- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Algae-Based Food Ingredient Market Size, Share | CAGR 6.1%

Global Algae-Based Food Ingredient Market Size, Share, Analysis By Ingredient Type (Proteins, Hydrocolloids, Pigments), By Source (Microalgae, Macroalgae - Seaweed), By Application (Food & Beverages, Dietary Supplements, Animal Nutrition), By Form (Powder, Liquid, Flakes & Granules) Industry Region & Key Players – Segment Overview, Dynamics, Strategies, Sustainable Food Ingredient Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 4.48 Billion | USD 7.63 Billion | 6.1% | North America, 34.8% |

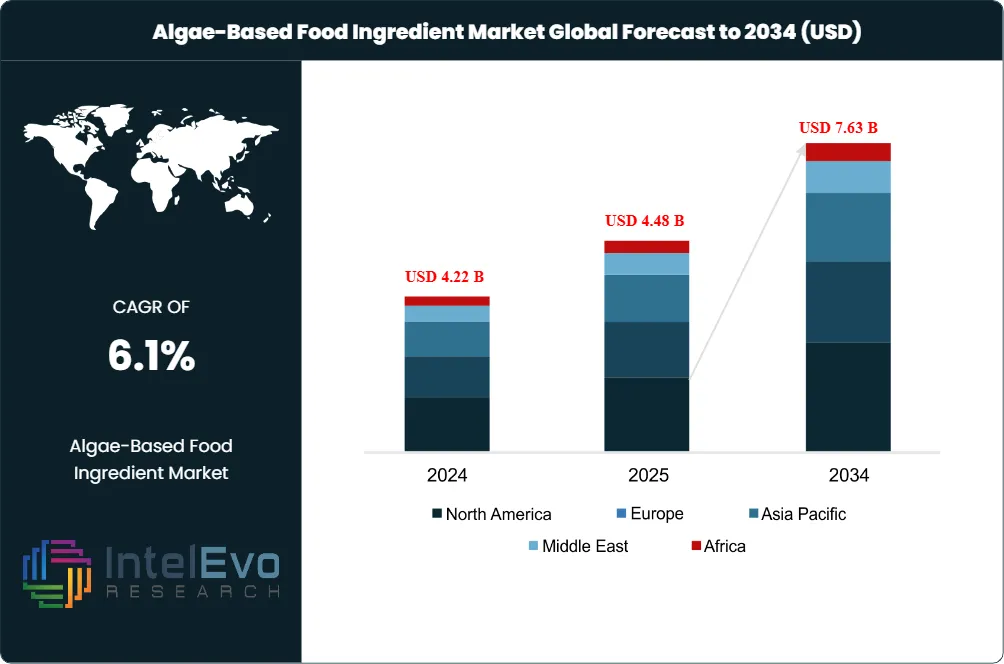

The Algae-Based Food Ingredient Market was valued at USD 4.22 Billion in 2024 and USD 4.48 Billion in 2025. The market is projected to reach USD 7.63 Billion by 2034, expanding at a CAGR of 6.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.15 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe algae-based food ingredient market is shifting from niche superfood powders toward mainstream formulation systems used by beverage, dairy alternative, confectionery, bakery, meat alternative, and infant nutrition manufacturers. Demand is anchored by three ingredient families: seaweed hydrocolloids such as carrageenan, alginate, and agar; microalgae nutrition ingredients such as spirulina, chlorella, and algae protein; and algae-derived omega-3 oils from strains such as Schizochytrium.

Global supply rests on a large aquatic biomass base. FAO reported 37.8 million tonnes of algae output in 2022, including 36.5 million tonnes from aquaculture, which gives ingredient processors a broad feedstock stream for food hydrocolloids, colorants, proteins, lipids, fibers, and minerals. The commercial issue is not biomass scarcity alone; it is the cost of consistent food-grade processing, contaminant control, flavor management, and regulatory approval across the United States, European Union, China, Japan, and India.

Regulatory activity became a direct growth catalyst in 2025 and 2026. The U.S. Food and Drug Administration cleared Galdieria extract blue for multiple food categories in May 2025 and confirmed the listing in the Federal Register in August 2025, allowing food brands to use a red-algae-derived blue color in beverages, dairy products, cereals, candies, frozen desserts, and toppings. EFSA published a safety opinion on blue galdieria extract in March 2026, strengthening the European technical file for phycocyanin-style algae color systems.

Company activity shows the same movement toward food-grade scale. Corbion reported growth in algae-derived omega-3 nutrition in 2025 and secured Chinese regulatory approvals for algae-derived DHA products in July 2025. Tate & Lyle completed the CP Kelco combination in November 2024 and reported a USD 420 Million new business pipeline by September 2025, bringing seaweed hydrocolloids closer to high-volume beverage, dairy, and sauce formulation programs. Givaudan and Fermentalg gained a stronger natural blue color position after the FDA action on Galdieria extract blue.

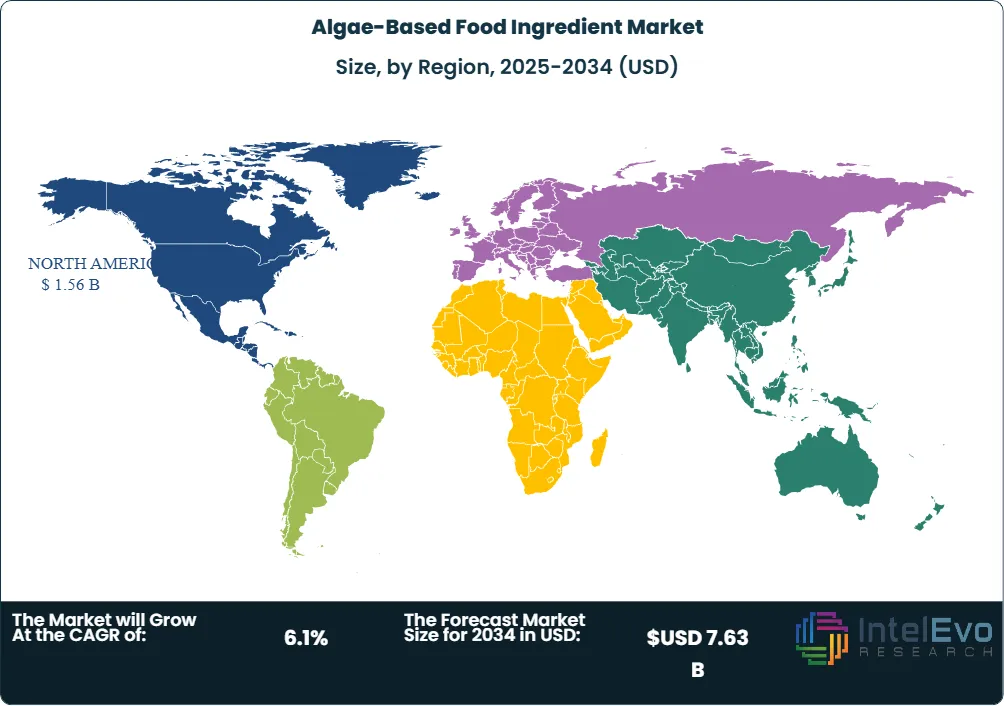

North America held the largest revenue share at 34.8% in 2025 because clean-label reformulation, synthetic dye replacement, vegan omega-3 adoption, and premium functional beverage launches created high-value demand. Asia Pacific remains the largest production base because China, Indonesia, South Korea, Japan, and the Philippines dominate seaweed cultivation and downstream carrageenan and agar supply. Through 2034, the algae-based food ingredient market should reward suppliers that can combine controlled cultivation, food-safety documentation, neutral taste, application support, and stable pricing.

Market Definition & Scope

The algae-based food ingredient market is defined as the global commercial activity around food-grade ingredients derived from macroalgae, microalgae, and cyanobacteria that are sold into food and beverage formulation. The market encompasses carrageenan, alginate, agar, spirulina, chlorella, phycocyanin, Galdieria extract blue, algae protein concentrates, algae fibers, algae oils, DHA, EPA, beta-carotene, and mineral-rich seaweed extracts.

This analysis includes ingredients used in beverages, dairy alternatives, meat and seafood alternatives, snacks, bakery, confectionery, infant nutrition, sports nutrition, meal replacements, sauces, dressings, and functional foods. It excludes algae ingredients sold primarily into cosmetics, pharmaceuticals, biofuels, fertilizers, bioplastics, and animal feed unless the same facility or product line directly supports human food ingredient commercialization. The algae-based food ingredient market sits within the broader specialty food ingredients category and overlaps with natural colors, hydrocolloids, plant-based proteins, and vegan omega-3 ingredients.

, By Source (Microalgae, Macroalgae - Seaweed), By Application (Food & Beverages, Dietary Supplements, Animal Nutrition), By Form (Powder, Liquid, Flakes & Granules) Industry Region & Key Players – Segment Overview, Dynamics, Strategies, Sustainable Food Ingredient Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The algae-based food ingredient market reached USD 4.48 Billion in 2025 and is projected to reach USD 7.63 Billion by 2034 at a 6.1% CAGR, adding USD 3.15 Billion in incremental revenue.

- Segment Dominance: Hydrocolloids held 42.6% share in 2025, equal to USD 1.91 Billion, because carrageenan, alginate, and agar remain embedded in dairy, confectionery, meat, and beverage stabilization systems.

- Segment Dominance: Food and beverage manufacturers represented 52.4% of 2025 demand, ahead of nutraceutical and dietary supplement brands at 28.8%, because hydrocolloids and natural colors serve higher-tonnage processed-food use cases.

- Driver: Synthetic dye replacement accelerated after the FDA cleared Galdieria extract blue in May 2025, giving manufacturers a new algae-derived blue color option for more than 15 food and beverage categories.

- Restraint: Production cost remains the primary constraint, with food-grade microalgae protein still priced at several multiples of soy, pea, and wheat protein because photobioreactors, drying, extraction, and flavor masking add processing cost.

- Opportunity: Algae-derived omega-3 and natural color systems create a combined 2034 opportunity above USD 2.20 Billion because infant nutrition, functional beverages, gummies, dairy alternatives, and confectionery brands need vegan DHA, EPA, and stable blue-green hues.

- Trend: Vertically integrated fermentation and controlled cultivation are replacing open-pond dependence for premium products, as Corbion, Fermentalg, Givaudan, DIC Corporation, and MiAlgae prioritize supply consistency and contaminant control.

- Regional: North America led the algae-based food ingredient market with 34.8% share and USD 1.56 Billion in 2025, while Asia Pacific posted the highest long-term growth because it combines seaweed cultivation scale with rising fortified-food consumption.

Key Insights Summary

- FAO measured global algae production at 37.8 million tonnes in 2022, with aquaculture contributing 36.5 million tonnes, giving food ingredient suppliers the largest non-terrestrial biomass stream in aquatic agriculture.

- The FDA added Galdieria extract blue to the color additive list in 2025, creating a permitted algae-derived blue color route for beverages, dairy drinks, cereals, candies, frozen desserts, puddings, and whipped toppings.

- EFSA reviewed blue galdieria extract in March 2026 and identified C-phycocyanin as more than 25% of the extract, supporting European safety assessment work for microalgae-derived blue color systems.

- Spirulina commonly contains 60% to 70% protein by dry weight, which makes it one of the densest non-animal protein ingredients used in powders, bars, beverages, pasta, snacks, and seafood alternatives.

- Corbion reported 2025 growth in its algae-derived omega-3 business and stated that AlgaVia serves human nutrition applications, while AlgaPrime DHA supports aquaculture and companion-animal nutrition.

- Tate & Lyle reported a USD 420 Million new business pipeline at 30 September 2025 after integrating CP Kelco, indicating that pectin, carrageenan, alginate, and other mouthfeel systems remain central to food reformulation.

- NOAA identifies seaweed farming as the fastest-growing aquaculture sector in the United States, while Alaska output grew 200% between the first commercial harvest in 2017 and 2019, supporting domestic kelp ingredient pilots.

Competitive Landscape Overview

The algae-based food ingredient market is moderately consolidated in hydrocolloids and fragmented in microalgae protein, natural colors, and culinary algae oils. The top four commercial groups, Tate & Lyle with CP Kelco, Corbion N.V., Cargill Incorporated, and Givaudan SA with Fermentalg-linked color capabilities, account for approximately 38% of 2025 revenue across food-grade algae-derived ingredient categories.

Competition differs by ingredient family. Hydrocolloid suppliers compete on seaweed sourcing, extraction yield, texture performance, and global regulatory support. Microalgae nutrition suppliers compete on strain productivity, taste neutrality, protein concentration, omega-3 purity, and documented heavy-metal control. Color suppliers compete on shade stability, pH tolerance, heat resistance, and exemption from certification in U.S. color rules.

The next competitive shift is toward application-ready systems rather than raw biomass. Food manufacturers want algae ingredients that work in acidic beverages, frozen desserts, dairy alternatives, plant-based seafood, gummies, and low-sugar sauces without marine off-notes. Vendors with pilot plants, sensory teams, and customer co-development labs will outgrow commodity biomass suppliers through 2034.

Competitive Landscape Matrix

| Company Name | Headquarters (Country) | Market Position | Key Product/Solution in this market | Geographic Strength | Recent Strategic Move |

| Tate & Lyle PLC / CP Kelco | United Kingdom / United States | Leader | GENU carrageenan, KELCOGEL, alginate and seaweed hydrocolloid systems | North America, Europe, Asia | Reported USD 420 Million new business pipeline by September 2025 after CP Kelco combination |

| Corbion N.V. | Netherlands | Leader | AlgaVia DHA, AlgaPrime DHA, algae-derived omega-3 oils | Europe, North America, China | Secured Chinese approvals for algae-derived DHA products in July 2025 |

| Cargill Incorporated | United States | Leader | Algae-based DHA for early life nutrition and specialized nutrition | North America, Europe, Asia | Expanded algae DHA sourcing through MARA-linked specialized nutrition programs |

| Givaudan SA | Switzerland | Leader | Everzure Galdieria natural blue color system | Europe, North America | Gained stronger U.S. color access after FDA clearance in May 2025 |

| DIC Corporation | Japan | Challenger | LINABLUE phycocyanin spirulina color | Japan, Europe, North America | Published 2026 technical communication on phycocyanin stability and spirulina nutrition |

| Cyanotech Corporation | United States | Challenger | Hawaiian Spirulina, BioAstin astaxanthin | United States, Asia | Continued positioning around Hawaiian open-pond spirulina and astaxanthin supply |

| Earthrise Nutritionals LLC | United States | Challenger | Earthrise spirulina powders and tablets | United States, Europe | Maintained food and supplement spirulina supply for clean-label brands |

| Algama Foods | France | Niche Player | Tamalga microalgae protein and food formulation platform | Europe, North America | Scaled Belgian biorefinery work after Series A funding support |

| AlgaeCore Technologies / SimpliiGood | Israel | Niche Player | Simplii Texture spirulina protein for seafood alternatives | Europe, Israel, United States | Advanced spirulina smoked salmon pilots after 2025 funding and EU clearance |

| MiAlgae Ltd. | United Kingdom | Niche Player | Algae-derived omega-3 from whisky co-products | United Kingdom, Europe | Moved Grangemouth facility toward Q2 2026 start-up for omega-3 scale-up |

By Ingredient Type

The algae-based food ingredient market by ingredient type is led by hydrocolloids, which held 42.6% share in 2025 and generated USD 1.91 Billion. Carrageenan, alginate, and agar are mature ingredients, but their use is expanding because dairy processors, plant-based beverage brands, confectionery makers, and meat processors need texture systems that replace animal gelatin, reduce fat, and stabilize protein suspensions. Tate & Lyle, CP Kelco, Cargill, Hispanagar, and Gino Biotech compete through extraction efficiency, seaweed sourcing, and application labs. Hydrocolloids grow slower than algae protein and colorants, but they carry the largest base because food manufacturers buy them by function, not by algae story.

Algae oils and omega-3 ingredients accounted for 24.7% share and USD 1.11 Billion in 2025. Corbion, Cargill, DSM-Firmenich, Bioriginal, and MiAlgae address infant nutrition, supplements, functional beverages, gummies, and plant-based seafood with DHA and EPA ingredients that avoid fish-oil taste and overfishing exposure. The segment benefits from vegan positioning and supply-chain resilience, but purification cost and oxidation control determine margins. Algae omega-3 growth outpaces hydrocolloids because brand owners can charge premiums for brain, eye, maternal, and healthy-aging claims.

Microalgae proteins, whole biomass powders, fibers, pigments, beta-carotene, and mineral extracts represented the remaining 32.7% in 2025. Spirulina, chlorella, and Galdieria-derived systems are moving from supplement shelves into pasta, bars, beverage powders, snacks, bakery, and seafood alternatives. Algama, SimpliiGood, DIC Corporation, Givaudan, Fermentalg, Cyanotech, and Earthrise compete through protein density, color performance, neutral taste, and regulatory dossiers. The fastest growth occurs where algae ingredients solve a formulation problem, such as stable blue color or fish-free seafood texture, rather than acting only as a nutrition badge.

By Source

Macroalgae, or seaweed, led the algae-based food ingredient market by source with 58.8% share in 2025, equal to USD 2.63 Billion. Brown and red seaweed dominate carrageenan, alginate, and agar supply because China, Indonesia, the Philippines, South Korea, Chile, and France maintain established harvest and cultivation chains. CP Kelco, Cargill, Hispanagar, Algaia, and Gino Biotech convert seaweed into texturizing systems for dairy, confectionery, meat, and beverage products. Macroalgae’s advantage is tonnage scale; its risk is climate-linked crop variability, coastal permitting, iodine control, and geopolitical concentration in Asian supply chains.

Microalgae and cyanobacteria held 41.2% share and USD 1.85 Billion in 2025. Spirulina, chlorella, Schizochytrium, Haematococcus, Dunaliella, and Galdieria are used for proteins, omega-3 oils, colors, carotenoids, and antioxidant ingredients. Corbion, DIC Corporation, Givaudan, Fermentalg, Cyanotech, Earthrise, Algama, and MiAlgae use controlled ponds, fermentation, or photobioreactors to improve consistency. Microalgae will grow faster than macroalgae through 2034 because precision fermentation and closed cultivation allow food companies to document contaminants, allergens, traceability, and functional performance more tightly.

By Application

Food and beverage processing led the algae-based food ingredient market by application with 52.4% share in 2025, equivalent to USD 2.35 Billion. Beverage, dairy alternative, confectionery, bakery, sauce, dressing, and frozen dessert manufacturers use seaweed hydrocolloids for viscosity, suspension, gel strength, and freeze-thaw stability. Tate & Lyle, CP Kelco, Cargill, Givaudan, and DIC Corporation support this channel through formulation labs and regulatory teams. The buyer’s procurement checklist usually covers carrageenan grade, pH stability, allergen status, heavy-metal limits, color fastness, sensory impact, and supplier redundancy.

Nutraceuticals and dietary supplements represented 28.8% share and USD 1.29 Billion in 2025. Spirulina tablets, chlorella powders, astaxanthin capsules, algae DHA softgels, gummies, and meal-replacement powders give supplement brands plant-based claims and measurable nutrient density. Corbion, DSM-Firmenich, Bioriginal, Cyanotech, Earthrise, and Taiwan Chlorella compete in this segment. Supplements carry higher gross margins than commodity food systems, but claims must be supported by composition testing, oxidation data, and country-specific rules on nutrition and health communication.

Plant-based meat, seafood alternatives, and infant and specialized nutrition accounted for 18.8% share and USD 0.84 Billion in 2025. SimpliiGood uses spirulina texture to target smoked salmon analogs, Algama supplies microalgae protein systems, and Corbion and Cargill serve DHA needs in early life nutrition. These applications have higher technical barriers because consumers notice marine flavor, color drift, aroma, and texture failure quickly. By 2034, seafood alternatives and infant nutrition should generate the highest dollar growth because algae ingredients directly replace fish-derived inputs.

By Form

Powders led the algae-based food ingredient market by form with 46.9% share in 2025, equal to USD 2.10 Billion. Spirulina, chlorella, carrageenan, alginate, agar, and beta-carotene powders are easier to ship, blend, dose, and store than fresh biomass or wet pastes. Cyanotech, Earthrise, CP Kelco, Hispanagar, DIC Corporation, and Gino Biotech rely on drying, milling, and packaging controls to protect color, protein, and gelling strength. Powder demand remains high because contract manufacturers can add it into dry beverage bases, bars, instant soups, bakery mixes, and gummies.

Liquid oils and emulsions held 31.4% share and USD 1.41 Billion in 2025, led by algae DHA and EPA systems used in infant nutrition, supplements, beverages, and functional foods. Corbion, Cargill, DSM-Firmenich, Bioriginal, and MiAlgae compete on oxidation management, solvent-free extraction claims, sensory profile, and documentation for vegan omega-3 positioning. Fresh, frozen, and paste forms captured 21.7% share, led by fresh seaweed, wet spirulina, and texturized microalgae ingredients. Liquid and fresh forms will grow faster through 2034 because they preserve color and texture, but they require cold-chain and shelf-life planning.

Regional Analysis

North America led the algae-based food ingredient market with 34.8% share and USD 1.56 Billion in 2025. The United States accounted for most regional demand because FDA food color actions, clean-label reformulation, dairy alternative innovation, and vegan omega-3 supplement growth created high-value opportunities. Corbion, Cargill, CP Kelco, Givaudan, Cyanotech, Earthrise, and SimpliiGood’s U.S. approval pathway shape regional competition. NOAA support for seaweed aquaculture and state programs in Alaska, Maine, and Connecticut encourage domestic kelp cultivation, although Asian supply still dominates seaweed hydrocolloid inputs.

Europe held 27.1% share and USD 1.21 Billion in 2025. Germany, France, the United Kingdom, the Netherlands, Spain, and Denmark drive demand through natural-color reformulation, plant-based seafood, clean-label dairy, and EU Novel Food compliance pathways. EFSA’s March 2026 blue galdieria extract safety opinion strengthened the technical basis for algae color adoption, while Algaia, Algama, Fermentalg, Givaudan, DSM-Firmenich, and MiAlgae support regional supply. Europe’s stricter additive and contaminant rules raise entry costs but also reward suppliers with strong dossiers.

Asia Pacific accounted for 28.6% share and USD 1.28 Billion in 2025 and remains the fastest-growing region through 2034. China, Japan, South Korea, Indonesia, the Philippines, India, and Australia combine production scale with rising fortified-food consumption. FAO data show Asia dominates aquaculture output, giving the region unmatched seaweed feedstock strength. Corbion’s July 2025 Chinese approvals for algae-derived DHA products show how regulatory access can turn supply scale into branded nutrition revenue. Japan and South Korea also support premium seaweed foods and algae color applications.

Latin America represented 5.8% share and USD 0.26 Billion in 2025. Brazil, Chile, Mexico, Peru, and Colombia are the main country markets, supported by beverage growth, dairy processing, seaweed harvesting, and nutraceutical retail. Chile provides seaweed inputs for alginate and agar supply chains, while Brazil’s functional food sector uses spirulina and algae oils in supplements and sports nutrition. Regional adoption remains price sensitive because imported algae DHA and phycocyanin cost more than soy protein, synthetic colors, and conventional emulsifiers.

Middle East and Africa held 3.7% share and USD 0.17 Billion in 2025. The Gulf states, South Africa, Morocco, Egypt, and Israel are the main demand nodes. Israel’s AlgaeCore Technologies supports spirulina-based seafood alternatives, while Gulf food manufacturers evaluate algae ingredients for premium beverages, nutrition powders, and clean-label confectionery. Africa has coastal biomass potential, but food-grade extraction capacity, cold-chain infrastructure, and regulatory testing remain limited. The region should grow from a small base as fortified foods and alternative proteins move into modern retail.

Country Analysis

The United States algae-based food ingredient market reached USD 1.34 Billion in 2025 and is forecast to grow at a 5.9% CAGR through 2034. Demand is driven by FDA action on Galdieria extract blue, synthetic dye replacement programs, vegan omega-3 supplements, and plant-based dairy and seafood innovation. Corbion, Cargill, CP Kelco, Givaudan, Cyanotech, Earthrise, and Algae Cooking Club support product availability. NOAA and USDA activity around seaweed aquaculture helps domestic kelp pilots, but carrageenan, agar, and alginate supply still depends heavily on Asian and Latin American seaweed flows.

China’s algae-based food ingredient market reached USD 0.55 Billion in 2025 and is projected to grow at a 7.2% CAGR through 2034. China combines large seaweed cultivation, domestic hydrocolloid production, functional beverage growth, and dietary supplement expansion. Corbion’s July 2025 Chinese regulatory approvals for algae-derived DHA products open a clearer route for human and animal nutrition applications. Chinese suppliers including Gino Biotech and local spirulina producers compete on cost, while multinational food brands require stronger contaminant documentation for exports.

Japan’s algae-based food ingredient market reached USD 0.31 Billion in 2025 and is forecast to grow at a 5.8% CAGR through 2034. Seaweed consumption is culturally established through nori, wakame, kombu, and agar-based products, giving Japanese consumers higher familiarity than most Western markets. DIC Corporation supplies LINABLUE phycocyanin, while domestic food manufacturers use agar, alginate, and seaweed powders in desserts, noodles, snacks, and functional foods. Japan’s aging population supports demand for algae minerals, dietary fiber, omega-3, and lower-calorie texture systems.

Germany’s algae-based food ingredient market reached USD 0.25 Billion in 2025 and is projected to grow at a 6.4% CAGR through 2034. German demand is shaped by clean-label retail standards, vegan product launches, EU Novel Food compliance, and natural color replacement in confectionery, dairy alternatives, and beverages. Givaudan, Fermentalg, DSM-Firmenich, Algaia, and Tate & Lyle serve multinational manufacturers from European technical centers. German buyers are strict on heavy metals, iodine, pesticide residues, allergen controls, and sustainability documentation, which favors suppliers with audited cultivation and extraction chains.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Ingredient Type

- Proteins

- Hydrocolloids

- Pigments

- Others

By Source

- Microalgae

- Macroalgae (Seaweed)

- Others

By Application

- Food & Beverages

- Dietary Supplements

- Animal Nutrition

- Others

By Form

- Powder

- Liquid

- Flakes & Granules

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.48 B |

| Forecast Revenue (2034) | USD 7.63 B |

| CAGR (2025-2034) | 6.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Ingredient Type, (Proteins, Hydrocolloids, Pigments, Others), By Source, (Microalgae, Macroalgae (Seaweed), Others), By Application, (Food & Beverages, Dietary Supplements, Animal Nutrition, Others), By Form, Powder, (Liquid, Flakes & Granules, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TATE & LYLE PLC / CP KELCO, CORBION N.V., CARGILL INCORPORATED, GIVAUDAN SA, DIC CORPORATION, DSM-FIRMENICH AG, CYANOTECH CORPORATION, EARTHRISE NUTRITIONALS LLC, HISPANAGAR S.A., ALGAIA S.A., ALGAMA FOODS, ALGAECORE TECHNOLOGIES LTD. / SIMPLIIGOOD, MI ALGAE LTD., FERMENTALG SA, TAIWAN CHLORELLA MANUFACTURING COMPANY, GINO BIOTECH, BIORIGINAL FOOD & SCIENCE CORP., ALGAE COOKING CLUB, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Source (Microalgae, Macroalgae - Seaweed), By Application (Food & Beverages, Dietary Supplements, Animal Nutrition), By Form (Powder, Liquid, Flakes & Granules) Industry Region & Key Players – Segment Overview, Dynamics, Strategies, Sustainable Food Ingredient Trends & Forecast 2026-2034")

, By Source (Microalgae, Macroalgae - Seaweed), By Application (Food & Beverages, Dietary Supplements, Animal Nutrition), By Form (Powder, Liquid, Flakes & Granules) Industry Region & Key Players – Segment Overview, Dynamics, Strategies, Sustainable Food Ingredient Trends & Forecast 2026-2034")

, By Source (Microalgae, Macroalgae - Seaweed), By Application (Food & Beverages, Dietary Supplements, Animal Nutrition), By Form (Powder, Liquid, Flakes & Granules) Industry Region & Key Players – Segment Overview, Dynamics, Strategies, Sustainable Food Ingredient Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Algae-Based Food Ingredient Market?

The Global Algae-Based Food Ingredient Market was valued at USD 4.22 Billion in 2024 and USD 4.48 Billion in 2025, and is projected to reach USD 7.63 Billion by 2034, growing at a CAGR of 6.1% from 2026 to 2034. Market growth is driven by plant-based nutrition, sustainable food ingredients, and functional food innovations.

Who are the major players in the Algae-Based Food Ingredient Market?

TATE & LYLE PLC / CP KELCO, CORBION N.V., CARGILL INCORPORATED, GIVAUDAN SA, DIC CORPORATION, DSM-FIRMENICH AG, CYANOTECH CORPORATION, EARTHRISE NUTRITIONALS LLC, HISPANAGAR S.A., ALGAIA S.A., ALGAMA FOODS, ALGAECORE TECHNOLOGIES LTD. / SIMPLIIGOOD, MI ALGAE LTD., FERMENTALG SA, TAIWAN CHLORELLA MANUFACTURING COMPANY, GINO BIOTECH, BIORIGINAL FOOD & SCIENCE CORP., ALGAE COOKING CLUB, OTHERS

Which segments covered the Algae-Based Food Ingredient Market?

By Ingredient Type, (Proteins, Hydrocolloids, Pigments, Others), By Source, (Microalgae, Macroalgae (Seaweed), Others), By Application, (Food & Beverages, Dietary Supplements, Animal Nutrition, Others), By Form, Powder, (Liquid, Flakes & Granules, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Algae-Based Food Ingredient Market

Published Date : 08 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date