- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global API Security Platform Market Size, Share & Forecast | CAGR 13.5%

Global API Security Platform Market Size, Share, Growth Analysis By Component (Platform/Solution, Professional Services, Managed Security Services), By Deployment Mode (Cloud-Based SaaS, On-Premise, Hybrid), By Security Type (API Discovery, Threat Detection, Authentication Security, Bot Mitigation, API Gateway Security, Data Leakage Protection), By Enterprise Size, By End-User Vertical, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

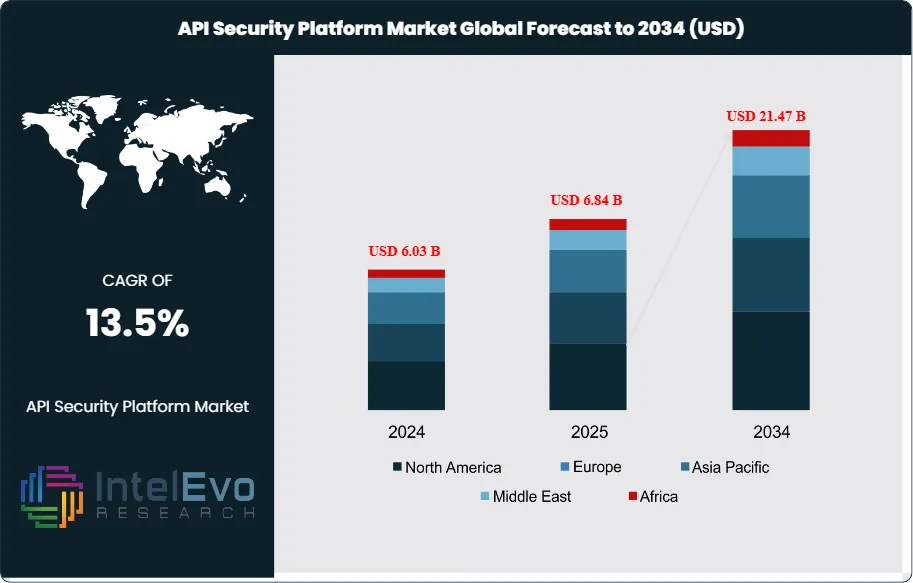

| USD 6.84 Billion | USD 21.47 Billion | 13.5% | North America, 43.2% |

The API Security Platform Market was valued at approximately USD 6.03 Billion in 2024 and reached USD 6.84 Billion in 2025. The market is projected to grow to USD 21.47 Billion by 2034, expanding at a CAGR of 13.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 14.63 Billion over the analysis period, driven by the rapid proliferation of API-connected architectures across enterprise software, the escalating frequency and sophistication of API-targeted cyberattacks, and tightening regulatory requirements mandating API security governance in financial services, healthcare, and critical infrastructure sectors.

Get More Information about this report -

Request Free Sample ReportAPI security platforms are purpose-built cybersecurity solutions that protect application programming interfaces from discovery gaps, authentication vulnerabilities, business logic abuse, data exfiltration, and volumetric attacks. As organizations migrate to microservices architectures, cloud-native development, and third-party ecosystem integrations, the API attack surface has expanded faster than traditional perimeter security tools can address. Industry analysis of breach investigation data indicates that API vulnerabilities were implicated in 68.3% of web application data breaches recorded in 2024 — a figure that underscores why API security has become a board-level technology priority distinct from conventional web application firewall (WAF) and application delivery controller investments. The average cost of an API-related data breach reached USD 4.87 Million in 2025, 16.4% above the overall average breach cost tracked by insurance actuarial data, reflecting the high volume of sensitive data transiting API channels.

The API security platform market is structured around five core capability domains: API discovery and inventory management, authentication and authorization security, runtime threat detection and response, API posture management, and sensitive data protection. Demand for integrated platforms covering all five domains is displacing point solutions focused on single capabilities. As of 2025, 58.7% of enterprise security buyers evaluated API security in the context of cloud-native application protection platform (CNAPP) consolidation — seeking vendors whose API security capabilities integrate with cloud workload protection, container security, and infrastructure-as-code scanning within a unified policy and analytics environment. The NIST Cybersecurity Framework 2.0, effective 2024, explicitly identifies API security governance as a critical function under the Protect and Detect categories, elevating API security from a developer concern to an enterprise security program requirement.

BFSI is the dominant end-user vertical at 31.8% of global API security platform revenue in 2025 at USD 2.18 Billion, driven by open banking mandates, PSD2 third-party provider API exposure in Europe, FDX open finance API standards in the United States, and the high value of financial data transiting payment, account aggregation, and trading APIs. Healthcare follows at 19.4% at USD 1.33 Billion, with HIPAA-protected health information (PHI) transmitted via EHR interoperability APIs under ONC 21st Century Cures Act information blocking rules creating direct security obligations. The technology and SaaS vertical represents 16.2% at USD 1.11 Billion, with hyperscale platform operators and SaaS companies managing millions of third-party API consumers requiring enterprise-grade API security governance.

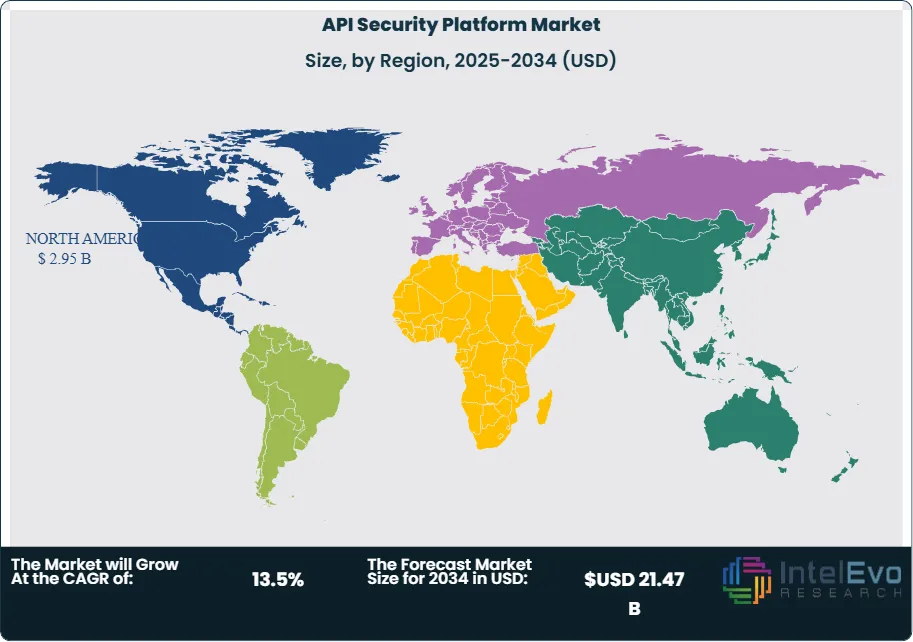

North America leads global API security platform demand with a 43.2% share at USD 2.95 Billion in 2025, anchored by the world's highest API deployment density, the concentration of global cybersecurity vendors, and CISA's binding operational directives mandating API security controls across US federal agencies. Europe accounts for 27.6% at USD 1.89 Billion, with DORA's ICT third-party risk provisions and NIS2 Directive security requirements driving API security investment among EU financial institutions and critical infrastructure operators. Asia Pacific is the fastest-growing region at 15.8% CAGR, with India's digital public infrastructure API ecosystem, Singapore's MAS TPRM guidelines, and China's expanding API economy generating strong platform demand.

, By Deployment Mode (Cloud-Based SaaS, On-Premise, Hybrid), By Security Type (API Discovery, Threat Detection, Authentication Security, Bot Mitigation, API Gateway Security, Data Leakage Protection), By Enterprise Size, By End-User Vertical, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global API security platform market was valued at USD 6.84 Billion in 2025 and is forecast to reach USD 21.47 Billion by 2034, growing at a CAGR of 13.5% during the 2026–2034 forecast period.

- Segment Dominance: By component, platform and solution offerings dominate with 64.3% of global revenue in 2025, as enterprises consolidate API discovery, threat detection, posture management, and data protection capabilities onto integrated platforms rather than maintaining disparate point tools across the API security stack.

- Segment Dominance: By security type, API discovery and inventory management leads with 22.8% of global revenue in 2025, reflecting the foundational nature of API visibility as the prerequisite capability for all downstream security functions — organizations cannot protect APIs they do not know exist.

- Driver: The global API call volume surpassed 100 trillion monthly transactions in 2025, growing at 28.4% annually as microservices architectures, mobile applications, and third-party ecosystem integrations multiply API exposure surfaces — each new API endpoint representing an unprotected attack vector until security controls are applied.

- Restraint: Alert fatigue and false-positive rates averaging 34–47% in legacy API security tools are undermining security operations center (SOC) confidence in API threat signals, slowing platform consolidation by compelling organizations to maintain parallel validation processes that increase total security operations cost by 19–28%.

- Opportunity: Securing AI agent-to-agent API communications — where LLM-based autonomous agents interact via API calls that bypass conventional human-review security gates — represents an estimated addressable market of USD 1.8 Billion by 2034, growing at 31.2% CAGR as agentic AI architectures proliferate across enterprise automation.

- Trend: Shift-left API security integration within CI/CD pipelines and API design toolchains reached 44.6% adoption among DevSecOps organizations in 2025, up from 18.3% in 2022, reflecting recognition that remediating API vulnerabilities in production costs 6.8 times more than addressing them at design or development stages.

- Regional Analysis: North America leads with a 43.2% market share at USD 2.95 Billion in 2025, driven by CISA federal API security directives, the highest enterprise API deployment density globally, and the concentration of world-leading API security platform vendors headquartered in the United States.

Competitive Landscape Overview

The API security platform market is moderately fragmented, with the top four vendors — Palo Alto Networks, CrowdStrike, Akamai Technologies (post-Noname acquisition), and Salt Security — accounting for approximately 46.7% of global revenue in 2025. Competition is technology-driven, with differentiation centered on AI behavioral analytics accuracy, protocol coverage breadth, API discovery completeness, and integration depth within broader CNAPP and extended detection and response (XDR) ecosystems. The market has experienced significant M&A consolidation since 2023, with major cybersecurity platform vendors acquiring pure-play API security specialists to add depth to their application security portfolios. Pure-play API security vendors face strategic pressure to either achieve sufficient scale to compete on platform breadth or accept acquisition by larger security platform operators, a dynamic that is compressing the independent vendor population and accelerating feature parity across the leading platforms.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move (2024–2026) |

| Palo Alto Networks | USA | Leader | Prisma Cloud API Security | North America / Europe | Acquired Apiiro for USD 500M to add API risk graph analytics, Mar 2025 |

| CrowdStrike | USA | Leader | Falcon API Security Module | North America / Europe | Launched AI-native API threat hunting across Falcon platform, Jun 2025 |

| Salt Security | USA | Challenger | Salt API Protection Platform | North America | Raised USD 140M Series D; expanded AI attack detection to gRPC/GraphQL, Feb 2025 |

| Noname Security | USA | Challenger | Noname API Security Platform | North America / Europe | Acquired by Akamai Technologies for USD 450M, May 2025 |

| Traceable AI | USA | Challenger | Traceable API Security | North America | Deployed LLM-powered API data leakage detection for BFSI sector, Aug 2025 |

| Imperva (Thales) | USA/France | Niche Player | Imperva API Security | North America / Europe | Integrated API security into Imperva Cloud WAF with unified policy engine, Oct 2025 |

| Akamai Technologies | USA | Leader | API Security (post-Noname) | Global | Completed Noname acquisition; unified API security under Akamai Guardicore platform, Jun 2025 |

| F5 Networks | USA | Niche Player | NGINX App Protect API Security | North America / APAC | Released NGINX API Connectivity Manager with zero-trust API gateway, Jan 2026 |

By Component

The API security platform market by component is led by platform and solution offerings, representing 64.3% of global revenue at USD 4.40 Billion in 2025. This segment encompasses standalone API security platforms, API security modules embedded within broader CNAPP and WAAP solutions, and API gateway security capabilities. Enterprise demand is shifting decisively toward integrated platforms covering the full API security lifecycle — from design-time specification scanning through runtime behavioral monitoring to post-incident forensics — as the cost and complexity of managing multiple-point API security tools across hybrid and multi-cloud environments becomes operationally unsustainable. Leading platform vendors including Palo Alto Prisma Cloud, CrowdStrike Falcon, and Akamai/Noname charge average enterprise annual contract values of USD 280,000–1.8 Million for API security platform subscriptions, with pricing driven by API call volume, number of API endpoints monitored, and breadth of module coverage.

Professional services represent 21.4% of market revenue at USD 1.46 Billion in 2025, covering API security assessment engagements, platform implementation and configuration, API penetration testing, threat modeling workshops, and developer security training. API security assessments from specialist firms average USD 45,000–180,000 per engagement depending on API portfolio complexity, and demand is driven by PCI DSS 4.0 Requirement 6.2.4 mandating API security testing in payment environments and DORA Article 26 ICT third-party API risk assessment requirements. Managed security services account for 14.3% at USD 978 Million, growing at 17.2% CAGR as resource-constrained security teams at mid-market organizations outsource API threat monitoring, incident response, and compliance reporting to managed detection and response (MDR) providers with dedicated API security capability.

By Deployment Mode

Cloud-based SaaS deployment leads the API security platform market at 71.6% of 2025 revenue, equivalent to USD 4.90 Billion. Cloud-delivered API security platforms offer elastic scalability to inspect API traffic volumes reaching hundreds of billions of daily transactions without infrastructure provisioning, automatic threat intelligence feed updates, and frictionless integration with cloud-native API gateways including AWS API Gateway, Azure API Management, and Google Apigee. The SaaS delivery model is particularly well-suited to API security because the API attack surface is predominantly cloud-resident — Cloudflare's network data indicates that 83.7% of web API traffic transits cloud infrastructure — making cloud-based interception and analysis architecturally optimal. Leading cloud API security platforms process threat intelligence across customer traffic pools, enabling cross-customer attack pattern detection that on-premise deployments cannot replicate.

On-premise deployments hold 16.8% of the market at USD 1.15 Billion in 2025, concentrated in government agencies subject to FedRAMP and IL4/IL5 data handling requirements, defense contractors operating in air-gapped environments, and financial institutions with legacy on-premise API infrastructure. This segment contracts at 2.8% annually as FedRAMP High-authorized cloud API security platforms reach availability and classified network API security requirements are addressed through dedicated government cloud deployments. Hybrid architectures represent 11.6% at USD 793 Million, serving enterprises with API traffic spanning on-premise legacy systems and cloud microservices simultaneously — a common configuration during cloud migration programs that typically spans 3–7 years for large financial institutions and healthcare organizations.

By Security Type

API discovery and inventory management is the leading security type in the API security platform market, accounting for 22.8% of revenue at USD 1.56 Billion in 2025. This capability addresses the foundational visibility gap — industry analysis indicates that the average enterprise has 40% more APIs in production than its security team is aware of, a category commonly referred to as shadow APIs. Automated API discovery using passive traffic analysis, active scanning of API gateway configurations, and code repository analysis can reduce shadow API exposure by 78–92% within 90 days of deployment, delivering immediate risk reduction that justifies budget authorization. Discovery platforms produce living API inventories that classify endpoints by sensitivity, authentication method, data type handled, and exposure level — feeding downstream security controls and compliance reporting.

Authentication and authorization security represents 19.6% of market revenue at USD 1.34 Billion in 2025, addressing OAuth 2.0 misconfiguration, broken object-level authorization (BOLA/IDOR), and JWT token vulnerabilities — the top three API vulnerability categories in the OWASP API Security Top 10 (2023 edition). API threat detection and response accounts for 18.4% at USD 1.26 Billion, using behavioral ML baselines to identify anomalous API call sequences indicative of account takeover, credential stuffing, or business logic abuse. API posture management holds 14.2% at USD 971 Million; bot mitigation and rate limiting 12.6% at USD 862 Million; and sensitive data and leakage protection 12.4% at USD 848 Million — the fastest-growing security type at 18.7% CAGR driven by GDPR, CCPA, and PCI DSS 4.0 API data exposure requirements.

By Enterprise Size

Large enterprises dominate the API security platform market, representing 69.4% of global revenue at USD 4.75 Billion in 2025. Organizations with more than 1,000 employees typically manage API portfolios of 500–15,000 endpoints and generate API traffic volumes requiring enterprise-grade monitoring infrastructure. Fortune 500 companies and global financial institutions are the highest-value accounts, with multi-year API security platform contracts averaging USD 750,000–4.2 Million annually when bundled with professional services and managed detection. Large enterprise buyers prioritize vendor ecosystem integration — specifically compatibility with existing SIEM, SOAR, XDR, and CNAPP investments — over standalone API security features, reflecting consolidation mandates from CISOs seeking to reduce security vendor sprawl.

Small and medium enterprises represent 30.6% of market revenue at USD 2.09 Billion in 2025, growing at 16.4% CAGR — the fastest segment growth rate — as cloud-native SME-oriented API security platforms emerge at accessible price points of USD 15,000–120,000 annually. SME API security demand is driven by SaaS companies whose entire business model is API-delivered, e-commerce operators subject to PCI DSS 4.0, and healthcare technology companies managing FHIR API interoperability obligations under the ONC Cures Act Final Rule. Product-led growth models from vendors including Traceable AI, Salt Security, and Escape are reducing SME onboarding friction, enabling API security deployments within 2–4 weeks without dedicated security engineering resources.

By End-User Vertical

The BFSI vertical leads API security platform adoption at 31.8% of global revenue at USD 2.18 Billion in 2025. Open banking regulations — including PSD2 in Europe, CDR in Australia, and FDX in the United States — mandate third-party API access to customer financial data, creating a structurally elevated attack surface that requires continuous API security governance. SWIFT's Customer Security Programme (CSP) and PCI DSS 4.0 Requirement 6.3 impose API vulnerability management obligations on global payment participants. A single unauthorized API access event at a Tier 1 bank can expose millions of account records, making API security investment a risk-weighted capital requirement analogous to credit risk provisioning. Average BFSI API security platform contract values are 34% above cross-industry averages, reflecting the regulatory compliance documentation and audit logging capabilities required alongside core security functions.

Healthcare and life sciences account for 19.4% at USD 1.33 Billion in 2025, driven by HL7 FHIR API mandates under the ONC Cures Act Final Rule, HIPAA Security Rule API audit controls, and the proliferation of health data exchange APIs connecting EHRs, payers, and patient-facing applications. Technology and SaaS companies represent 16.2% at USD 1.11 Billion, managing API ecosystems that serve millions of third-party developers and require enterprise-grade rate limiting, OAuth scope enforcement, and abuse detection. Retail and e-commerce holds 12.4% at USD 848 Million, with payment API security and account takeover prevention the primary use cases. Government and defense accounts for 9.8% at USD 670 Million, telecommunications 6.2% at USD 424 Million, and energy and utilities 4.2% at USD 287 Million.

Regional Analysis

North America API Security Platform Market

North America leads the global API security platform market with a 43.2% share at USD 2.95 Billion in 2025. The United States accounts for 88.1% of regional revenue at USD 2.60 Billion, reflecting the world's highest enterprise API deployment density, the home market advantage of leading API security vendors, and the most proactive regulatory posture on API security globally. CISA's Binding Operational Directive 23-02 mandating API vulnerability remediation across US federal agencies generated USD 340 Million in government API security procurement in fiscal year 2024 alone. The OCC's guidance on third-party API risk management and the CFPB's Personal Financial Data Rights Rule establishing consumer API access rights are each creating compliance-driven API security investment at US banks and fintech companies. The US technology sector — home to the world's largest API-economy companies including Salesforce, Twilio, Stripe, and AWS — maintains API security programs at a scale and sophistication that sets global market benchmarks. Canada contributes 8.2% of North American revenue, with OSFI's B-13 technology risk guideline driving financial institution API security investment. Mexico accounts for 3.7% of regional revenue, with adoption accelerating at domestic financial institutions and digital banking operators.

Europe API Security Platform Market

Europe holds 27.6% of global API security platform revenue at USD 1.89 Billion in 2025. The European market is distinguished by the density of compliance-driven API security mandates taking effect simultaneously across financial services, critical infrastructure, and technology sectors. DORA's ICT third-party risk requirements mandate that EU financial entities assess and monitor the API security posture of all technology providers with access to their systems — creating cascading API security procurement across the entire EU financial services supply chain. NIS2 Directive security measures, effective October 2024, impose API security controls on operators of essential services across energy, transport, health, and digital infrastructure sectors in all EU member states. Germany is the largest European market at 23.4% of regional revenue, driven by BaFin's technology risk supervision framework, the country's concentration of industrial IoT API deployments in manufacturing, and SAP's customer base driving API security investment in enterprise application environments. The UK contributes 20.8% of European revenue with NCSC API security guidance and FCA operational resilience requirements. France and the Netherlands each represent approximately 14–15% of European revenue.

Asia Pacific API Security Platform Market

Asia Pacific accounts for 18.6% of global API security platform revenue at USD 1.27 Billion in 2025, growing at 15.8% CAGR — the fastest regional rate globally. India is the largest and fastest-growing APAC market, representing 26.4% of regional revenue at USD 335 Million, driven by the world's largest digital public infrastructure (DPI) API ecosystem — covering Aadhaar identity, UPI payments, DigiLocker, and Account Aggregator frameworks — which collectively process over 14 billion API transactions daily and require sovereign-grade API security governance. RBI's Account Aggregator framework security guidelines and SEBI's cybersecurity circular mandating API access controls are activating enterprise compliance procurement. Japan contributes 23.8% of APAC revenue at USD 302 Million, with METI's cybersecurity management guidelines and JFSA's IT governance inspections driving financial sector adoption. China represents 21.6% at USD 274 Million, with domestic API security platform vendors Hillstone Networks and Sangfor Technologies capturing significant share against global vendors subject to data localization constraints. Singapore accounts for 12.2% at USD 155 Million, functioning as the ASEAN API security technology hub.

Latin America API Security Platform Market

Latin America holds 6.2% of global API security platform revenue at USD 424 Million in 2025. Brazil dominates the regional market at 46.8% of LATAM revenue at USD 198 Million, driven by the Central Bank of Brazil's Open Finance (Open Banking) framework — which mandates API exposure for all Brazilian financial institutions with assets above BRL 1 Billion — creating the world's most comprehensive open banking API ecosystem outside the EU, with direct API security procurement implications for 1,200+ participating institutions. Bacen's Resolution 4,658 cybersecurity requirements and LGPD data protection enforcement are reinforcing API security investment across Brazilian technology companies and retailers. Mexico represents 27.4% of LATAM revenue at USD 116 Million, with CNBV's cybersecurity guidelines for financial institutions and the rapid growth of Mexican fintech companies building API-first financial services driving adoption. Colombia contributes 10.2% at USD 43 Million, with SFC cybersecurity guidance and Colombian fintech growth activating mid-market adoption.

Middle East & Africa API Security Platform Market

The Middle East and Africa region accounts for 4.4% of global API security platform revenue at USD 301 Million in 2025. The UAE leads regional demand at 36.2% of MEA revenue at USD 109 Million, with CBUAE's Open Finance framework establishing API security requirements for licensed financial institutions, DIFC's cybersecurity framework mandating API risk assessments, and Abu Dhabi's concentration of sovereign wealth fund technology platforms requiring enterprise API security governance. Saudi Arabia contributes 28.6% of MEA revenue at USD 86 Million, driven by SAMA's cybersecurity framework, Vision 2030 digital economy API infrastructure investment, and the Saudi National Cybersecurity Authority's (NCA) ECC-1:2018 controls mandating API security testing for government entities. South Africa represents 18.4% of MEA revenue at USD 55 Million, anchored by JSE-listed company cybersecurity governance requirements, SARB cybersecurity guidance for banks, and the POPIA enforcement environment. The regional market is constrained by cybersecurity skills gaps that limit internal API security program maturity and create dependence on managed security service providers for API threat monitoring.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Platform / Solution

- Professional Services

- Managed Security Services

By Deployment Mode

- Cloud-Based (SaaS)

- On-Premise

- Hybrid

By Security Type

- API Discovery & Inventory Management

- Authentication & Authorization Security

- API Threat Detection & Response

- Bot Mitigation & Rate Limiting

- API Posture Management

- Data Leakage & Sensitive Data Protection

- API Gateway Security

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By End-User Vertical

- Banking, Financial Services & Insurance (BFSI)

- Retail & E-Commerce

- Healthcare & Life Sciences

- Government & Defense

- Telecommunications

- Technology & SaaS

- Energy & Utilities

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.84 B |

| Forecast Revenue (2034) | USD 21.47 B |

| CAGR (2025-2034) | 13.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Platform / Solution, Professional Services, Managed Security Services ), By Deployment Mode (Cloud-Based (SaaS), On-Premise, Hybrid), By Security Type (API Discovery & Inventory Management, Authentication & Authorization Security, API Threat Detection & Response, Bot Mitigation & Rate Limiting, API Posture Management, Data Leakage & Sensitive Data Protection, API Gateway Security), By Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs)), By End-User Vertical (Banking, Financial Services & Insurance (BFSI), Retail & E-Commerce, Healthcare & Life Sciences, Government & Defense, Telecommunications, Technology & SaaS, Energy & Utilities) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PALO ALTO NETWORKS, AKAMAI TECHNOLOGIES (NONAME SECURITY), CROWDSTRIKE, SALT SECURITY, TRACEABLE AI, IMPERVA (THALES GROUP), F5 NETWORKS, FORTINET, BROADCOM (SYMANTEC), CLOUDFLARE, AWS (AMAZON WEB SERVICES), MICROSOFT AZURE API MANAGEMENT, GOOGLE CLOUD APIGEE, IBM SECURITY, 42CRUNCH, ESCAPE TECHNOLOGIES, STACKHAWK, WIBO GLOBAL, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-Based SaaS, On-Premise, Hybrid), By Security Type (API Discovery, Threat Detection, Authentication Security, Bot Mitigation, API Gateway Security, Data Leakage Protection), By Enterprise Size, By End-User Vertical, Industry Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based SaaS, On-Premise, Hybrid), By Security Type (API Discovery, Threat Detection, Authentication Security, Bot Mitigation, API Gateway Security, Data Leakage Protection), By Enterprise Size, By End-User Vertical, Industry Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based SaaS, On-Premise, Hybrid), By Security Type (API Discovery, Threat Detection, Authentication Security, Bot Mitigation, API Gateway Security, Data Leakage Protection), By Enterprise Size, By End-User Vertical, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the API Security Platform Market?

The Global API Security Platform Market was valued at USD 6.03 Billion in 2024 and is projected to reach USD 21.47 Billion by 2034, growing at a CAGR of 13.5% from 2026 to 2034, driven by rising API-based cyber threats, increasing adoption of cloud-native applications, and growing demand for zero-trust and AI-powered API security solutions.

Who are the major players in the API Security Platform Market?

PALO ALTO NETWORKS, AKAMAI TECHNOLOGIES (NONAME SECURITY), CROWDSTRIKE, SALT SECURITY, TRACEABLE AI, IMPERVA (THALES GROUP), F5 NETWORKS, FORTINET, BROADCOM (SYMANTEC), CLOUDFLARE, AWS (AMAZON WEB SERVICES), MICROSOFT AZURE API MANAGEMENT, GOOGLE CLOUD APIGEE, IBM SECURITY, 42CRUNCH, ESCAPE TECHNOLOGIES, STACKHAWK, WIBO GLOBAL, OTHERS

Which segments covered the API Security Platform Market?

By Component (Platform / Solution, Professional Services, Managed Security Services ), By Deployment Mode (Cloud-Based (SaaS), On-Premise, Hybrid), By Security Type (API Discovery & Inventory Management, Authentication & Authorization Security, API Threat Detection & Response, Bot Mitigation & Rate Limiting, API Posture Management, Data Leakage & Sensitive Data Protection, API Gateway Security), By Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs)), By End-User Vertical (Banking, Financial Services & Insurance (BFSI), Retail & E-Commerce, Healthcare & Life Sciences, Government & Defense, Telecommunications, Technology & SaaS, Energy & Utilities)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

API Security Platform Market

Published Date : 14 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date