

- Data Protection

- Data Anomaly Detection

- Others

By Application

- Governance and Compliance

- Security and Anomaly Detection

- Privacy Management

- Bias Detection and Mitigation

By End Use

- BFSI

- Government

- IT and Telecommunication

- Healthcare

- Manufacturing

- Retail and E-commerce

- Media and Entertainment

- Others

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.88 B |

| Forecast Revenue (2034) | USD 16.38 B |

| CAGR (2025-2034) | 21.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Solutions, Services), By Deployment, (Cloud, On-premise), By Type, (AI Application Security, Data Protection, Data Anomaly Detection, Others), By Application, (Governance and Compliance, Security and Anomaly Detection, Privacy Management, Bias Detection and Mitigation), By End Use, (BFSI, Government, IT and Telecommunication, Healthcare, Manufacturing, Retail and E-commerce, Media and Entertainment, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT, IBM, GOOGLE CLOUD, PALO ALTO NETWORKS, SERVICENOW, SALESFORCE, AMAZON WEB SERVICES, DATAROBOT, CREDO AI, FIDDLER AI, SAP, SAS INSTITUTE, RAPID7, RSA SECURITY, HEWLETT PACKARD ENTERPRISE, CONCENTRIC AI, BOSCH AI SHIELD, LOGICMANAGER, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Market Size, Share, Growth & Industry Analysis By Offering (Solutions, Services), By Deployment (Cloud, On-Premise), By Type (AI Application Security, Data Protection, Data Anomaly Detection, Others), By Application (Governance & Compliance, Security & Anomaly Detection, Privacy Management, Bias Detection & Mitigation), By End-Use (BFSI, Government, IT & Telecom, Healthcare, Manufacturing, Retail & E-Commerce, Media & Entertainment) Industry Trends & Forecast 2026–2034")

Market Size, Share, Growth & Industry Analysis By Offering (Solutions, Services), By Deployment (Cloud, On-Premise), By Type (AI Application Security, Data Protection, Data Anomaly Detection, Others), By Application (Governance & Compliance, Security & Anomaly Detection, Privacy Management, Bias Detection & Mitigation), By End-Use (BFSI, Government, IT & Telecom, Healthcare, Manufacturing, Retail & E-Commerce, Media & Entertainment) Industry Trends & Forecast 2026–2034")

Market Size, Share, Growth & Industry Analysis By Offering (Solutions, Services), By Deployment (Cloud, On-Premise), By Type (AI Application Security, Data Protection, Data Anomaly Detection, Others), By Application (Governance & Compliance, Security & Anomaly Detection, Privacy Management, Bias Detection & Mitigation), By End-Use (BFSI, Government, IT & Telecom, Healthcare, Manufacturing, Retail & E-Commerce, Media & Entertainment) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the AI Trust Risk and Security Management (AI TRiSM) Market?

Global vapor recovery unit market valued at USD 1.80B in 2024, reaching USD 3.41B by 2034, growing at a CAGR of 6.6% from 2026–2034.

Who are the major players in the AI Trust Risk and Security Management (AI TRiSM) Market?

MICROSOFT, IBM, GOOGLE CLOUD, PALO ALTO NETWORKS, SERVICENOW, SALESFORCE, AMAZON WEB SERVICES, DATAROBOT, CREDO AI, FIDDLER AI, SAP, SAS INSTITUTE, RAPID7, RSA SECURITY, HEWLETT PACKARD ENTERPRISE, CONCENTRIC AI, BOSCH AI SHIELD, LOGICMANAGER, Others

Which segments covered the AI Trust Risk and Security Management (AI TRiSM) Market?

By Offering, (Solutions, Services), By Deployment, (Cloud, On-premise), By Type, (AI Application Security, Data Protection, Data Anomaly Detection, Others), By Application, (Governance and Compliance, Security and Anomaly Detection, Privacy Management, Bias Detection and Mitigation), By End Use, (BFSI, Government, IT and Telecommunication, Healthcare, Manufacturing, Retail and E-commerce, Media and Entertainment, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

AI Trust Risk and Security Management (AI TRiSM) Market

Published Date : 28 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date