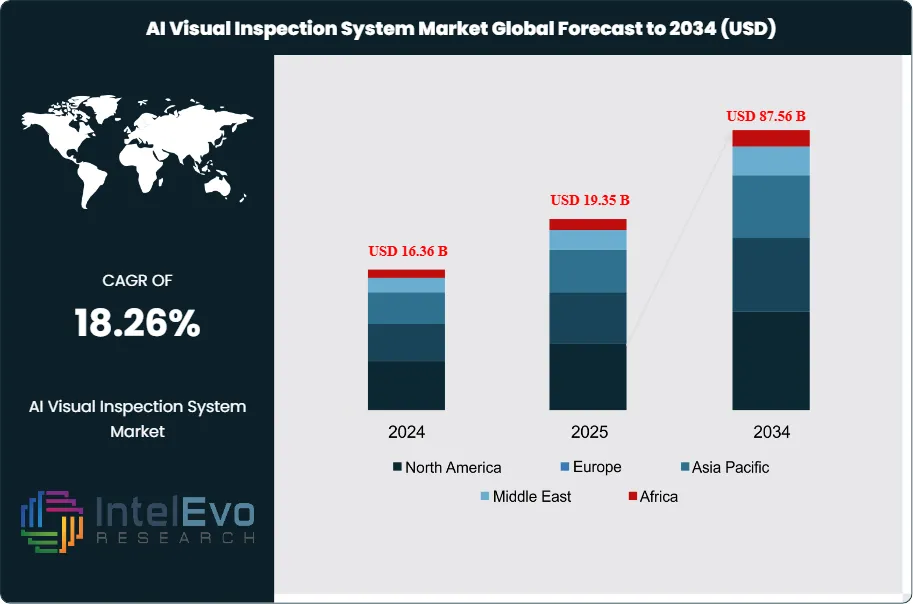

The AI Visual Inspection System Market size is expected to be worth around USD 87.56 Billion by 2034, from USD 16.36 Billion in 2024, growing at a CAGR of 18.26% during the forecast period from 2024 to 2034. The AI Visual Inspection System Market encompasses advanced technologies that integrate artificial intelligence, computer vision, and machine learning algorithms to automatically examine products, components, and processes for defects, quality issues, or inconsistencies. These systems enhance traditional manual inspection methods by providing superior accuracy, speed, and consistency in detecting anomalies across various manufacturing and industrial applications.

The market is experiencing robust growth driven by the increasing demand for automation in manufacturing processes, the proliferation of Industry 4.0 technologies, and the critical need for enhanced quality control standards. Rising labor costs, stringent regulatory requirements, and the growing complexity of manufactured products are compelling organizations to adopt AI-powered inspection solutions that can operate continuously with minimal human intervention.

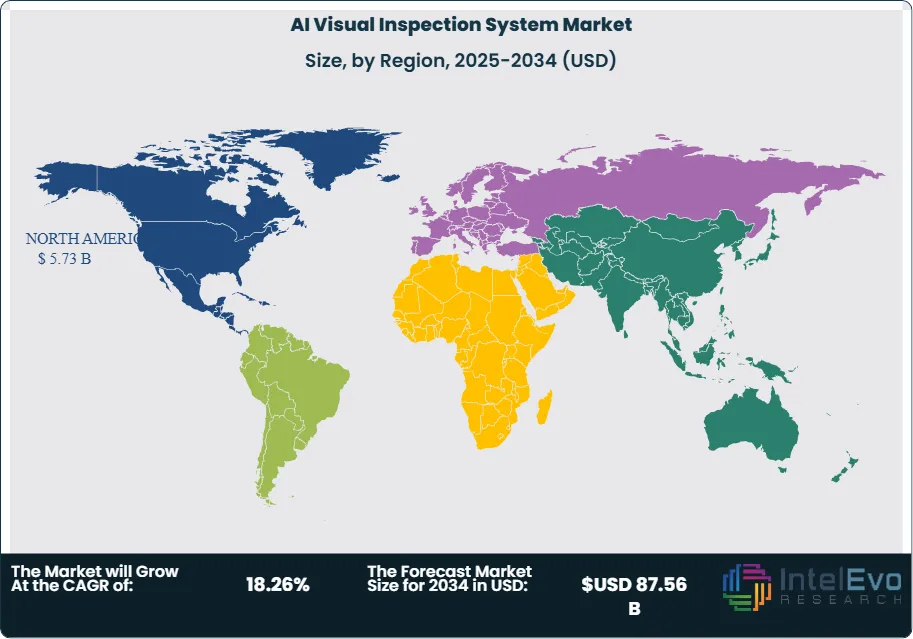

North America currently dominates the global market landscape, accounting for a substantial portion of market revenue due to early technology adoption, significant investments in automation infrastructure, and the presence of leading technology providers. The region benefits from strong manufacturing bases in automotive, electronics, and aerospace sectors, which serve as primary drivers for AI visual inspection system deployment.

The pandemic accelerated the adoption of contactless and automated inspection technologies as manufacturers sought to maintain quality standards while reducing human contact and ensuring operational continuity. Supply chain disruptions highlighted the importance of robust quality control systems, leading to increased investments in AI-powered inspection solutions that could operate independently of manual oversight.

Ongoing trade tensions and geopolitical uncertainties have intensified the focus on supply chain resilience and quality assurance. Manufacturers are investing in advanced inspection systems to ensure consistent product quality across distributed production networks and to meet varying international standards and regulatory requirements.

Key Takeaways

Market Growth: The AI Visual Inspection System Market is expected to reach USD 87.56 Billion by 2034, fueled by accelerating factory automation, widespread Industry 4.0 adoption, and heightened quality assurance demands.

System Type Dominance: Deep Learning Model segment leads the market due to superior accuracy and adaptability in pattern recognition.

Component Dominance: Hardware segment dominates the market, driven by the essential role of cameras, sensors, and processing units.

Industry Vertical Dominance: Manufacturing holds the largest share in the segment, owing to widespread automation adoption.

Drivers: Key drivers accelerating growth include Industry 4.0 adoption and automation demand, which boost market expansion through enhanced productivity and quality standards.

Restraints: Growth is hindered by high implementation costs and integration challenges, which create barriers such as capital constraints and technical complexity.

Opportunities: The market is poised for expansion due to opportunities like AI advancement and IoT integration, which enable enhanced inspection capabilities and connectivity.

Trends: Emerging trends including edge computing implementation and real-time analytics are reshaping the market by enabling faster processing and immediate decision-making.

Regional Leader: North America leads owing to technological advancement and strong manufacturing base. Asia-Pacific and Europe show high promise due to industrial growth and digitalization initiatives.

System Type Analysis:

The System Type segment represents the core technological foundation of AI visual inspection systems, encompassing Deep Learning Models, Pre-trained Models, and Other Types. Deep Learning Models have emerged as the dominant force, capturing significant market share due to their exceptional ability to learn complex patterns and adapt to new defect types without extensive reprogramming. These models excel in applications requiring nuanced pattern recognition and can continuously improve their accuracy through exposure to new data. Pre-trained Models offer faster deployment for standard inspection tasks, while Other Types include hybrid and specialized solutions for niche applications.

Component Analysis:

The Component segmentation divides the market into Hardware, Software, and Services categories, each playing a crucial role in system functionality. Hardware components, including high-resolution cameras, advanced sensors, and powerful processing units, form the backbone of visual inspection systems and represent the largest revenue contributor. Software solutions encompass AI algorithms, image processing tools, and user interfaces that enable intelligent decision-making. Services include system integration, maintenance, training, and support functions that ensure optimal system performance and user adoption across diverse industrial environments.

Industry Vertical Analysis:

Manufacturing Leads With over 40% Market Share In AI Visual Inspection System Market: The manufacturing sector dominates industrial vision because virtually every production line relies on rigorous quality assurance, rapid defect detection, and continuous process optimization. Yet no two applications are identical: automotive paint inspection demands micron-level precision in harsh shop-floor conditions, while food packaging checks prioritize split-second throughput and hygiene compliance. This wide variation compels vendors to push technological boundaries, tailoring optics, AI models, and ruggedized enclosures to meet sector-specific performance goals and evolving regulatory standards.

Regional Analysis:

North America Leads With more than 35% Market Share In AI Visual Inspection System Market: North America maintains its leadership position in the AI Visual Inspection System market, driven by substantial investments in automation infrastructure, strong presence of technology providers, and early adoption of Industry 4.0 principles. The region benefits from a mature manufacturing ecosystem spanning automotive, aerospace, electronics, and pharmaceutical sectors, all of which demand high-precision quality control solutions. Advanced research and development capabilities, coupled with favorable regulatory environments, have positioned North America as the innovation hub for AI-powered inspection technologies.

Asia-Pacific emerges as the fastest-growing region, propelled by rapid industrialization, expanding manufacturing capabilities, and increasing focus on product quality standards. Countries like China, Japan, and South Korea are investing heavily in smart manufacturing initiatives, creating substantial demand for automated inspection solutions. The region's cost-competitive manufacturing environment, combined with growing quality consciousness, drives adoption across diverse industries from electronics to automotive components.

Europe demonstrates steady growth supported by stringent quality regulations, environmental standards, and the push toward sustainable manufacturing practices. The region's emphasis on precision engineering, particularly in automotive and machinery sectors, creates consistent demand for advanced inspection technologies. Government initiatives promoting digital transformation and Industry 4.0 adoption further accelerate market expansion across European markets.

Component (Hardware, Software, Services); System Type (Deep Learning Model, Pre-trained Model, Others) Industry Vertical (Manufacturing, Semiconductors & Electronics, Healthcare, Retail, Others)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

IBM Corporation, Keyence Corporation, Alphabet Inc., Amazon.com Inc., Siemens AG, National Instruments (NI), Cognex Corporation, Fujitsu Limited, NEC Corporation, Ombrulla, Teledyne DALSA, OMRON Corporation, Basler AG

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

FIGURE 21 NORTH AMERICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 22 NORTH AMERICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE SYSTEM TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 23 NORTH AMERICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 24 U.S. AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 25 U.S. AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 26 CANADA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 27 CANADA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 28 MEXICO AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 29 MEXICO AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 30 MARKET SHARE BY COUNTRY

FIGURE 31 APAC AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 32 APAC AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE SYSTEM TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 33 APAC AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 34 CHINA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 35 CHINA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 36 JAPAN AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 37 JAPAN AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 38 KOREA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 39 KOREA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 40 INDIA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 41 INDIA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 42 SOUTHEAST ASIA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 43 SOUTHEAST ASIA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 44 MARKET SHARE BY COUNTRY

FIGURE 45 MIDDLE EAST AND AFRICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 46 MIDDLE EAST AND AFRICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE SYSTEM TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 47 MIDDLE EAST AND AFRICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 48 SAUDI ARABIA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 49 SAUDI ARABIA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 50 UAE AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 51 UAE AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 52 EGYPT AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 53 EGYPT AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 54 NIGERIA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 55 NIGERIA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 56 SOUTH AFRICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 57 SOUTH AFRICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 58 MARKET SHARE BY COUNTRY

FIGURE 59 EUROPE AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 60 EUROPE AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE SYSTEM TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 61 EUROPE AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 62 GERMANY AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 63 GERMANY AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 64 FRANCE AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 65 FRANCE AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 66 UK AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 67 UK AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 68 SPAIN AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 69 SPAIN AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 70 ITALY AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 71 ITALY AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 72 MARKET SHARE BY COUNTRY

FIGURE 73 SOUTH AMERICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 74 SOUTH AMERICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE SYSTEM TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 75 SOUTH AMERICA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 76 BRAZIL AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 77 BRAZIL AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 78 ARGENTINA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 79 ARGENTINA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 80 COLUMBIA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE COMPONENT ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 81 COLUMBIA AI VISUAL INSPECTION SYSTEM CURRENT AND FUTURE INDUSTRY VERTICAL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 82 FINANCIAL OVERVIEW:

Key Players Analysis

Cognex Corporation: Cognex maintains its position as a market leader with approximately 8-12% market share, leveraging its extensive portfolio of machine vision products and deep learning-based inspection solutions. The company's competitive edge stems from decades of experience in industrial automation, comprehensive product ecosystem spanning hardware and software solutions, and strong relationships with major manufacturing customers across automotive, electronics, and consumer goods sectors. Cognex's strategy focuses on continuous innovation in AI algorithms, expansion into new application areas, and strategic acquisitions that enhance technological capabilities and market reach.

Keyence Corporation: Keyence commands significant market presence through its integrated approach to factory automation and quality control solutions. The company differentiates itself through exceptional customer service, rapid product development cycles, and comprehensive training programs that ensure successful system implementation. Keyence's expansion strategy emphasizes geographical diversification, particularly in emerging markets, while maintaining strong positions in developed economies through continuous technology advancement and customer relationship management.

Omron Corporation: Omron leverages its broad industrial automation expertise to deliver comprehensive AI visual inspection solutions that integrate seamlessly with broader manufacturing systems. The company's competitive differentiators include deep understanding of manufacturing processes, extensive partner ecosystem, and commitment to developing solutions that address specific industry challenges. Omron's strategic focus involves expanding its AI capabilities through research partnerships, developing industry-specific solutions, and enhancing system integration capabilities.

Teledyne DALSA: Teledyne DALSA specializes in high-performance imaging and vision systems for demanding industrial applications. The company's market edge comes from advanced sensor technologies, specialized solutions for challenging inspection environments, and strong technical support capabilities. Strategic initiatives include expanding into new vertical markets, developing next-generation imaging technologies, and building partnerships with system integrators and original equipment manufacturers.

National Instruments (NI): National Instruments provides flexible platform-based approaches to visual inspection that enable customers to develop customized solutions for unique applications. The company's competitive strength lies in its modular hardware and software architecture, extensive developer community, and comprehensive educational resources. NI's strategic direction involves expanding cloud-based offerings, enhancing AI development tools, and supporting emerging technologies such as edge computing and IoT integration.

Market Key Players

IBM Corporation

Keyence Corporation

Alphabet Inc.

Amazon.com Inc.

Siemens AG

National Instruments (NI)

Cognex Corporation

Fujitsu Limited

NEC Corporation

Ombrulla

Teledyne DALSA

OMRON Corporation

Basler AG

Drivers:

Industry 4.0 and Automation Demand:

The widespread adoption of Industry 4.0 principles is fundamentally transforming manufacturing operations, creating unprecedented demand for intelligent automation solutions including AI visual inspection systems. This technological revolution emphasizes connected, smart factories where every process is optimized through data-driven insights and automated decision-making. AI visual inspection systems serve as critical components in this ecosystem, providing real-time quality monitoring, predictive maintenance capabilities, and seamless integration with other automated systems. The driver manifests through increased capital investments in smart manufacturing infrastructure, growing recognition of automation's competitive advantages, and the need to maintain quality standards while reducing labor dependency. Organizations implementing Industry 4.0 initiatives report significant improvements in production efficiency, reduced defect rates, and enhanced traceability throughout their manufacturing processes.

Rising Quality Standards and Regulatory Compliance:

Increasingly stringent quality standards and regulatory requirements across industries are compelling manufacturers to adopt more sophisticated inspection technologies. Modern consumers and business partners demand higher product quality, zero-defect manufacturing, and complete traceability of production processes. AI visual inspection systems enable manufacturers to meet these expectations by providing consistent, objective, and comprehensive quality assessment capabilities that exceed human inspection limitations. This driver gains momentum through evolving regulatory frameworks in automotive, medical devices, aerospace, and food processing industries, where quality failures can result in significant financial penalties, safety hazards, and reputational damage. The timeline for implementation typically spans 12-24 months, with strategic outcomes including improved compliance rates, reduced recall risks, and enhanced brand reputation in quality-sensitive markets.

Restraints:

High Implementation Costs and Capital Requirements:

The substantial initial investment required for AI visual inspection system implementation represents a significant barrier for many organizations, particularly small and medium-sized enterprises. These costs encompass hardware procurement, software licensing, system integration, employee training, and ongoing maintenance expenses. Advanced AI systems require high-performance computing infrastructure, specialized cameras and sensors, and custom software development to address specific inspection requirements. The financial impact extends beyond initial capital expenditure to include operational costs such as system updates, algorithm refinement, and technical support. Organizations often struggle to justify these investments due to unclear return-on-investment timelines and uncertainty about technology evolution. Mitigation strategies include phased implementation approaches, leasing arrangements, cloud-based deployment models, and government incentive programs that reduce upfront financial barriers and make advanced inspection technologies more accessible to diverse market segments.

Technical Complexity and Integration Challenges:

The sophisticated nature of AI visual inspection systems creates substantial technical hurdles that can impede adoption and successful implementation. These systems require seamless integration with existing manufacturing equipment, enterprise software systems, and quality management processes, often necessitating significant modifications to established workflows. Technical challenges include ensuring compatibility between different technology platforms, managing data flows between systems, maintaining inspection accuracy across varying environmental conditions, and addressing cybersecurity concerns in connected manufacturing environments. Historical implementation experiences reveal that projects frequently exceed planned timelines and budgets due to unforeseen technical complexities. Cross-regional impacts vary based on available technical expertise, with developed markets showing better integration success rates compared to emerging markets where technical skills may be limited. Organizations must invest in specialized training, partner with experienced system integrators, and maintain dedicated technical support resources to overcome these challenges.

Opportunities:

Edge Computing and Real-Time Processing:

The convergence of AI visual inspection systems with edge computing technologies presents substantial growth opportunities by enabling real-time processing, reduced latency, and enhanced system responsiveness. Edge computing allows inspection algorithms to process data locally, eliminating the need for cloud connectivity and reducing response times to milliseconds. This capability is particularly valuable in high-speed manufacturing environments where immediate quality decisions are critical for maintaining production efficiency. The opportunity encompasses developing specialized edge hardware optimized for AI workloads, creating lightweight algorithms suitable for edge deployment, and establishing new business models around edge-enabled inspection solutions. Market sectors affected include automotive assembly lines, electronics manufacturing, pharmaceutical production, and food processing where real-time quality control directly impacts productivity and safety. The growth potential extends to IoT integration, predictive maintenance applications, and autonomous quality management systems.

Expanding Applications in Emerging Industries:

The proliferation of AI visual inspection technology into previously untapped market segments presents significant expansion opportunities for solution providers and technology developers. Emerging applications include renewable energy component inspection, additive manufacturing quality control, agricultural product grading, and construction material assessment. These niche markets often have specialized requirements that existing solutions don't fully address, creating opportunities for customized system development and industry-specific feature enhancement. Success enablers include deep understanding of industry-specific quality requirements, partnerships with domain experts, flexible system architectures that can be adapted to unique inspection challenges, and cost-effective deployment models suitable for emerging market budgets. The opportunity extends to developing standardized inspection protocols for new industries, creating certification programs for specialized applications, and establishing service ecosystems that support technology adoption in non-traditional manufacturing environments.

Trends:

Integration of Multi-Modal Sensing Technologies:

The visual inspection industry is experiencing a transformative shift toward multi-modal sensing approaches that combine traditional visual inspection with thermal imaging, X-ray analysis, ultrasonic testing, and other sensing modalities. This integration provides comprehensive quality assessment capabilities that can detect internal defects, material composition variations, and structural anomalies invisible to conventional cameras. Advanced AI algorithms process data from multiple sensors simultaneously, creating holistic quality profiles that exceed the capabilities of any single inspection method. The trend reflects growing demands for thorough quality validation in critical applications such as aerospace components, medical devices, and automotive safety systems. Implementation requires sophisticated data fusion algorithms, multi-sensor hardware platforms, and advanced processing capabilities that can handle diverse data types in real-time manufacturing environments. This transformation enables detection of previously unidentifiable defects and supports predictive quality management approaches.

Democratization Through Cloud-Based AI Services:

The AI visual inspection market is witnessing significant democratization through cloud-based service models that make advanced inspection capabilities accessible to organizations regardless of their technical expertise or capital resources. Cloud platforms provide pre-trained AI models, scalable processing infrastructure, and user-friendly interfaces that enable rapid deployment without substantial upfront investments. This trend responds to behavioral shifts toward software-as-a-service consumption models and regulatory changes that support cloud-based manufacturing technologies. Small and medium-sized manufacturers can now access enterprise-grade inspection capabilities through subscription-based pricing models, while larger organizations benefit from reduced infrastructure management overhead and improved system scalability. The transformation includes development of industry-specific inspection templates, automated model training services, and integrated quality management platforms that connect inspection results with broader business systems and compliance reporting requirements.

Recent Development

In May 2025: UnitX, a leading innovator in artificial intelligence solutions for manufacturing environments, has introduced GenX today—a cutting-edge Generative AI system that promises to reshape how industrial vision systems identify defects. The revolutionary GenX platform addresses a critical industry challenge by creating highly detailed synthetic defect imagery using minimal training data, requiring only three authentic sample images to begin operations.

In November 2024: Rockwell Automation has announced significant enhancements to FactoryTalk Analytics VisionAI, an advanced quality inspection solution engineered to transform manufacturing quality assurance operations. During a demonstration session conducted by Amanda Thompson, who serves as product manager for the FactoryTalk Analytics VisionAI division, the enhanced platform revealed its dual capability to both detect manufacturing defects and deliver comprehensive analysis of underlying defect origins.

Frequently Asked Questions

How big is the AI Visual Inspection System Market?

he AI Visual Inspection System Market is projected to hit $87.56B by 2034, growing at a robust 18.26% CAGR. Discover key drivers and trends in this rapidly evolving market.

Who are the major players in the AI Visual Inspection System Market?

IBM Corporation, Keyence Corporation, Alphabet Inc., Amazon.com Inc., Siemens AG, National Instruments (NI), Cognex Corporation, Fujitsu Limited, NEC Corporation, Ombrulla, Teledyne DALSA, OMRON Corporation, Basler AG

Which segments covered the AI Visual Inspection System Market?

Component (Hardware, Software, Services); System Type (Deep Learning Model, Pre-trained Model, Others) Industry Vertical (Manufacturing, Semiconductors & Electronics, Healthcare, Retail, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

System Type (Deep Learning Model, Pre-trained Model, Others) Industry Vertical (Manufacturing, Semiconductors & Electronics, Healthcare, Retail, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

System Type (Deep Learning Model, Pre-trained Model, Others) Industry Vertical (Manufacturing, Semiconductors & Electronics, Healthcare, Retail, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

System Type (Deep Learning Model, Pre-trained Model, Others) Industry Vertical (Manufacturing, Semiconductors & Electronics, Healthcare, Retail, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

System Type (Deep Learning Model, Pre-trained Model, Others) Industry Vertical (Manufacturing, Semiconductors & Electronics, Healthcare, Retail, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")