- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Antibody-Drug Conjugate Market Size, Share | CAGR 17.7%

Global Antibody-Drug Conjugate Market Size, Share, Growth Analysis By Drug Type (HER2-Targeting ADCs, TROP2-Targeting ADCs, Folate Receptor-Targeting ADCs, CD79b-Targeting ADCs), By Linker Type (Cleavable, Non-Cleavable, Disulfide, Hydrazone), By Payload Type (Auristatins, Maytansinoids, Camptothecin Derivatives, PBDs), By Therapeutic Area, By End-User & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 8.94 Billion | USD 38.76 Billion | 17.7% | North America, 48.2% |

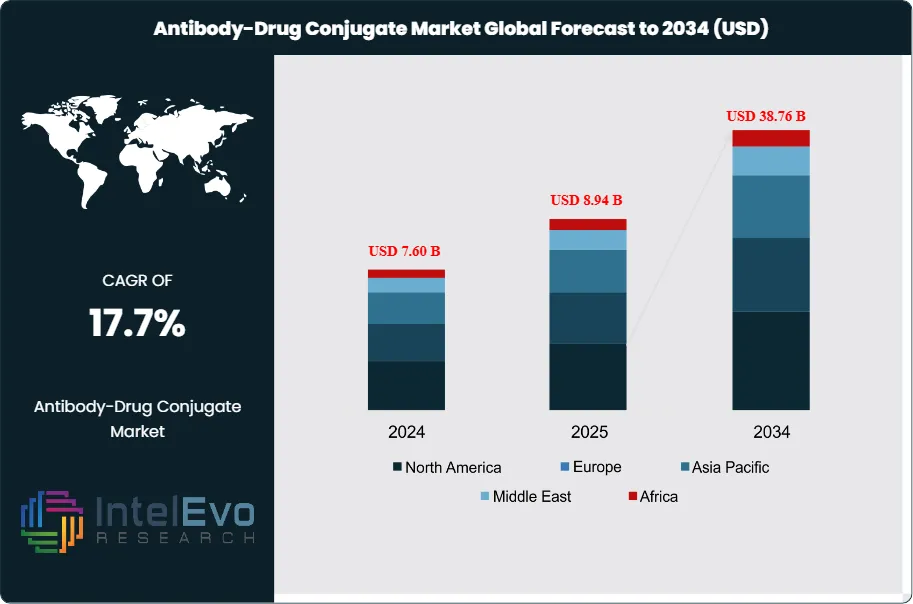

The Antibody-Drug Conjugate Market was valued at approximately USD 7.60 Billion in 2024 and reached USD 8.94 Billion in 2025. The market is projected to grow to USD 38.76 Billion by 2034, expanding at a CAGR of 17.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 29.82 Billion over the analysis period, driven by a record pipeline of ADC clinical programs, accelerating label expansions across approved products, and surging pharmaceutical investment in targeted oncology modalities that minimize systemic toxicity relative to conventional chemotherapy.

Get More Information about this report -

Request Free Sample ReportAntibody-drug conjugates are engineered biologic constructs that combine the target specificity of monoclonal antibodies with the cytotoxic potency of small-molecule payloads via precision-engineered linker chemistry. As of 2025, fourteen ADCs have received FDA approval under the Biologics License Application (BLA) pathway, with over 150 additional candidates in active clinical trials globally. The FDA's Oncology Center of Excellence has designated ADCs a priority modality class under its Project Optimus framework, which mandates dose optimization data for oncology drug filings, directly increasing clinical development investment in the ADC market. The European Medicines Agency (EMA) has similarly expedited ADC reviews under its PRIME designation scheme, with four ADCs receiving PRIME status between 2023 and 2025.

The antibody-drug conjugate market is concentrated in oncology, which accounts for 94.2% of total market revenue in 2025, with breast cancer, lung cancer, and hematologic malignancies representing the three largest therapeutic areas. HER2-targeting ADCs led by Enhertu (trastuzumab deruxtecan, AstraZeneca/Daiichi Sankyo) and Kadcyla (ado-trastuzumab emtansine, Roche) collectively generated USD 5.1 Billion in 2024 global revenue, demonstrating the commercial scalability achievable with differentiated ADC platforms. The TROP2 antigen target class is the fastest-growing ADC segment, with three TROP2-targeting candidates in pivotal trials as of mid-2025, reflecting industry consensus that TROP2 expression patterns across breast, lung, and urothelial cancers create a large multi-indication addressable market.

Strategic consolidation is reshaping the antibody-drug conjugate market structure. Pfizer's USD 43 Billion acquisition of Seagen in 2023, fully integrated by 2024, created the most extensive commercial ADC portfolio in the industry. AbbVie's USD 10.1 Billion acquisition of ImmunoGen in 2024 secured Elahere (mirvetuximab soravtansine), the first approved ADC for folate receptor-alpha-positive ovarian cancer. These transactions collectively transferred over USD 53 Billion in strategic value, signaling C-suite consensus that ADC platforms represent multi-decade revenue assets with significant label expansion optionality. Venture investment in ADC biotech startups reached USD 3.8 Billion globally in 2024, sustaining a deep preclinical pipeline that will feed clinical stage activity through 2034.

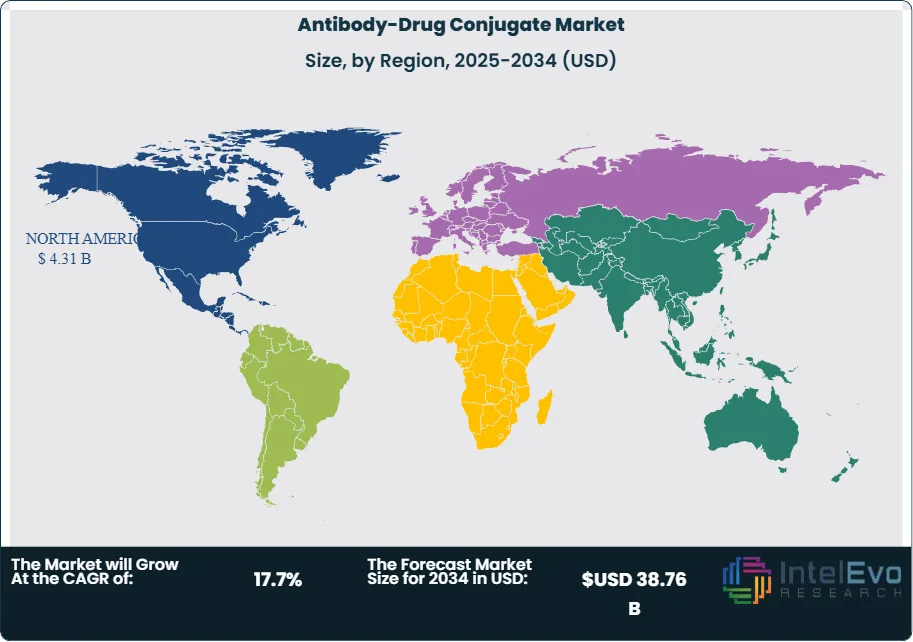

Regional dynamics in the antibody-drug conjugate market reflect both oncology disease burden and healthcare infrastructure capacity. North America holds 48.2% of the 2025 market at USD 4.31 Billion, supported by high oncology drug reimbursement rates and a dense network of National Cancer Institute (NCI)-designated cancer centers driving early ADC adoption. Asia Pacific is the fastest-growing region, with Japan contributing disproportionately due to Daiichi Sankyo's ADC partnership revenues and China's National Medical Products Administration (NMPA) accelerating ADC regulatory reviews under priority review pathways introduced in 2023.

, By Linker Type (Cleavable, Non-Cleavable, Disulfide, Hydrazone), By Payload Type (Auristatins, Maytansinoids, Camptothecin Derivatives, PBDs), By Therapeutic Area, By End-User & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global antibody-drug conjugate market was valued at USD 8.94 Billion in 2025 and is forecast to reach USD 38.76 Billion by 2034, expanding at a CAGR of 17.7% across the 2026-2034 forecast period.

- Segment Dominance: HER2-targeting ADCs lead the By Drug Type segment with a 38.5% share in 2025, valued at USD 3.44 Billion, underpinned by the commercial success of Enhertu and Kadcyla across breast and gastric cancer indications globally.

- Segment Dominance: Breast cancer leads the By Therapeutic Area segment with 42.0% market share in 2025, representing USD 3.76 Billion in revenue, driven by multiple approved ADCs across HER2-positive, HER2-low, and TROP2-expressing breast cancer subtypes.

- Driver: An unprecedented ADC clinical pipeline exceeding 150 active trials in 2025, supported by USD 3.8 Billion in venture capital deployment in 2024, is accelerating the rate of new indication approvals and sustaining above-market revenue growth through 2034.

- Restraint: ADC manufacturing complexity, requiring bioconjugation suites with controlled drug-antibody ratio (DAR) processing and cytotoxic containment infrastructure at biosafety level 2, increases cost of goods by 35-55% versus standard monoclonal antibody biologics, constraining margin profiles and limiting manufacturer capacity.

- Opportunity: Bispecific ADC platforms and ADC-immunotherapy combination regimens represent the largest emerging commercial opportunity, with an estimated addressable market of USD 12 Billion by 2034 across solid tumor indications where single-agent ADC monotherapy demonstrates insufficient durable response rates.

- Trend: Site-specific conjugation technology, replacing heterogeneous DAR mixtures (DAR 0-8) with homogeneous DAR 2 or DAR 4 constructs, is the defining ADC manufacturing trend of 2025, with 68% of new ADC IND filings using site-specific linker attachment strategies versus 31% in 2020.

- Regional Analysis: North America leads all regions with a 48.2% share in 2025, representing USD 4.31 Billion in revenue, supported by fourteen FDA-approved ADCs, NCI-designated cancer center adoption, and the highest oncology drug reimbursement rates globally.

Competitive Landscape Overview

The antibody-drug conjugate market exhibits moderate consolidation in 2025, with the top four companies — Pfizer, AstraZeneca, Roche, and AbbVie — collectively holding approximately 58% of global market revenue. Competition is technology-driven, centered on antibody engineering precision, linker stability profiles, payload potency class, and clinical differentiation across increasingly crowded antigen target classes including HER2, TROP2, and folate receptor-alpha. M&A intensity remains high, with six significant ADC-focused transactions exceeding USD 500 Million completed between 2024 and mid-2025. The entry of Chinese biotech companies including Duality Biologics and Kelun-Biotech into major out-licensing agreements with Big Pharma has introduced a new competitive dynamic, with Asian ADC technology platforms now commanding deal structures comparable to US and European counterparts.

Competitive Landscape Matrix

| Company | HQ | Position | Key ADC Product | Geo Strength | Recent Strategic Move (2024-2026) |

| Pfizer Inc. | USA | Leader | Padcev (enfortumab vedotin) | North America / Global | Completed USD 43B Seagen acquisition integration (2024); launched ADC portfolio expansion targeting 8 new oncology indications through 2027. |

| AstraZeneca plc | UK | Leader | Enhertu (trastuzumab deruxtecan) | Global | Received FDA approval for Enhertu in HR+/HER2-low breast cancer (2024); global Enhertu revenue exceeded USD 3.1B in 2024, up 76% year-on-year. |

| Roche / Genentech | Switzerland | Leader | Kadcyla (ado-trastuzumab emtansine) | Europe / North America | Initiated Phase III trial for next-generation HER2-targeting ADC RO7325503 in combination with atezolizumab (Q1 2025). |

| AbbVie Inc. | USA | Leader | Teliso-V (telisotuzumab vedotin) | North America | FDA approved Teliso-V for c-Met-high NSCLC in August 2025, opening a USD 1.2B addressable indication and expanding the non-breast ADC market. |

| Daiichi Sankyo | Japan | Challenger | Dato-DXd (datopotamab deruxtecan) | Asia Pacific / Global | Secured FDA Breakthrough Therapy designation for Dato-DXd in NSCLC (2025); expects filing NDA by end of 2025 for accelerated US approval. |

| Gilead Sciences | USA | Challenger | Trodelvy (sacituzumab govitecan) | North America | Expanded Trodelvy label to HR+/HER2- breast cancer following Phase III TROPiCS-02 data readout; targeting USD 2B peak sales by 2026. |

| Seagen / Pfizer | USA | Challenger | Tukysa + ADC combination | North America | Pfizer-Seagen combination pipeline yielded 3 IND filings for novel ADC-immunotherapy combinations in H1 2025. |

| ImmunoGen Inc. | USA | Niche Player | Elahere (mirvetuximab soravtansine) | North America | ABBV-CLS-7262 out-licensing deal with AbbVie signed for USD 580M upfront (Jan 2026), validating maytansinoid ADC payload platform. |

| Mersana Therapeutics | USA | Niche Player | Upifitamab rilsodotin (UpRi) | North America | Reported Phase II UpRi data showing 39% ORR in platinum-resistant ovarian cancer (Sep 2025), supporting BLA filing preparation. |

| MSD / Merck | USA | Challenger | MK-2870 (sacituzumab tirumotecan) | North America / Asia Pacific | Entered co-development agreement with Kelun-Biotech for MK-2870 across 6 solid tumor indications; Phase III enrollment commenced Q2 2025. |

By Drug Type / Antigen Target:

HER2-targeting ADCs command the largest segment share at 38.5% in 2025, valued at USD 3.44 Billion, reflecting the commercial maturity of Enhertu and Kadcyla and the clinical depth of the HER2 ADC pipeline across breast, gastric, and lung cancer indications. The label expansion of Enhertu into HER2-low metastatic breast cancer in 2024, covering an estimated 60% of all metastatic breast cancer patients in the US, fundamentally expanded the addressable HER2 ADC market beyond the traditional HER2-positive 15-20% of patients. TROP2-targeting ADCs hold 22.0% share at USD 1.97 Billion, with Trodelvy (sacituzumab govitecan, Gilead) driving commercial revenues across triple-negative and HR+/HER2- breast cancer. Three additional TROP2 ADC candidates are in Phase III trials, creating competitive pressure on Trodelvy's pricing and market share through 2027. Folate receptor-alpha ADCs represent 14.5% at USD 1.30 Billion, anchored by Elahere in platinum-resistant ovarian cancer. CD79b-targeting ADCs account for 12.5% at USD 1.12 Billion, led by Polivy (polatuzumab vedotin) in diffuse large B-cell lymphoma. Other antigen-targeting ADCs — including c-Met, Nectin-4, and B7-H3 programs — collectively represent 12.5% at USD 1.12 Billion, a segment growing fastest as new antigen classes progress through clinical development.

By Linker Type:

Cleavable linkers constitute 64.5% of the ADC market in 2025, valued at USD 5.77 Billion, and represent the dominant linker architecture across most approved products. Cleavable linker systems — encompassing protease-cleavable valine-citrulline sequences, pH-sensitive hydrazone bonds, and glutathione-responsive disulfide chemistry — release cytotoxic payloads selectively in the low-pH, protease-rich tumor microenvironment, enhancing therapeutic index by reducing systemic payload exposure. The proprietary tetrapeptide cleavable linker employed in Daiichi Sankyo's DXd-platform ADCs has become the industry benchmark for stability-selectivity balance, supporting a drug-antibody ratio of 8 while maintaining favorable pharmacokinetic profiles. Non-cleavable linkers hold 35.5% share at USD 3.17 Billion, preferred in hematologic malignancy indications where lysosomal degradation of the entire ADC construct within tumor cells is reliably achieved, generating active metabolite payloads without requiring specific tumor microenvironment characteristics.

By Payload / Cytotoxic Agent:

Auristatins (MMAE and MMAF) represent the largest payload class with 34.0% market share, valued at USD 3.04 Billion in 2025. Their microtubule-disrupting mechanism of action, potency in the subnanomolar IC50 range, and established manufacturability have made auristatins the most widely deployed ADC payload class. Camptothecin derivatives, primarily DXd and SN-38, are the fastest-growing payload class at 28.5% share (USD 2.55 Billion), reflecting the clinical dominance of Daiichi Sankyo's DXd-platform ADCs. DXd's bystander killing effect — the ability to kill antigen-negative tumor cells adjacent to antigen-positive cells through membrane-permeable payload diffusion — provides a clinical differentiation advantage in heterogeneous solid tumors. Maytansinoids (DM1 and DM4) hold 22.5% share at USD 2.01 Billion, anchored by Kadcyla's established breast cancer franchise. Calicheamicin accounts for 8.0% at USD 0.72 Billion, primarily through Mylotarg and Besylomab in hematologic malignancies. Pyrrolobenzodiazepine (PBD) dimers represent 7.0% at USD 0.63 Billion, used in highly potent ADC programs targeting low-antigen-expressing solid tumors.

By Therapeutic Area:

Breast cancer leads at 42.0% share, valued at USD 3.76 Billion in 2025, reflecting the largest number of approved ADCs in any single tumor type. Lung cancer represents 18.5% at USD 1.65 Billion, with both NSCLC (Enhertu in HER2-mutant lung, Dato-DXd pending approval) and SCLC programs building a substantial pipeline. Hematologic malignancies (AML, DLBCL, multiple myeloma) account for 17.0% at USD 1.52 Billion, supported by Mylotarg, Polivy, Blenrep, and Pepaxto. Urothelial and bladder cancer holds 12.5% at USD 1.12 Billion, driven by Padcev (enfortumab vedotin). Ovarian cancer represents 6.0% at USD 0.54 Billion, growing at an above-average rate following Elahere approval. Other solid tumors contribute 4.0% at USD 0.36 Billion.

By End-User:

Hospitals and NCI-designated cancer centers represent 58.5% of ADC consumption at USD 5.23 Billion in 2025, reflecting the current requirement for oncologist-supervised infusion administration and on-site adverse event management. Specialty oncology clinics hold 24.0% share at USD 2.15 Billion, gaining share as administration protocols mature and safety monitoring requirements become more standardized. Academic medical centers account for 12.0% at USD 1.07 Billion, serving dual roles as clinical trial enrollment sites and early commercial adopters. CDMOs and contract manufacturers represent 5.5% at USD 0.49 Billion, capturing ADC manufacturing outsourcing revenue as capacity demands exceed in-house biomanufacturing investment rates.

Regional Analysis

North America

North America commands 48.2% of the global antibody-drug conjugate market in 2025, valued at USD 4.31 Billion. The United States accounts for 93% of North American ADC revenue, driven by fourteen FDA-approved ADC products, the highest oncology drug formulary access rates globally, and a reimbursement environment where Centers for Medicare and Medicaid Services (CMS) average sales price (ASP) payment methodology supports ADC pricing at USD 10,000-35,000 per treatment cycle. The NCI-designated cancer center network, comprising 72 centers nationally, functions as an early adoption engine for newly approved ADCs, generating rapid volume uptake within 6-12 months of approval. Canada contributes 6% of regional revenue, with provincial drug formulary reviews creating 12-18 month delays versus US approval timelines. The 340B Drug Pricing Program in the US, covering over 2,500 safety-net healthcare providers, is simultaneously expanding ADC patient access and creating pricing pressure as covered entities negotiate deeper discounts. North America is forecast to grow at a CAGR of 16.8% to reach USD 18.2 Billion by 2034.

Europe

Europe accounts for 22.6% of the global antibody-drug conjugate market in 2025, at USD 2.02 Billion. Germany leads European ADC demand with 26% of regional revenue, supported by the AMNOG (Arzneimittelmarktneuordnungsgesetz) benefit assessment system that evaluates ADC added benefit versus comparator therapies within 12 months of approval. France holds 19% through its Autorisation d'Acces Precoce (AAP) early access program, which has granted temporary ADC access to over 8,000 French oncology patients since 2022. The UK contributes 17%, with NICE technology appraisals for Enhertu and Trodelvy delivering positive recommendations that drive NHS formulary access across Integrated Care Boards. Switzerland represents 10%, home to Roche and its Kadcyla global manufacturing and regulatory operations. The EMA's PRIME designation program has reduced average European ADC approval timelines from 13.2 months to 9.8 months for priority products, accelerating revenue uptake. European market growth is forecast at a CAGR of 16.4% to reach USD 8.36 Billion by 2034.

Asia Pacific

Asia Pacific represents 21.8% of the global antibody-drug conjugate market in 2025, valued at USD 1.95 Billion, and is the fastest-growing region at a projected CAGR of 20.1% through 2034, reaching USD 11.78 Billion. Japan is the largest Asia Pacific market at 34% of regional revenue (USD 663 Million), reflecting Daiichi Sankyo's domestic ADC manufacturing and the Japanese PMDA's Priority Review system, which approved three ADCs within 18 months of US approvals between 2023 and 2025. China accounts for 29% of Asia Pacific revenue at USD 566 Million, with NMPA's priority review classification for ADCs cutting approval timelines from 26 months to 12-14 months following 2023 regulatory reforms. South Korea contributes 16%, driven by Samsung Biologics' USD 2.1 Billion ADC CDMO expansion investment and growing domestic ADC clinical trial activity by Hanmi Pharmaceutical and Legochem Biosciences. India represents 12%, primarily through ADC clinical trial enrollment and API manufacturing for international supply chains, with domestic ADC commercialization expected by 2027.

Latin America

Latin America holds 4.6% of the global antibody-drug conjugate market in 2025, valued at USD 411 Million. Brazil represents 54% of regional revenue, with ANVISA's priority drug review pathway reducing ADC approval timelines by 40% since 2022. Mexico accounts for 26%, with COFEPRIS regulatory harmonization with FDA approval decisions accelerating market entry. Argentina contributes 12%, with ADC access concentrated in private healthcare sector oncology practices. Public healthcare system ADC reimbursement across Brazil's SUS (Sistema Unico de Saude) remains limited to two approved ADCs, constraining volume growth in the largest market. The Pan American Health Organization (PAHO) pooled procurement initiative for oncology biologics is expected to create a regional ADC access mechanism by 2027, potentially doubling the reimbursed patient population. Regional growth is forecast at a CAGR of 17.2% to reach USD 1.62 Billion by 2034.

Middle East and Africa

Middle East and Africa accounts for 2.8% of the global antibody-drug conjugate market in 2025, valued at USD 250 Million. The UAE leads with 38% of MEA revenue, driven by Dubai Healthcare City's oncology center infrastructure and Gulf Cooperation Council (GCC) reimbursement schemes for innovative oncology biologics. Saudi Arabia holds 35%, with the Saudi Food and Drug Authority (SFDA) fast-track review pathway for oncology products approved in 2024 reducing registration timelines by 35%. South Africa represents 18%, with ADC access concentrated in private hospital groups Discovery Health and Mediclinic International. Regional infrastructure gaps in cold-chain logistics and specialized oncology nursing training limit ADC administration capacity in sub-Saharan Africa outside South Africa. International Finance Corporation (IFC) investments in private oncology healthcare capacity across Egypt and Kenya are creating early-stage ADC market development conditions. The region is forecast to grow at a CAGR of 18.1% to reach USD 1.25 Billion by 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Drug Type / Modality

- HER2-Targeting ADCs

- TROP2-Targeting ADCs

- Folate Receptor-Targeting ADCs

- CD79b-Targeting ADCs

- Other Antigen-Targeting ADCs

By Linker Type

- Cleavable Linkers (pH-sensitive, protease-cleavable)

- Non-Cleavable Linkers

- Disulfide Linkers

- Hydrazone Linkers

By Payload / Cytotoxic Agent

- Auristatins (MMAE / MMAF)

- Maytansinoids (DM1 / DM4)

- Calicheamicin

- Camptothecin Derivatives (DXd, SN-38)

- Pyrrolobenzodiazepines (PBD)

By Therapeutic Area

Breast Cancer

- Lung Cancer (NSCLC / SCLC)

- Blood Cancers (AML / DLBCL / MM)

- Urothelial / Bladder Cancer

- Colorectal Cancer

- Ovarian Cancer

- Other Solid Tumors

By End-User

- Hospitals & Cancer Centers

- Specialty Oncology Clinics

- Academic Medical Centers

- CDMO / Contract Manufacturers

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.94 B |

| Forecast Revenue (2034) | USD 38.76 B |

| CAGR (2025-2034) | 17.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Drug Type / Modality, (HER2-Targeting ADCs, TROP2-Targeting ADCs, Folate Receptor-Targeting ADCs, CD79b-Targeting ADCs, Other Antigen-Targeting ADCs ), By Linker Type, (Cleavable Linkers (pH-sensitive, protease-cleavable), Non-Cleavable Linkers, Disulfide Linkers, Hydrazone Linkers), By Payload / Cytotoxic Agent, (Auristatins (MMAE / MMAF), Maytansinoids (DM1 / DM4), Calicheamicin, Camptothecin Derivatives (DXd, SN-38), Pyrrolobenzodiazepines (PBD)), By Therapeutic Area (Breast Cancer, Lung Cancer (NSCLC / SCLC), Blood Cancers (AML / DLBCL / MM), Urothelial / Bladder Cancer, Colorectal Cancer, Ovarian Cancer, Other Solid Tumors), By End-User, (Hospitals & Cancer Centers, Specialty Oncology Clinics, Academic Medical Centers, CDMO / Contract Manufacturers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PFIZER INC., ASTRAZENECA PLC, ROCHE / GENENTECH, ABBVIE INC., DAIICHI SANKYO, GILEAD SCIENCES, IMMUNOGEN INC., MERSANA THERAPEUTICS, MSD / MERCK, SEAGEN (PFIZER), REGENERON PHARMACEUTICALS, SYNAFFIX BV, TUBULIS GMBH, SUTRO BIOPHARMA, ADC THERAPEUTICS, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Linker Type (Cleavable, Non-Cleavable, Disulfide, Hydrazone), By Payload Type (Auristatins, Maytansinoids, Camptothecin Derivatives, PBDs), By Therapeutic Area, By End-User & Forecast 2026-2034")

, By Linker Type (Cleavable, Non-Cleavable, Disulfide, Hydrazone), By Payload Type (Auristatins, Maytansinoids, Camptothecin Derivatives, PBDs), By Therapeutic Area, By End-User & Forecast 2026-2034")

, By Linker Type (Cleavable, Non-Cleavable, Disulfide, Hydrazone), By Payload Type (Auristatins, Maytansinoids, Camptothecin Derivatives, PBDs), By Therapeutic Area, By End-User & Forecast 2026-2034")

Frequently Asked Questions

How big is the Antibody-Drug Conjugate Market?

The Global Antibody-Drug Conjugate Market was valued at USD 7.60 Billion in 2024 and is projected to reach USD 38.76 Billion by 2034, growing at a CAGR of 17.7% from 2026 to 2034, driven by rising cancer prevalence, increasing approvals of targeted oncology therapies, advancements in linker and payload technologies, and growing investments in precision medicine and biologics development.

Who are the major players in the Antibody-Drug Conjugate Market?

PFIZER INC., ASTRAZENECA PLC, ROCHE / GENENTECH, ABBVIE INC., DAIICHI SANKYO, GILEAD SCIENCES, IMMUNOGEN INC., MERSANA THERAPEUTICS, MSD / MERCK, SEAGEN (PFIZER), REGENERON PHARMACEUTICALS, SYNAFFIX BV, TUBULIS GMBH, SUTRO BIOPHARMA, ADC THERAPEUTICS, OTHERS

Which segments covered the Antibody-Drug Conjugate Market?

By Drug Type / Modality, (HER2-Targeting ADCs, TROP2-Targeting ADCs, Folate Receptor-Targeting ADCs, CD79b-Targeting ADCs, Other Antigen-Targeting ADCs ), By Linker Type, (Cleavable Linkers (pH-sensitive, protease-cleavable), Non-Cleavable Linkers, Disulfide Linkers, Hydrazone Linkers), By Payload / Cytotoxic Agent, (Auristatins (MMAE / MMAF), Maytansinoids (DM1 / DM4), Calicheamicin, Camptothecin Derivatives (DXd, SN-38), Pyrrolobenzodiazepines (PBD)), By Therapeutic Area (Breast Cancer, Lung Cancer (NSCLC / SCLC), Blood Cancers (AML / DLBCL / MM), Urothelial / Bladder Cancer, Colorectal Cancer, Ovarian Cancer, Other Solid Tumors), By End-User, (Hospitals & Cancer Centers, Specialty Oncology Clinics, Academic Medical Centers, CDMO / Contract Manufacturers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Antibody-Drug Conjugate Market

Published Date : 18 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date