- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Antimicrobial Packaging Market Size, Share & Growth Analysis | 7.4% CAGR

Global Antimicrobial Packaging Market Size, Share & Industry Analysis By Material Type (Plastic, Biopolymer, Paperboard, Other Material Types), By Antimicrobial Agents (Organic Acids, Enzymes, Essential Oils, Bacteriocins, Other Antimicrobial Agents), By Packaging Type (Bags, Pouches, Cartons, Trays, Other Packaging Types), By Application (Food & Beverages, Healthcare, Personal Care, Other Applications) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034

Report Overview

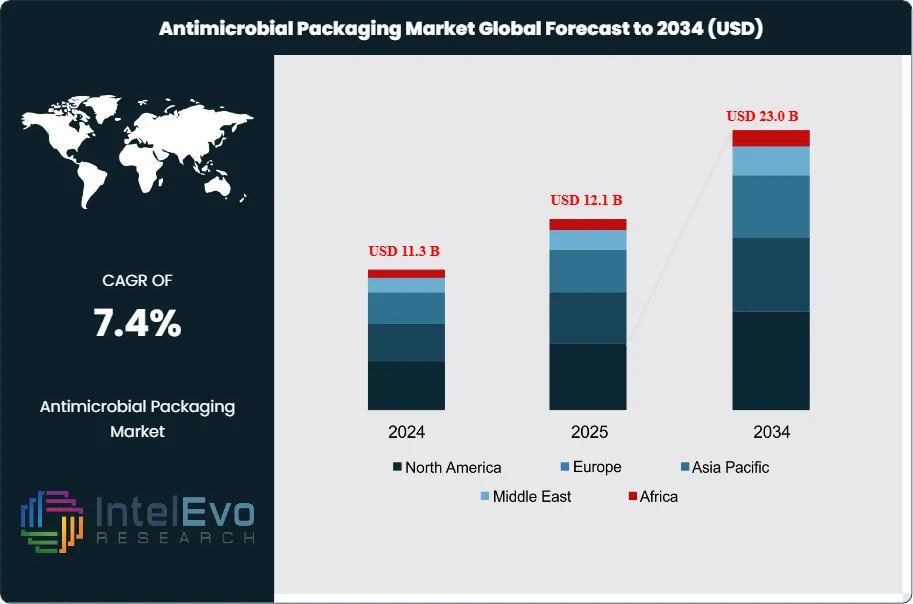

The Antimicrobial Packaging Market was valued at USD 11.3 Billion in 2024 and is estimated to reach approximately USD 12.1 Billion in 2025. Driven by increasing demand for extended shelf-life packaging solutions, rising concerns over food safety, and growing adoption of antimicrobial materials across food, healthcare, and pharmaceutical packaging, the market is projected to grow from about USD 13.0 Billion in 2026 to nearly USD 23.0 Billion by 2034, registering a compound annual growth rate (CAGR) of around 7.4% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportAntimicrobial packaging embeds active agents into films, papers, and coatings to suppress bacteria, fungi, and other microbes. This functional shift positions packaging as a safety and quality-control layer, not only a container. Adoption concentrates in food, beverages, pharmaceuticals, and personal care, where spoilage reduction and contamination control translate directly into lower returns, fewer recalls, and longer distribution reach.

Demand accelerates as packaged-food volumes rise and as regulators tighten hygiene and shelf-life compliance. Global health exposure remains material: foodborne illnesses affect about 600 million people each year and contribute to roughly 420,000 deaths, reinforcing the economic and public-health rationale for contamination-mitigation tools. Consumers also push the market toward sustainability outcomes. Around 64% prefer brands that use sustainable packaging, nearly half show willingness to pay a premium, and 75% of companies report commitments to sustainable packaging, yet fewer than 30% indicate readiness to meet regional standards or internal targets. This gap increases near-term demand for validated, audit-ready antimicrobial solutions.

On the supply side, material innovation and manufacturing scale-up set the pace. Producers balance efficacy with safety limits, migration thresholds, and recycling compatibility, while navigating approval timelines that can extend product qualification cycles by 9–18 months in regulated end uses. Investment signals intensify around circularity and resin innovation. SK Chemicals has invested USD 98.4 million to acquire a chemical recycling facility and a PET production plant with 70,000 metric tons of annual depolymerization capacity and 50,000 metric tons of rPET output, supporting antimicrobial formats that also meet recycled-content mandates.

Technology adoption increasingly shapes competitiveness. AI-enabled quality inspection, automated dosing controls for additives, and digital traceability systems reduce defect rates and strengthen compliance documentation. Smart-packaging concepts, including embedded indicators and data-linked labels, support tighter cold-chain monitoring and faster root-cause analysis during incidents. Risks persist in cost inflation for specialty additives, performance trade-offs in bio-based substrates, and enforcement actions tied to unverified sustainability claims.

Regionally, North America and Europe account for an estimated 55% of revenue due to stringent food and pharmaceutical standards, while Asia-Pacific posts the fastest growth at roughly 8.5% CAGR, led by China, India, and Southeast Asia as modern retail expands. Near-term investment hotspots center on bio-based antimicrobial chemistries, nanostructured coatings, and scalable recycling-integrated packaging platforms that reduce waste while sustaining product protection.

, By Antimicrobial Agents (Organic Acids, Enzymes, Essential Oils, Bacteriocins, Other Antimicrobial Agents), By Packaging Type (Bags, Pouches, Cartons, Trays, Other Packaging Types), By Application (Food & Beverages, Healthcare, Personal Care, Other Applications) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market grows at a 7.4% CAGR, 2024-2034, rising from 10.5 billion USD, 2024 to 23.0 billion USD, 2034.

- Segment Dominance: Plastic leads material types with 56.1%, 2024, supported by cost and durability at scale (estimated: 6.3 billion USD, 2024).

- Segment Dominance: Organic acids lead antimicrobial agents with 32.3%, 2024, reflecting strong fit for food safety use cases (estimated: 3.7 billion USD, 2024).

- Driver: Food and beverages drive adoption with 43.1%, 2024, as brands prioritize longer shelf life and contamination control (estimated: 4.9 billion USD, 2024).

- Restraint: Compliance and validation cycles raise time-to-market and cost (estimated: 12.0 months, 2024), which slows new material and additive approvals.

- Opportunity: Sustainable antimicrobial formats expand as buyers shift spend toward verified eco-design (estimated: 0.9 billion USD, 2024) and scale through 2034.

- Trend: Flexible formats gain share as pouches reach 43.5%, 2024, and suppliers digitize production controls (estimated: 18.0% adoption, 2024).

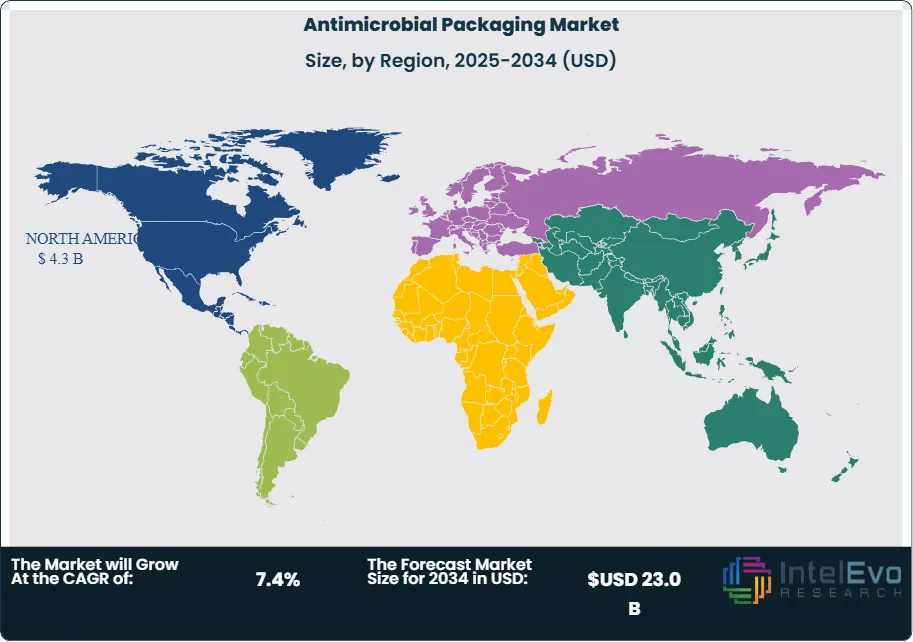

- Regional Analysis: Asia-Pacific leads with 38.2%, 2024, backed by urbanization and packaged-food demand (estimated: 4.3 billion USD, 2024).

By Type

In 2025, plastics remain the primary substrate for antimicrobial packaging, supported by established converting capacity, predictable barrier performance, and low unit economics across high-volume SKUs. Plastic materials accounted for 56.1% of market revenue in 2023, and this dominance is expected to persist through the late 2020s as food and healthcare brands prioritize moisture and oxygen resistance at scale. Polyethylene and polypropylene continue to anchor most flexible formats because they integrate cleanly with additive masterbatches and antimicrobial coatings used in commercial production.

Biopolymers expand from a smaller base as regulators and retailers increase scrutiny of waste and recycled content. Growth concentrates in compostable or bio-based films where suppliers can demonstrate migration compliance and shelf-life performance comparable to conventional plastics. Paperboard maintains traction in selected dry-food and secondary packaging formats, but it faces constraints in high-moisture applications due to lower intrinsic barrier properties unless paired with functional coatings. Metals and glass remain niche options tied to stringent protection requirements in pharmaceuticals and medical devices, where rigid formats and high integrity matter more than lightweighting.

The outlook beyond 2025 depends on how quickly material platforms meet both antimicrobial efficacy targets and end-of-life requirements. Brands increasingly demand packaging that supports recycling stream compatibility and clear documentation on additive safety. This raises the bar for qualification and can extend commercialization timelines, particularly for new bio-based structures.

By Application

Flexible formats dominate antimicrobial packaging demand because they reduce material usage per unit while delivering barrier performance. Pouches captured 43.5% of packaging-type share in 2023, and they continue to benefit from rapid growth in ready-to-eat meals, sauces, dairy, and beverage concentrates through 2025 and beyond. Converters favor pouches because they run on high-speed lines and support multiple closure systems, which helps brand owners manage product variety without large cost penalties.

Bags retain a meaningful role in bulk and value-focused applications, particularly in dry foods and secondary containment where antimicrobial protection supports longer storage cycles. Cartons hold steady in selected perishable categories that require stackability and rigidity, but flexible formats typically win on cost per pack and distribution efficiency. Trays and other rigid formats concentrate in healthcare and certain fresh-food presentations where stability and sterility handling drive purchasing decisions.

After 2025, format selection increasingly reflects total landed cost and compliance risk. Brand owners also demand stronger validation evidence for antimicrobial claims across logistics conditions. This raises adoption hurdles for smaller suppliers but supports premium pricing for solutions with verified performance and traceable documentation.

By End-Use

Food and beverages represent the largest end-use driver for antimicrobial packaging, with a 43.1% application share recorded in 2023. The segment continues to expand in 2025 as manufacturers push longer distribution reach and reduce spoilage losses in chilled and ambient categories. Antimicrobial films and coatings help maintain product integrity during storage and transport, which supports fewer returns and better consistency across retail channels.

Healthcare and pharmaceuticals account for a smaller revenue base than food, but the segment grows steadily due to sterility requirements and tighter contamination controls. Packaging suppliers increasingly align product designs with regulatory expectations on material safety, additive migration, and labeling. Personal care applications also rise as consumers demand better hygiene outcomes and longer shelf stability in high-turn products. Industrial and household uses remain limited but stable, mainly where microbial control supports handling safety or storage life.

Looking forward, end-use growth hinges on compliance readiness and total cost. Qualification cycles can delay rollouts when products require food-contact and medical-grade verification. Suppliers that provide robust testing data and consistent manufacturing controls improve conversion rates across regulated buyers after 2025.

By Region

Asia Pacific leads global demand and held 38.2% market share in 2023, equivalent to about USD 4.0 billion. The region sustains momentum through 2025, driven by packaged-food growth, expanding cold-chain networks, and higher urban consumption in China, India, Japan, and Southeast Asia. Local producers also scale flexible packaging capacity quickly, which supports faster adoption of antimicrobial structures in mainstream categories.

North America remains a high-value market due to strict food safety expectations and strong healthcare and pharmaceutical activity in the United States and Canada. Investment focuses on validation, traceability, and manufacturing control, which supports recurring demand for proven antimicrobial additives and coatings. Europe tracks closely, supported by sustainability rules and retailer pressure for materials aligned with circularity targets. This favors bio-based and recyclable designs when suppliers can maintain barrier and safety performance.

Latin America and the Middle East and Africa expand from smaller bases after 2025. Growth ties to modern retail penetration, rising imports, and healthcare investment in markets such as Brazil, Mexico, the UAE, and Saudi Arabia. Adoption accelerates where suppliers can offer cost-stable solutions that meet local compliance needs and perform across longer distribution routes.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Material Type

- Plastic

- Biopolymer

- Paperboard

- Other Material Types

By Antimicrobial Agents

- Organic Acids

- Enzymes

- Essential Oils

- Bacteriocins

- Other Antimicrobial Agents

By Packaging Type

- Bags

- Pouches

- Cartons

- Trays

- Other Packaging Types

By Application

- Food and Beverages

- Healthcare

- Personal Care

- Other Applications

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 12.1 B |

| Forecast Revenue (2034) | USD 23.0 B |

| CAGR (2025-2034) | 7.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material Type (Plastic, Biopolymer, Paperboard, Other Material Types), By Antimicrobial Agents (Organic Acids, Enzymes, Essential Oils, Bacteriocins, Other Antimicrobial Agents), By Packaging Type (Bags, Pouches, Cartons, Trays, Other Packaging Types), By Application (Food and Beverages, Healthcare, Personal Care, Other Applications) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BASF SE, Amcor plc, Tetra Pak International S.A., DuPont, Sealed Air Corporation, Dunmore Europe GmbH, Mondi Group, Berry Global Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Antimicrobial Agents (Organic Acids, Enzymes, Essential Oils, Bacteriocins, Other Antimicrobial Agents), By Packaging Type (Bags, Pouches, Cartons, Trays, Other Packaging Types), By Application (Food & Beverages, Healthcare, Personal Care, Other Applications) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

, By Antimicrobial Agents (Organic Acids, Enzymes, Essential Oils, Bacteriocins, Other Antimicrobial Agents), By Packaging Type (Bags, Pouches, Cartons, Trays, Other Packaging Types), By Application (Food & Beverages, Healthcare, Personal Care, Other Applications) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

, By Antimicrobial Agents (Organic Acids, Enzymes, Essential Oils, Bacteriocins, Other Antimicrobial Agents), By Packaging Type (Bags, Pouches, Cartons, Trays, Other Packaging Types), By Application (Food & Beverages, Healthcare, Personal Care, Other Applications) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Landscape, Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Antimicrobial Packaging Market?

The Global Antimicrobial Packaging Market was valued at USD 11.3 Billion in 2024 and is projected to reach USD 23.0 Billion by 2034, growing at a CAGR of 7.4% from 2026–2034. Explore market trends, food safety packaging innovations, key growth drivers, competitive landscape, and future opportunities.

Who are the major players in the Antimicrobial Packaging Market?

BASF SE, Amcor plc, Tetra Pak International S.A., DuPont, Sealed Air Corporation, Dunmore Europe GmbH, Mondi Group, Berry Global Inc.

Which segments covered the Antimicrobial Packaging Market?

By Material Type (Plastic, Biopolymer, Paperboard, Other Material Types), By Antimicrobial Agents (Organic Acids, Enzymes, Essential Oils, Bacteriocins, Other Antimicrobial Agents), By Packaging Type (Bags, Pouches, Cartons, Trays, Other Packaging Types), By Application (Food and Beverages, Healthcare, Personal Care, Other Applications)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Antimicrobial Packaging Market

Published Date : 06 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date