- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global AI Voice Agent Market Size & Forecast 2034 | CAGR 22.2%

AI Voice Agent Market

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 4.86 Billion | USD 29.52 Billion | 22.2% | North America, 37.0% |

The AI Voice Agent Market was valued at approximately USD 3.98 Billion in 2024 and reached USD 4.86 Billion in 2025. The market is projected to grow to USD 29.52 Billion by 2034, expanding at a CAGR of 22.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 24.66 Billion over the analysis period. The AI Voice Agent Market is moving from experimental chatbot pilots to revenue-linked production systems that answer calls, verify identity, retrieve enterprise data, complete actions, and transfer context to human teams when needed. Current market assessment shows that customer service and contact center use cases account for the largest demand pool in 2025 because voice remains the highest-cost service channel in many industries and because enterprises are now buying voice automation as a business system rather than a demo feature.

Get More Information about this report -

Request Free Sample ReportThe AI Voice Agent Market is expanding because three layers of the stack matured at the same time. Speech-to-speech models improved. Enterprise orchestration tools became easier to deploy. Telephony and business-system connectors became more accessible to non-technical teams. Google Cloud introduced a rebuilt Conversational Agents product inside Customer Engagement Suite in April 2025, with human-like voices, emotional cues, and no-code agent building. Amazon introduced Nova Sonic in April 2025 as a unified speech understanding and generation model for real-time conversational applications. OpenAI advanced production-grade voice deployment with new Realtime API capabilities in August 2025, while Microsoft continued to add speech, IVR, and multi-agent features to Copilot Studio across the 2025 release cycle. These changes reduced implementation friction and widened the addressable market beyond large contact centers.

Demand remains strongest in enterprises with high call volumes, regulated workflows, and expensive live-agent labor. Platform and solution revenue accounted for 64.0% of the AI Voice Agent Market in 2025 because buyers still prioritize workflow design, model orchestration, analytics, guardrails, and channel integration over stand-alone consulting. Cloud deployment represented 73.0% of 2025 demand because fast implementation, elastic compute, and managed telephony matter more than local control in most first-wave deployments. Large enterprises led spending at 68.0% because they can absorb integration work across CRM, ERP, CCaaS, and identity systems. Still, the most attractive growth pocket now sits in upper-midmarket buyers using no-code builders and packaged templates to automate appointment setting, billing calls, claims updates, collections, and intake workflows.

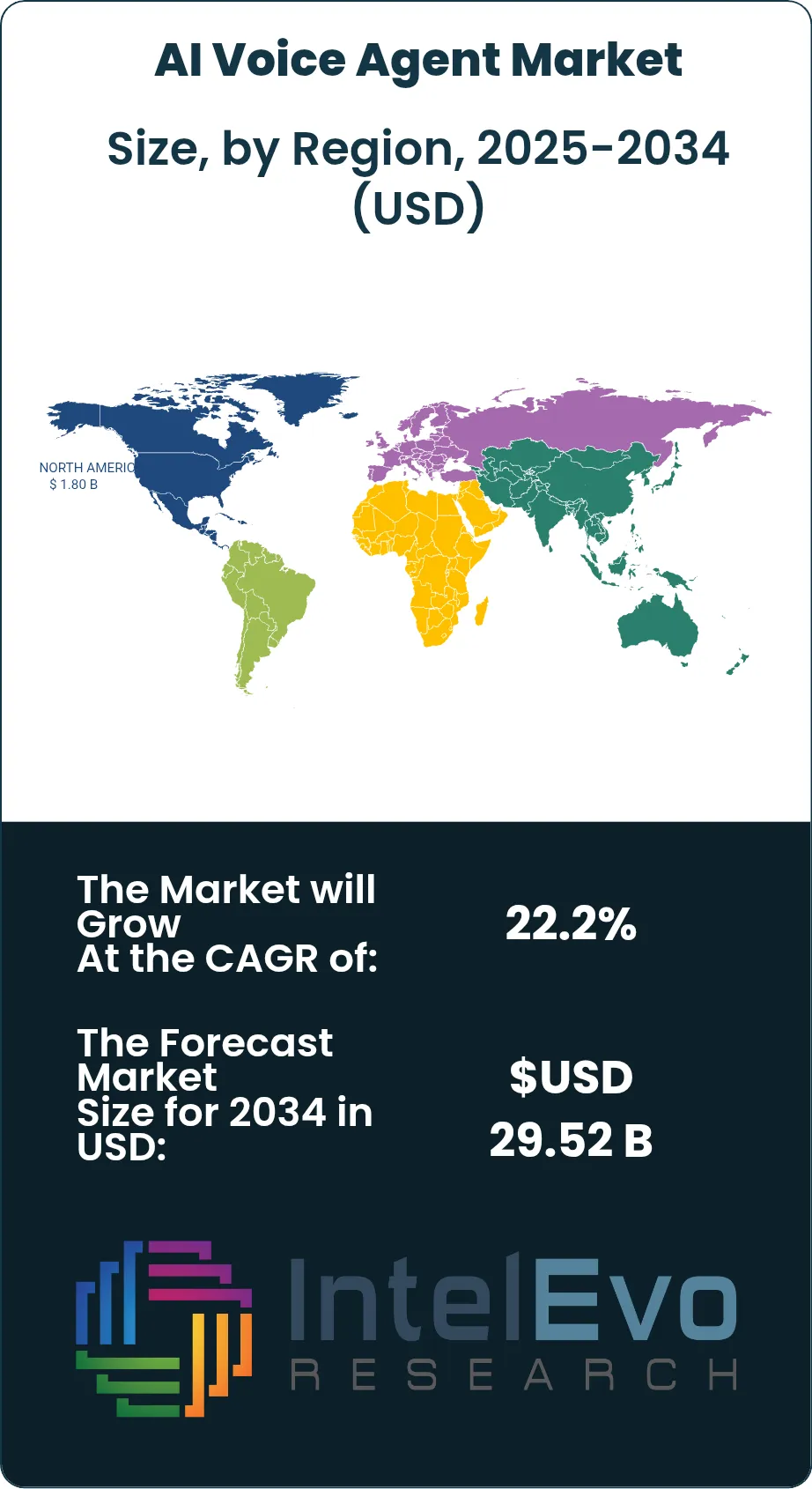

Regulation is now shaping procurement as much as model quality. The EU AI Act entered into force in August 2024, with prohibited-practice and AI-literacy provisions applying from February 2025 and broader obligations unfolding through 2026. In the United States, NIST’s AI Risk Management Framework remains the main reference point for governance, safety, transparency, and monitoring. Those rules matter directly to the AI Voice Agent Market because voice agents process personal data, make procedural decisions, and often operate inside financial, healthcare, and public-service flows. North America led global revenue with USD 1.80 Billion in 2025, but Asia Pacific is building the strongest medium-term expansion base as India, Australia, Japan, and China add enterprise AI capacity and multilingual service automation.

Key Takeaways

- Market Growth: The AI Voice Agent Market stood at USD 4.86 Billion in 2025 and is projected to reach USD 29.52 Billion by 2034, reflecting a 22.2% CAGR across 2025–2034. The market is shifting from pilot deployments to production-scale enterprise automation tied to contact center, sales, and operations workflows.

- Segment Dominance: Platform and solution revenue led the AI Voice Agent Market by offering with a 64.0% share in 2025, equal to USD 3.11 Billion. Buyers still spend most on orchestration, model control, analytics, and channel integration rather than pure implementation support.

- Segment Dominance: Customer service and contact center applications held the largest application share at 41.0% in 2025, equal to USD 1.99 Billion. That lead is supported by high call volumes, clear labor savings, and stronger demand for multilingual self-service.

- Driver: The main growth driver is the rapid improvement in real-time speech AI and enterprise orchestration. Microsoft said customers created more than 3 million AI agents in FY25, with over 1 million custom agents built in the last quarter alone, showing how fast enterprise agent adoption is spreading.

- Restraint: Governance and deployment complexity remain the main restraint. Europe accounted for 23.0% of 2025 revenue, yet procurement cycles are lengthening as firms prepare for AI Act obligations that began applying in February 2025 and continue to expand through August 2026.

- Opportunity: The largest near-term opportunity sits in regulated, voice-heavy workflows such as healthcare intake, collections, and service resolution. RingCentral’s March 2026 healthcare launch with 80+ EHR integrations shows how vertical templates can open new spend pools beyond classic contact centers.

- Trend: Real-time speech-to-speech architecture is becoming the dominant product trend. OpenAI, Amazon, Google, and Microsoft all expanded low-latency voice tooling in 2025, while cloud deployment already represented 73.0% of market demand in 2025.

- Regional Analysis: North America led the AI Voice Agent Market with 37.0% of global revenue in 2025, equal to USD 1.80 Billion. The region benefits from hyperscaler concentration, mature CCaaS demand, and faster enterprise adoption of AI governance and observability practices.

Competitive Landscape Overview

The AI Voice Agent Market is moderately consolidated, with the top four companies accounting for an estimated 31.7% of global revenue in 2025. Competition is platform-based and technology-driven. Buyers compare latency, speech quality, business-system connectivity, governance, and ease of deployment more than headline model performance alone. Competitive intensity increased across 2025 and early 2026 as Google rebuilt Conversational Agents, Amazon launched Nova Sonic, NICE introduced CXone Mpower Agents, OpenAI pushed production voice tooling, and RingCentral entered with a voice-first orchestration product.

| Company Name | Headquarters (Country) | Market Position | Key Product/Solution in this market | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Google Cloud | United States | Leader | Customer Engagement Suite / Conversational Agents | North America, Europe | Launched rebuilt Conversational Agents and expanded Verizon work in April 2025 |

| Microsoft | United States | Leader | Copilot Studio | North America, Europe | Expanded speech, IVR, and multi-agent tooling across the 2025 release cycle |

| Amazon Web Services | United States | Leader | Amazon Connect / Nova Sonic | North America, Asia Pacific | Launched Nova Sonic for real-time conversational AI in April 2025 |

| NICE | Israel | Leader | CXone Mpower Agents | North America, Europe | Launched CXone Mpower Agents in June 2025 |

| OpenAI | United States | Challenger | Realtime API / gpt-realtime | North America | Released production-focused Realtime API updates in August 2025 |

| Five9 | United States | Challenger | Five9 AI Agents / Genius AI | North America | Expanded Genius AI capabilities in November 2025 |

| Kore.ai | United States | Challenger | Kore.ai Agent Platform | Asia Pacific, North America | Formed a strategic partnership with Microsoft in May 2025 |

| Cognigy | Germany | Challenger | Cognigy.AI Voice AI Agents | Europe, North America | Partnered with TeKnowledge in July 2025 to widen global delivery reach |

| Talkdesk | United States | Niche Player | Talkdesk AI Agents for voice | North America, Europe | Launched AI Agents for voice in March 2025 |

| RingCentral | United States | Niche Player | AIR Pro | North America | Entered the market with AIR Pro in March 2026 |

Segmentation Analysis

The AI Voice Agent Market is segmented most clearly by offering, deployment, enterprise size, and application in 2025. The largest revenue pools sit where voice automation must connect directly with enterprise systems, resolve intent in real time, and work under governance controls.

By Offering:

Platform and solution revenue held 64.0% of the AI Voice Agent Market in 2025, equal to USD 3.11 Billion, while services represented 36.0%, or USD 1.75 Billion. The split shows that buyers want reusable platforms, not isolated custom projects. Platform spend covers voice orchestration, prompt and policy control, speech models, analytics, telephony connectors, guardrails, testing, and workflow tools. Services remain important, especially for data grounding, CRM integration, and call-flow redesign, but they rarely win the budget center on their own. Google’s Customer Engagement Suite, Microsoft Copilot Studio, Amazon Connect, and NICE CXone Mpower all now bundle voice handling, orchestration, and observability into packaged environments. That pulls more value into software and platform subscriptions. Service demand remains strong in complex deployments, yet margins are shifting toward vendors that can convert implementation work into recurring software revenue. This is why solution-led firms and hyperscalers hold a stronger position than pure systems integrators in the current cycle.

By Deployment:

Cloud deployment accounted for 73.0% of 2025 revenue, or USD 3.55 Billion, compared with 27.0%, or USD 1.31 Billion, for on-premise and private-cloud environments. Cloud leads because voice agents require real-time inference, elastic usage management, rapid speech model updates, and continuous testing across telephony channels. Managed cloud stacks also reduce the operational burden of scaling to thousands of simultaneous calls. On-premise demand still matters in banking, healthcare, government, and markets with strict data-residency rules, but most buyers no longer want to manage the full speech and model stack themselves. That explains why the strongest product launches in 2025 came from cloud-native platforms. Amazon linked Nova Sonic to Bedrock-era development patterns. OpenAI pushed production voice agents through the Realtime API. Google and Microsoft positioned voice tooling inside broader cloud and enterprise AI environments. The result is a deployment market where private environments remain relevant, yet public and managed cloud continue to absorb most new workloads.

By Enterprise Size:

Large enterprises represented 68.0% of the AI Voice Agent Market in 2025, equal to USD 3.30 Billion, while SMEs accounted for 32.0%, or USD 1.56 Billion. Large firms lead because they have the call volumes, data estates, and budget logic to justify enterprise-grade deployments across service, sales, billing, and internal support. They also face more pressure to document AI behavior, apply governance controls, and measure call outcomes against service metrics. That said, SME adoption is rising faster because the product stack is easier to deploy than it was a year ago. No-code builders from NICE, RingCentral, Microsoft, and Google reduce the amount of technical work needed to launch a production voice flow. Prebuilt templates, multilingual models, and direct CRM integrations are lowering the entry barrier for clinics, retailers, franchise networks, lenders, and local service providers. This shift matters because the SME segment is where the market still has the largest untapped volume pool, especially for inbound call handling and outbound scheduling.

By Application:

Customer service and contact centers led demand with 41.0% of 2025 revenue, or USD 1.99 Billion. Sales and lead qualification followed at 21.0%, or USD 1.02 Billion. Scheduling and operations represented 16.0%, or USD 0.78 Billion. Collections and reminders held 12.0%, or USD 0.58 Billion. Healthcare intake and triage accounted for 10.0%, or USD 0.49 Billion. Customer service leads because the return on automation is easiest to measure through containment rates, handle-time reduction, after-hours coverage, and lower transfer volumes. Sales and lead qualification are growing quickly because voice agents can qualify prospects, book meetings, and update CRM systems without large agent teams. Scheduling demand is rising in field service, hospitality, and outpatient care. Collections and reminders remain attractive because scripted compliance and call frequency lend themselves to automation. Healthcare is still smaller in revenue share, but it is becoming one of the strongest vertical expansion paths as vendors add workflow integrations and governed execution layers. Talkdesk supports 59 languages for AI Agents for voice, while RingCentral’s healthcare launch integrated with more than 80 EHR systems, underscoring how application depth is expanding beyond standard call deflection.

Regional Analysis

The AI Voice Agent Market shows a clear regional split in 2025. North America leads on revenue and installed enterprise software, while Asia Pacific is building the strongest long-term expansion base through multilingual service demand, AI infrastructure investment, and rapid enterprise agent adoption.

North America:

North America accounted for 37.0% of the AI Voice Agent Market in 2025, equal to USD 1.80 Billion. The United States dominates regional demand because it hosts the deepest concentration of hyperscalers, CCaaS vendors, and enterprise AI buyers. Google Cloud, Microsoft, AWS, OpenAI, Five9, Talkdesk, and RingCentral all have strong U.S. product and go-to-market positions. Canada is the second-largest regional market, supported by enterprise cloud adoption, bilingual service requirements, and growing public-sector use of governed AI workflows. Mexico remains smaller in platform spend but important in contact center operations and multilingual service delivery. The region also benefits from a stronger governance base than most peers. NIST’s AI RMF gives buyers a common risk framework, and large enterprises increasingly treat observability, audit trails, and escalation logic as standard buying criteria. North America should remain the largest revenue region through 2034 because it combines budget depth with fast product commercialization.

Europe:

Europe held 23.0% of global AI Voice Agent Market revenue in 2025, equal to USD 1.12 Billion. The United Kingdom, Germany, France, and the Netherlands drive most regional demand. The United Kingdom leads because financial services, telecom, travel, and software-led service operations adopted conversational AI earlier than many peers. Germany and France follow through regulated enterprise deployments in banking, insurance, healthcare administration, and industrial service environments. The Netherlands is gaining relevance because firms such as CM.com are commercializing agentic voice tools for round-the-clock customer interaction. Europe’s main differentiator is governance intensity. The EU AI Act is already shaping procurement, documentation, model selection, and vendor contracts, especially for firms handling voice data across borders. That creates a slower buying cycle than North America, but it also supports demand for enterprise-grade governance, data control, and multilingual performance. Europe should remain a high-value region even if implementation pace stays more measured than in the United States.

Asia Pacific:

Asia Pacific represented 26.0% of the AI Voice Agent Market in 2025, equal to USD 1.26 Billion. China, Japan, India, and Australia are the key markets. India is the most important growth engine because enterprise AI adoption is accelerating across IT services, financial services, telecom, and outsourcing-heavy service models. Microsoft said customers created more than 3 million AI agents in FY25, with India highlighted as an AI-first labor market. Google also announced an AI hub in India in October 2025, adding infrastructure and connectivity that should widen enterprise deployment capacity. Japan remains a major buyer because labor scarcity and service quality standards support automation investment. Australia is attractive for voice AI because contact center modernization and cloud adoption are both advanced. China remains relevant through large enterprise and platform-scale AI investment, though deployment patterns differ from English-speaking markets. Asia Pacific should record the fastest regional expansion through 2034 because voice remains a primary customer channel across large multilingual populations.

Latin America:

Latin America accounted for 6.0% of the AI Voice Agent Market in 2025, equal to USD 0.29 Billion. Brazil, Mexico, and Colombia are the region’s most relevant countries. Brazil leads because it combines large customer-service operations with growing demand for collections, financial-service automation, and Portuguese-language voice workflows. Mexico benefits from its role in Spanish-language service delivery and its links to North American customer experience operations. Colombia remains strategically important because it is a major multilingual outsourcing center and an early user of workflow-based service automation. Regional growth is tied less to premium enterprise orchestration and more to high-volume use cases such as appointment confirmation, payment reminders, booking support, service updates, and inbound self-service. Budget sensitivity remains higher than in North America and Europe, which keeps demand focused on cloud-based products and quick-return use cases. Vendors with multilingual support and packaged deployment paths have the clearest advantage in this region.

Middle East & Africa:

Middle East & Africa held 8.0% of global revenue in 2025, equal to USD 0.39 Billion. The UAE, Saudi Arabia, and South Africa form the main demand center. Saudi Arabia is becoming a strategic AI infrastructure location, supported by Google Cloud and PIF’s AI hub effort, which carries a stated USD 10 billion investment plan. The UAE continues to pull enterprise AI projects into finance, public services, aviation, and hospitality through faster cloud and digital-service spending. South Africa is emerging as a governed customer-experience hub. NICE launched a local dedicated CXone Mpower instance in South Africa in December 2025, which matters because data residency and low-latency access are critical for voice automation in regulated environments. The region still starts from a smaller installed base than North America or Europe, yet it is attracting higher-value projects where Arabic, English, and regional data-control requirements favor enterprise-grade voice stacks.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Platforms and Solutions

- Services

By Deployment

- Cloud

- On-Premise and Private Cloud

By Enterprise Size

- Large Enterprises

- SMEs

By Application

- Customer Service and Contact Centers

- Sales and Lead Qualification

- Scheduling and Operations

- Collections and Reminders

- Healthcare Intake and Triage

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.86 B |

| Forecast Revenue (2034) | USD 29.52 B |

| CAGR (2025-2034) | 22.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Platforms and Solutions, Services), By Deployment, (Cloud, On-Premise and Private Cloud), By Enterprise Size, (Large Enterprises, SMEs), By Application, (Customer Service and Contact Centers, Sales and Lead Qualification, Scheduling and Operations, Collections and Reminders, Healthcare Intake and Triage) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | GOOGLE CLOUD, MICROSOFT, AMAZON WEB SERVICES, NICE, OPENAI, FIVE9, KORE.AI, COGNIGY, TALKDESK, RINGCENTRAL, SALESFORCE, SERVICENOW, IBM, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Frequently Asked Questions

How big is the AI Voice Agent Market?

Global AI voice agent market valued at USD 3.98B in 2024, reaching USD 29.52B by 2034, growing at a CAGR of 22.2% from 2026–2034.

Who are the major players in the AI Voice Agent Market?

GOOGLE CLOUD, MICROSOFT, AMAZON WEB SERVICES, NICE, OPENAI, FIVE9, KORE.AI, COGNIGY, TALKDESK, RINGCENTRAL, SALESFORCE, SERVICENOW, IBM, OTHERS

Which segments covered the AI Voice Agent Market?

By Offering, (Platforms and Solutions, Services), By Deployment, (Cloud, On-Premise and Private Cloud), By Enterprise Size, (Large Enterprises, SMEs), By Application, (Customer Service and Contact Centers, Sales and Lead Qualification, Scheduling and Operations, Collections and Reminders, Healthcare Intake and Triage)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date