- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Amniotic Membrane Market Size, Share & Forecast | CAGR 12.3%

Global Amniotic Membrane Market Size, Share, Analysis By Product Type (Cryopreserved, Dehydrated Amniotic Membranes), By Application (Surgical Wounds, Ophthalmology, Orthopedics, Other Applications), By End-Use (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Research Institutes), Industry Overview, Market Dynamics, Competitive Landscape, Key Players, Regional Insights, Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

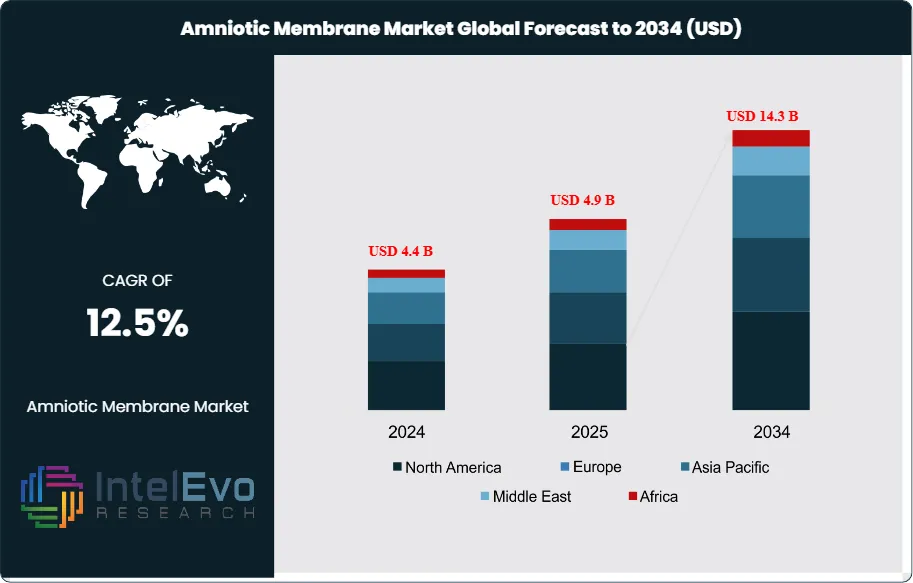

| USD 4.9 Billion | USD 14.3 Billion | 12.5% | North America, 35.2% |

The Amniotic Membrane Market is estimated at USD 4.4 Billion in 2024 and is on track to reach roughly USD 14.3 Billion by 2034, The market is further estimated to reach approximately USD 4.9 Billion in 2025, and is expected to expand at a compound annual growth rate (CAGR) of around 12.5% during the forecast period from 2026 to 2034. Growth is driven by increasing adoption of regenerative medicine, rising demand for advanced wound care solutions, and expanding applications in ophthalmology, orthopedics, and surgical procedures. Additionally, advancements in tissue preservation technologies and growing awareness of biologics-based therapies are further supporting market expansion globally.

Get More Information about this report -

Request Free Sample ReportGrowth reflects a sustained move toward biologic repair in ophthalmology, surgery, and advanced wound care. Providers use amniotic membranes because the tissue supports epithelialization, helps limit microbial burden, and reduces pain at the treatment site. Utilization continues to expand across diabetic foot ulcers, venous leg ulcers, pressure injuries, corneal ulcers, pterygium excision, and limbal stem cell deficiency care. Chronic wound management is estimated to represent about 55% of 2024 revenue, supported by rising diabetes prevalence and longer wound duration, while ophthalmology contributes roughly 30% as outpatient eye procedures scale.

Supply remains tightly linked to donated placental tissue availability, recovery-network coverage, and accredited processing capacity. Tissue banks and manufacturers invest in donor screening, sterility assurance, and standardized handling to improve lot consistency and shorten release timelines. Regulation shapes both risk and cost. In the United States, FDA requirements for human cells and tissue products, donor eligibility rules, and state tissue-banking oversight increase documentation and quality-control intensity. In Europe, tissue directives and device compliance expectations strengthen traceability and post-market vigilance. Reimbursement variability remains a central commercial constraint, with payers tightening documentation requirements and driving price discipline in commoditized wound indications.

Technology upgrades increasingly determine scale economics and product performance. Automation in aseptic processing and packaging reduces contamination events and increases throughput. Digital quality management systems compress deviation closure cycles and improve audit readiness. AI-driven analytics support donor-risk triage, demand forecasting, and site-level utilization tracking, which improves inventory placement and reduces expiries. Product innovation also advances through improved decellularization control, cryopreservation methods, and shelf-stable formats that simplify storage and broaden point-of-care access.

Regionally, the United States leads with an estimated 40% revenue share in 2024, supported by high procedure volumes and more established coverage for select wound indications. Europe contributes about 30%, driven by ophthalmology and structured hospital procurement. Asia-Pacific approaches 25% and posts the fastest growth as tissue-banking capacity expands and private wound-care networks scale; China, India, and Southeast Asia stand out as investment hotspots. Key risks include donor supply shocks, compliance failures, and substitution pressure from synthetic or collagen-based alternatives as buyers standardize formularies.

, By Application (Surgical Wounds, Ophthalmology, Orthopedics, Other Applications), By End-Use (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Research Institutes), Industry Overview, Market Dynamics, Competitive Landscape, Key Players, Regional Insights, Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: Market value rises from 3.9 billion USD, 2023 to 12.7 billion USD, 2033, implying 12.5% CAGR, 2026-2034. This trajectory signals sustained demand expansion across clinical wound care and ocular repair, estimated: 14.3 billion USD, 2034.

- Segment Dominance: Cryopreserved amniotic membrane leads product mix at 57.0% revenue share, 2023. This leadership reflects higher clinical acceptance and established cold-chain distribution, estimated: 58.0% revenue share, 2024.

- Segment Dominance: Surgical wounds lead applications at 40.2% revenue share, 2023. Hospitals anchor demand concentration at 39.5% end-use share, 2023, indicating strong acute-care procurement power, estimated: 40.0% share, 2024.

- Driver: Rising transplant volumes expand tissue-based product utilization, estimated: 6.0% procedure growth, 2024. Expanded donor recovery and improved processing quality lift usable tissue supply, estimated: 4.0% yield improvement, 2024.

- Restraint: Tightening donor screening and tissue-handling compliance elevates operating costs, estimated: 8.0% cost inflation, 2024. Reimbursement variability and documentation requirements slow adoption velocity, estimated: 10.0% claim-denial rate, 2024.

- Opportunity: Regenerative medicine therapy development expands addressable revenue, estimated: 1.2 billion USD, 2030. New adjacencies in cosmetics and dentistry create incremental growth lanes, estimated: 0.6 billion USD, 2034.

- Trend: Manufacturers accelerate new amniotic membrane product development across indications, estimated: 15.0% R&D budget growth, 2024. Emerging economies increase adoption as distribution and affordability improve, estimated: 14.0% volume growth, 2024.

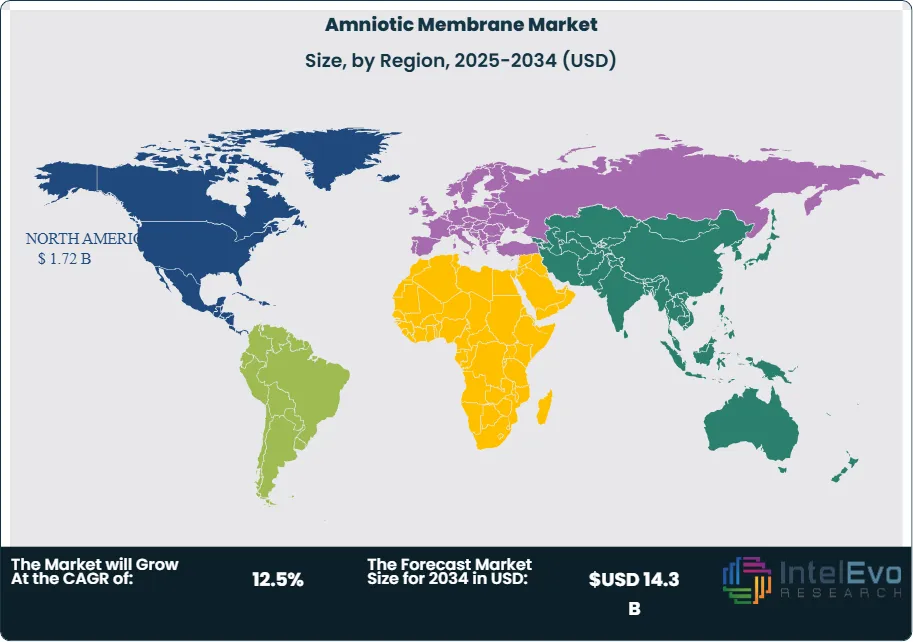

- Regional Analysis: North America leads with 35.2% revenue share, 2023 and 1.4 billion USD, 2023. Investment hotspots expand in Asia-Pacific as tissue banking and private wound-care networks scale, estimated: 25.0% revenue share, 2024.

Competitive Landscape

The Global Amniotic Membrane Market is moderately consolidated, with the top five companies accounting for an estimated 45.0%–52.0% of 2025 market revenue. Competition is innovation-driven and clinically validated, where tissue processing technology, regulatory compliance, product differentiation (cryopreserved vs dehydrated), and physician adoption shape market share more than pricing. Competitive intensity increased in 2025–2026 as companies expanded regenerative portfolios, invested in advanced preservation technologies, and strengthened distribution across wound care, ophthalmology, and surgical applications.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| SMITH & NEPHEW | UK | Leader | Advanced wound care and amniotic membrane-based products | North America, Europe | Expanded regenerative wound care portfolio and biologics segment in 2025. |

| ORGANOGENESIS | US | Leader | Amniotic and placental-derived wound care solutions | North America | Strengthened advanced wound care product portfolio and distribution in 2025. |

| MIIMEDX GROUP | US | Leader | Placental tissue allografts and regenerative therapies | North America | Expanded product pipeline and improved reimbursement positioning in 2025. |

| ALLIQUA BIOMEDICAL | US | Leader | Advanced wound care and biologic tissue products | North America | Focused on expanding wound care distribution channels in 2025. |

| COOK BIOTECH | US | Leader | Biologic grafts and regenerative tissue solutions | North America, Europe | Expanded surgical and wound care applications in 2025. |

| AMNIO TECHNOLOGY | US | Challenger | Cryopreserved and dehydrated amniotic membrane products | North America | Expanded production capacity and product portfolio in 2025. |

| SKYE BIOLOGICS | US | Challenger | Placental tissue products for surgical and wound care use | North America | Strengthened clinical adoption and product reach in 2025. |

| HUMAN REGENERATION TECHNOLOGIES | US | Challenger | Tissue regeneration and amniotic membrane solutions | North America | Focused on advanced preservation and processing technologies in 2025. |

| TISSUE TECH (BIO-TISSUE) | US | Niche Player | Cryopreserved amniotic membrane for ophthalmology | North America | Expanded ophthalmic product portfolio and clinical applications in 2025. |

| DERMA SCIENCES (INTEGRA LIFESCIENCES) | US | Niche Player | Regenerative wound care and biologic dressings | North America, Europe | Strengthened integration with advanced wound care platforms in 2025. |

Summary Insight:

The market is evolving toward advanced biologics, regenerative therapies, and clinically validated wound care solutions. Companies with strong regulatory capabilities, differentiated preservation technologies, and established clinical adoption are gaining share, while smaller players compete through niche applications and regional distribution. Expansion into new therapeutic areas and emerging markets will define competitive positioning through 2034.

By Type

Cryopreserved and dehydrated amniotic membranes define the core product structure of the global market. Cryopreserved variants continue to generate the majority of revenue, accounting for more than 57% of total market value in 2023. Their dominance extends into 2025 due to preserved cellular integrity, retained biological activity, and consistent clinical outcomes. These membranes are stored at ultra-low temperatures near minus 80 degrees Celsius in glucose-based media, which helps maintain native tissue structure and therapeutic properties. Adoption remains strongest in advanced surgical settings where predictable healing response is critical.

Clinical demand for cryopreserved membranes remains particularly strong in ophthalmic and reconstructive procedures. Surgeons rely on these products to control inflammation, reduce fibrosis, and support faster epithelial recovery. Ongoing investments in tissue processing and cold-chain logistics are expected to sustain above-market growth through 2030, with segment CAGR estimated above 13%.

Dehydrated amniotic membranes serve a complementary role, especially in wound management. These products function as biological dressings in surgical reconstructions, pressure ulcers, and chronic leg wounds. Their room-temperature storage, ease of handling, and lower cost support wider use across outpatient and lower-acuity care settings. Utilization continues to expand in 2025 as providers prioritize operational efficiency and cost control.

By Application

Surgical wound care remains the largest application area, contributing more than 40.2% of global revenue in 2023 and maintaining leadership into 2025. Growth is tied to rising procedure volumes, higher chronic wound incidence, and increased use of biologic coverings in post-operative recovery. Amniotic membranes support faster tissue repair, reduce infection risk, and limit scar formation, which improves clinical outcomes and hospital throughput.

Ophthalmology represents a high-growth application supported by rising cataract, corneal, and ocular surface procedures. Amniotic membranes are widely used to manage inflammation and accelerate healing following ocular surgery. Cosmetic and reconstructive procedures further support demand, particularly in burn treatment where rapid epithelialization is required.

Emerging applications in orthopedics and dermatology continue to broaden the addressable market. Regenerative medicine adoption and improved processing methods support continued penetration, particularly in developing healthcare systems where cost sensitivity remains high.

By End-Use

Hospitals remain the primary end-use segment, accounting for approximately 39.5% of total revenue in 2023. This leadership continues in 2025 as hospitals serve as central hubs for complex surgeries, trauma care, and chronic wound treatment. Integrated procurement systems and reimbursement access further reinforce hospital demand.

Ambulatory Surgical Centers show faster growth as procedures shift toward outpatient settings. These facilities value rapid application, reduced recovery time, and lower complication rates. Specialty clinics and academic institutes also expand usage, particularly for research-driven applications and pilot clinical programs.

By Region

North America continues to lead the global market with more than 35.2% revenue share and an estimated value of USD 1.4 billion in 2023. Growth through 2025 is supported by advanced healthcare infrastructure, strong reimbursement frameworks, and the presence of established tissue processing companies. Technology adoption and alternative biologic therapies further support regional expansion.

Europe ranks second, supported by publicly funded healthcare systems and rising chronic disease prevalence. Increased surgical volumes and standardized care protocols drive steady demand across major economies. Asia Pacific posts the fastest growth rate through 2030 due to expanding healthcare infrastructure, rising disposable income, and unmet clinical demand. India and Japan remain focal points for future capacity expansion and investment activity.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

Product Type

- Cryopreserved

- Dehydrated

Application

- Surgical Wounds

- Ophthalmology

- Other Applications

End-use

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Clinics

- Research And Academic Institutes

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.9 B |

| Forecast Revenue (2034) | USD 14.3 B |

| CAGR (2025-2034) | 12.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Product Type, (Cryopreserved, Dehydrated), Application, (Surgical Wounds, Ophthalmology, Other Applications), End-use, (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Research And Academic Institutes) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Amniox Medical Inc., Katena Products, Inc., Skye Biologics, Inc., Applied Biologics LLC, Organogenesis, Inc., MiMedx Group Inc., Human Regenerative Technologies, LLC, Alliqua BioMedical Inc., DermaSciences, Amnio Technology, LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Surgical Wounds, Ophthalmology, Orthopedics, Other Applications), By End-Use (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Research Institutes), Industry Overview, Market Dynamics, Competitive Landscape, Key Players, Regional Insights, Trends & Forecast 2026–2034")

, By Application (Surgical Wounds, Ophthalmology, Orthopedics, Other Applications), By End-Use (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Research Institutes), Industry Overview, Market Dynamics, Competitive Landscape, Key Players, Regional Insights, Trends & Forecast 2026–2034")

, By Application (Surgical Wounds, Ophthalmology, Orthopedics, Other Applications), By End-Use (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Research Institutes), Industry Overview, Market Dynamics, Competitive Landscape, Key Players, Regional Insights, Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Amniotic Membrane Market?

The Global Amniotic Membrane Market was valued at USD 4.4 Billion in 2024 and is expected to reach USD 4.9 Billion in 2025, projected to hit USD 14.3 Billion by 2034, growing at a CAGR of 12.3% from 2026–2034, driven by regenerative medicine, advanced wound care, and expanding surgical applications.

Who are the major players in the Amniotic Membrane Market?

Amniox Medical Inc., Katena Products, Inc., Skye Biologics, Inc., Applied Biologics LLC, Organogenesis, Inc., MiMedx Group Inc., Human Regenerative Technologies, LLC, Alliqua BioMedical Inc., DermaSciences, Amnio Technology, LLC

Which segments covered the Amniotic Membrane Market?

Product Type, (Cryopreserved, Dehydrated), Application, (Surgical Wounds, Ophthalmology, Other Applications), End-use, (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Research And Academic Institutes)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date