Global Anti-Satellite Weapon Market Size, Share, Analysis By Type (Kinetic Kill, Non-Kinetic Physical, Directed Energy Weapons, Electronic Warfare), By Orbit (LEO, MEO, GEO), By Platform (Air-Launched, Ground-Based, Sea-Based, Space-Based), By End-User (Army, Navy, Air Force, Space Force) Industry Region & Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Geopolitical Drivers, Growth Trends & Forecast 2026-2034

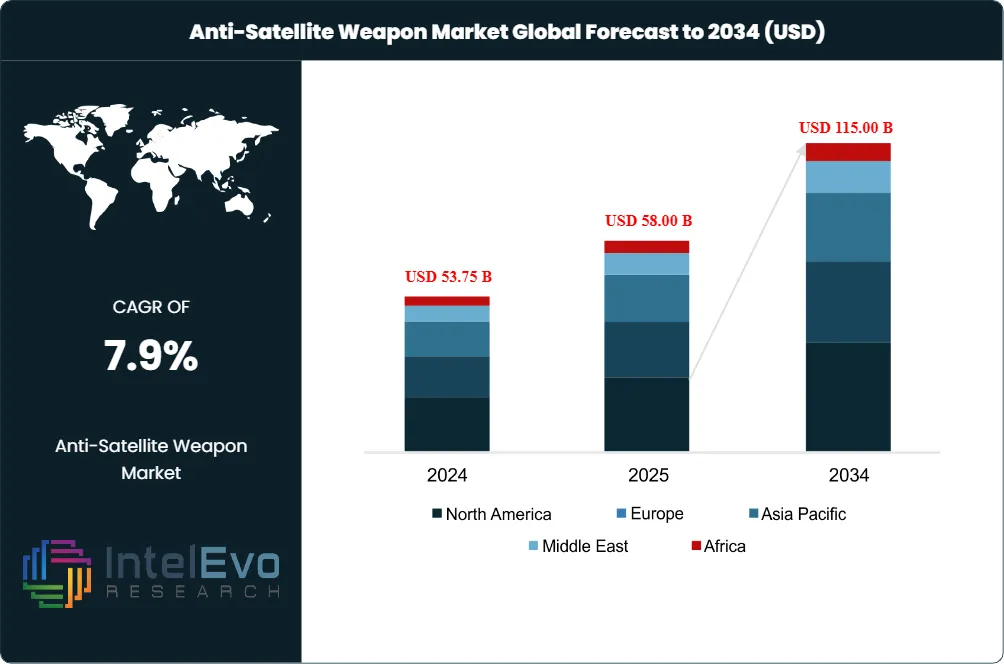

The Anti-Satellite Weapon Market was valued at USD 53.75 Billion in 2024 and USD 58.00 Billion in 2025. The market is projected to reach USD 115.00 Billion by 2034, expanding at a CAGR of 7.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 57.00 Billion over the analysis period. Estimates across published sources diverge meaningfully because category definitions vary; this analysis adopts a mid-range estimate that includes direct-ascent kinetic interceptors, co-orbital systems, ground-based and space-based directed energy weapons, electronic warfare systems against satellites, and counter-space cyber tooling.

The Anti-Satellite Weapon Market is being shaped by three structural forces. First, the Golden Dome layered homeland-defense initiative, valued at USD 185 Billion at announcement, opened a U.S. budget channel for orbital interceptors and reframed counter-space spending from a research line into a procurement category. Second, persistent Russian co-orbital activity through the Cosmos series — including Cosmos 2581, 2582, 2583 launched on February 14, 2025 and Cosmos 2588 launched on May 23, 2025 — has hardened NATO's appetite for dedicated counter-space inventory. Third, China's modernization, including roughly 1,007 satellites on orbit by May 2025 and a portfolio of Shijian and TJS experimental platforms, has anchored Asia Pacific as the principal pacing region for capability development.

Regulatory gravity sits on the 1967 Outer Space Treaty Article IV, the Partial Test Ban Treaty, the Comprehensive Nuclear Test Ban Treaty, the U.S. Space Force's April 2025 Space Warfighting framework document, and the December 2024 UN General Assembly resolution on weapons of mass destruction in outer space, which passed 167-4 with 6 abstentions. Trade-body anchors include the Secure World Foundation's annual Global Counterspace Capabilities reporting and U.S. Space Command public attribution statements. Industry compliance is governed under MIL-STD-1553 data bus, MIL-STD-461 EMC, and ITAR/EAR export control schedules USML Categories IV and XV.

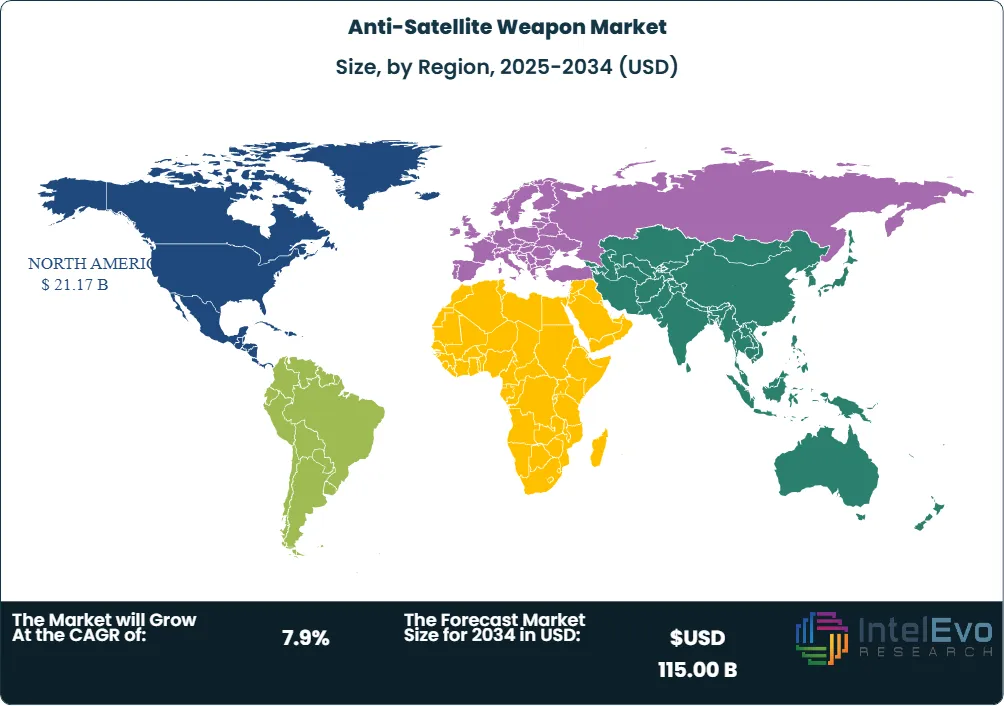

North America held approximately 36.5% of 2025 revenue, anchored by U.S. Space Force, Missile Defense Agency, and Space Systems Command procurement. Asia Pacific is forecast to expand at roughly 9.8% CAGR through 2034, the steepest of any region, on the back of People's Liberation Army and DRDO programs. Forward through 2034, the strongest growth pockets are non-kinetic systems — directed energy, reversible jamming, and cyber-ASAT — because kinetic debris liability under Outer Space Treaty Article IX continues to constrain test cadence for high-altitude kinetic weapons.

Market Definition & Scope

The Anti-Satellite Weapon Market is defined as the global commercial activity around weapon systems and integrated subsystems specifically engineered to destroy, disable, deny, degrade, or disrupt satellites and their associated ground or link-segment infrastructure. The market encompasses kinetic kill vehicles (direct-ascent and co-orbital), high-energy lasers and high-power microwave systems aimed at satellite sensors or structures, electronic warfare jammers and spoofers targeting satellite communication and navigation links, and offensive cyber tooling designed to compromise on-board flight software or ground command networks.

This analysis includes military procurement of dedicated counter-space platforms, dual-use missile-defense interceptors with credible orbital reach (such as those derived from PAC-3, THAAD, SM-3, and the Indian PDV Mk-II), and the Space-Based Interceptor (SBI) prototype pipeline funded under the Golden Dome architecture. Excluded from scope are passive space situational awareness sensors, satellite-protection systems, generic missile defense applications without an orbital engagement use case, and broader space militarization spending on intelligence, surveillance, and reconnaissance satellites that are not weapon platforms. The Anti-Satellite Weapon Market sits inside the broader Space Militarization Market, which industry analysis indicates was approximately USD 65 Billion in 2025.

Key Takeaways

Market Growth: the global Anti-Satellite Weapon Market expanded from USD 58.00 Billion in 2025 toward a projected USD 115.00 Billion by 2034 at a 7.9% CAGR.

Segment Dominance (Type): Kinetic Kill Vehicles (direct-ascent and co-orbital combined) accounted for roughly 41.0% of 2025 revenue, the largest share by weapon type.

Segment Dominance (End User): Government Defense Agencies absorbed approximately 78.5% of 2025 demand by buyer channel, reflecting state-only procurement of strategic counter-space assets.

Driver: U.S. Department of War FY2025 space-defense allocation exceeded USD 33 Billion, with the Golden Dome layered homeland-defense plan announced at USD 185 Billion through completion.

Restraint: Outer Space Treaty Article IV constraints and the November 2021 Russian Nudol kinetic test (which generated more than 1,500 trackable debris pieces) cap the political space for kinetic ASAT testing in low Earth orbit.

Opportunity: Non-kinetic systems (directed energy weapons, reversible jamming, cyber-ASAT) carry the steepest growth profile, with industry analysis indicating a 9.5% CAGR through 2034 on the back of orbital debris avoidance.

Trend: Space-Based Interceptor (SBI) prototyping under Golden Dome moved from research to procurement contracting between November 2025 and May 2026, with USD 3.2 Billion in OTA awards across 20 contracts to 12 firms.

Regional: North America retained leadership at 36.5% share (USD 21.17 Billion) in 2025, with the United States contributing approximately 91% of regional revenue.

Key Insights Summary

The Anti-Satellite Weapon Market rests on a small set of verifiable technical statistics that frame strategic posture and industrial allocation through 2034.

U.S. Space Systems Command booked 20 prototype Other Transaction Authority contracts worth up to USD 3.2 Billion across 12 companies between late 2025 and May 1, 2026, with prototypes required to be ready for testing by 2028 under the Space-Based Interceptor program.

The Russian A-235 Nudol direct-ascent system destroyed Cosmos 1408 on November 15, 2021 at an altitude of approximately 480 kilometers, generating roughly 1,500 trackable debris fragments that compelled International Space Station crew to take shelter in escape capsules during early debris-cloud passes.

Russia placed three military satellites — Cosmos 2581, 2582, and 2583 — into low Earth orbit aboard a Soyuz-2.1v on February 14, 2025, and U.S. Space Command observers tracked coordinated formation behavior consistent with rendezvous and proximity operations training.

India's DRDO completed the Mk-IIA Sahastra Shakti high-energy laser directed-energy weapon test on April 13, 2025, demonstrating a 30 kilowatt vehicle-mounted system at a 5 kilometer engagement range; the agency is concurrently funding the DURGA II 100 kilowatt program for higher-power applications.

The 2007 Chinese SC-19 direct-ascent kinetic test against the Fengyun-1C satellite generated more than 3,000 trackable fragments and an estimated 150,000 sub-catalog particles, which remain a structural reference point for orbital debris liability conversations through 2026.

The Space Development Agency awarded a USD 3.5 Billion Tranche 3 tracking-layer contract in late 2025 for 72 new satellites scheduled for launch from 2029, anchoring the sensor side of the kill chain that ASAT weapons depend on.

Competitive Landscape Overview

The Anti-Satellite Weapon Market is highly consolidated. Industry analysis indicates that the top four prime contractors — Lockheed Martin Corporation, Northrop Grumman Corporation, RTX Corporation, and BAE Systems plc — together captured an estimated 48% of 2025 revenue, with state research organizations (DRDO, China Academy of Launch Vehicle Technology, Russian Almaz-Antey) anchoring an additional 22% of global activity. Competition is technology-led and program-of-record-led, not price-led, because counter-space contracts are awarded on system maturity, intercept geometry, and policy fit rather than unit economics.

Competitive evolution accelerated through Q4 2025 and Q1 2026 as the Golden Dome SBI awards drew defense-tech-native challengers into a category that previously skewed toward incumbent missile primes. SpaceX, Anduril Industries, and GITAI received Other Transaction Authority awards alongside Lockheed Martin, Northrop Grumman, RTX, and General Dynamics, breaking the traditional five-prime cartel structure. M&A activity in the trailing 12 months centered on subsystem consolidation rather than top-line ASAT primes; the largest disclosed adjacency move was Lockheed Martin's USD 233 Million Full-Rate Production Block II IRST award in October 2025.

Competitive Landscape Matrix

Company

HQ

Position

Key Product / Solution

Geographic Strength

Recent Strategic Move (Trailing 18 Months)

Lockheed Martin Corporation

United States

Leader

Space-Based Interceptor, THAAD, NGI

North America, NATO

On May 1, 2026 the company picked up SBI prototype contracts under Golden Dome through Space Systems Command.

Northrop Grumman Corporation

United States

Leader

Ground-based midcourse defense, NGI

North America, Five Eyes

Through late 2025 the firm took multiple SBI Other Transaction Authority awards inside the USD 3.2 Billion Golden Dome envelope.

RTX Corporation

United States

Leader

SM-3, Cosmic-class kill vehicles

North America, Japan

During 2025 the company widened its missile-tracking constellation footprint under Space Development Agency programs and entered SBI prototyping.

BAE Systems plc

United Kingdom

Leader

Counter-space EW, DEW R&D

UK, Australia, NATO

Through 2025 the group continued investment in directed-energy and counter-space electronic warfare research aligned to UK Space Command requirements.

Anduril Industries

United States

Challenger

Lattice space-domain awareness

North America

In late 2025 the firm joined the Golden Dome SBI prototyping pool alongside SpaceX and traditional primes.

L3Harris Technologies, Inc.

United States

Challenger

Counter Communications System (CCS)

North America

During 2025 the company continued CCS sustainment and training cycles at Peterson Space Force Base.

Defence Research & Development Organisation

India

Challenger

PDV Mk-II, Sahastra Shakti laser

India

On April 13, 2025 DRDO concluded the Mk-IIA Sahastra Shakti 30 kilowatt laser DEW field test.

Rafael Advanced Defense Systems

Israel

Niche Player

Iron Beam directed energy weapons

Israel, Europe

Through 2025 the company progressed the Iron Beam high-energy laser toward operational deployment with the Israel Defense Forces.

Segmentation Analysis

The global Anti-Satellite Weapon Market segments most usefully along four axes: by weapon type, by orbit engaged, by buyer channel, and by deployment platform. Each axis surfaces different procurement, policy, and industrial signals.

By Weapon Type

The Anti-Satellite Weapon Market is led by Kinetic Kill Vehicles, which industry analysis indicates held approximately 41.0% revenue share (USD 23.78 Billion) in 2025 because direct-ascent interceptors derived from missile-defense lineages (PAC-3, THAAD, SM-3, PDV Mk-II, A-235 Nudol) carry the largest existing program backlogs. Co-orbital subsystems, including Russian Cosmos-series payloads and Chinese SJ-series experimental satellites, contribute the smaller co-orbital share. Directed Energy Weapons (high-energy lasers and high-power microwave systems) accounted for around 22.5% (USD 13.05 Billion) and are forecast to expand at 9.8% CAGR through 2034, the steepest of any weapon type, reflecting Indian DURGA II, Israeli Iron Beam, U.S. HELIOS, and Russian Peresvet program activity.

Electronic Warfare Systems against satellites — including the U.S. Counter Communications System (CCS) operated at Peterson Space Force Base, Russian Tirada-2 and Bylina jammers, and Chinese GNSS jamming inventories — captured approximately 23.0% (USD 13.34 Billion) in 2025 and are the principal beneficiary of low political cost (no debris) and reversibility, which makes them deployable in active conflict zones such as Ukraine. Cyber-ASAT tooling, the smallest reported category at roughly 13.5% (USD 7.83 Billion), nonetheless attracts disproportionate research dollars because it offers asymmetric leverage at low industrial-base cost. Compared to the 41.0% kinetic share, the combined non-kinetic share of 59.0% represents an 18.0 percentage point lead and is widening through 2034.

By Orbit Engaged

Low Earth Orbit dominated the Anti-Satellite Weapon Market at approximately 64.0% revenue share (USD 37.12 Billion) in 2025 because all four publicly tested direct-ascent kinetic systems — U.S. SM-3 (2008), Chinese SC-19 (2007), Indian PDV Mk-II (2019), and Russian A-235 Nudol (2021) — engaged LEO targets. Geosynchronous Earth Orbit engagement capability captured roughly 21.5% (USD 12.47 Billion) and is the focus of co-orbital RPO platforms; multiple Chinese SJ-series and TJS-series satellites have been observed conducting unusual GEO maneuvers per U.S. Space Threat Fact Sheet reporting. Medium Earth Orbit engagement, primarily relevant for navigation-satellite denial against GPS, BeiDou, GLONASS, and Galileo, accounted for the remaining 14.5% (USD 8.41 Billion) and is the most under-weighted segment relative to operational importance.

By Buyer Channel

Government Defense Agencies dominated the Anti-Satellite Weapon Market at approximately 78.5% revenue share (USD 45.53 Billion) in 2025, reflecting that ASAT weapons are state-only inventory subject to ITAR/EAR export controls and the 1967 Outer Space Treaty. The U.S. Space Force, Missile Defense Agency, and Space Systems Command together constituted the single largest buying centre at an estimated USD 19 Billion in 2025. Defense Prime Contractors, who buy subsystems for integration into government deliverables, captured roughly 16.0% (USD 9.28 Billion). The remaining 5.5% (USD 3.19 Billion) sits in research consortia, defense-tech VCs (which posted USD 49.1 Billion in calendar 2025 across all categories), and dual-use commercial platforms such as the Space Development Agency Tranche 3 tracking layer.

By Deployment Platform

Ground-Launched systems led the Anti-Satellite Weapon Market at approximately 38.5% revenue share (USD 22.33 Billion) in 2025 because direct-ascent kinetic interceptors and ground-based laser dazzlers (such as the Russian Peresvet system fielded to five strategic missile divisions starting in 2018) make up the largest installed base. Space-Based platforms held around 32.0% (USD 18.56 Billion) and are forecast to expand at roughly 11.0% CAGR through 2034, anchored by the Golden Dome Space-Based Interceptor program. Sea-Launched and Air-Launched platforms — the latter including derivative-of-fighter-launched concepts under exploration in the U.S. and India — together contributed the remainder. Compared to the 38.5% ground share against the 32.0% space share, the 6.5 percentage point delta is forecast to invert by 2030 if Golden Dome SBI prototypes complete their 2028 testing milestone.

Regional Analysis

The Anti-Satellite Weapon Market exhibits sharply concentrated regional shares because only four nations have publicly tested direct-ascent kinetic ASATs — the United States, Russia, China, and India — and a handful of others operate non-kinetic counter-space inventory.

North America held approximately 36.5% revenue share (USD 21.17 Billion) of the Anti-Satellite Weapon Market in 2025. The United States contributed an estimated 91% of regional revenue (USD 19.27 Billion). The U.S. Department of War's FY2025 space-defense allocation exceeded USD 33 Billion, the U.S. Space Force's April 2025 Space Warfighting framework codified counter-space as a doctrinal priority, and Space Systems Command's USD 3.2 Billion SBI Other Transaction Authority awards across 20 contracts cemented the regional pipeline through 2028. Canada contributed the balance through NORAD-aligned space domain awareness and ground-based optical sensor integration.

Asia Pacific captured approximately 31.5% (USD 18.27 Billion) of the Anti-Satellite Weapon Market in 2025 and is forecast at 9.8% CAGR through 2034, the steepest of any region. China's PLA fielded direct-ascent ASAT systems are believed mature for LEO targets and developmental for MEO/GEO, with at least one and possibly three programs running per Secure World Foundation reporting. China launched Shijian-29A and 29B from Wenchang on December 31, 2025 for what was described as space target detection technology verification. India's DRDO progressed Mk-IIA Sahastra Shakti laser DEW testing on April 13, 2025 and continued to advance the DURGA II 100 kilowatt program, with infrared-seeker work at Bharat Dynamics, Electronic Corporation of India, and Alpha Design Technologies.

Europe represented approximately 18.0% (USD 10.44 Billion) of the Anti-Satellite Weapon Market in 2025, anchored by the United Kingdom, France, Germany, and Italy. The UK Space Command's continued partnership with BAE Systems on directed-energy and counter-space electronic warfare research is the principal European production driver. The EU Space Defense Strategy enhances collective situational awareness and resilience against hostile space activities, and France retains an Olymp-K-incident-driven appetite for indigenous counter-space capability. Eastern European spending stepped up through 2025 in response to Russian co-orbital activity.

Middle East and Africa held the remaining roughly 9.5% (USD 5.51 Billion) of the Anti-Satellite Weapon Market in 2025, anchored by Israel and Saudi Arabia. Israeli demand sources from indigenous suppliers Rafael Advanced Defense Systems (Iron Beam) and Elbit Systems, with Iron Beam progressing toward operational deployment with the Israel Defense Forces through 2025. Gulf Cooperation Council buyers source via Foreign Military Sales pathways from U.S. and Israeli primes.

Latin America accounted for the smallest share at approximately 4.5% (USD 2.61 Billion) of the Anti-Satellite Weapon Market in 2025, with Brazil leading regional procurement through Programa Estratégico de Sistemas Espaciais and Embraer Defense partnerships. Regional CAGR through 2034 is forecast at approximately 5.5%, slower than Asia Pacific but the relevant base is small.

Country Analysis

Country-level analysis of the Anti-Satellite Weapon Market sharpens four national pictures that regional aggregates obscure.

The United States Anti-Satellite Weapon Market reached approximately USD 19.27 Billion in 2025 and is forecast at 8.4% CAGR through 2034, the largest and most program-mature national market. The Golden Dome Space-Based Interceptor program — announced at USD 185 Billion through completion — channels procurement through Space Systems Command, with USD 3.2 Billion in OTA prototype awards across 20 contracts to 12 firms booked between November 2025 and May 1, 2026. The L3Harris-built Counter Communications System remains the principal deployed offensive jamming inventory, exercised at Peterson Space Force Base under the U.S. Space Force. The April 2025 Space Warfighting framework formally moved counter-space from supportive to offensive doctrine.

China's Anti-Satellite Weapon Market is estimated at approximately USD 9.50 Billion in 2025 with a forecast 11.0% CAGR through 2034. PLA programs include at least one mature LEO direct-ascent system descended from the SC-19, plus developmental MEO/GEO interceptors, plus the Shijian and TJS experimental satellite series performing GEO RPO maneuvers. By May 2025 China's on-orbit fleet exceeded 1,007 satellites, including more than 510 ISR-capable platforms that anchor the targeting kill chain. The December 31, 2025 launch of Shijian-29A and 29B from Wenchang supports space target detection technology validation, a dual-use signature that crosses into co-orbital ASAT capability.

Russia's Anti-Satellite Weapon Market is estimated at approximately USD 7.20 Billion in 2025 with a forecast 5.5% CAGR through 2034 (export-controlled and sanctions-constrained). The A-235 Nudol direct-ascent system completed its first satellite kill against Cosmos 1408 on November 15, 2021. Co-orbital activity continued through 2025 with Cosmos 2581-2583 launched on February 14, 2025 from Plesetsk Cosmodrome and Cosmos 2588 launched on May 23, 2025, both observed in close proximity to U.S. reconnaissance satellites. Peresvet ground-based laser systems were fielded to five strategic missile divisions starting in 2018, and the alleged nuclear-EMP ASAT capability remains undeployed and untested per State Department reporting.

India's Anti-Satellite Weapon Market reached approximately USD 4.20 Billion in 2025 with a forecast 10.5% CAGR through 2034. DRDO operates the PDV Mk-II direct-ascent system that completed Mission Shakti on March 27, 2019, the Mk-IIA Sahastra Shakti 30 kilowatt vehicle-mounted laser tested on April 13, 2025 with a 5 kilometer engagement range, and the DURGA II 100 kilowatt program. Production partners include Bharat Electronics Limited, Bharat Dynamics, Adani Defence & Aerospace (which launched a vehicle-mounted counter-drone laser at Aero India 2025), and Larsen & Toubro. The Defence Space Agency and Defence Space Research Organisation institutionalize the operational and research split, with Space Command anchoring doctrine.

By Weapon Type, (Kinetic Kill Vehicles (KKVs), Directed Energy Weapons (Laser Systems), Electronic Warfare Systems, Cyber Anti-Satellite Weapons, Co-Orbital Anti-Satellite Weapons, (Missile-Based Anti-Satellite Systems, High-Power Microwave (HPM) Weapons, Radio Frequency (RF) Jamming Systems, Others), By Orbit Engaged, (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Earth Orbit (GEO), Highly Elliptical Orbit (HEO), Polar Orbit, Sun-Synchronous Orbit (SSO), Others), By Buyer Channel, (Defense Ministries, Space Defense Commands, Military Space Forces, National Intelligence Agencies, Government Space Agencies, Defense Research Organizations, Others), By Deployment Platform, (Ground-Based Systems, Air-Launched Systems, Sea-Based Systems, Space-Based Systems, Mobile Launcher Platforms, Fixed Launch Installations, Others)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

LOCKHEED MARTIN CORPORATION, NORTHROP GRUMMAN CORPORATION, RTX CORPORATION, BAE SYSTEMS PLC, ANDURIL INDUSTRIES, INC., L3HARRIS TECHNOLOGIES, INC., DEFENCE RESEARCH & DEVELOPMENT ORGANISATION (DRDO), RAFAEL ADVANCED DEFENSE SYSTEMS LTD., BLUEHALO LLC, BOEING COMPANY, GENERAL DYNAMICS CORPORATION, SPACEX, AEROJET ROCKETDYNE (NOW L3HARRIS), THALES GROUP, AIRBUS DEFENCE AND SPACE, ASELSAN A.S., ALMAZ-ANTEY, CHINA AEROSPACE SCIENCE AND TECHNOLOGY CORPORATION, BHARAT DYNAMICS LIMITED, OTHERS

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 176 ANTI-SATELLITE WEAPON MARKET CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Player Analysis

The top four prime contractors in the Anti-Satellite Weapon Market are Lockheed Martin Corporation, Northrop Grumman Corporation, RTX Corporation, and BAE Systems plc, profiled below from publicly disclosed positioning and verified contract awards.

Lockheed Martin Corporation occupies a leading position in the Anti-Satellite Weapon Market through its Space-Based Interceptor portfolio and the underlying THAAD, PAC-3, and Next Generation Interceptor lineages. On May 1, 2026 the company picked up Space-Based Interceptor prototype contracts under U.S. Space Force Space Systems Command, work that builds on its hypersonic strike systems and missile warning and tracking heritage. The October 2025 USD 233 Million Block II IRST Full-Rate Production award rounds out the company's targeting-sensor adjacency. Strategic differentiators include vertical integration of kinetic kill vehicles, deep next-generation overhead persistent infrared satellite production at the company's California and Colorado sites, and the only existing combat-proven exo-atmospheric kill vehicle qualification base in the Western Hemisphere. The company's competitive moat is the institutional intercept-physics knowledge accrued across decades of Aegis BMD and ground-based midcourse defense work.

Northrop Grumman Corporation holds a leading position in the Anti-Satellite Weapon Market through Ground-Based Midcourse Defense, Next Generation Interceptor, and Space-Based Interceptor prototyping under Golden Dome. The company secured multiple SBI Other Transaction Authority awards inside the Space Systems Command USD 3.2 Billion envelope in late 2025 and early 2026. Northrop Grumman is also a principal supplier to the Space Development Agency's tracking layer, with Tranche 3 work covering 72 satellites scheduled for launch beginning 2029. Strategic positioning rests on solid rocket motor manufacturing scale, an integrated systems engineering capability for layered missile defense, and the company's deep relationship with Missile Defense Agency. Differentiators include Northrop Grumman's expertise in kill-vehicle guidance, navigation, and control software, plus its recent recapitalization of the Promontory solid rocket motor facility in Utah to support volume.

RTX Corporation is a leading Anti-Satellite Weapon Market participant through SM-3 cooperative development with Mitsubishi Heavy Industries, Cosmic-class kinetic kill vehicle work, and Space-Based Interceptor prototyping. During 2025 the company widened its missile-tracking constellation footprint inside Space Development Agency programs and entered the SBI competition. Collins Aerospace, the RTX subsidiary, anchors the company's wearable and pilot-system positioning in adjacent defense markets. Strategic positioning rests on Raytheon Missiles & Defense's intercept-engagement heritage from SM-3 Block IIA through to Standard Missile-6, plus the company's exclusive U.S.-Japan SM-3 Block IIA cooperative production framework. The company differentiates on multi-mission interceptor design that crosses ballistic, hypersonic, and orbital engagement use cases without requiring separate inventory.

BAE Systems plc holds a leading position in the Anti-Satellite Weapon Market through directed-energy weapons research, counter-space electronic warfare systems, and integration work for U.K. Space Command. The company runs sustained R&D on high-power microwave systems and free-electron lasers under Five Eyes cooperation frameworks, complementing its broader sensor and signal-intelligence portfolio. Strategic positioning rests on a deep portfolio of qualified U.K. Ministry of Defence components combined with Australian and U.S. cleared-defense subsidiaries that allow trilateral AUKUS technology flows. Differentiators include vertically integrated optics, RF, and EW manufacturing in the United Kingdom and the United States, plus the company's role as a principal supplier to the U.K. Space Operations Centre at RAF High Wycombe.

Market Key Players

LOCKHEED MARTIN CORPORATION

NORTHROP GRUMMAN CORPORATION

RTX CORPORATION

BAE SYSTEMS PLC

ANDURIL INDUSTRIES, INC.

L3HARRIS TECHNOLOGIES, INC.

DEFENCE RESEARCH & DEVELOPMENT ORGANISATION (DRDO)

RAFAEL ADVANCED DEFENSE SYSTEMS LTD.

BLUEHALO LLC

BOEING COMPANY

GENERAL DYNAMICS CORPORATION

SPACEX

AEROJET ROCKETDYNE (NOW L3HARRIS)

THALES GROUP

AIRBUS DEFENCE AND SPACE

ASELSAN A.S.

ALMAZ-ANTEY

CHINA AEROSPACE SCIENCE AND TECHNOLOGY CORPORATION

BHARAT DYNAMICS LIMITED

OTHERS

Drivers

Growing Militarization of Space and Strategic Defense Investments

The increasing dependence on satellites for military communications, navigation, intelligence, surveillance, reconnaissance (ISR), and missile warning systems is driving governments to strengthen their counter-space capabilities. As geopolitical competition intensifies, nations are investing heavily in anti-satellite (ASAT) technologies to protect critical space assets and maintain strategic deterrence.

Defense modernization programs across major military powers are accelerating the development of advanced anti-satellite systems, including kinetic interceptors, electronic warfare platforms, cyber capabilities, and directed energy weapons. These investments are significantly contributing to market expansion.

Rising Importance of Space Asset Protection

Modern military operations rely heavily on satellite infrastructure for command and control, precision-guided weapons, and real-time battlefield intelligence. The growing strategic value of space-based assets is encouraging governments to develop offensive and defensive counter-space capabilities that can neutralize potential threats during conflict scenarios.

Increasing deployment of military satellites, expanding space surveillance networks, and rising investments in space domain awareness technologies are creating sustained demand for advanced anti-satellite weapon systems.

Restraints

International Regulations and Arms Control Concerns

The development and testing of anti-satellite weapons are subject to increasing international scrutiny due to concerns regarding space security, orbital debris, and long-term sustainability of the space environment. Governments must balance national security priorities with international treaties and diplomatic commitments.

Growing discussions surrounding global arms control agreements, responsible behavior in space, and restrictions on destructive ASAT testing may limit the pace of market expansion and influence procurement strategies.

High Development Costs and Technical Complexity

Anti-satellite weapon systems require sophisticated missile guidance technologies, advanced sensors, precision tracking systems, electronic warfare capabilities, and space surveillance infrastructure. Developing and maintaining these highly specialized systems involves substantial financial investment and long development cycles.

In addition, integrating anti-satellite capabilities with existing defense architectures while ensuring operational reliability under complex space conditions presents significant technical challenges for defense organizations.

Trends

Expansion of Non-Kinetic Counter-Space Technologies

Defense organizations are increasingly prioritizing non-destructive counter-space capabilities such as cyber warfare, electronic jamming, spoofing systems, high-power microwave weapons, and directed energy technologies. These systems can temporarily disrupt satellite operations without generating hazardous orbital debris.

The growing emphasis on reversible and scalable counter-space effects is reshaping military procurement strategies while supporting responsible space security initiatives.

Integration of Artificial Intelligence and Space Domain Awareness

Artificial intelligence, machine learning, and advanced data analytics are being integrated into space surveillance and tracking systems to improve threat detection, orbital object identification, and decision-making capabilities. AI-enabled platforms enhance the ability to monitor satellite movements and identify potential hostile activities in real time.

Advancements in autonomous tracking, predictive analytics, and integrated command-and-control systems are strengthening the effectiveness of next-generation anti-satellite defense operations.

Opportunities

Rising Defense Spending on Space Security Programs

Governments worldwide are significantly increasing investments in military space programs to strengthen national security and protect critical satellite infrastructure. Growing budgets for space defense, missile defense, and strategic deterrence programs are creating substantial opportunities for manufacturers of anti-satellite technologies.

The establishment of dedicated military space commands and expanded defense procurement initiatives is expected to accelerate the adoption of advanced counter-space systems across both developed and emerging defense markets.

Innovation in Multi-Domain Defense and Counter-Space Solutions

The convergence of satellite surveillance, missile defense, electronic warfare, cyber operations, and artificial intelligence is creating opportunities for integrated counter-space solutions capable of addressing increasingly complex security challenges. Multi-domain defense strategies are encouraging the development of highly interoperable anti-satellite systems.

Continued advancements in directed energy weapons, high-power microwave technologies, autonomous interception systems, space situational awareness, quantum sensing, AI-enabled command platforms, and resilient space defense architectures are expected to create significant long-term growth opportunities, positioning anti-satellite weapon systems as a strategic component of future military space operations and national defense capabilities.

Investment & M&A Activity

The Anti-Satellite Weapon Market recorded approximately USD 7.2 Billion in disclosed contracting and adjacency-deal activity over the trailing 12 months, reflecting a procurement-led rather than M&A-led capital cycle in this state-restricted category.

The single largest disclosed counter-space contracting event in the trailing 12 months was the Space Systems Command Space-Based Interceptor prototyping competition, which booked USD 3.2 Billion across 20 Other Transaction Authority awards to 12 firms between November 2025 and May 1, 2026. Awardees include Lockheed Martin Corporation, Northrop Grumman Corporation, RTX Corporation, General Dynamics Corporation, SpaceX, Anduril Industries, and GITAI, with prototypes required ready for testing by 2028 ahead of the Golden Dome layered defense initial operating capability. On May 1, 2026 Lockheed Martin specifically disclosed its SBI selection, building on the company's THAAD, PAC-3, Next Generation Interceptor, hypersonic strike, and missile warning and tracking heritage. The Space Development Agency Tranche 3 tracking layer award totalling USD 3.5 Billion in late 2025 anchors the sensor side of the kill chain that ASAT weapons depend on.

Adjacent funding patterns through the trailing 12 months tracked the broader defense venture capital surge, which posted a record USD 49.1 Billion in calendar 2025 across all categories per industry analysis, roughly twice the prior-year figure. Counter-space-relevant rounds include autonomy and AI-software platforms positioning for Golden Dome integration. Lockheed Martin Corporation's October 20, 2025 USD 233 Million Block II IRST Full-Rate Production award, while a sensor program rather than a weapon, underwrites the targeting chain that direct-ascent kinetic ASAT systems require for engagement. India's DRDO continued its USD 100 million-class outlay request for DURGA II directed-energy weapons through 2025, consistent with the Aero India 2025 unveiling of the Adani Defence & Aerospace co-developed counter-drone laser platform. M&A among publicly traded ASAT primes remained limited because the buyer base is government-only and acquisitions are gated by Committee on Foreign Investment in the United States review.

Recent Developments

The Anti-Satellite Weapon Market posted six verified non-deal developments across the trailing 18 months, four of which fell inside the trailing six-month window.

May 2026 — Lockheed Martin Corporation and U.S. Space Force Space Systems Command

On the first day of May 2026, the U.S. Space Force selected Lockheed Martin to develop capabilities supporting the Space-Based Interceptor program, work that draws on the company's THAAD, PAC-3, Next Generation Interceptor, hypersonic strike, and missile warning and tracking lineages to deliver an early-engagement orbital layer inside the Golden Dome layered homeland defense architecture.

Strategic Impact: The award formalizes orbital kinetic interception as a U.S. procurement category rather than a research curiosity and creates a live production pull on solid rocket motor, kill vehicle, and infrared seeker capacity through 2028 testing milestones.

April-May 2026 — U.S. Space Force Space Systems Command (Multi-Vendor)

Across late 2025 and into May 2026, Space Systems Command issued 20 Other Transaction Authority prototype contracts worth up to USD 3.2 Billion to 12 firms — including Lockheed Martin, Northrop Grumman, RTX, General Dynamics, SpaceX, Anduril Industries, and GITAI — for Space-Based Interceptor concepts, with all awardees required to have prototypes ready for testing by 2028.

Strategic Impact: The 20-award structure breaks the traditional five-prime cartel pattern in U.S. missile defense and explicitly invites defense-tech-native challengers into orbital kinetic engagement, reshaping competitive dynamics through the early years of the forecast period.

April 2025 — U.S. Space Force

Through the April 2025 publication of Space Warfighting: A Framework for Planners under General Saltzman, the U.S. Space Force codified the service's transition from primarily supportive functions to offensive and defensive counter-space operations, framing space superiority as the basis from which the Joint Force projects power, deters aggression, and secures the homeland.

Strategic Impact: The framework document is a doctrinal anchor that aligns Space Force programs of record around offensive counter-space capability and provides Congressional and allied buyers with a public reference point for ASAT-relevant procurement justification.

April 2025 — Defence Research & Development Organisation (DRDO), India

On April 13, 2025, DRDO's Centre for High Energy Systems and Sciences concluded a successful field test of the Mk-IIA Sahastra Shakti vehicle-mounted laser directed-energy weapon at 30 kilowatts of output power and a 5 kilometer engagement range, with the agency concurrently funding the DURGA II 100 kilowatt program for higher-power follow-on applications.

Strategic Impact: The Sahastra Shakti milestone moves India into the second tier of nations with fielded directed-energy weapons capable of contributing to a counter-space kill chain, reducing reliance on imported kinetic interceptors for low-altitude target sets.

May 2025 — Russian Space Forces (Cosmos 2588 Launch)

On May 23, 2025, Russia placed the Cosmos 2588 satellite into low Earth orbit on an orbital plane very close to that of U.S. reconnaissance satellite USA 338, which independent observers including Marco Langbroek and Bart Hendrickx assessed as the fourth instance in five years of a Russian military satellite shadowing a U.S. optical reconnaissance asset.

Strategic Impact: The Cosmos 2588 deployment reinforces the assessment that Russia maintains a dormant co-orbital ASAT capability and continues to drive U.S. and allied investment in space domain awareness, satellite hardening, and responsive launch.

February 2025 — Russian Space Forces (Plesetsk Cosmodrome Launch)

On February 14, 2025, a Soyuz-2.1v rocket from Plesetsk Cosmodrome placed three Russian military satellites — Cosmos 2581, 2582, and 2583 — into low Earth orbit at approximately 500 miles altitude, where U.S. Space Command observers documented coordinated formation behavior consistent with rendezvous-and-proximity-operations training, including patterns that simulated isolating a target spacecraft.

Strategic Impact: The triple-launch episode validates Russian RPO maturity at small-satellite scale and intensifies pressure on NATO buyers to accelerate satellite hardening, on-orbit servicing, and dedicated counter-space inventory.

Frequently Asked Questions

How big is the Anti-Satellite Weapon Market?

The Global Anti-Satellite Weapon Market was valued at USD 53.75 Billion in 2024 and USD 58.00 Billion in 2025, and is projected to reach USD 115.00 Billion by 2034, growing at a CAGR of 7.9% from 2026 to 2034. Market growth is driven by military space modernization, counter-space technologies, and rising defense investments.

Who are the major players in the Anti-Satellite Weapon Market?

LOCKHEED MARTIN CORPORATION, NORTHROP GRUMMAN CORPORATION, RTX CORPORATION, BAE SYSTEMS PLC, ANDURIL INDUSTRIES, INC., L3HARRIS TECHNOLOGIES, INC., DEFENCE RESEARCH & DEVELOPMENT ORGANISATION (DRDO), RAFAEL ADVANCED DEFENSE SYSTEMS LTD., BLUEHALO LLC, BOEING COMPANY, GENERAL DYNAMICS CORPORATION, SPACEX, AEROJET ROCKETDYNE (NOW L3HARRIS), THALES GROUP, AIRBUS DEFENCE AND SPACE, ASELSAN A.S., ALMAZ-ANTEY, CHINA AEROSPACE SCIENCE AND TECHNOLOGY CORPORATION, BHARAT DYNAMICS LIMITED, OTHERS

Which segments covered the Anti-Satellite Weapon Market?

By Weapon Type, (Kinetic Kill Vehicles (KKVs), Directed Energy Weapons (Laser Systems), Electronic Warfare Systems, Cyber Anti-Satellite Weapons, Co-Orbital Anti-Satellite Weapons, (Missile-Based Anti-Satellite Systems, High-Power Microwave (HPM) Weapons, Radio Frequency (RF) Jamming Systems, Others), By Orbit Engaged, (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Earth Orbit (GEO), Highly Elliptical Orbit (HEO), Polar Orbit, Sun-Synchronous Orbit (SSO), Others), By Buyer Channel, (Defense Ministries, Space Defense Commands, Military Space Forces, National Intelligence Agencies, Government Space Agencies, Defense Research Organizations, Others), By Deployment Platform, (Ground-Based Systems, Air-Launched Systems, Sea-Based Systems, Space-Based Systems, Mobile Launcher Platforms, Fixed Launch Installations, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, By Orbit (LEO, MEO, GEO), By Platform (Air-Launched, Ground-Based, Sea-Based, Space-Based), By End-User (Army, Navy, Air Force, Space Force) Industry Region & Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Geopolitical Drivers, Growth Trends & Forecast 2026-2034")

, By Orbit (LEO, MEO, GEO), By Platform (Air-Launched, Ground-Based, Sea-Based, Space-Based), By End-User (Army, Navy, Air Force, Space Force) Industry Region & Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Geopolitical Drivers, Growth Trends & Forecast 2026-2034")

, By Orbit (LEO, MEO, GEO), By Platform (Air-Launched, Ground-Based, Sea-Based, Space-Based), By End-User (Army, Navy, Air Force, Space Force) Industry Region & Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Geopolitical Drivers, Growth Trends & Forecast 2026-2034")

, By Orbit (LEO, MEO, GEO), By Platform (Air-Launched, Ground-Based, Sea-Based, Space-Based), By End-User (Army, Navy, Air Force, Space Force) Industry Region & Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Geopolitical Drivers, Growth Trends & Forecast 2026-2034")